Global Wireless Electric Vehicle Charging Market By Application(Commercial Charging Station, Home Charging Unit), By Component(Base Charging Pad, Power Control Unit, Vehicle Charging Pad), By Distribution Channel(Aftermarket, OE Market) , By Charging Type(Dynamic Wireless Charging System, Stationary Wireless Charging System) , By Propulsion Type(BEV, PHEV), By Vehicle Type(Commercial Vehicle, Passenger Car) , By Power Supply Range(3–50 kW), By Charging System(Magnetic Power Transfer, Capacitive Power Transfer, Inductive Power Tran

-

14120

-

July 2024

-

300

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Report Overview

- Key Takeaways

- Driving factors

- Restraining Factors

- By Application Analysis

- By Component Analysis

- By Distribution Channel Analysis

- By Charging Type Analysis

- By Propulsion Type Analysis

- By Vehicle Type Analysis

- By Power Supply Range Analysis

- By Charging System Analysis

- Key Market Segments

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

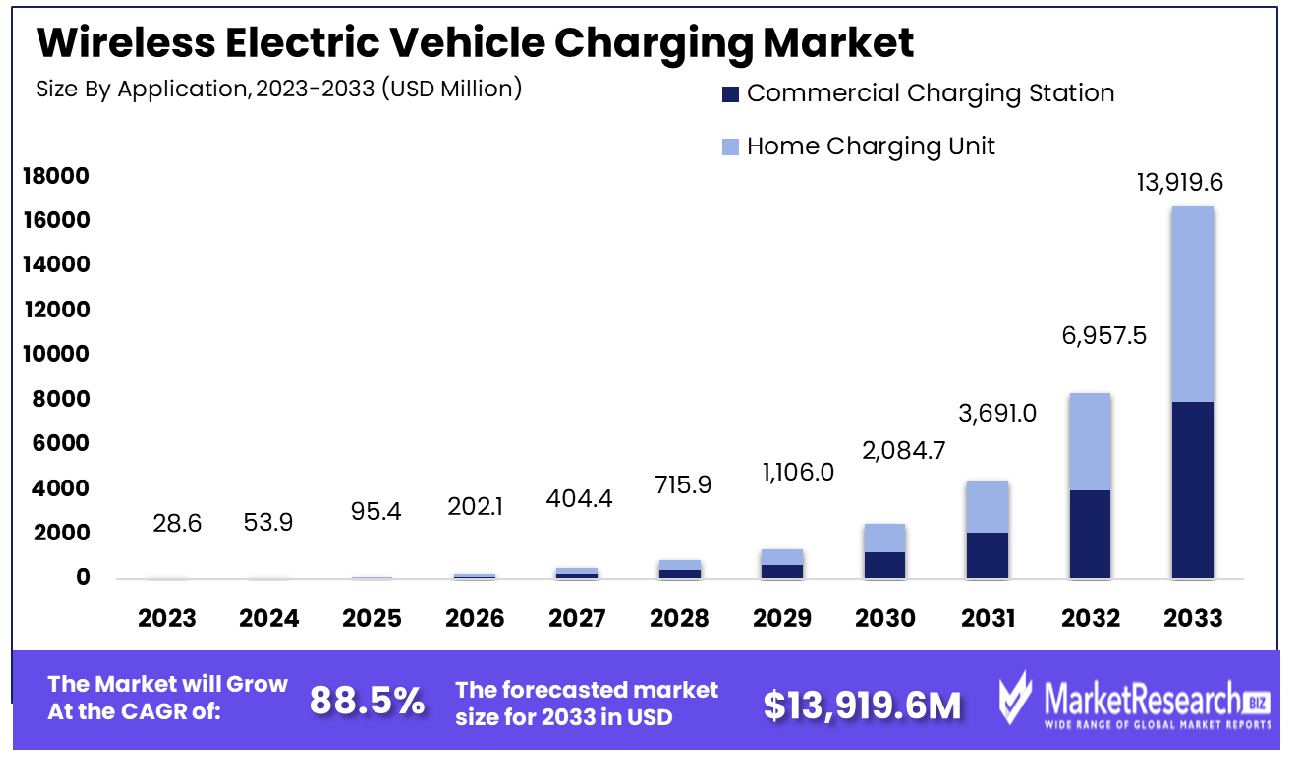

The Global Wireless Electric Vehicle Charging Market was valued at USD 28.6 million in 2023. It is expected to reach USD 13,919.6 million by 2033, with a CAGR of 88.5% during the forecast period from 2024 to 2033.

The Wireless Electric Vehicle Charging Market encompasses technologies that enable the transfer of electrical energy from a power source to an electric vehicle (EV) without the need for physical connectors or cables. This market leverages inductive charging technology, wherein coils in the charging station and vehicle communicate to facilitate energy transfer through an electromagnetic field.

This innovation promises to enhance convenience, reduce wear and tear associated with manual charging, and support the broader adoption of EVs by streamlining the charging process. As EV adoption grows, this market is positioned as a critical component in the evolution of sustainable transportation infrastructure.

The Wireless Electric Vehicle (EV) Charging Market is poised for significant growth, driven by advancements in technology and increasing global demand for electric vehicles. As vehicles evolve towards more autonomous functionalities, the integration of seamless charging solutions such as wireless EV charging becomes critical. This market utilizes inductive charging technology, which allows electric vehicles to charge without physical cables, presenting a streamlined and user-friendly alternative to traditional plug-in methods.

The adoption of the SAE J2954 standard, which outlines specifications for wireless charging levels at 3.7 kW, 7 kW, and 11 kW, marks a pivotal standardization step, ensuring compatibility and safety across different vehicle models and charging stations. This standard not only enhances current technology but also sets the groundwork for future enhancements that could accommodate higher power levels as technology progresses.

Moreover, the surge in patent applications within this sector—from 21 to 43 applications within a year—illustrates a burgeoning innovation landscape and a near 100% increase in developmental activity. This suggests a robust intellectual property environment and a competitive market, with numerous players seeking to capitalize on proprietary advancements.

Key Takeaways

- Market Growth: The Global Wireless Electric Vehicle Charging Market was valued at USD 28.6 million in 2023. It is expected to reach USD 13,919.6 million by 2033, with a CAGR of 88.5% during the forecast period from 2024 to 2033.

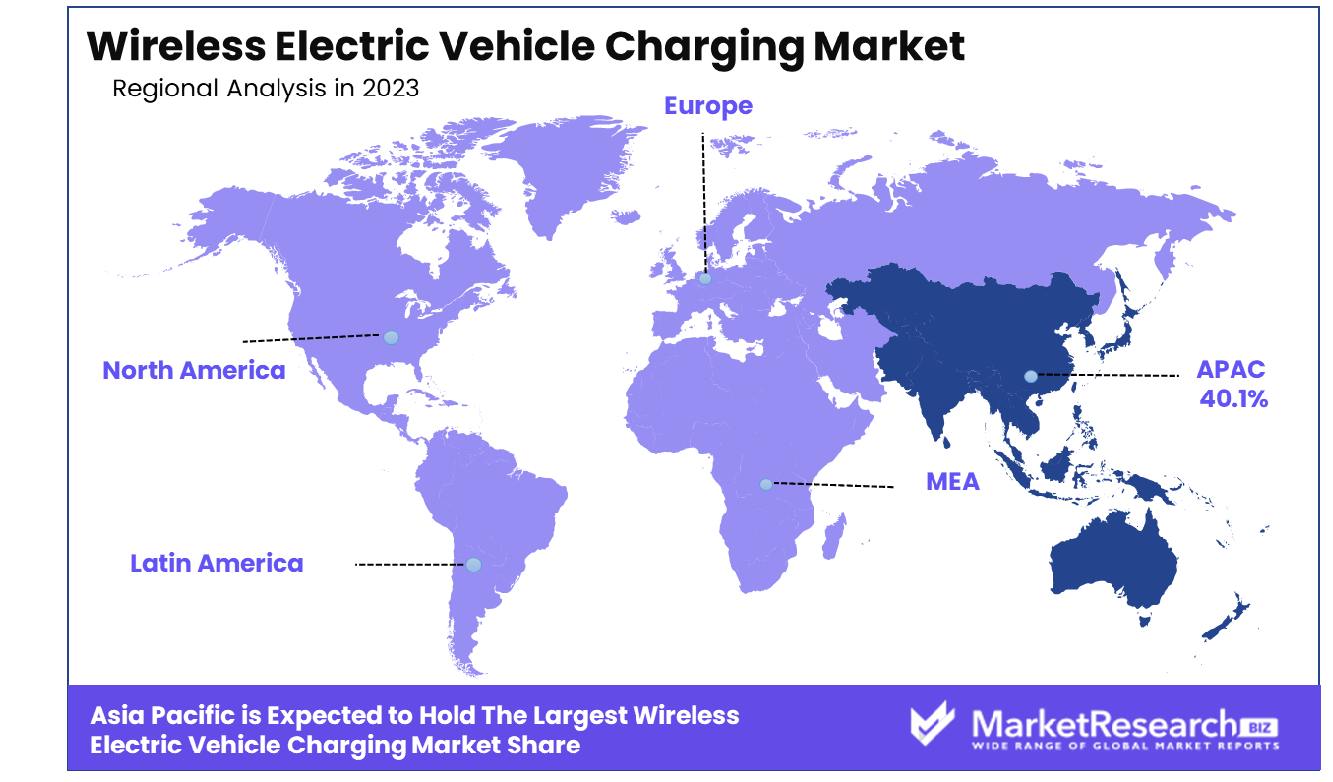

- Regional Dominance: Asia Pacific dominates with 40.1% of the Wireless EV Charging Market.

- By Application: Home charging units dominated, capturing 60% of the market.

- By Component: Base charging pads led with a 50% market share.

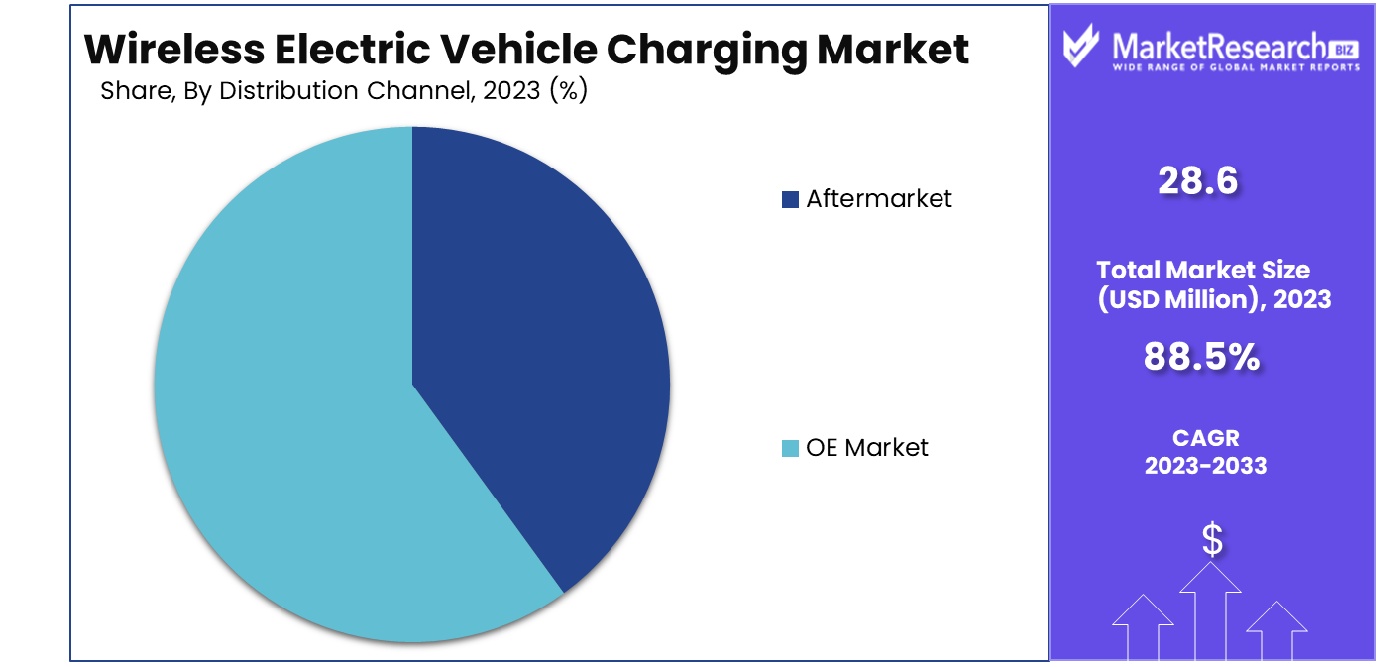

- By Distribution Channel: The OE market was the main channel, dominating at 65%.

- By Charging Type: Stationary wireless systems held a 70% majority in charging.

- By Propulsion Type: Battery Electric Vehicles (BEV) dominated propulsion types at 55%.

- By Vehicle Type: Passenger cars dominated vehicle types with a 70% share.

- By Power Supply Range: Power supply ranges of 11–50 kW led by 45%.

- By Charging System: Inductive power transfer systems dominated, achieving a 65% market share.

Driving factors

Growth in the Electric Vehicle Industry

The expansion of the electric vehicle (EV) industry serves as a cornerstone for the growth of the Wireless Electric Vehicle Charging Market. As more consumers and businesses adopt EVs, driven by a growing awareness of environmental issues and the economic benefits of electric mobility, the demand for efficient and user-friendly charging solutions escalates.

This increasing EV adoption directly correlates with the need for innovative charging infrastructures, like wireless charging, that can support the high volume of electric vehicles expected on the roads in the coming years.

Increasing Demand for Convenient and Advanced Charging Solutions

Consumers and enterprises are continuously seeking more convenient and advanced charging solutions that integrate seamlessly into daily routines. Wireless EV charging offers a significant advantage by eliminating the physical hassle of plugging in vehicles and reducing wear and tear associated with mechanical connectors.

This convenience factor, combined with the potential for these systems to be installed in various locations such as homes, offices, and public spaces, substantially enhances user experience and accessibility, making it a highly attractive option for current and prospective EV owners.

Supportive Government Policies and Incentives for EV Infrastructure

Governments worldwide are implementing policies and incentives to encourage the adoption of electric vehicles and the development of related infrastructure, which includes wireless charging systems. These policies often come in the form of tax rebates, grants, and subsidies, as well as regulations that mandate or highly encourage the use of green technologies.

Such government support not only alleviates the initial investment burden for new technologies but also signals a long-term commitment to sustainable transport solutions, thereby fostering a conducive environment for the growth of the wireless EV charging market. Together, these factors synergistically propel the market forward, reinforcing its expansion as part of a broader movement towards electrification and technological innovation in transportation.

Restraining Factors

High Cost of Wireless Charging Technology

The substantial cost associated with developing and implementing wireless charging technology is a significant restraining factor in the growth of the Wireless Electric Vehicle Charging Market. The integration of advanced components and the need for extensive R&D to ensure safety and efficiency lead to higher initial investments compared to traditional charging systems.

This cost barrier can deter both manufacturers and consumers from adopting wireless charging solutions, particularly in cost-sensitive markets and among consumers who view the premium of wireless technology as not justifying the convenience it offers.

Technical Challenges Related to Efficiency and Compatibility

Efficiency losses during power transmission and compatibility issues between different EV models and charging systems further inhibit market expansion. Wireless charging systems typically experience energy losses during the transfer process, which can be more pronounced than in conventional wired charging, potentially affecting the overall appeal of the technology due to increased energy costs and reduced charging speed.

Moreover, the current lack of standardized protocols across different manufacturers means that not all EVs can use all available wireless charging systems without specific modifications or adapters. This fragmentation within the industry can complicate the consumer's experience and slow down the adoption rates.

By Application Analysis

The Home Charging Unit dominated the market with a significant 60% share in applications.

In 2023, the Home Charging Unit held a dominant market position in the "By Application" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 60% share. This significant market presence underscores the pivotal role of home-based charging solutions in facilitating the adoption and convenience of electric vehicles (EVs). The Home Charging Unit segment's dominance is attributed to the growing consumer preference for at-home charging facilities, which offer the convenience of overnight charging and the elimination of range anxiety.

On the other hand, the Commercial Charging Station segment accounted for a smaller share of the market. Despite this, commercial stations are critical in providing the necessary infrastructure for EV users on the go, and they are expected to grow as urbanization and EV adoption increase. This segment's expansion is fueled by government initiatives and investments in EV infrastructure aimed at reducing carbon emissions and promoting sustainable transportation solutions.

The wireless electric vehicle charging market itself is driven by advancements in technology that enhance the efficiency and convenience of charging without the physical constraints of plug-in systems. Innovations in inductive charging technology have made it possible to increase power transfer efficiency and reduce charging times, making wireless charging more appealing to both residential and commercial users.

As the market continues to evolve, the dynamics between home and commercial charging solutions will be crucial in shaping the future landscape of EV infrastructure. With ongoing technological improvements and supportive regulatory frameworks, the wireless electric vehicle charging market is poised for significant expansion, promising enhanced accessibility and convenience for EV users worldwide.

By Component Analysis

Base Charging Pads led components in the market, capturing a dominant 50% share.

In 2023, the Base Charging Pad held a dominant market position in the "By Component" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 50% share. This substantial market share highlights the critical role of the base charging pad as the foundational component in the infrastructure of wireless EV charging systems. The prominence of the base charging pad is primarily due to its direct impact on the efficiency and reliability of the wireless charging process, which is essential for consumer adoption and satisfaction.

Conversely, the Power Control Unit and the Vehicle Charging Pad also play significant roles but command smaller segments of the market. The Power Control Unit, responsible for managing the power transfer and ensuring safety during the charging process, is integral to the functionality of wireless charging systems. Despite its importance, it accounted for a lesser share compared to the base charging pad, possibly due to the higher visibility and direct interaction consumers have with the charging pads.

Similarly, the Vehicle Charging Pad, which interacts directly with the base pad to receive the charge, is an essential component but has not reached the same level of market penetration as the base charging pad. This could be attributed to the current variations in vehicle compatibility and the gradual adoption of wireless charging technology across different EV models.

As technology progresses and more vehicles become equipped with built-in compatibility for wireless charging, it is anticipated that the market shares for both the Power Control Unit and Vehicle Charging Pad will see substantial growth. Advancements in technology, coupled with increasing consumer demand for convenience and innovative charging solutions, are likely to drive further development and distribution of all components within the wireless EV charging market.

By Distribution Channel Analysis

The OE Market emerged as the leading distribution channel, holding a 65% market share.

In 2023, the OE Market held a dominant market position in the "By Distribution Channel" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 65% share. This substantial market presence underscores the increasing integration of wireless charging technology directly from original equipment manufacturers (OEMs). The dominance of the OE Market is driven by the growing partnerships between wireless charging technology providers and automotive manufacturers, aiming to embed this innovative technology into new vehicles to enhance consumer appeal and functionality.

Conversely, the Aftermarket segment, while smaller, represents a significant portion of the market, providing solutions for existing electric vehicle (EV) owners who wish to upgrade to wireless charging capabilities. The aftermarket channel faces challenges such as compatibility issues and the need for professional installation, which can deter potential users. However, it remains a vital component of the market by offering flexibility for users to adopt new technologies without purchasing new vehicles.

The robust growth of the OE Market can be attributed to consumer preferences for seamless, integrated technologies that do not require additional modifications. Additionally, as automotive manufacturers increasingly focus on electric and autonomous vehicles, wireless charging is becoming a key feature that enhances the overall value proposition of EVs.

Looking forward, the OE Market is expected to maintain its leadership position as more automakers incorporate wireless charging as a standard feature in their new models. Meanwhile, the Aftermarket will likely continue to grow, supported by advancements in technology that simplify installation and improve compatibility across various vehicle models.

By Charging Type Analysis

Stationary Wireless Charging Systems dominated the charging type segment with a 70% market share.

In 2023, the Stationary Wireless Charging System held a dominant market position in the "By Charging Type" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 70% share. This commanding market share underscores the system's widespread adoption, primarily driven by its reliability and the ease of integration into existing infrastructure. Stationary systems, which require the vehicle to be parked over a charging pad, are favored in both residential and commercial settings due to their straightforward installation and operation.

Conversely, the Dynamic Wireless Charging System, which allows vehicles to charge while in motion through embedded road systems, captured a smaller portion of the market. Despite its innovative approach to solving a range of issues and enhancing convenience, the dynamic system faces significant hurdles in terms of higher costs, complex installation, and slower development and deployment rates compared to stationary systems.

The predominant preference for Stationary Wireless Charging Systems is largely influenced by current consumer behavior, which aligns well with home charging during overnight hours or fast charging in dedicated parking areas. Moreover, the technology's maturity means it is often more cost-effective and quicker to deploy than dynamic systems.

As the market evolves, dynamic charging systems are expected to gain traction, especially in commercial and urban planning applications where continuous vehicle operation is crucial. However, for the foreseeable future, stationary systems are likely to maintain their lead due to their established technology, lower barriers to entry, and broad compatibility with existing electric vehicle models.

By Propulsion Type Analysis

Battery Electric Vehicles (BEVs) led the propulsion type category, comprising 55% of the market.

In 2023, Battery Electric Vehicles (BEVs) held a dominant market position in the "By Propulsion Type" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 55% share. This prominent market share is indicative of the growing consumer preference for fully electric vehicles, which do not utilize any form of internal combustion engine. BEVs benefit greatly from advancements in wireless charging technology, which enhance their usability and appeal by simplifying the charging process and reducing reliance on plug-in methods.

In contrast, Plug-in Hybrid Electric Vehicles (PHEVs), which combine a traditional internal combustion engine with electric propulsion, accounted for a smaller share of the market. Although PHEVs offer a bridging technology for consumers transitioning from conventional vehicles to electric vehicles, the dual-system complexity and the presence of an internal combustion engine make them less dependent on purely electric charging infrastructure, including wireless systems.

The larger market share of BEVs can be attributed to several factors. Firstly, the increasing range of BEVs, coupled with their decreasing battery costs, makes them more accessible and practical for a broader range of consumers. Secondly, environmental regulations and government incentives are driving the adoption of cleaner, fully electric vehicles, which aligns well with the deployment of wireless charging technologies.

As the automotive industry continues to evolve towards more sustainable solutions, the market for BEVs and their associated charging technologies is expected to expand further. Wireless charging stands to play a crucial role in this growth by offering an efficient, user-friendly solution that aligns with the environmental and practical needs of modern consumers.

By Vehicle Type Analysis

Passenger Cars significantly dominated vehicle types, accounting for 70% of the market share.

In 2023, the Passenger Car segment held a dominant market position in the "By Vehicle Type" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 70% share. This significant market dominance is primarily attributed to the escalating demand for electric passenger cars among consumers seeking sustainable and innovative transportation solutions. The convenience offered by wireless charging systems, which eliminate the need for manual cable connections, has particularly enhanced the appeal of electric passenger cars, making them a preferred choice for daily commutes and personal use.

Conversely, the Commercial Vehicle segment, encompassing electric buses, trucks, and vans, accounted for a smaller share of the market. Although growing, this segment faces different challenges, such as the need for higher power outputs and longer charging durations, which currently limit the rapid adoption of wireless charging technologies in commercial settings. However, as technology advances, commercial vehicles are expected to increasingly benefit from wireless charging, especially in fleet operations where operational efficiency is crucial.

The dominant position of Passenger Cars in the wireless charging market is bolstered by several factors. Increasing urbanization and consumer awareness of environmental issues are driving the adoption of cleaner, more efficient personal vehicles. Additionally, governments worldwide are implementing regulations and offering incentives to support electric vehicle adoption, further stimulating the growth of the electric car market.

As the technology for wireless charging continues to evolve and scale, it is anticipated that both segments will experience growth, with passenger cars maintaining a strong lead due to their widespread use and the direct benefits they offer to individual consumers.

By Power Supply Range Analysis

The 11–50 kW power supply range held a substantial 45% dominance in the market.

In 2023, the 11–50 kW range held a dominant market position in the "By Power Supply Range" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 45% share. This segment caters predominantly to the needs of passenger cars and light commercial vehicles, offering an optimal balance between charging speed and infrastructure costs. The dominance of the 11–50 kW category reflects its suitability for a broad range of applications, from private homes to public and semi-public parking areas, where the majority of daily charging occurs.

In contrast, the 3–<11 kW range, primarily used for slower, overnight charging, captured a smaller market share. Although ideal for residential settings due to lower energy consumption rates and minimal infrastructure requirements, its slower charging speed makes it less attractive for drivers who require quicker charging options.

The >50 kW range, designed for rapid charging in commercial and industrial settings, also holds a smaller portion of the market. While it supports fast charging for vehicles requiring quick turnaround times, such as buses and fleet vehicles, the higher costs associated with this technology and the more intensive infrastructure demands limit its widespread adoption in the current market landscape.

The preference for the 11–50 kW power supply range underscores a market trend towards solutions that offer a practical compromise between speed and cost, facilitating broader adoption. As the electric vehicle market continues to expand and diversify, the demand for mid-range wireless charging solutions is expected to grow, supported by enhancements in efficiency and reductions in technology costs.

By Charging System Analysis

Inductive Power Transfer systems were the most prevalent, dominating 65% of the charging system market.

In 2023, Inductive Power Transfer held a dominant market position in the "By Charging System" segment of the Wireless Electric Vehicle Charging Market, capturing more than a 65% share. This prominence is largely due to its well-established technology and widespread adoption across various applications, from residential to commercial charging stations. Inductive charging systems utilize electromagnetic fields to transfer energy between two coils—one in the charging station and the other in the vehicle—providing a safe and efficient method to charge electric vehicles without physical connectors.

Contrastingly, Magnetic Power Transfer and Capacitive Power Transfer accounted for smaller segments of the market. Magnetic Power Transfer, similar in principle to inductive systems but typically designed for higher power applications, has not yet seen widespread commercial adoption due to its nascent stage of development and higher costs. Capacitive Power Transfer, employing electric fields for wireless power transmission and known for its potential in high-frequency applications, also remains less common due to technical challenges and limited infrastructure.

The robust market share of Inductive Power Transfer can be attributed to its reliability and consumer trust, built over years of proven performance and safety. It is particularly favored in urban settings and public charging facilities where ease of use and minimal maintenance are critical. As the market for electric vehicles grows, the demand for reliable and user-friendly charging solutions like inductive power transfer is expected to rise, driven by continued innovations that enhance efficiency and reduce costs.

Key Market Segments

By Application

- Commercial Charging Station

- Home Charging Unit

By Component

- Base Charging Pad

- Power Control Unit

- Vehicle Charging Pad

By Distribution Channel

- Aftermarket

- OE Market

By Charging Type

- Dynamic Wireless Charging System

- Stationary Wireless Charging System

By Propulsion Type

- BEV

- PHEV

By Vehicle Type

- Commercial Vehicle

- Passenger Car

By Power Supply Range

- 3–<11 kW

- 11–50 kW

- >50 kW

By Charging System

- Magnetic Power Transfer

- Capacitive Power Transfer

- Inductive Power Transfer

Growth Opportunity

Integration with Smart City Projects

The integration of wireless electric vehicle (EV) charging technology into smart city projects represents a significant opportunity for the market in 2023. As cities worldwide aim to reduce their carbon footprints and enhance urban mobility, smart city initiatives increasingly incorporate sustainable technologies.

Wireless EV charging systems, embedded in public infrastructures like roads, parking lots, and public transport stations, can facilitate continuous charging and support the seamless operation of EV fleets in urban environments. This alignment with smart city goals not only expands the market reach of wireless charging solutions but also attracts substantial investments and partnerships from public and private sectors committed to urban sustainability.

Development of Fast-Charging Wireless Technologies

Another promising avenue in 2023 is the development and commercialization of fast-charging wireless technologies. As one of the main critiques of wireless charging is the speed at which it charges EVs compared to conventional methods, advancements that minimize charging time while maintaining efficiency could revolutionize the market.

Efforts to enhance the power capacity of wireless systems—from the current standards defined by the SAE J2954 up to faster levels—will cater to consumer demands for quicker, more convenient charging solutions. Successfully addressing this could not only mitigate one of the key restraining factors—the efficiency concern—but also position wireless charging as a truly competitive alternative to traditional plug-in charging stations.

Latest Trends

Development of Dynamic Wireless Charging Systems for Moving Vehicles

In 2023, one of the most groundbreaking trends in the global Wireless Electric Vehicle Charging Market is the development of dynamic wireless charging systems, which allow vehicles to charge while in motion. This innovative approach addresses one of the primary limitations of EVs—the need to stop charging—thus significantly enhancing the convenience and practicality of using electric vehicles for longer journeys.

The implementation of embedded charging tracks on highways and major roads can revolutionize travel dynamics by effectively eliminating range anxiety and making electric vehicles more appealing to the mass market. This technology not only promises to boost consumer confidence in EVs but also stimulates further research and investment in wireless charging infrastructure.

Increasing Standardization and Interoperability Among Different EV Models and Charging Systems

Another trend shaping the market in 2023 is the increasing focus on standardization and interoperability across different EV models and wireless charging systems. Efforts by industry consortia and regulatory bodies to standardize wireless charging protocols, like the adoption of the SAE J2954 standard, aim to ensure that vehicles and chargers from different manufacturers are compatible.

This interoperability is crucial for consumer convenience and the scalability of wireless charging solutions, as it alleviates concerns about exclusivity and compatibility that have historically hindered technology adoption. Enhanced standardization also facilitates broader infrastructure deployment, paving the way for more universal and accessible charging networks.

Regional Analysis

The Asia Pacific region dominates the Wireless Electric Vehicle Charging Market, holding a significant 40.1% share.

In North America, the market is driven by significant technological advancements and a robust electric vehicle infrastructure. The region benefits from the presence of major industry players and a high rate of EV adoption, making it a strong contender in the wireless charging market.

Europe follows closely, with stringent environmental regulations and government incentives boosting the adoption of EVs and, consequently, wireless EV charging technologies. European nations are actively investing in smart city projects that integrate these technologies into urban planning.

Asia Pacific stands out as the dominating region in this market, holding a substantial 40.1% share. This dominance is propelled by rapid urbanization, increasing environmental awareness, and substantial investments in EV infrastructure, particularly in countries like China, Japan, and South Korea. The region’s commitment to reducing carbon emissions significantly contributes to the adoption of innovative charging solutions.

The Middle East & Africa and Latin America are still emerging in the wireless EV charging market. These regions present a significant growth potential due to increasing urbanization and the gradual shift towards sustainable energy solutions. However, the current adoption rates are relatively lower compared to other regions, primarily due to infrastructural and economic challenges.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Wireless Electric Vehicle Charging Market is witnessing substantial contributions and competitive dynamics from a range of key players. These companies are at the forefront of innovation and deployment of wireless EV charging solutions, each bringing unique technologies and strategic approaches to the market.

Robert Bosch GmbH and Continental AG are leveraging their extensive automotive industry experience to integrate wireless charging systems into next-generation vehicles, focusing on high efficiency and reliability. WiTricity Corporation is pioneering with its patented magnetic resonance technology, which is crucial for improving the range and efficiency of wireless charging systems.

ZTE Corporation and Toyota Motor Corporation are expanding their R&D efforts to include dynamic wireless charging technologies that allow charging on the move, a critical development expected to revolutionize the market. Meanwhile, Toshiba Corporation and Qualcomm, Inc. continue to push the boundaries of battery technology and charging speeds, ensuring that wireless charging is not only convenient but also fast.

Evatran Group and Powermat Technologies Ltd. are focused on scaling their solutions to broader consumer markets, emphasizing user-friendly designs and widespread accessibility. Similarly, WiBotic Inc. and PowerSquare Inc. are enhancing their offerings for industrial and commercial vehicle applications, which are anticipated to represent a growing segment of the market.

Emerging players like Freewire Technologies and Swiftmile are also making notable inroads by targeting niche markets and deploying innovative business models, such as mobile charging stations and integrated service networks.

Market Key Players

- Robert Bosch GmbH

- Continental AG

- WiTricity Corporation

- ZTE Corporation

- HELLA KGaA Hueck & Co.

- Toyota Motor Corporation

- Toshiba Corporation

- Qualcomm, Inc.

- Evatran Group

- Powermat Technologies Ltd.

- PowerbyProxi Limited

- Energids Corp.

- WiBotic Inc.

- PowerSquare Inc.

- Aircharge

- Tecnomen Corporation

- Steca Elektronik GmbH

- Lumen Australia

- ECOtality

- Momentum Dynamics

- ZENS

- Freewire Technologies

- CIRCONTROL

- Swiftmile

Recent Development

- In April 2024, ZTE Corporation launched a collaborative project with several automotive manufacturers to integrate their wireless charging technology into public transport systems. This project is focused on enhancing the infrastructure for electric buses and taxis.

- In February 2024, Robert Bosch GmbH introduced a new wireless charging system for electric vehicles (EVs) that reduces charging time by 30%. This innovation is designed to enhance the convenience and efficiency of EV charging.

Report Scope

Report Features Description Market Value (2023) USD 28.6 Million Forecast Revenue (2033) USD 13,919.6 Million CAGR (2024-2032) 88.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Application(Commercial Charging Station, Home Charging Unit), By Component(Base Charging Pad, Power Control Unit, Vehicle Charging Pad), By Distribution Channel(Aftermarket, OE Market) , By Charging Type(Dynamic Wireless Charging System, Stationary Wireless Charging System) , By Propulsion Type(BEV, PHEV), By Vehicle Type(Commercial Vehicle, Passenger Car) , By Power Supply Range(3–<11 kW, 11–50 kW, >50 kW), By Charging System(Magnetic Power Transfer, Capacitive Power Transfer, Inductive Power Transfer) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Robert Bosch GmbH, Continental AG, WiTricity Corporation, ZTE Corporation, HELLA KGaA Hueck & Co., Toyota Motor Corporation, Toshiba Corporation, Qualcomm, Inc., Evatran Group, Powermat Technologies Ltd., PowerbyProxi Limited, Energids Corp., WiBotic Inc., PowerSquare Inc., Aircharge, Tecnomen Corporation, Steca Elektronik GmbH, Lumen Australia, ECOtality, Momentum Dynamics, ZENS, Freewire Technologies, CIRCONTROL, Swiftmile Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Robert Bosch GmbH

- Continental AG

- WiTricity Corporation

- ZTE Corporation

- HELLA KGaA Hueck & Co.

- Toyota Motor Corporation

- Toshiba Corporation

- Qualcomm, Inc.

- Evatran Group

- Powermat Technologies Ltd.

- PowerbyProxi Limited

- Energids Corp.

- WiBotic Inc.

- PowerSquare Inc.

- Aircharge

- Tecnomen Corporation

- Steca Elektronik GmbH

- Lumen Australia

- ECOtality

- Momentum Dynamics

- ZENS

- Freewire Technologies

- CIRCONTROL

- Swiftmile

Our Clients

View Our Licence Options