Block Margarine Market Report By Type (Soft, Hard), By Nature (Organic, Conventional), By Distributional Channel (Online, Offline), By Application (Bakery, Confectionaries, Spreads, Households, Other applications), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46199

-

May 2024

-

321

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

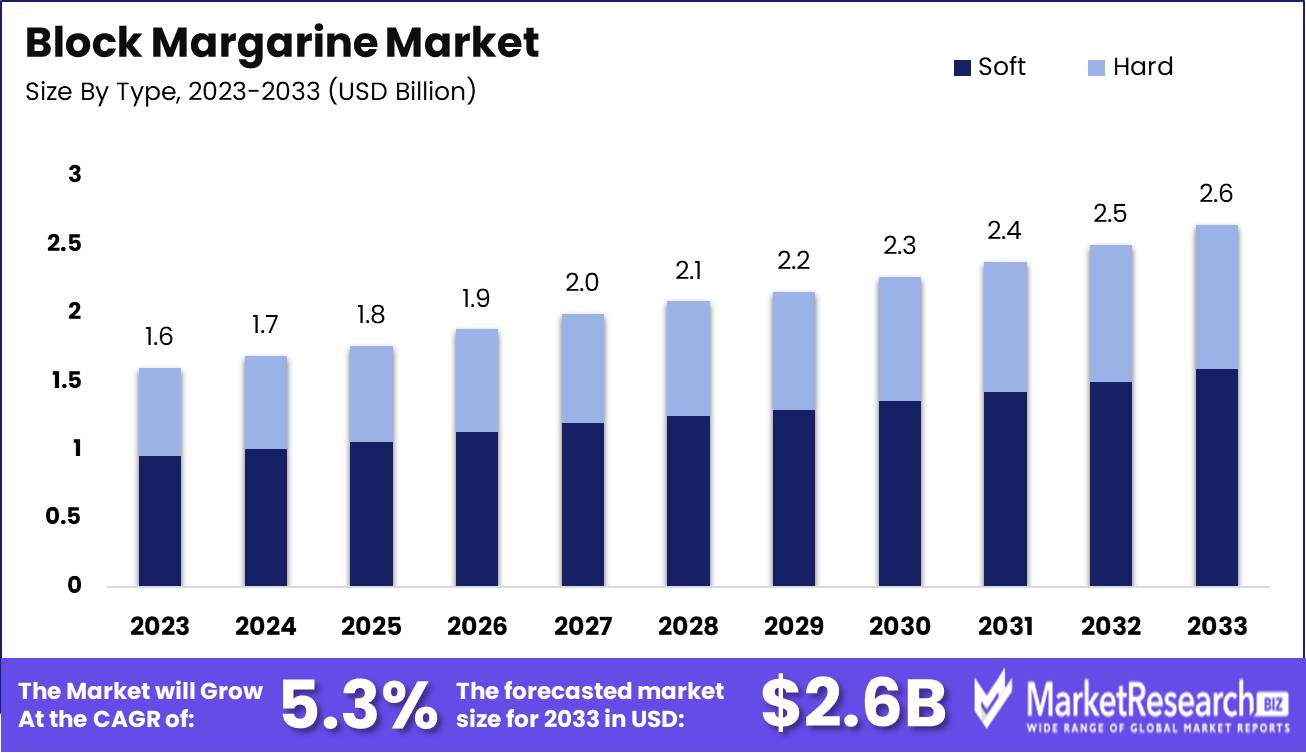

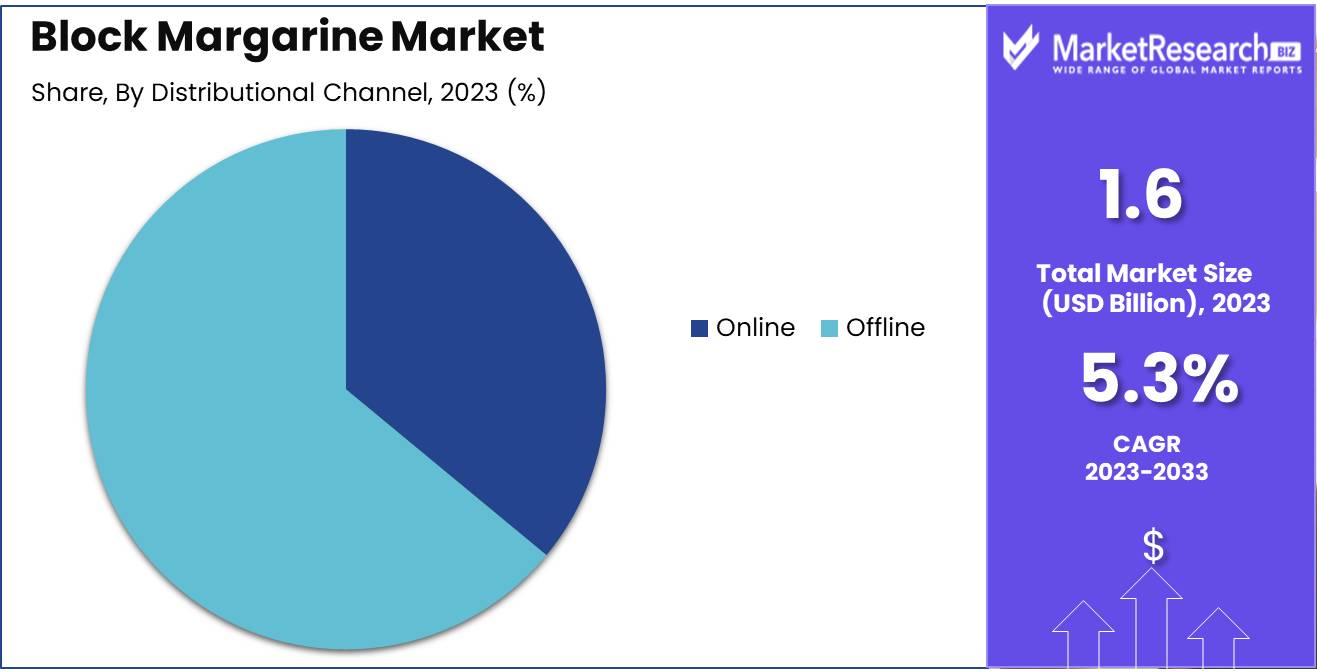

The Global Block Margarine Market size is expected to be worth around USD 2.6 billion by 2033, from USD 1.6 billion in 2023, growing at a CAGR of 5.3% during the forecast period from 2024 to 2033.

The Block Margarine Market encompasses the sector of the food industry specializing in the production and distribution of solid, block-shaped margarine products. These margarines are versatile substitutes for butter, favored for their convenience, spreadability, and lower cost.

The market is driven by shifting consumer preferences towards healthier alternatives, convenience foods, and plant-based options. Key players in this market focus on product innovation, quality assurance, and sustainable sourcing practices to meet evolving consumer demands and regulatory standards. Strategic partnerships, mergers, and acquisitions are common strategies employed to strengthen market position and expand distribution networks.

The Block Margarine Market is poised for steady growth in the coming years, driven by a combination of factors including shifting consumer preferences, dietary trends, and technological advancements in manufacturing processes. With global production of margarine estimated at approximately 9.5 million metric tons in 2021, the market showcases resilience and adaptability in meeting evolving consumer demands. The United States, Germany, Mexico, and Russia emerge as key players in margarine production, reflecting the market's global footprint and diverse supplier landscape.

High per capita consumption rates in countries such as Germany, Poland, and select African nations like Morocco underscore the widespread acceptance and usage of margarine as a versatile culinary ingredient and butter substitute.

Amidst changing dietary preferences and health-conscious consumer behaviors, manufacturers in the Block Margarine Market are innovating to offer healthier, plant-based alternatives, fortified with essential nutrients and free from trans fats. Additionally, advancements in production technologies are enhancing product quality, shelf life, and sensory attributes, further fueling market growth.

As the market continues to evolve, stakeholders must remain attuned to consumer preferences, regulatory developments, and competitive dynamics. Strategic investments in research and development, product diversification, and marketing initiatives will be crucial for companies seeking to capitalize on emerging growth opportunities and maintain a competitive edge in this dynamic landscape. Overall, the Block Margarine Market presents promising prospects for growth and innovation, underpinned by shifting consumer lifestyles and evolving market dynamics.

Key Takeaways

- Market Value: USD 1.6 billion in 2023; growing at a CAGR of 5.3%; expected to reach USD 2.6 billion by 2033.

- Type Analysis: Soft margarine dominates with 54.3%; widely used in baking due to its ease of use and versatility.

- Nature Analysis: Conventional margarine dominates; preferred for its availability and cost-effectiveness.

- Distribution Channel Analysis: Offline channels dominate with 64%; preferred for in-person purchases and promotional opportunities.

- Application Analysis: The bakery segment dominates with 34.3%; high demand for baked goods drives this segment.

- Dominant Region: APAC dominates with 38.6%; significant market share due to large consumer base and growing food industry.

- High Growth: North America; significant market presence with steady growth due to high consumption of margarine in baking and cooking.

- Analyst Viewpoint: The market is expected to grow steadily with moderate competition. Future predictions highlight growth in organic margarine and online distribution channels.

- Growth Opportunities: Key players can leverage opportunities in organic products, expand online presence, and innovate with new formulations to meet consumer preferences.

Driving Factors

Increasing Demand for Convenient and Cost-Effective Bakery Products Drives Market Growth

The Block Margarine Market is experiencing growth due to the increasing demand for convenient and cost-effective bakery products. Block margarine is a key ingredient in the production of various baked goods, including cakes, pastries, and bread. Consumers are increasingly seeking affordable and readily available baked items, which boosts the demand for block margarine. This trend is particularly evident in the rise of industrial bakeries and quick-service restaurants, which rely heavily on block margarine for their products.

For instance, the global bakery market is projected to reach USD 600 billion by 2025, growing at a CAGR of 3.9% from 2023 to 2032. This expansion fuels the demand for block margarine, as it is a cost-effective and versatile ingredient. Additionally, the shift towards home baking during the COVID-19 pandemic has also contributed to the increased demand for baking ingredients, including block margarine. As consumers continue to value convenience and cost-effectiveness, the block margarine market is expected to grow.

Versatility in Applications Drives Market Growth

The versatility of block margarine extends its applications beyond the bakery industry, significantly driving market growth. Block margarine is used in confectioneries, sauces, and spreads, making it a valuable functional ingredient across various food sectors. The food manufacturing industry's need for cost-effective and functional fats has increased the demand for block margarine.

For example, many snack food manufacturers use block margarine as a cost-effective alternative to butter or other premium fats. The global snack food market, valued at USD 450 billion in 2023, is expected to grow at a CAGR of 4.2% from 2024 to 2032. This growth in the snack food sector further boosts the demand for block margarine. Moreover, the dairy alternatives market, which includes margarine, is projected to reach USD 35 billion by 2027, growing at a CAGR of 10.5% from 2020 to 2027. The broad range of applications for block margarine ensures its continued demand and market expansion.

Advancements in Formulations and Health Considerations Drive Market Growth

Advancements in block margarine formulations and increasing health considerations are significant drivers of market growth. Manufacturers are continually improving block margarine to meet evolving consumer preferences and health concerns. The development of trans-fat-free and low-fat variants has opened up new market opportunities. Health-conscious consumers are increasingly seeking healthier alternatives, driving the demand for improved block margarine products.

For instance, the introduction of plant-based block margarines made from sustainable and healthy oils has gained traction. The global plant-based food market, which includes plant-based margarine, is projected to reach USD 74.2 billion by 2027, growing at a CAGR of 11.9% from 2020 to 2027. This shift towards healthier and more sustainable products significantly impacts the block margarine market. Additionally, regulatory changes and guidelines promoting healthier food options support the market's growth. The combination of improved formulations and health considerations ensures a positive outlook for the block margarine market.

Restraining Factors

Health Concerns and Negative Perceptions Restrain Market Growth

Health concerns and negative perceptions about block margarine limit its market growth. Despite improvements in formulations, some consumers remain wary of potential health risks. Margarine has been associated with trans fats and artificial ingredients, which are perceived as unhealthy. This perception drives consumers towards more natural alternatives like butter or plant-based oils.

Awareness of the potential health risks of trans fats has led many to reduce their intake of margarine-based products. For example, a study found that a 2% increase in trans fat consumption is associated with a 23% increase in cardiovascular disease risk. As a result, consumers are increasingly choosing healthier options, restraining the growth of the block margarine market.

Competition from Alternatives and Substitutes Restrains Market Growth

The block margarine market faces significant competition from alternatives like butter, plant-based oils, and other specialty fats. As consumer preferences shift towards healthier and more natural options, the demand for these alternatives has increased. The rise of plant-based diets and the popularity of vegan and vegetarian lifestyles further contribute to the demand for substitute products.

Additionally, the increasing use of olive oil and avocado oil in baking and cooking has impacted the demand for block margarine in certain consumer segments. This competition limits the growth potential of the block margarine market.

Type Analysis

Soft margarine dominates with 54.3% due to its wide application and ease of use in baking.

The block margarine market is segmented by type into soft and hard margarine. Soft margarine dominates the market with a significant share of 54.3%. This dominance is due to its wide application in both industrial and household baking. Soft margarine is preferred for its ease of use, spreadability, and ability to blend well with other ingredients, making it ideal for cakes, pastries, and bread. The market for soft margarine is driven by the growing demand for convenient and cost-effective baking solutions. Industrial bakeries and quick-service restaurants favor soft margarine for its consistency and functional properties, which enhance the texture and flavor of baked goods.

Hard margarine, while less dominant, plays a crucial role in the market. It is primarily used in professional baking and confectionery applications where a firmer texture is required. Hard margarine is valued for its stability at higher temperatures and its ability to create flakier pastries and pie crusts. Although it holds a smaller market share, hard margarine's demand is supported by its specialized applications in the food industry.

Nature Analysis

Conventional margarine dominates due to its widespread availability and cost-effectiveness.

The block margarine market is segmented by nature into organic and conventional margarine. Conventional margarine currently holds the majority share in the market. This segment's dominance is attributed to its widespread availability, cost-effectiveness, and longer shelf life. Conventional margarine is preferred by many consumers and food manufacturers due to its affordability and versatility. It is used extensively in commercial baking, food manufacturing, and household cooking, contributing to its large market share.

Organic margarine, while representing a smaller segment, is gaining traction as consumers become more health-conscious and environmentally aware. The demand for organic margarine is driven by the growing preference for natural and sustainably sourced ingredients. Organic margarine is free from synthetic additives and preservatives, appealing to consumers seeking healthier and more natural food options. The global organic food market, projected to reach USD 272.18 billion by 2027, supports the increasing demand for organic margarine. As consumer awareness and preference for organic products rise, this segment is expected to grow, although it currently lags behind conventional margarine.

Distribution Channel Analysis

Offline channels dominate with 64% due to consumer preference for in-person purchases and promotions.

The distribution channel analysis of the block margarine market reveals that the offline segment dominates with a 64% market share. Offline channels, including supermarkets, hypermarkets, and specialty stores, are the primary points of sale for block margarine. These retail outlets offer consumers the advantage of immediate purchase and the ability to compare products directly. The prominence of offline channels is driven by consumer preference for buying groceries and food products in person, where they can ensure product quality and freshness. Furthermore, offline stores often run promotions and discounts, attracting a larger customer base.

The online distribution channel, while currently smaller, is rapidly gaining importance. The convenience of online shopping, coupled with the increasing penetration of e-commerce platforms, is driving growth in this segment. Consumers appreciate the ease of ordering from home, extensive product variety, and doorstep delivery services. The COVID-19 pandemic has accelerated the shift towards online shopping, with many consumers opting for contactless purchasing options. The global e-commerce food and beverage market, expected to reach USD 71.62 billion by 2028, underscores the potential growth of the online segment in the block margarine market.

Application Analysis

The bakery segment dominates with 34.3% due to high demand for baked goods.

The block margarine market is segmented by application into bakery, confectioneries, spreads, households, and other applications. The bakery segment is the dominant sub-segment, holding a 34.3% market share. Block margarine's extensive use in baking drives this dominance. It is a crucial ingredient in cakes, pastries, bread, and other baked goods, offering the desired texture, flavor, and consistency. The demand for bakery products is high in both commercial and household settings, supporting the growth of this segment. The global bakery market, projected to reach USD 600 billion by 2025, reflects the strong demand for block margarine in this application.

Confectioneries, spreads, and household uses represent other significant segments. In confectioneries, block margarine is used for making various sweets and treats, contributing to the segment's growth. The spreads segment benefits from the versatility of margarine as a convenient and affordable alternative to butter. Households use block margarine for everyday cooking and baking, adding to its market presence. Other applications, though smaller in share, include its use in sauces and prepared foods, further diversifying the market's scope.

Key Market Segments

By Type

- Soft

- Hard

By Nature

- Organic

- Conventional

By Distributional Channel

- Online

- Offline

By Application

- Bakery

- Confectionaries

- Spreads

- Households

- Other applications

Growth Opportunities

Product Innovation and Formulation Improvements Offer Growth Opportunity

Product innovation and formulation improvements present significant growth opportunities in the block margarine market. Manufacturers can address evolving consumer preferences and health concerns by developing products with enhanced nutritional profiles. For example, block margarines with healthier oils, reduced trans fats, or fortified with essential vitamins and minerals can attract health-conscious consumers.

The introduction of block margarines enriched with plant-based omega-3 fatty acids or vitamins can appeal to those seeking functional food products. This focus on health benefits aligns with the increasing demand for healthier food options. The global functional food market is projected to reach USD 275.77 billion by 2025, growing at a CAGR of 7.9% from 2020 to 2025. By leveraging innovation, manufacturers can tap into this expanding market, driving growth and capturing new consumer segments.

Sustainable and Ethical Sourcing Offers Growth Opportunity

Sustainable and ethical sourcing offers a significant growth opportunity in the block margarine market. Consumers are increasingly aware of the environmental and social impacts of their purchases. Manufacturers can differentiate their products by emphasizing sustainable and ethical sourcing practices. This includes using responsibly sourced and sustainably produced ingredients, eco-friendly manufacturing processes, and promoting fair trade and ethical labor practices.

Brands that use sustainably sourced palm oil or other plant-based oils can resonate with environmentally conscious consumers. By addressing these concerns, manufacturers can appeal to a broader consumer base and gain a competitive advantage in the market.

Trending Factors

Clean Label and Transparency Trends Are Trending Factors

Clean label and transparency trends are driving growth in the block margarine market. Consumers are increasingly demanding simple, transparent ingredient lists and fewer artificial additives. Manufacturers respond by offering block margarines with clean labels, featuring recognizable and natural ingredients.

Transparent labeling that details product ingredients and nutritional content appeals to health-conscious consumers. For instance, brands that highlight the use of simple, recognizable ingredients and provide clear labeling resonate with consumers seeking clean and transparent food products. This trend emphasizes the importance of transparency and simplicity in driving consumer preference and market growth.

Plant-Based and Vegan Alternatives Are Trending Factors

The increasing popularity of plant-based diets and veganism is a significant trend in the block margarine market. There is growing demand for plant-based and vegan-friendly alternatives to traditional dairy-based products. Manufacturers have the opportunity to develop block margarines made from plant-based oils and free from animal-derived ingredients.

Offering vegan-certified block margarines caters to this expanding consumer segment. For example, block margarines made from coconut oil or other plant-based sources appeal to consumers following a vegan or plant-based lifestyle. This trend highlights the shift towards plant-based products and the potential for market expansion.

Regional Analysis

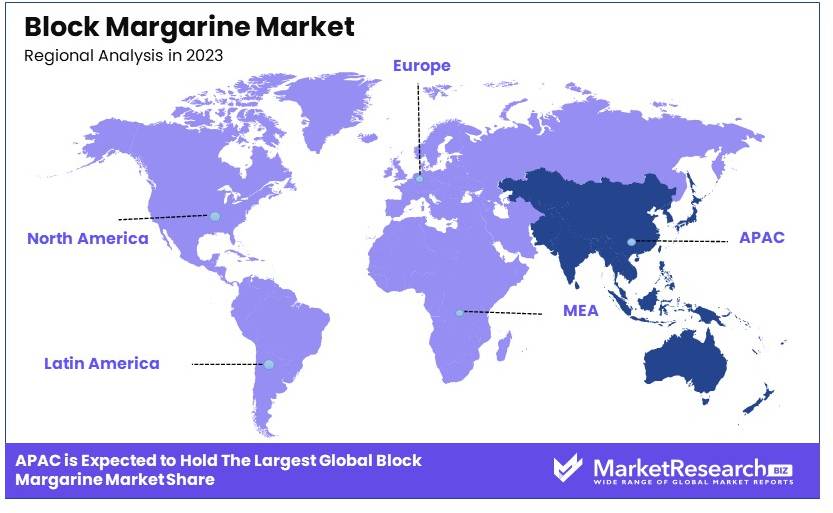

APAC Dominates with 38.6% Market Share

The Asia-Pacific (APAC) region leads the block margarine market with a 38.6% market share. This dominance is driven by several key factors.

High population density and growing urbanization in countries like China and India boost the demand for convenient and affordable food products, including block margarine. The rise in disposable incomes and changing dietary habits further support market growth. Additionally, the expanding food processing industry and increasing number of bakeries and quick-service restaurants in the region contribute significantly to the demand for block margarine.

APAC's diverse culinary traditions and the increasing adoption of Western-style baking influence the block margarine market positively. The region's large base of cost-sensitive consumers favors block margarine over more expensive alternatives. Furthermore, government initiatives promoting the food processing sector and favorable trade policies enhance the market environment. For instance, the food processing industry in India is expected to grow at a CAGR of 11.0% from 2020 to 2025, driving the demand for block margarine.

North America Market Share and Growth Rate

North America holds a significant share of the block margarine market, driven by high consumer awareness and preference for healthier food options. The market in this region is projected to grow at a CAGR of 3.5% from 2020 to 2025. The emphasis on clean label products and the increasing demand for plant-based alternatives contribute to this growth.

Europe Market Share and Growth Rate

Europe accounts for a substantial market share, supported by the region's well-established food processing industry and strong demand for bakery products. The European market is expected to grow at a CAGR of 4.2% from 2020 to 2025. The trend towards sustainable and organic food products further drives the demand for block margarine in Europe.

Middle East & Africa Market Share and Growth Rate

The Middle East & Africa region holds a smaller share of the block margarine market but shows potential for growth. The market is expected to grow at a CAGR of 4.5% from 2020 to 2025, driven by the rising demand for bakery products and the increasing influence of Western dietary habits.

Latin America Market Share and Growth Rate

Latin America has a growing market share in the block margarine industry, supported by the expanding food and beverage sector. The market in this region is projected to grow at a CAGR of 3.8% from 2020 to 2025. The increasing popularity of convenience foods and the rise of quick-service restaurants contribute to the market's growth in Latin America.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Block Margarine Market, Unilever and Bunge Limited stand out as leading players, leveraging their extensive distribution networks and brand strength to dominate the market. Together with Upfield and Conagra Brands, Inc., these companies influence market trends through their commitment to innovation and consumer-focused products.

Unilever, in particular, benefits from strong brand recognition and a diverse product portfolio that meets various consumer needs, from baking to general cooking uses. Bunge's strategic focus on expanding its footprint in emerging markets significantly impacts its market position and growth potential.

Arla Foods and Associated British Foods plc emphasize their product quality and the integration of sustainable practices, appealing to health-conscious consumers and those valuing environmental stewardship.

Wilmar International Ltd. and Fuji Oil Holdings Inc. focus on the Asian markets, bringing regional preferences into their product development, which enhances their competitiveness in these areas.

Smaller players like Royal Smilde Foods and Vandemoortele are crucial for their specialized offerings and regional market penetration, especially in Europe, where traditional tastes favor block margarine varieties.

The competitive landscape in the Block Margarine Market is defined by a mix of global giants and regional specialists, each contributing to the industry’s dynamics through strategic innovation, market expansion, and responsiveness to consumer preferences.

Market Key Players

- Unilever

- Bunge Limited

- Arla Foods

- Wilmar International Ltd.

- Conagra Brands, Inc.

- Royal Smilde Foods

- Upfield

- Fuji Oil Holdings Inc.

- Associated British Foods plc

- NMGK Group

- EPM Group

- Ventura Foods, LLC

- Puratos Group

- Vandemoortele

- Mewah International Inc.

Recent Developments

- On April 2024, UK-based spread company Flora announced the removal of dairy from its entire range of spreads, making them all vegan-friendly. This change aligns with Flora's commitment to a plant-based future and follows the parent company Upfield's goal to make all its brands vegan by 2025.

- Inflation has significantly impacted the prices of butter and margarine, with prices soaring by 31% and 44% respectively in December compared to the previous year. Factors contributing to this surge include supply disruptions due to the Russian invasion of Ukraine affecting margarine production and a decrease in milk supply for butter production.

- On October 2023, CSM Ingredients inaugurated a new margarine production line at its facility in Crema, Italy, coinciding with the plant's 100th anniversary celebration. This new production line enhances the facility's capacity to over 70,000 tons per year and underscores CSM's commitment to sustainable and innovative food production.

Report Scope

Report Features Description Market Value (2023) USD 1.6 Billion Forecast Revenue (2033) USD 2.6 Billion CAGR (2024-2033) 5.3% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Soft, Hard), By Nature (Organic, Conventional), By Distributional Channel (Online, Offline), By Application (Bakery, Confectionaries, Spreads, Households, Other applications) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Unilever, Bunge Limited, Arla Foods, Wilmar International Ltd., Conagra Brands, Inc., Royal Smilde Foods, Upfield, Fuji Oil Holdings Inc., Associated British Foods plc, NMGK Group, EPM Group, Ventura Foods, LLC, Puratos Group, Vandemoortele, Mewah International Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Unilever

- Bunge Limited

- Arla Foods

- Wilmar International Ltd.

- Conagra Brands, Inc.

- Royal Smilde Foods

- Upfield

- Fuji Oil Holdings Inc.

- Associated British Foods plc

- NMGK Group

- EPM Group

- Ventura Foods, LLC

- Puratos Group

- Vandemoortele

- Mewah International Inc.

Our Clients

View Our Licence Options