Bacille Calmette-Guerin Vaccine Market By Age Group (Pediatrics, Adults), By Application (Tuberculosis, Bladder cancer), By End-use (Hospitals, Clinics), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

50901

-

September 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

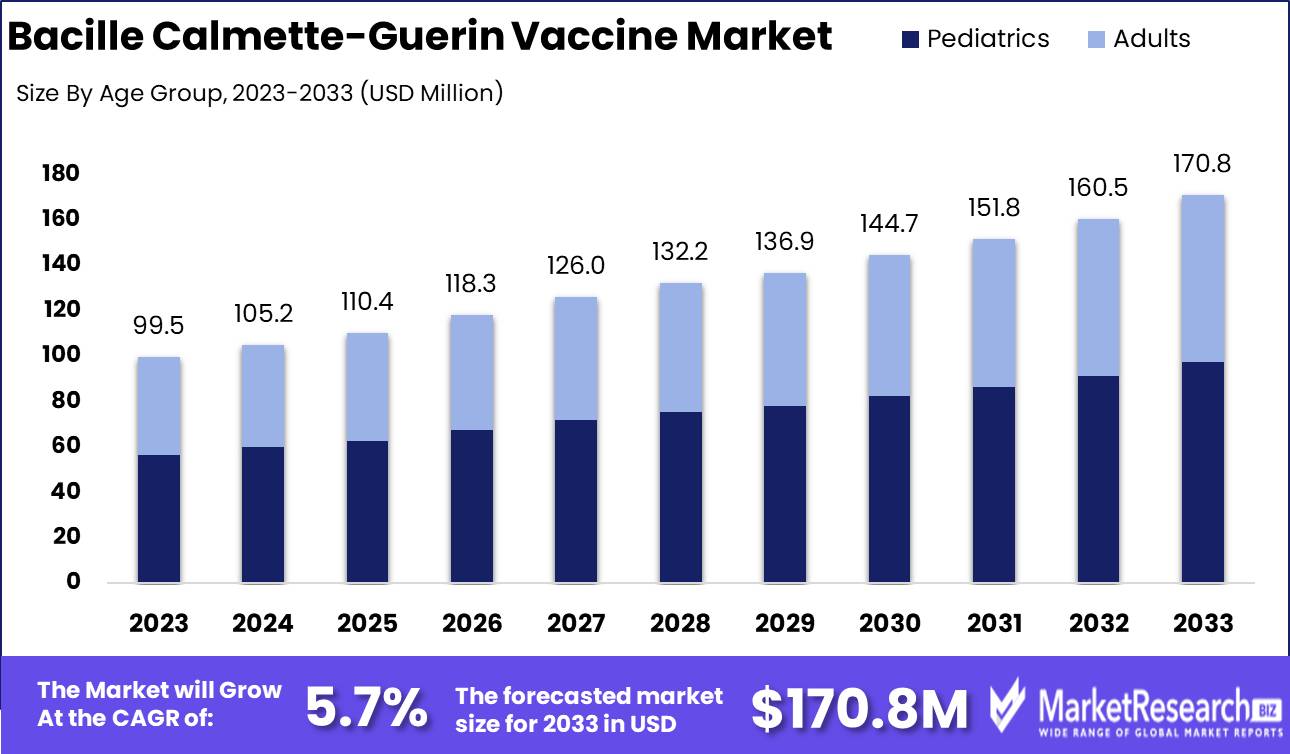

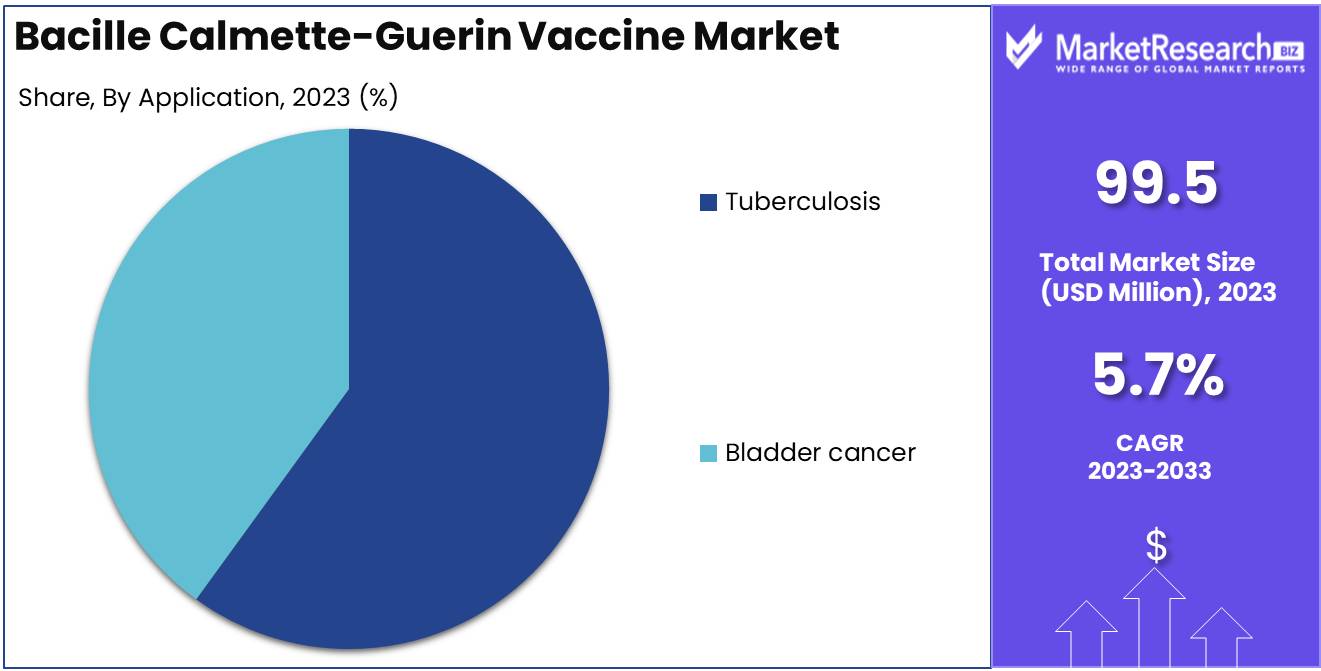

The Bacille Calmette-Guerin Vaccine Market was valued at USD 99.5 million in 2023. It is expected to reach USD 170.8 million by 2033, with a CAGR of 5.7% during the forecast period from 2024 to 2033.

The Bacille Calmette-Guerin (BCG) vaccine market encompasses the development, production, and distribution of vaccines designed to protect against tuberculosis (TB). BCG vaccines, derived from a weakened strain of Mycobacterium bovis, are primarily utilized to prevent severe forms of TB in infants and young children, particularly in regions with high TB incidence. This market includes various vaccine formulations and delivery systems, influenced by factors such as global TB prevalence, vaccination policies, and technological advancements in vaccine production.

The Bacille Calmette-Guérin (BCG) vaccine market is poised for notable evolution, driven by several converging factors. Analysts observe a significant increase in the incidence of tuberculosis (TB) worldwide, particularly in regions with high disease burden. This rising prevalence underscores the critical need for effective vaccination strategies, thereby bolstering demand for BCG vaccines.

Moreover, the growing global awareness and expansion of vaccination programs are expected to further stimulate market growth. Governments and health organizations are intensifying efforts to educate the public and expand immunization initiatives, which is anticipated to positively impact vaccine uptake.

However, the market's trajectory is not without challenges. Issues related to vaccine supply and distribution persist, potentially constraining access and affecting overall market performance. Despite these challenges, the BCG vaccine market is on a positive growth trajectory. The combined effect of increasing TB incidence, enhanced awareness, and ongoing vaccination programs provides a robust foundation for market expansion. Analysts predict that addressing supply chain issues and leveraging advancements in vaccine technology will be crucial for sustaining growth and meeting global health objectives. Consequently, the BCG vaccine market is set to experience sustained growth, supported by both rising demand and concerted efforts to overcome existing obstacles.

Key Takeaways

- Market Growth: The Bacille Calmette-Guerin Vaccine Market was valued at USD 99.5 million in 2023. It is expected to reach USD 140.0 million by 2033, with a CAGR of 5.7% during the forecast period from 2024 to 2033.

- By Age Group: Pediatrics dominated the BCG vaccine market, driven by preventive needs.

- By Application: Tuberculosis dominated the BCG vaccine market, driven by prevalence.

- By End-use: Hospitals dominated the BCG vaccine market, followed by clinics.

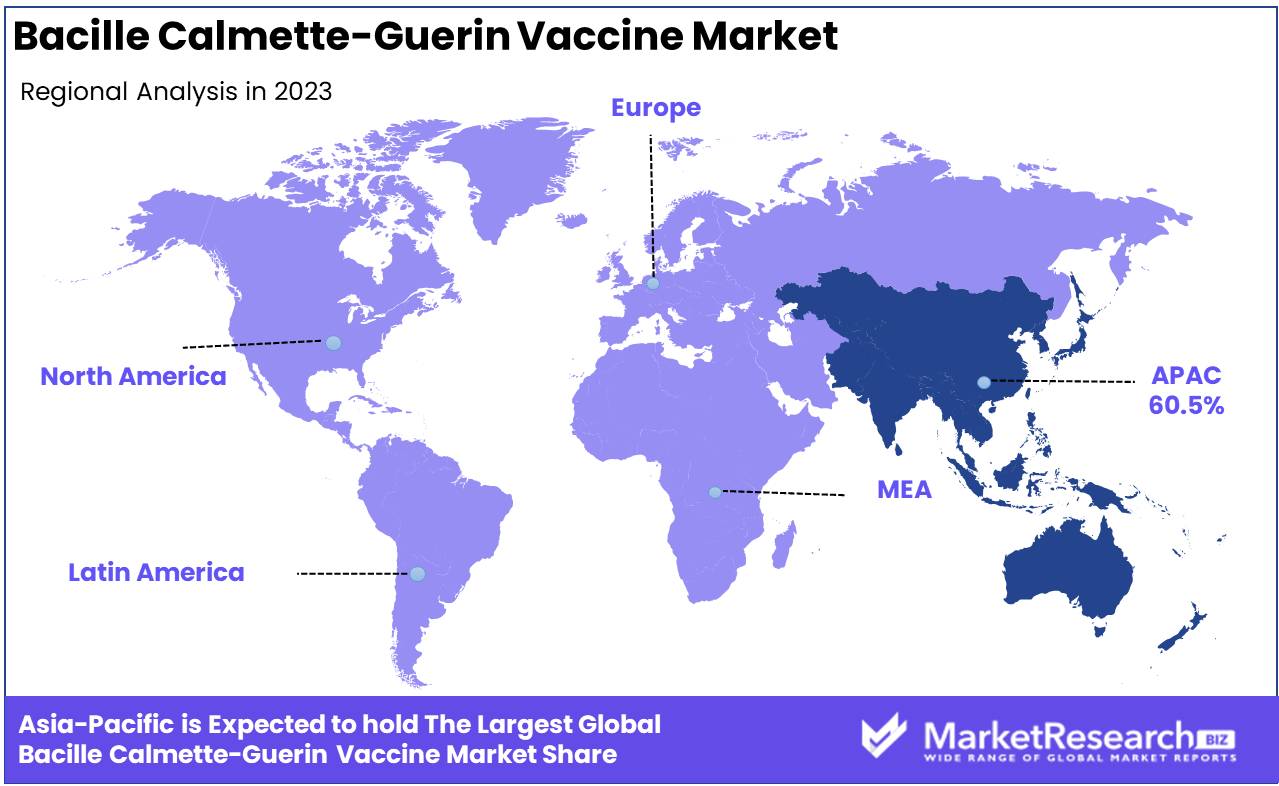

- Regional Dominance: Asia Pacific dominates the BCG vaccine market with a 60.5% largest share.

- Growth Opportunity: The global BCG vaccine market is set to grow due to expanded use in bladder cancer treatment and improved manufacturing processes, enhancing availability and therapeutic efficacy.

Driving factors

Global Initiatives to Combat Tuberculosis (TB)

Global initiatives aimed at combating tuberculosis (TB) significantly influence the Bacille Calmette-Guerin (BCG) vaccine market. The World Health Organization (WHO) and various global health organizations have intensified efforts to address the persistent burden of TB, which remains one of the top ten causes of death worldwide. These initiatives often include large-scale vaccination campaigns, increased funding for TB control programs, and collaborative efforts between governments and non-governmental organizations.

According to the WHO, an estimated 10 million people fell ill with TB in 2021, demonstrating the critical need for effective vaccination strategies. The focus on TB eradication has driven demand for the BCG vaccine, which is a cornerstone of preventive measures against the disease. The increased investment in TB prevention programs and the promotion of the BCG vaccine contribute to market growth by expanding vaccination coverage and raising awareness about TB control.

Government Immunization Programs

Government immunization programs are pivotal in driving the growth of the BCG vaccine market. Many countries have integrated BCG vaccination into their routine immunization schedules, particularly in regions with high TB prevalence. These programs are designed to provide widespread vaccine access and ensure that populations at risk are adequately protected.

For instance, in countries like India and Bangladesh, where TB incidence rates are high, the BCG vaccine is administered as part of the national immunization program. Such programs not only increase vaccine uptake but also create a steady demand for BCG vaccines. Government-led initiatives often include financial subsidies, distribution logistics, and public health campaigns, all of which contribute to market expansion. The reliance on government programs for vaccine distribution and administration underscores the significant role these initiatives play in the overall growth of the BCG vaccine market.

Advancements in Vaccine Manufacturing Technologies

Advancements in vaccine manufacturing technologies play a crucial role in shaping the BCG vaccine market. Innovations such as improved production processes, enhanced quality control, and the development of more efficient vaccine formulations contribute to market growth by making the vaccine more accessible and affordable.

Recent technological developments in vaccine production have led to increased production capacities and reduced costs. For example, the adoption of modern biotechnological methods and automated production systems has streamlined vaccine manufacturing, resulting in higher output and better quality control. These advancements not only help meet the growing global demand for BCG vaccines but also facilitate the entry of new players into the market, fostering competition and driving further innovation.

Restraining Factors

Supply Concentration and Its Impact on Market Stability

Supply Concentration within the Bacille Calmette-Guerin (BCG) vaccine market is a critical restraining factor that influences market dynamics and growth potential. The production of BCG vaccines is concentrated in a few key manufacturers, which can lead to supply chain vulnerabilities. When production is dominated by a small number of companies, the market becomes susceptible to disruptions due to manufacturing issues, geopolitical tensions, or economic fluctuations affecting these suppliers. For instance, if a major supplier faces production delays or quality control problems, the overall availability of BCG vaccines may be significantly impacted, leading to shortages and higher prices.

This concentration can also hinder market expansion as new entrants find it challenging to compete with established players who control a substantial share of the supply. Furthermore, the reliance on a few suppliers can result in reduced bargaining power for buyers, limiting their ability to negotiate prices and terms. Consequently, this supply concentration can slow down market growth by constraining the distribution network and increasing market volatility.

Limited Product Registration and Market Expansion

Limited Product Registration is another significant factor impacting the Bacille Calmette-Guerin vaccine market. The approval and registration of vaccines are stringent processes that vary from one region to another, affecting how quickly new BCG vaccines can enter the market. Regulatory barriers and extended approval times can delay the introduction of new formulations or production innovations, thereby restricting market growth.

For example, if new BCG vaccine products are not promptly registered or face regulatory hurdles, the market may experience slower adoption rates and limited availability of advanced vaccine options. This limitation can prevent the expansion of the market in regions with high demand or where regulatory processes are particularly rigorous. Additionally, the complexity and cost of navigating different regulatory environments can deter potential new entrants, further consolidating the market and potentially stifling innovation.

By Age Group Analysis

In 2023, Pediatrics dominated the BCG vaccine market, driven by preventive needs.

In 2023, The Pediatrics segment held a dominant market position in the Bacille Calmette-Guerin (BCG) Vaccine Market, specifically within the Age Group segment. This preeminence can be attributed to the heightened focus on tuberculosis prevention in infants and children, as the BCG vaccine is traditionally administered shortly after birth. The prevalence of tuberculosis in pediatric populations, coupled with the vaccine's established efficacy in reducing severe forms of the disease, underpins the significant demand for BCG vaccination in this age group. Governments and health organizations globally continue to endorse the use of BCG for pediatric immunization, contributing to the segment's substantial market share.

Conversely, the Adult segment, while smaller in market share compared to Pediatrics, also plays a crucial role in the BCG vaccine market. The demand within this segment primarily stems from the use of BCG for therapeutic purposes in adult patients with bladder cancer, where it has shown efficacy in reducing cancer recurrence. Although not as predominant as the Pediatric segment, the Adult segment's growth is supported by continued research and the expanding application of BCG in oncology. The market dynamics for adults reflect a more specialized use case, emphasizing the vaccine's versatility and its evolving role in medical treatments beyond tuberculosis prevention.

By Application Analysis

In 2023, Tuberculosis dominated the BCG vaccine market, driven by prevalence.

In 2023, Tuberculosis held a dominant market position in the application segment of the Bacille Calmette-Guerin (BCG) Vaccine Market. Tuberculosis, a persistent global health issue, continues to drive the demand for BCG vaccines due to its high prevalence in both developing and developed regions. The efficacy of BCG vaccines in preventing tuberculosis, particularly in children and individuals with a high risk of exposure, has cemented their essential role in public health strategies. The World Health Organization (WHO) emphasizes BCG vaccination as a critical component of tuberculosis control programs, further bolstering its market presence. Additionally, ongoing initiatives to enhance tuberculosis diagnosis and treatment, along with governmental support for vaccination programs, contribute to the sustained demand for BCG vaccines.

Conversely, the Bladder Cancer application segment also represents a significant portion of the BCG vaccine market. BCG therapy is a standard treatment for superficial bladder cancer, which has been demonstrated to reduce recurrence rates and improve patient outcomes. The growing incidence of bladder cancer, coupled with the effectiveness of BCG as an intravesical treatment, continues to drive market growth in this segment. The increasing adoption of BCG therapy, alongside advancements in treatment protocols and patient management, underscores its vital role in bladder cancer care.

By End-use Analysis

In 2023, Hospitals dominated the BCG vaccine market, followed by clinics.

In 2023, Hospitals held a dominant market position in the end-use segment of the Bacille Calmette-Guérin (BCG) vaccine market. The prevalence of hospitals as the primary end-users can be attributed to their extensive infrastructure and capacity to manage a high volume of vaccinations. Hospitals offer a comprehensive range of services, including diagnostic and therapeutic interventions, which makes them a central hub for BCG vaccination programs, especially in regions with high tuberculosis (TB) incidence. Additionally, the integration of BCG vaccination within hospital settings facilitates efficient patient management and follow-up care, contributing to better overall health outcomes.

Conversely, clinics have also emerged as significant players in the BCG vaccine market, albeit with a different emphasis. Clinics, particularly those focused on primary care and preventive medicine, contribute to the market by offering accessible vaccination services to diverse populations. Their role is increasingly crucial in areas where hospitals may not be as readily available. Clinics provide personalized patient care and often serve as the first point of contact for vaccination, thereby supporting public health initiatives and ensuring widespread BCG vaccine coverage.

Key Market Segments

By Age Group

- Pediatrics

- Adults

By Application

- Tuberculosis

- Bladder cancer

By End-use

- Hospitals

- Clinics

Growth Opportunity

Expanding BCG Vaccine Usage for Bladder Cancer Treatment

The Bacille Calmette-Guerin (BCG) vaccine, traditionally utilized for tuberculosis (TB) prevention, is experiencing an expanded role in oncology, particularly in bladder cancer treatment. The therapeutic use of BCG in treating non-muscle invasive bladder cancer (NMIBC) has shown significant efficacy. The market opportunity is amplified by increasing adoption rates of BCG as a standard of care in bladder cancer management. Clinical studies continue to validate the benefits of BCG in reducing recurrence rates and improving patient outcomes, driving higher demand for the vaccine. This shift towards oncological applications provides a substantial growth opportunity, as healthcare providers seek effective treatments amid rising bladder cancer incidences.

Improving BCG Vaccine Manufacturing Processes

Advancements in BCG vaccine manufacturing processes are further poised to enhance market prospects. Innovations aimed at improving the production efficiency and quality control of BCG vaccines are expected to address supply chain constraints and reduce production costs. Enhanced manufacturing techniques are anticipated to bolster the availability of BCG vaccines globally, ensuring consistent supply to meet growing demand. Additionally, improvements in vaccine formulation and stabilization techniques contribute to longer shelf life and better vaccine performance, which is critical for both TB prevention and bladder cancer treatment.

Latest Trends

Expanding BCG Vaccine Usage for Bladder Cancer Treatment

The Bacille Calmette-Guerin (BCG) vaccine, historically used for tuberculosis prevention, is experiencing a notable shift in its application towards bladder cancer treatment. In recent years, there has been a growing body of evidence supporting the efficacy of BCG therapy for non-muscle invasive bladder cancer (NMIBC). This development is driven by its immunotherapeutic benefits, which have been shown to significantly reduce recurrence rates and improve patient outcomes. As clinical research continues to validate these findings, the use of BCG in oncology is anticipated to expand. This trend is likely to stimulate market growth as healthcare providers and institutions increasingly adopt BCG for bladder cancer management. The expanding use of BCG in this new therapeutic context reflects a broader trend toward repurposing existing vaccines for innovative treatments, a development that may open new revenue streams for manufacturers.

Improving BCG Vaccine Manufacturing Processes

Another significant trend in the BCG vaccine market is the enhancement of manufacturing processes. Historically, the production of BCG vaccines has been characterized by challenges related to consistency and scalability. However, advancements in biotechnological techniques and the implementation of more refined quality control measures are addressing these issues. Innovations such as improved fermentation technologies and optimized formulation processes are expected to enhance the efficiency and reliability of BCG vaccine production. These improvements are poised to address supply chain constraints and meet the growing demand driven by its expanded use in cancer therapy. As manufacturing processes become more streamlined, the overall market for BCG vaccines is anticipated to experience a period of stability and growth, driven by both increased demand and enhanced production capabilities.

Regional Analysis

Asia Pacific dominates the BCG vaccine market with a 60.5% largest share.

The global Bacille Calmette-Guerin (BCG) vaccine market demonstrates significant regional variations, influenced by differing healthcare infrastructures, tuberculosis prevalence, and vaccination policies. As of the latest data, the Asia Pacific region leads the market, commanding approximately 60.5% of the global share. This dominance is attributed to the high incidence of tuberculosis and robust public health initiatives in countries such as India and China, where BCG vaccination remains a critical component of national immunization programs.

In North America, the BCG vaccine market holds a smaller share due to the lower incidence of tuberculosis and the preference for targeted therapy over widespread vaccination. The market is relatively stable, with the United States accounting for the majority of this region's demand. However, advancements in vaccine technology and public health policies continue to influence market dynamics.

Europe represents a diverse landscape with varying levels of BCG vaccine adoption. Countries with higher tuberculosis rates, such as Eastern European nations, exhibit higher market shares compared to Western Europe. The region’s market is also shaped by the European Union's health policies and funding for vaccination programs.

The Middle East & Africa show a growing market potential driven by increasing healthcare access and rising tuberculosis cases in specific countries. Despite challenges in healthcare infrastructure, efforts to enhance vaccination coverage are contributing to gradual market growth.

Latin America, while smaller in market share compared to Asia Pacific, is experiencing steady growth. Countries in this region are bolstering vaccination efforts in response to regional health challenges, thus influencing the market dynamics.

Overall, the Asia Pacific region’s dominance, supported by its substantial share of 60.5%, underscores its pivotal role in the global BCG vaccine market.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global Bacille Calmette-Guerin (BCG) vaccine market is characterized by a diverse array of key players, each contributing uniquely to the sector's dynamics.

Merck & Co., Inc. continues to dominate the market due to its extensive research and development capabilities and robust distribution network. The company's established reputation and global reach afford it a significant competitive advantage, enabling it to maintain a substantial market share. Sanofi, another major player, leverages its comprehensive portfolio and advanced manufacturing capabilities. Its strategic focus on enhancing vaccine accessibility in emerging markets complements its established presence in developed regions, thereby broadening its market footprint.

China National Group Corporation (Sinopharm) stands out for its significant contributions to vaccine production and distribution in China and other regions. The company’s strong governmental ties and expansive distribution network facilitate its prominent role in the market. Serum Institute of India Pvt. Ltd. is noted for its large-scale production capacity and cost-effective pricing strategies. This positions it as a key supplier in developing countries, where affordability and availability are critical.

Interfax Ltd. and BCG Vaccine Laboratory are recognized for their specialized focus on BCG vaccines, contributing to innovation and quality assurance within the market. Similarly, Japan BCG Laboratory and Torlak Institute of Virology are important regional players with expertise in BCG vaccine development and production. Other notable contributors, such as AJ Biologics Sdn Bhd, Biomed Lublin S.A., GSBPL, Microgen, Stevens Serum Institute, Taj Pharmaceuticals Limited, and Zydus Group, enhance the competitive landscape through their unique technological advancements and regional strengths.

The competitive landscape of the BCG vaccine market is marked by a blend of established multinational corporations and specialized regional players, each driving growth through innovation, strategic positioning, and market expansion.

Market Key Players

- AJ Biologics Sdn Bhd

- BCG Vaccine Laboratory

- Biomed Lublin S.A.

- China National Group Corporation (Sinopharm)

- GSBPL

- Intervax Ltd.

- Japan BCG Laboratory

- Merck & Co., Inc.

- Microgen

- Sanofi

- Serum Institute of India Pvt. Ltd.

- Stetens Serum Institute

- Taj Pharmaceuticals Limited

- Torlak Institute of Virology

- Zydus Group

Recent Development

- In June 2024, The University of Oxford published results from a clinical trial investigating a modified BCG vaccine with improved efficacy for tuberculosis (TB). The trial demonstrated enhanced immune response and protection against TB, potentially leading to an updated formulation with broader applicability.

- In March 2024, The Serum Institute of India announced a partnership with the World Health Organization to enhance the global supply of the BCG vaccine. This collaboration aims to address the supply shortages in low and middle-income countries and ensure a consistent and reliable distribution of the vaccine.

- In January 2024, UroGen Pharma received FDA approval for a new formulation of the BCG vaccine specifically for the treatment of bladder cancer. This approval expands the therapeutic use of the vaccine and offers a potentially more effective treatment option for patients with high-risk non-muscle invasive bladder cancer.

Report Scope

Report Features Description Market Value (2023) USD 99.5 Million Forecast Revenue (2033) USD 170.8 Million CAGR (2024-2032) 5.7% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Age Group (Pediatrics, Adults), By Application (Tuberculosis, Bladder cancer), By End-use (Hospitals, Clinics) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape AJ Biologics Sdn Bhd, BCG Vaccine Laboratory, Biomed Lublin S.A., China National group corporation (Sinopharm), GSBPL, Intervax Ltd., Japan BCG Laboratory, Merck & Co., Inc., Microgen, Sanofi, Serum Institute of India Pvt. Ltd., Stetens Serum Institute, Taj Pharmaceuticals Limited, Torlak Institute of Virology, Zydus Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- AJ Biologics Sdn Bhd

- BCG Vaccine Laboratory

- Biomed Lublin S.A.

- China National Group Corporation (Sinopharm)

- GSBPL

- Intervax Ltd.

- Japan BCG Laboratory

- Merck & Co., Inc.

- Microgen

- Sanofi

- Serum Institute of India Pvt. Ltd.

- Stetens Serum Institute

- Taj Pharmaceuticals Limited

- Torlak Institute of Virology

- Zydus Group

Our Clients

View Our Licence Options