Achondroplasia Market By Treatment (Surgery, Growth Hormone Therapy, Supportive Therapy, Vosoritide), By Route of Administration (Oral, Parenteral), By End-User (Hospitals & Clinics, Homecare, Speciality Centers, Other), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

38274

-

April 2024

-

285

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

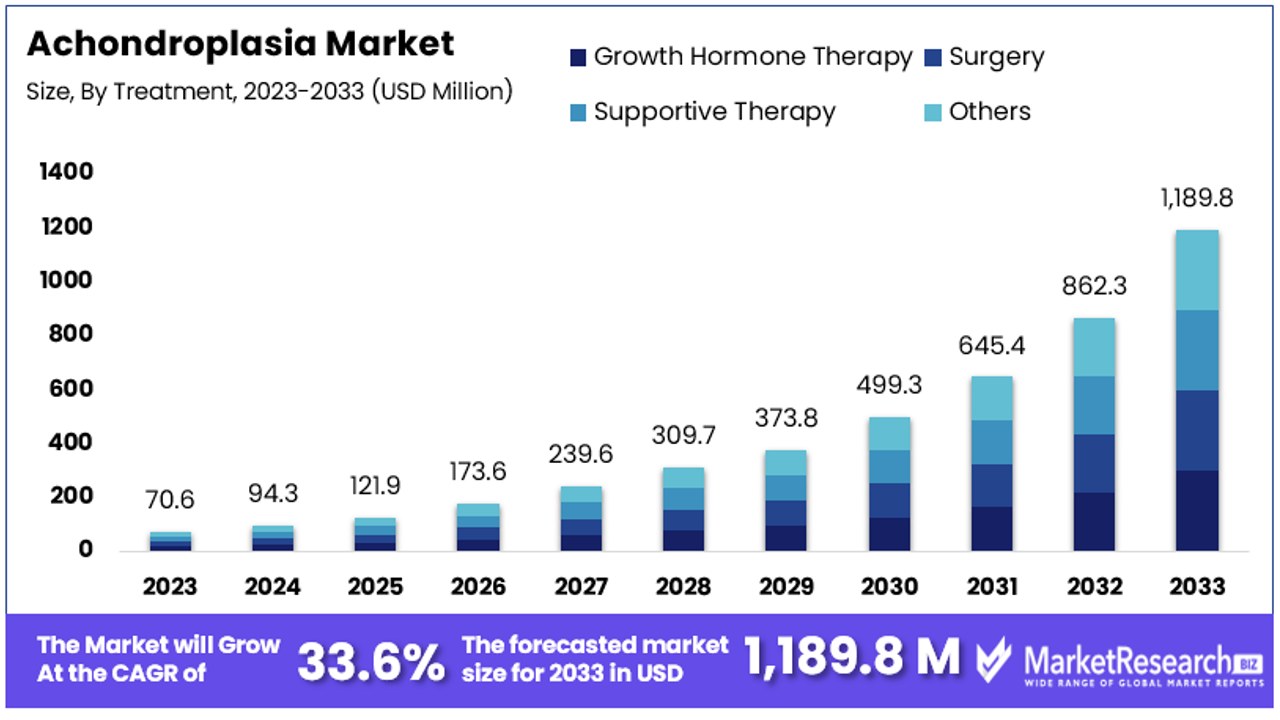

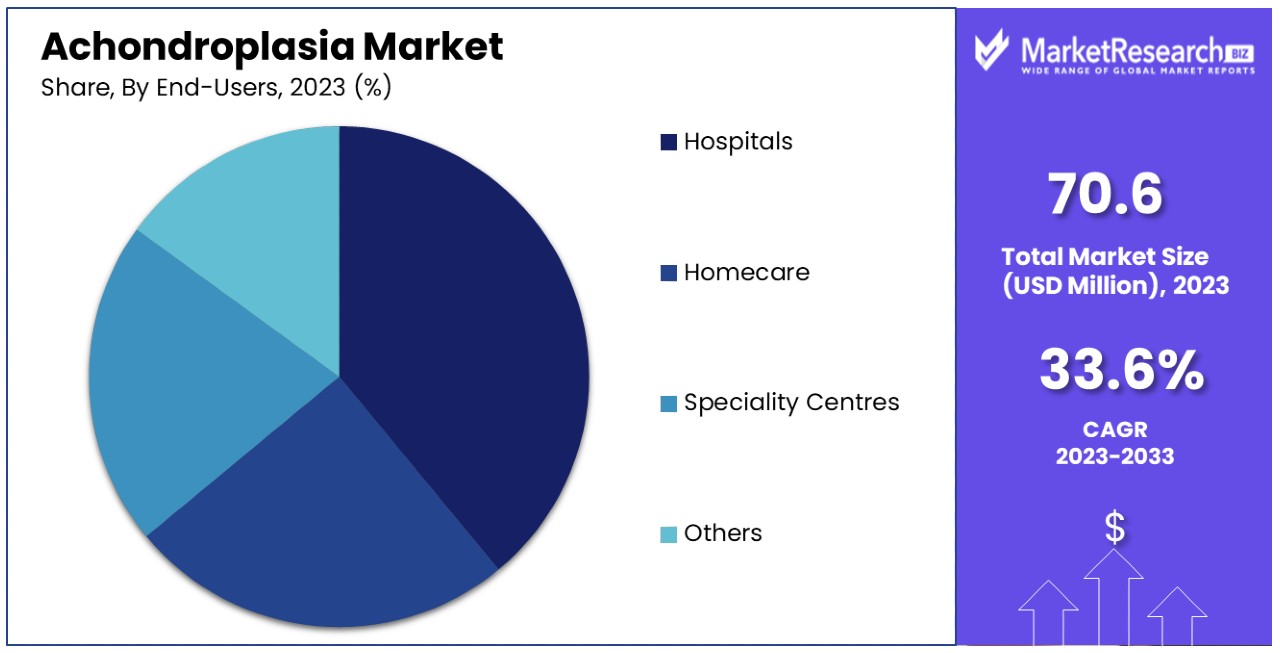

The Global Achondroplasia Market size is expected to be worth around USD 1,189.8 Million by 2033, from USD 70.6 Million in 2023, growing at a CAGR of 33.60% during the forecast period from 2024 to 2033.

The surge in demand for advanced treatments and medications is one of the main driving factors for the achondroplasia market expansion. Achondroplasia is a rare type of genetic bone disorder. It is recognized as the most common skeletal dysplasia in human bodies. Achondroplasia accounts for more than 90% of cases of uneven short stature, which is called dwarfism.

Such a condition is caused by a mutation in the transmembrane section of the fibroblast growth factor receptor 3, which is also known as FGFR3. It monitors an autosomal dominant way for the legacy with 100% penetrance. The FGFR3 gene guides the body to create the necessary proteins for bone growth and maintenance. The mutation in the FGFR3 gene leads to the protein becoming overactive and obstructing normal skeletal formation.

Achondroplasia in children is very common, as it does not let cartilage transform into a normal bone. This leads to the formation of short arms and legs with a large head. According to the National Center for Biotechnology Information in August 2023, there are over 80% of cases where the condition prevails due to sporadic mutations, which cause children to be born with achondroplasia with no genetic medical history of the disorder among the parents.

Moreover, 20% of achondroplastic people have at least one affected parent. The risk to the children of people with achondroplasia of inheriting a mutated replica of the FGFR3 gene is 50%. When both individuals are affected by this condition, their children or offspring have a 1 out of 4 chance of having normal height, a 1 in 2 chance of having heterozygous achondroplasia, and a 1 in 4 chance of having homozygous achondroplasia.

Achondroplasia can be examined before birth by fetal ultrasound. This diagnosis uses sound waves and a computer to analyze and develop images of the baby that is growing inside the womb. DNA testing will also be done before the birth to check fetal ultrasound outcomes. There is no treatment for the children or individuals affected by achondroplasia.

But some doctors are using growth hormones to boost the growth rate of a child’s bones. Regular health checks and proper medication help deal with achondroplasia. The demand for the achondroplasia market will increase due to the sudden rise in achondroplasia cases, which will help in market expansion in the coming years.

Key Takeaways

- Market Value: The Achondroplasia Market is expected to reach USD 1,189.8 Million by 2033, exhibiting significant growth from USD 70.6 Million in 2023, with a notable CAGR of 33.60% during the forecast period from 2024 to 2033.

- Dominant Segments:

- Growth Hormone Therapy commands a 27% share, playing a pivotal role in managing achondroplasia by stimulating bone growth.

- Parenteral Route of Administration prevails due to the administration of growth hormone therapy via injections.

- Hospitals lead as the primary end-user segment, providing comprehensive care including diagnosis, treatment, and management.

- Hospital Pharmacies dominate distribution channels, ensuring immediate access to prescribed therapies, especially in hospital settings.

- Regional Dynamics: North America dominates with a 36% market share, followed closely by Europe at approximately 29%, driven by strong healthcare systems and significant research activities.

- Key Players: Pfizer Inc., Novartis AG, Eli Lilly and Company, among others, are key players shaping the achondroplasia market landscape. These players contribute to market growth through research, development, and the provision of therapeutic solutions.

- Analyst Viewpoint: Analysts anticipate continued growth in the achondroplasia market, driven by advancements in treatment modalities, increased awareness, and expanding research efforts.

- Growth Opportunities:

- The market offers opportunities for innovation in treatment modalities, especially in supportive therapies and surgical interventions.

- Expanding into emerging markets and leveraging digital health technologies could further drive market growth and accessibility to treatments

Driving Factors

Increasing Awareness and Early Diagnosis Drives Market Growth

The growth of the Achondroplasia Market is significantly propelled by heightened awareness and the prioritization of early diagnosis. In recent years, efforts to increase awareness among healthcare professionals and the general public have been fruitful, leading to a higher rate of early detection. This awareness enables early interventions, improving patient outcomes and stimulating demand for tailored treatments and management strategies.

Statistics indicate that early diagnosis facilitates better management of symptoms, reducing long-term complications and improving quality of life for those affected. Moreover, this trend has encouraged investments in research and development, aiming to meet the rising demand for effective solutions. The convergence of increased awareness and early diagnosis not only amplifies the need for specialized healthcare services but also fosters a more informed and prepared community, ready to address the challenges of achondroplasia.

Advancements in Genetic Testing and Prenatal Screening Fuel Market Expansion

Advancements in genetic testing and prenatal screening have revolutionized the detection of achondroplasia, offering profound implications for market growth. With the refinement of prenatal screening techniques, such as chorionic villus sampling (CVS) and amniocentesis, the detection of the FGFR3 gene mutation—responsible for achondroplasia—has become more accessible and accurate.

This technological progress has enabled early intervention strategies and personalized care plans from birth, significantly impacting the market by increasing the demand for specialized prenatal and postnatal services. The ability to identify achondroplasia prenatally allows for a proactive healthcare approach, enhancing the demand for innovative treatment options and supporting services. Consequently, this factor not only contributes to the direct expansion of the market but also catalyzes further research and development efforts aimed at addressing the unique needs of this population.

Development of Targeted Therapies Catalyzes Market Innovation

The exploration and development of targeted therapies represent a pivotal shift in the Achondroplasia Market, driving substantial growth through innovation. Current research initiatives focus on addressing the genetic roots of achondroplasia, with companies like BioMarin Pharmaceutical and QED Therapeutics at the forefront of developing novel therapeutic solutions. These targeted therapies aim to correct the disproportionate growth characteristics and alleviate associated health complications, offering hope for a significant improvement in patient quality of life.

Although still under development, these therapeutic approaches signify a major advancement in treatment paradigms, promising to transform patient care and management. The focus on targeted therapies not only underscores the market's evolution towards more effective and personalized treatment options but also highlights the industry's commitment to addressing the comprehensive needs of individuals with achondroplasia. This focus encourages ongoing investment in research and development, further fueling market growth and innovation.

Restraining Factors

High Cost of Treatments and Interventions Restrains Market Growth

The Achondroplasia Market faces significant growth constraints due to the high costs associated with treatments and interventions. For many affected families, the financial burden of growth hormone therapy, surgical procedures, and other necessary interventions is daunting. In regions lacking comprehensive healthcare coverage or subsidized care, these costs become prohibitive, limiting the willingness or ability of patients to seek out advanced treatments.

This financial barrier not only impacts the direct adoption of current treatments but also potentially stifles demand for new, innovative therapies that may come at an even higher cost. Consequently, the high cost of treatments directly limits the market's expansion, as it restricts the patient population that can afford these critical care options, thus hindering overall market growth.

Limited Awareness and Access in Developing Regions Restrains Market Growth

In developing regions, the growth of the Achondroplasia Market is further restrained by limited awareness and access to diagnosis and treatment. Despite increasing global awareness, many developing countries still face challenges such as inadequate healthcare infrastructure, scarcity of genetic testing facilities, and socio-economic barriers.

These challenges lead to underdiagnosis and limited access to essential care and support for individuals with achondroplasia. The lack of awareness and resources not only affects the ability of patients to receive timely and effective treatment but also impacts the market's potential for growth in these regions. The unmet needs in developing countries represent a significant gap in the market, limiting the expansion of the achondroplasia treatment and care ecosystem globally.

Treatment Analysis

Growth Hormone Therapy Dominates Achondroplasia Market with 27% Share

In the Achondroplasia Market, the treatment segment is integral to understanding the landscape of therapeutic options available and their market dynamics. Among these, Growth Hormone Therapy emerges as the dominant sub-segment. This therapy plays a pivotal role in managing achondroplasia by stimulating bone growth and improving the stature of individuals affected by this genetic condition. Its prominence in the market is attributed to the tangible outcomes it delivers in terms of height increase and the improvement of proportional discrepancies, making it a highly sought-after treatment option for achondroplasia patients.

Surgery, another significant sub-segment, includes procedures aimed at correcting specific abnormalities associated with achondroplasia, such as spinal stenosis and limb lengthening. Although impactful, surgeries are typically reserved for severe cases due to their invasive nature and the risks involved. Supportive Therapy encompasses a range of non-invasive treatments such as physical therapy, occupational therapy, and counseling, which are crucial for enhancing the quality of life of individuals with achondroplasia but don't directly influence growth as hormone therapy does. The "Others" category includes emerging treatments and interventions still under research or in early stages of adoption, which could potentially reshape the market landscape in the future.

Surgery and supportive therapy segments, while not as large as growth hormone therapy, contribute to the market by offering essential interventions for managing complications and improving the functionality and well-being of patients. These treatments address the multifaceted needs of achondroplasia patients, underscoring the importance of a comprehensive treatment approach that includes both medical and supportive care.

Route of Administration Analysis

Parenteral Route Prevails in Achondroplasia Treatment Market

In the Route of Administration segment, Parenteral is the dominant sub-segment, primarily due to the administration of growth hormone therapy, which is typically delivered through injections. This method's prevalence is closely linked to the effectiveness of growth hormone therapy in managing achondroplasia, making parenteral administration a critical component of the treatment landscape. Oral administration, while convenient and less invasive, currently plays a secondary role in the achondroplasia market, largely because the key therapies for achondroplasia, including growth hormone, do not have oral formulations.

The dominance of the parenteral route in the achondroplasia market is reinforced by advancements in injection devices and techniques that aim to improve patient comfort and compliance. However, the invasive nature of injections and the requirement for regular administration pose challenges, particularly for pediatric patients. The development of oral therapies for achondroplasia or the adaptation of existing treatments to oral formulations could significantly impact this segment, potentially shifting market dynamics toward a more balanced distribution between oral and parenteral routes.

End-Users Analysis

Hospitals Lead End-User Segment in Achondroplasia Market, Providing Comprehensive Care

Hospitals represent the dominant end-user segment in the Achondroplasia Market, primarily due to the comprehensive care they offer, including diagnosis, treatment, and management of achondroplasia. The availability of specialized services, such as surgery and growth hormone therapy, makes hospitals a central hub for achondroplasia care.

Homecare, while growing, primarily supports post-treatment recovery and ongoing supportive therapies, highlighting the trend towards maintaining quality of life outside hospital settings. Specialty Centers, dedicated to genetic disorders or pediatric care, play a critical role in providing specialized treatments and support for achondroplasia patients, often working in conjunction with hospitals to offer comprehensive care. The "Others" category encompasses various healthcare settings that contribute to the care continuum, such as community clinics and rehabilitation centers, offering accessible care options and supporting the overall treatment landscape.

Hospitals' dominance is supported by their ability to offer multi-disciplinary care, essential for addressing the complex needs of achondroplasia patients. The integration of various treatment modalities, from surgery to hormone therapy and supportive care, within hospital settings facilitates a holistic approach to achondroplasia management. However, the expanding role of homecare and specialty centers reflects a shift towards personalized and specialized care, indicating a diversifying market that accommodates the varying needs and preferences of patients and families.

Distribution Channel Analysis

Hospital Pharmacies Dominate Distribution Channels in Achondroplasia Treatment Market

The Distribution Channel segment is crucial for understanding how treatments for achondroplasia reach patients. Hospital Pharmacies stand out as the dominant sub-segment, primarily due to their role in dispensing medications and treatments directly to patients receiving care in hospital settings, including growth hormone therapy and post-surgical medications.

Online Pharmacies are rapidly growing, offering convenience and accessibility, especially for homecare settings, by delivering medications and supplies directly to patients' homes. Retail Pharmacies complement the distribution landscape by providing access to supportive care medications and over-the-counter products that assist in managing symptoms associated with achondroplasia.

The prominence of hospital pharmacies is linked to the integrated care model in hospital settings, where immediate access to prescribed therapies is critical for treatment efficacy and patient convenience. The rise of online pharmacies reflects broader trends in healthcare towards digitalization and patient-centered care, offering a discreet and efficient option for obtaining medications. Retail pharmacies serve as an essential access point for the broader community, including individuals with achondroplasia who require immediate or routine over-the-counter medications.

The distribution of treatments for achondroplasia through these channels ensures that patients have access to necessary therapies across different settings, supporting comprehensive care. The growth of online and retail pharmacies indicates a shift towards more diversified and accessible distribution models, which could further evolve with advancements in e-commerce and digital health technologies.

Key Market Segments

By Treatment

- Growth Hormone Therapy

- Surgery

- Supportive Therapy

- Others

By Route of Administration

- Oral

- Parenteral

By End-Users

- Hospitals

- Homecare

- Speciality Centres

- Others

By Distribution Channel

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

Growth Opportunities

Personalized Medicine and Precision Therapies Offer Growth Opportunity

The advent of personalized medicine and precision therapies marks a transformative growth opportunity within the Achondroplasia Market. As research unravels the genetic intricacies of achondroplasia, the development of treatments tailored to individual genetic profiles becomes feasible.

This approach not only promises to enhance the efficacy of treatments but also to significantly improve the quality of life for patients. With the potential to precisely target the genetic anomalies causing achondroplasia, personalized therapies could revolutionize patient care, fostering a surge in demand for customized treatment plans and contributing to market expansion.

Expansion of Newborn Screening Programs Offers Growth Opportunity

The expansion of newborn screening programs to include achondroplasia represents a substantial opportunity for market growth. Early detection of achondroplasia through newborn screening enables immediate access to treatment and support, laying the groundwork for improved long-term outcomes.

As newborn screening for achondroplasia becomes more widespread, a corresponding increase in the need for diagnostic services, genetic counseling, and early intervention measures is anticipated. This trend not only supports the market's growth by boosting demand for existing services and treatments but also opens avenues for the development of new therapeutic and support options.

Trending Factors

Patient-Centric Approach and Improved Quality of Life Are Trending Factors

The shift towards a patient-centric approach in managing achondroplasia emphasizes the importance of improving the quality of life for individuals with the condition. This trend reflects a holistic view of care that encompasses emotional, social, and psychological support alongside traditional medical treatments.

Initiatives such as support groups, counseling, and educational resources are gaining prominence, indicating a broader understanding of the needs of those living with achondroplasia. This comprehensive care model is becoming a benchmark in the healthcare sector, driving advancements in services and treatments that address the full spectrum of patient needs.

Telemedicine and Remote Monitoring Are Trending Factors

Telemedicine and remote monitoring are rapidly emerging as pivotal elements in the care of individuals with achondroplasia. These technologies offer a new avenue for healthcare delivery, enabling continuous patient care without the need for physical hospital visits.

This is particularly beneficial for patients in remote or underserved regions, where access to specialized care may be limited. The growing adoption of these technologies highlights their potential to significantly enhance accessibility to healthcare services, reduce the logistical burden on families, and streamline the management of achondroplasia, contributing to a trend towards more accessible and efficient patient care.

Genetic Counseling and Prenatal Testing Advancements Are Trending Factors

Advancements in genetic counseling and prenatal testing for achondroplasia are shaping up as key trending factors in the market. The progress in genetic testing technologies has improved the ability of healthcare providers to offer detailed guidance and support to expectant parents.

This trend towards enhanced genetic counseling and testing services reflects a growing emphasis on informed decision-making and early intervention. As these services become more accessible and comprehensive, they play a critical role in empowering families with crucial information and support, further emphasizing the market's trend towards anticipatory and informed healthcare practices.

Regional Analysis

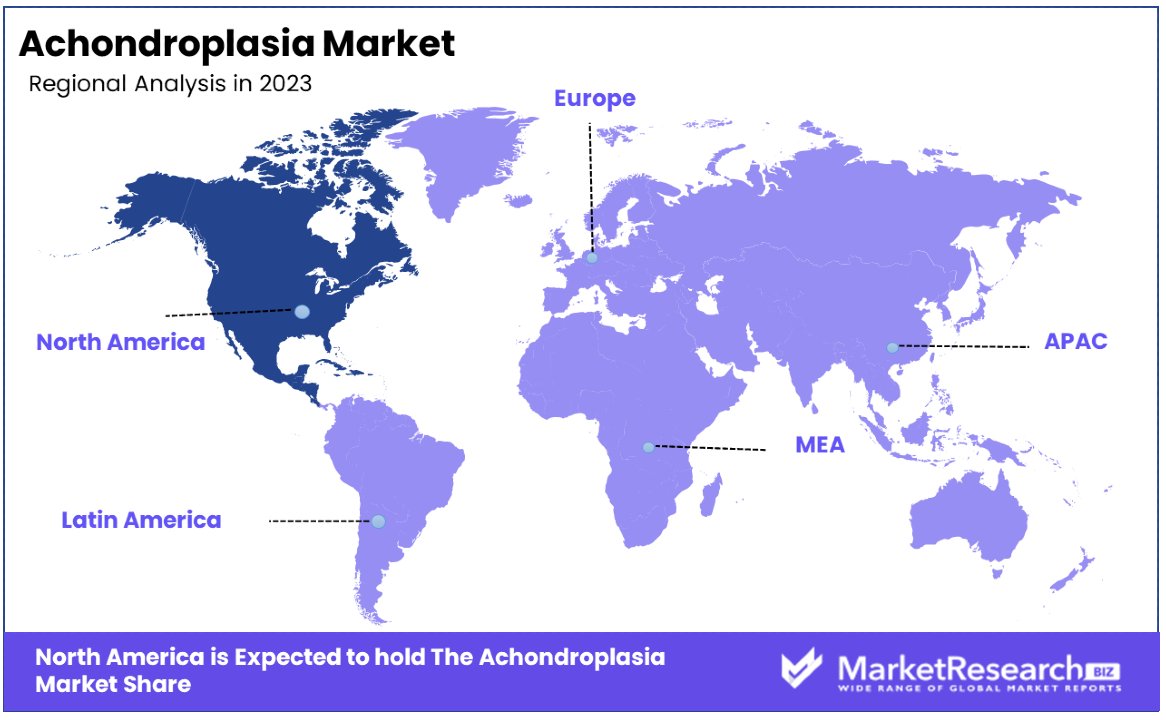

North America Dominates with 36% Market Share

North America's commanding 36% share in the Achondroplasia Market is attributed to several key factors, including advanced healthcare infrastructure, significant investments in genetic research, and a strong focus on personalized medicine. The region's developed healthcare system enables widespread access to cutting-edge treatments and interventions, while ongoing research initiatives contribute to the development of innovative therapies. Additionally, heightened awareness and supportive policies towards genetic disorders drive early diagnosis and treatment, bolstering the market's growth in this region.

North America are shaped by a collaborative ecosystem that includes research institutions, biotech companies, and healthcare providers. This collaboration facilitates rapid advancements in treatment approaches and enhances patient care. The region's robust regulatory framework also plays a crucial role in ensuring the safety and efficacy of new therapies, encouraging innovation in the market.

For other regions:

- Europe follows North America closely with a market share of approximately 29%, driven by similar factors such as strong healthcare systems, high awareness, and significant research activities.

- Asia Pacific is experiencing rapid growth, with a market share of 21%, attributed to improving healthcare infrastructure, increasing awareness, and rising investments in healthcare technologies.

- Middle East & Africa hold a smaller market share of 9%, where growth is gradually increasing due to improving access to healthcare and rising awareness of genetic disorders.

- Latin America also has a significant presence in the market with a share of 5%, where growth is driven by improvements in healthcare infrastructure and increased focus on child health.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the competitive landscape of the Achondroplasia market, several key players vie for prominence, each contributing unique approaches to address the challenges associated with this genetic disorder. Pfizer Inc., a pharmaceutical giant renowned for its innovation, collaborates on groundbreaking research and development initiatives.

Ascendis Pharma A/S stands out for its commitment to transformative therapies, leveraging advanced technologies to target the underlying causes of Achondroplasia. BridgeBio Pharma, Inc. distinguishes itself through a diversified pipeline and strategic partnerships, positioning it as a formidable contender in the market.

Teva Pharmaceutical Industries Ltd. and Ipsen Pharma bring their extensive expertise in drug development and commercialization to the forefront, exploring novel treatment modalities to improve patient outcomes. Novartis AG, Eli Lilly and Company, and JCR Pharmaceuticals Co., Ltd. exhibit a global presence and robust research capabilities, driving innovation and expanding therapeutic options for Achondroplasia patients worldwide.

Additionally, emerging players like Xiamen Amoytop Biotech Co., ProLynx Inc., and Ferring B.V. contribute to the competitive landscape with promising advancements in biotechnology and drug delivery systems. KVK TECH, INC., LG Chem, VIVUS LLC., F. Hoffmann-La Roche Ltd, BioMarin Pharmaceutical Inc., and Bristol-Myers Squibb Company further enrich the market with their diverse portfolios and commitment to addressing the unmet needs of Achondroplasia patients. As competition intensifies, collaborative efforts and strategic alliances are likely to drive innovation and propel advancements in Achondroplasia therapeutics.

Market Key Players

- Pfizer Inc.

- Ascendis Pharma A/S

- BridgeBio Pharma, Inc.

- Teva Pharmaceutical Industries Ltd.

- Ipsen Pharma

- Novartis AG

- Eli Lilly and Company

- JCR Pharmaceuticals Co., Ltd

- Xiamen Amoytop Biotech Co.,

- ProLynx Inc.

- Ferring B.V.

- KVK TECH, INC.

- LG Chem

- VIVUS LLC.

- F. Hoffmann-La Roche Ltd

- BioMarin Pharmaceutical

- Bristol-Myers Squibb Company

Recent Developments

- In 2022, Ascendis Pharma AS will initiate a Phase 3 clinical trial for Vosoritide, a treatment for achondroplasia; BioMarin Pharmaceutical Inc will follow suit in 2023.

- In 2023, The acquisition of BridgeBio Pharma Inc by Pfizer Inc demonstrated the pharmaceutical giant's continued dedication to achondroplasia treatment research. The acquisition has strengthened Pfizer's pipeline with BBP-265, a prospective genetic disease therapy in preclinical development. It is believed that BBP-265 targets the underlying cause of achondroplasia by promoting endochondral bone growth.

- In 2023, BioMarin Pharmaceutical Inc. will initiate the Phase 2 clinical trial for BMN-270, its achondroplasia treatment. In addition to targeting the underlying genetic cause of achondroplasia, this therapy aims to enhance the production of the FGFR3 receptor, which plays a crucial role in the disorder's development.

Report Scope

Report Features Description Market Value (2022) USD 70.6 Mn Forecast Revenue (2032) USD 1,189.8 Mn CAGR (2023-2032) 33.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Treatment (Surgery, Growth Hormone Therapy, Supportive Therapy, Vosoritide)

By Route of Administration (Oral, Parenteral)

By End-User (Hospitals & Clinics, Homecare, Speciality Centers, Other End-Users)Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Teva Pharmaceuticals Industries Ltd, F.Hoffman-La Roche Ltd., Aurobiondo Pharma, Bristol-Myers Squibb Company, GSK plc, Ascendis Pharma A/S, Mylan N.V., Johnson & Johnson, Pfizer Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Teva Pharmaceutricals Industries Ltd

- BioMarin Pharmaceutical

- F.Hoffman-La Roche Ltd.

- Aurobiondo Pharma

- Bristol-Myers Squibb Company

- GSK plc

- Ascendis Pharma A/S

- Mylan N.V.

- Johnson & Johnson

- Pfizer Inc.

- Other Key Palyers

Our Clients

View Our Licence Options