Veterinary Diagnostics Market By Type (companion animals and food-producing animals), By End-User (veterinary hospitals & clinics, research institutions, and others), By Product (instruments, consumables, and services), By Food-producing animals (poultry, cattle, and others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

26868

-

March 2023

-

151

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Veterinary Diagnostics Market Report Overview

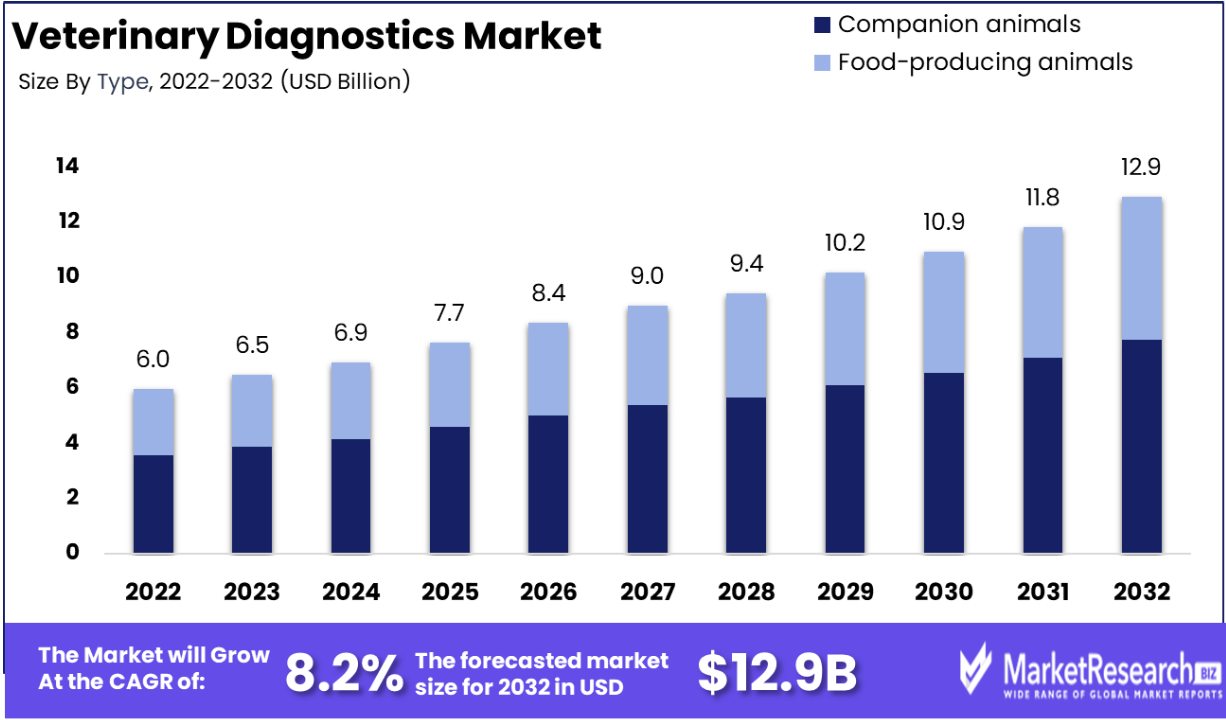

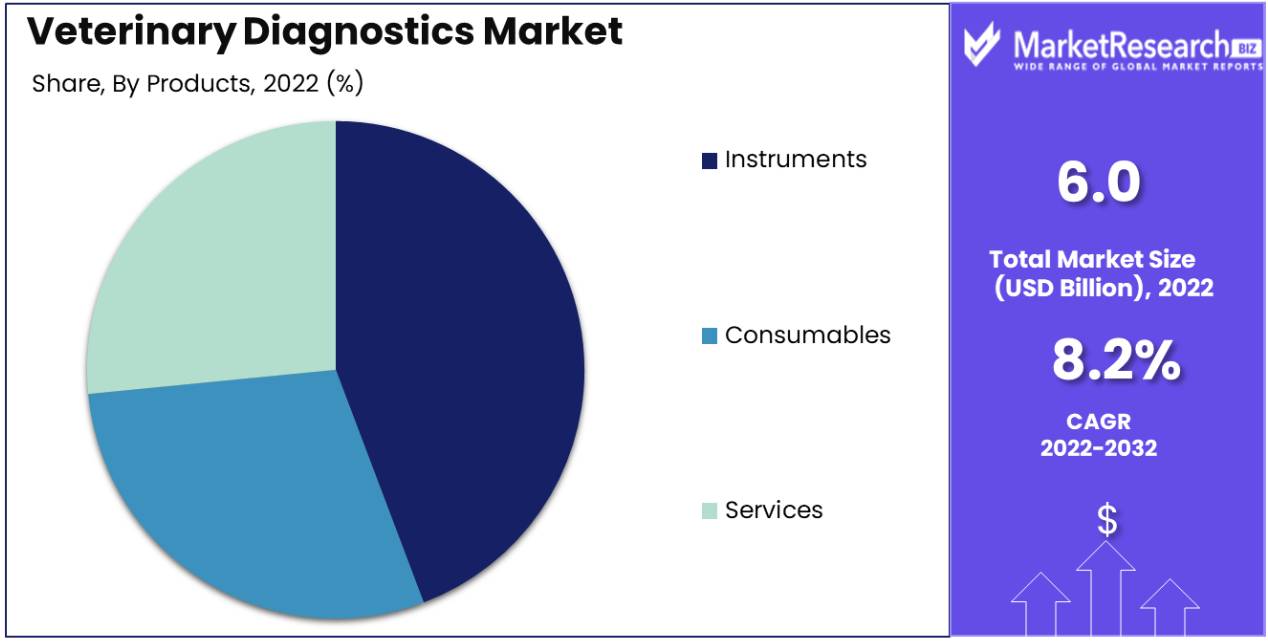

Veterinary Diagnostics Market size is expected to be worth around USD 12.9 Bn by 2032 from USD 6 Bn in 2022, growing at a CAGR of 8.2% during the forecast period from 2023 to 2032.

The veterinary diagnostics market plays a crucial role in the field of animal healthcare, offering critical insights into the health and well-being of animals. Veterinary diagnostics encompass a wide range of diagnostic tests and procedures used by veterinarians to diagnose, monitor, and manage various diseases and conditions in animals, thereby ensuring their welfare and the safety of the human population that interacts with them.

The Veterinary Diagnostics market in 2023 has witnessed significant developments that are reshaping the industry landscape. One of the most notable events was the acquisition of Abaxis by Zoetis, a prominent player in the veterinary pharmaceutical and diagnostics sector. Abaxis specializes in the development and manufacturing of veterinary diagnostic products. This strategic acquisition has expanded Zoetis' existing portfolio, enabling the company to offer veterinarians a more extensive range of diagnostic products and services. This move enhances Zoetis' position in the market, providing veterinarians with comprehensive solutions to improve patient care.

In the same year, IDEXX Laboratories, Inc. introduced a revolutionary innovation to the Veterinary Diagnostics market with the launch of the blood analyzer. This blood analyzer represents a significant leap forward in diagnostic technology, capable of conducting more than 100 tests on a single sample in a 20 minutes. This unparalleled speed and comprehensiveness make the IDEXX Catalyst One the fastest and most comprehensive blood analyzer available for veterinary use. IDEXX's innovation empowers veterinarians with the ability to quickly and accurately diagnose a wide range of conditions, enhancing the efficiency and effectiveness of veterinary care.

These recent developments highlight the dynamic nature of the Veterinary Diagnostics market in 2023. With Zoetis' strategic acquisition and IDEXX Laboratories' revolutionary technology, the industry is poised for continued growth and innovation, ultimately benefiting both veterinarians and their animal patients. As technology continues to advance and companies invest in expanding their product offerings, the future of veterinary diagnostics holds promise for improved care and diagnostic capabilities in the field of animal health.

The veterinary diagnostics market has witnessed significant growth in recent years, fueled by factors such as increased pet ownership, technological advancements, the rise of point-of-care diagnostics, and the emphasis on preventive care. Moreover, the convergence of human and animal health concerns, coupled with the integration of AI and machine learning, is expected to drive further expansion in the industry. As the veterinary diagnostics sector continues to evolve, it remains an integral component of the broader effort to ensure the health and well-being of animals and humans alike.

Driving factors

Increasing Demand for Animal Healthcare:

The escalating demand for animal healthcare services is a primary driving factor for the Veterinary Diagnostics Market. As pet ownership rates rise and the significance of livestock production expands globally, there is a concomitant increase in the need for accurate and timely diagnostic tools to ensure the well-being of animals.

Rising Incidence of Zoonotic Diseases:

The surge in zoonotic diseases, which are illnesses transmissible between animals and humans, necessitates the development and utilization of advanced diagnostic methods. This trend emphasizes the importance of veterinary diagnostics in identifying and managing diseases that pose a public health risk.

Technological Advancements:

Continuous advancements in diagnostic technologies such as PCR (Polymerase Chain Reaction), ELISA (Enzyme-Linked Immunosorbent Assay), and imaging techniques like MRI (Magnetic Resonance Imaging) have significantly improved the accuracy and efficiency of veterinary diagnostics. These innovations drive market growth by enhancing diagnostic capabilities.

Growing Role of Innovative Technologies in Animal Healthcare:

The Veterinary Diagnostics Market is influenced by the growing adoption of innovative technologies. Point-of-care testing, telemedicine, and wearable devices for animals are examples of innovative solutions that are transforming the landscape of animal healthcare, increasing the need for sophisticated diagnostic tools.

Restraining Factors

High Cost of Veterinary Diagnostics Tests:

The veterinary diagnostics market faces a significant restraint in the form of the high cost associated with diagnostic tests. Advanced diagnostic technologies, such as molecular diagnostics and imaging modalities, require substantial investments in equipment and reagents. This cost is often passed on to pet owners and livestock producers, making these diagnostics less accessible for some segments of the population. The economic constraints may discourage individuals from seeking timely diagnostics for their animals, potentially leading to delayed or inadequate healthcare interventions.

Limited Availability of Diagnostic Tests for Certain Diseases:

Another constraint in the veterinary diagnostics market is the limited availability of diagnostic tests for certain diseases. While there has been substantial progress in developing diagnostic tools for common ailments, such as respiratory infections and gastrointestinal disorders, there remains a gap in diagnostic solutions for less prevalent or emerging diseases. The development and validation of diagnostic assays for rare or emerging diseases can be challenging due to limited sample availability and insufficient research funding. Consequently, veterinarians may face difficulties in accurately diagnosing and managing these conditions, impacting animal health and potentially posing zoonotic risks.

Lack of Skilled Professionals:

The shortage of skilled professionals in the field of veterinary diagnostics is a significant restraining factor. Performing and interpreting diagnostic tests require specialized training and expertise. The shortage of qualified veterinary diagnosticians and laboratory technicians hinders the efficient delivery of diagnostic services. This shortage of skilled personnel not only affects the accuracy and efficiency of diagnostics but also limits the adoption of cutting-edge diagnostic techniques in veterinary medicine.

By Type Analysis

In the veterinary diagnostics industry, the market can be divided into two primary segments: companion animals and food-producing animals.

The companion animal segment has a major share of the veterinary diagnostics market. This segment encompasses pets like dogs, cats, and other small animals, which are considered members of the family by many households. The demand for diagnostic services and products for companion animals is consistently high, driven by factors such as increased pet ownership, the growing awareness of pet health, and advancements in veterinary medicine.

On the other hand, the food-producing animals primarily pertains to animals raised for food production, such as cattle, poultry, swine, and other livestock. This category is equally crucial but distinct, as it deals with ensuring the health and well-being of animals that contribute to the global food supply chain. Diagnostic tools and services for this segment are vital for disease prevention, early detection, and maintaining the quality of animal-derived products.

By End-user Analysis

The largest share within this market is attributed to the Veterinary hospitals & clinics segment. Veterinary hospitals and clinics are at the forefront of animal healthcare, routinely employing diagnostic services and tools to provide accurate assessments and treatment plans for pets and animals under their care. The high demand for diagnostics in this segment is driven by the need for timely and precise diagnoses, which are essential for ensuring the well-being of animals.

Additionally, the segments encompasses a diverse range including research institutions, reference laboratories, and point-of-care testing or in-house testing facilities. These institutions play a critical role in advancing veterinary medicine, conducting research, and offering specialized diagnostic services. Reference laboratories, in particular, are instrumental in providing comprehensive diagnostic solutions. They are also expected to show rapid growth in the forecast period.

By Product Analysis

Veterinary diagnostics is a lucrative market with a vast selection of products tailored to animal healthcare requirements. The instruments segment is the market leader, accounting for the greatest share. This segment's growth can be attributed to the increasing prevalence of zoonotic diseases and the rising frequency of animal health examinations. In addition, the development of diagnostic technologies and the rising demand for early diagnosis and preventative healthcare are propelling the expansion of this market segment.

As the importance of pet healthcare continues to grow, pet owners are willing to spend more on diagnostic services. Analyzers, test packages, reagents, and consumables are among the numerous products offered by the instruments segment. These items are indispensable for the diagnosis and early detection of animal maladies. In addition, pet owners are becoming increasingly aware of the significance of early diagnosis, which drives the demand for these products.

In the coming years, the instruments subsegment of the veterinary diagnostics market is projected to grow at the highest rate. The development of new products that are more accurate, dependable, and efficient than conventional diagnostic instruments is the result of technological advancements. In addition, the rising demand for animal healthcare and early diagnosis is anticipated to fuel the expansion of this market segment over the next few years.

Key Market Segments

Type

- Companion animals

- Food-producing animals.

End-User

- Veterinary hospitals & clinics

- Research institutions

- Reference laboratories

- Point-of-care testing/in-house testing

Product

- Instruments

- Consumables

- services

Food-producing animals

- Poultry

- Cattle

- Sheep & goat

- Pigs

- Other food-producing animals

Growth Opportunity

Growing Awareness of Animal Welfare

The increasing awareness and concern for animal welfare have led to higher standards of care, prompting the need for comprehensive diagnostics. Consumers, regulatory bodies, and veterinary professionals are placing greater emphasis on early disease detection and preventive healthcare, driving the demand for advanced diagnostic solutions.

Advancements in Veterinary Molecular Diagnostics

The Veterinary Diagnostics Market is experiencing growth due to significant advancements in veterinary molecular diagnostics. These technologies enable the rapid and accurate detection of pathogens and genetic markers, enhancing the overall diagnostic capabilities in veterinary medicine.

Point-of-Care (POC) Diagnostics

The adoption of Point-of-Care (POC) diagnostics in veterinary practice is a key driving factor. POC diagnostics offer immediate test results, reducing turnaround time for diagnosis and treatment decisions. This convenience and speed are increasingly valued by veterinarians and pet owners alike.

Latest Trends

Increased Expenditure on Animal Health

In recent years, there has been a noteworthy surge in expenditure on animal health. Pet owners, livestock producers, and animal enthusiasts are increasingly recognizing the importance of proactive healthcare measures for animals. This trend is driven by a growing awareness of zoonotic diseases, concerns about animal welfare, and the desire for longer, healthier lives for pets and production animals. Consequently, the veterinary diagnostics market is experiencing a boost as more resources are allocated to diagnostics, preventive care, and regular check-ups.

Growing Demand for Veterinary Imaging

The veterinary diagnostics market is witnessing a robust demand for advanced imaging technologies. Pet owners and veterinarians alike are seeking more accurate and comprehensive diagnostic solutions. This trend is driven by the availability of cutting-edge imaging modalities such as MRI (Magnetic Resonance Imaging), CT (Computed Tomography), and advanced ultrasound systems in veterinary clinics. These technologies enable precise diagnosis of various medical conditions, including musculoskeletal disorders, cancers, and neurological ailments, thereby facilitating targeted treatment strategies. The growing demand for veterinary imaging is not only enhancing diagnostic capabilities but also expanding the scope of veterinary services offered.

The Development of Non-Invasive Diagnostic Tests

Traditionally, invasive procedures such as biopsies and surgical interventions were commonly employed for diagnosis, but there is now a paradigm shift towards less invasive and stress-free diagnostic methods. Non-invasive diagnostic tests, including blood tests, urine analysis, and molecular diagnostics, are gaining prominence due to their reduced patient discomfort and quicker results. These tests provide valuable insights into various diseases, such as infectious diseases, endocrine disorders, and genetic conditions. The shift towards non-invasive diagnostics is improving the overall diagnostic experience for animals and encouraging earlier disease detection and intervention.

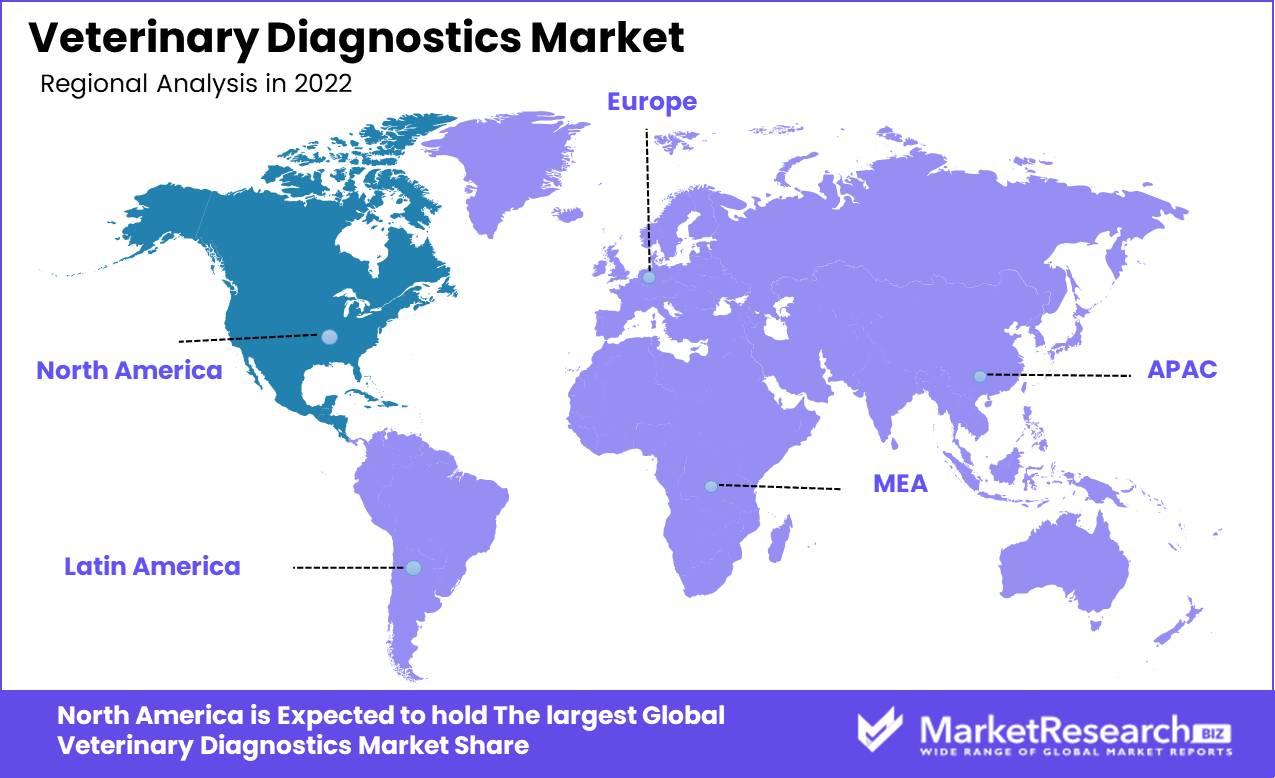

Regional Analysis

North America is expected to dominate due to rising healthcare costs, an increase in the incidence of veterinary diseases, and an increase in pet ownership. The expansion can be attributed to key factors such as a rise in pet ownership, a greater awareness of animal health, and positive government initiatives relating to animal health.

Increased expenditure on animal healthcare has been a major factor in the expansion of the North American veterinary diagnostics market. The increasing awareness of animal health and welfare has prompted pet owners to seek out improved medical care for their furry companions. Advanced technologies, such as molecular diagnostic testing, imaging, and rapid diagnostics, are transforming the veterinary diagnostics industry. These developments allow for the timely and accurate diagnosis of animal diseases, resulting in improved treatment outcomes.

In recent years, the incidence of veterinary diseases has increased in North America. It is alarming that diseases like rabies, Lyme disease, and heartworm are on the rise. This has increased the demand for diagnostic and testing services for animals. As a result, veterinary clinics and animal hospitals have begun investing in modern diagnostic instruments to provide pet owners with dependable and precise test results.

The increase in pet ownership in North America has been a significant factor in the market's expansion. Over 67% of U.S. households own at least one companion, and this percentage increases annually. It is anticipated that the rising demand for diagnostic services will continue to rise as the number of canines continues to rise.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the future years, the veterinary diagnostics market is anticipated to expand at a significant rate. The leading players in this market are investing in R&D to introduce new products and services to satisfy the market's growing demand. These players are focused on developing sophisticated diagnostic technologies that provide accurate results in a shorter amount of time.

Zoetis, Abaxis, IDEXX Laboratories, Heska Corporation, Thermo Fisher Scientific, Inc., Virbac, Bio-Rad Laboratories, Inc., Neogen Corporation, IDEXX Laboratories, and VCA Inc. are some of the major key participants in the veterinary diagnostics market. Zoetis is considered the market leader in veterinary diagnostics because it provides a vast array of products and services. Due to its extensive product offering and high-quality services, the company has a strong presence on the market.

Another major participant in the veterinary diagnostics market is IDEXX Laboratories. The company has a dominant presence on the U.S. market and is committed to expanding its operations internationally. IDEXX Laboratories provides numerous diagnostic products and services for companion animals, livestock, and poultry.

Heska Corporation's diagnostic products and services are renowned for their innovation. The company provides a variety of products, including chemistry, haematology, and immunoassay analyzers. Heska Corporation is committed to enhancing the standard of veterinary care by offering precise and dependable eterinary Diagnostics market

To gain a larger market share, key players are implementing business strategies such as diverse product offerings, regional expansion, business expansion, joint ventures, and new product launches.

- ABAXIS Inc.

- Thermo Fisher Scientific Inc.

- Heska Corporation

- VCA Inc.

- Neogen Corporation

- Zoetis Inc.

- ID.Vet.

- IDEXX Laboratories Inc

- Mindray Medical International Ltd.

- Virbac

- GE Healthcare

- Agfa Healthcare

- Randox Laboratories Ltd.

- Agrolabo S.P.A

Recent Development

- In 2023, Iowa State University’s Veterinary Diagnostic Laboratory implements a 384-sample automated system operating 24/7 with minimal staffing. This automation significantly improves diagnostic testing efficiency and throughput.

- In 2023, IDEXX Laboratories, a global veterinary diagnostics company, develops a new Cystatin B Test detecting kidney injuries earlier in cats and dogs, improving treatment prospects.

- In 2023, IDEXX Laboratories plans to initiate the Cystatin B Test in the United States and Canada, with 2024 European introduction. This strategic rollout provides advanced kidney diagnostics access to veterinarians and pet owners across multiple regions.

- In 2021, IDEXX Laboratories, Inc. introduces the SNAP Heartworm RT Test for faster, more accurate canine heartworm disease diagnosis, allowing earlier detection and treatment.

Report Scope:

Report Features Description Market Value (2022) USD 6 Bn Forecast Revenue (2032) USD 12.9 Bn CAGR (2023-2032) 8.2% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, Largest Market Share, COVID-19 Impact, Market Opportunity, Industry Trends, Competitive Landscape, Recent Developments Segments Covered Type: companion animals, food-producing animals

End-User: veterinary hospitals & clinics, research institutions, reference laboratories, point-of-care testing/in-house testing

Product: instruments, consumables, and services

Food-producing animals: poultry, cattle, sheep & goat, pigs, other food-producing animalsRegional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of Asia-Pacific Region; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape ABAXIS Inc., Thermo Fisher Scientific Inc., Heska Corporation, VCA Inc., Neogen Corporation, Zoetis Inc., ID.Vet., IDEXX Laboratories, Mindray Medical International Ltd., Virbac, GE Healthcare, Agfa Healthcare, Agrolabo S.P.A. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- ABAXIS Inc.

- Thermo Fisher Scientific Inc.

- Heska Corporation

- VCA Inc.

- Neogen Corporation

- Zoetis Inc.

- ID.Vet.

- IDEXX Laboratories Inc

- Mindray Medical International Ltd.

- Virbac

- GE Healthcare

- Agfa Healthcare

- Randox Laboratories Ltd.

- Agrolabo S.P.A

Our Clients

View Our Licence Options