Urgent Care Apps Market By Product (Emergency Care Triage Apps, In-hospital Communication Apps, Post-hospital Apps), By Clinical Area (Trauma, Cardiac Conditions, Stroke, Other Clinical Areas), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46152

-

April 2024

-

137

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

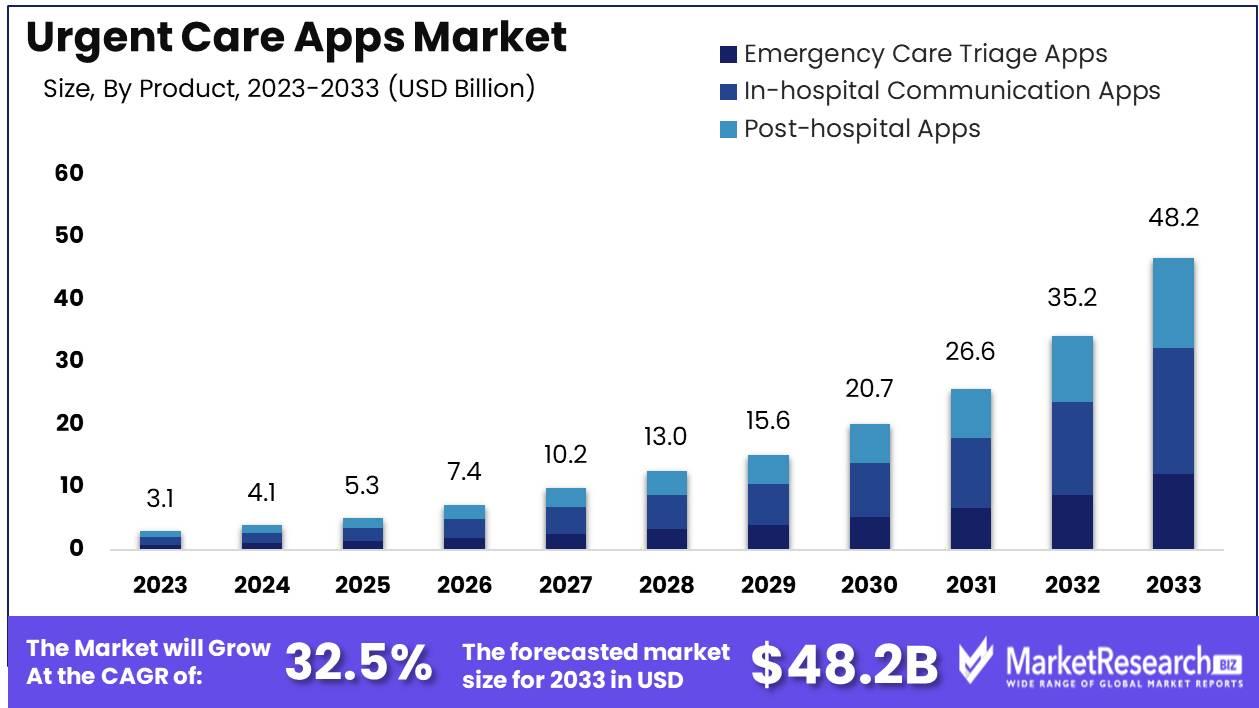

The Global Urgent Care Apps Market was valued at USD 3.1 Bn in 2023. It is expected to reach USD 48.2 Bn by 2033, with a CAGR of 32.5% during the forecast period from 2024 to 2033.

The Urgent Care Apps Market refers to a rapidly evolving sector within the digital health landscape, focusing on applications designed to provide timely medical assistance and triage services to users in need of urgent care. These innovative platforms leverage advanced technologies such as AI-driven symptom assessment, telemedicine consultations, and real-time medical guidance to deliver convenient and efficient healthcare solutions. With the growing demand for accessible and responsive healthcare services, the Urgent Care Apps Market presents significant opportunities for healthcare providers, tech developers, and investors alike to enhance patient outcomes, streamline care delivery, and transform the future of urgent medical assistance.

As an analyst observing the Urgent Care Apps Market, it's evident that the landscape is experiencing significant growth and transformation, fueled by technological advancements and shifting consumer preferences. The convergence of healthcare and digital solutions has led to the emergence of urgent care apps as a pivotal component of the healthcare ecosystem. With convenience and accessibility becoming paramount concerns for patients, these apps offer a viable alternative to traditional healthcare delivery models, providing on-demand medical services remotely.

Supportive data underscores the burgeoning adoption of telehealth digital solutions, with a notable 54% of adults in the United States having utilized such platforms. This widespread acceptance reflects a fundamental shift in healthcare-seeking behavior, where individuals increasingly rely on digital channels for their medical needs. Furthermore, the success of wellness apps, which generated a substantial $950 million in revenue in 2023 with over 50 million users, highlights the immense market potential and appetite for digital health solutions.

The meteoric rise of telehealth digital solutions, as evidenced by the robust adoption rates among American adults, underscores a paradigm shift in healthcare delivery. This shift is further accentuated by the noteworthy revenue generated by wellness apps, indicative of a burgeoning market ripe for exploration and investment. As traditional healthcare models undergo a digital transformation, urgent care apps stand poised to redefine patient experiences and reshape the competitive landscape.

Key Takeaways

- Market Growth: The Global Urgent Care Apps Market was valued at USD 3.1 Bn in 2023. It is expected to reach USD 48.2 Bn by 2033, with a CAGR of 32.5% during the forecast period from 2024 to 2033.

- By Product: In-hospital communication apps hold a 41.2% share, crucial for enhancing coordination and efficiency within healthcare facilities.

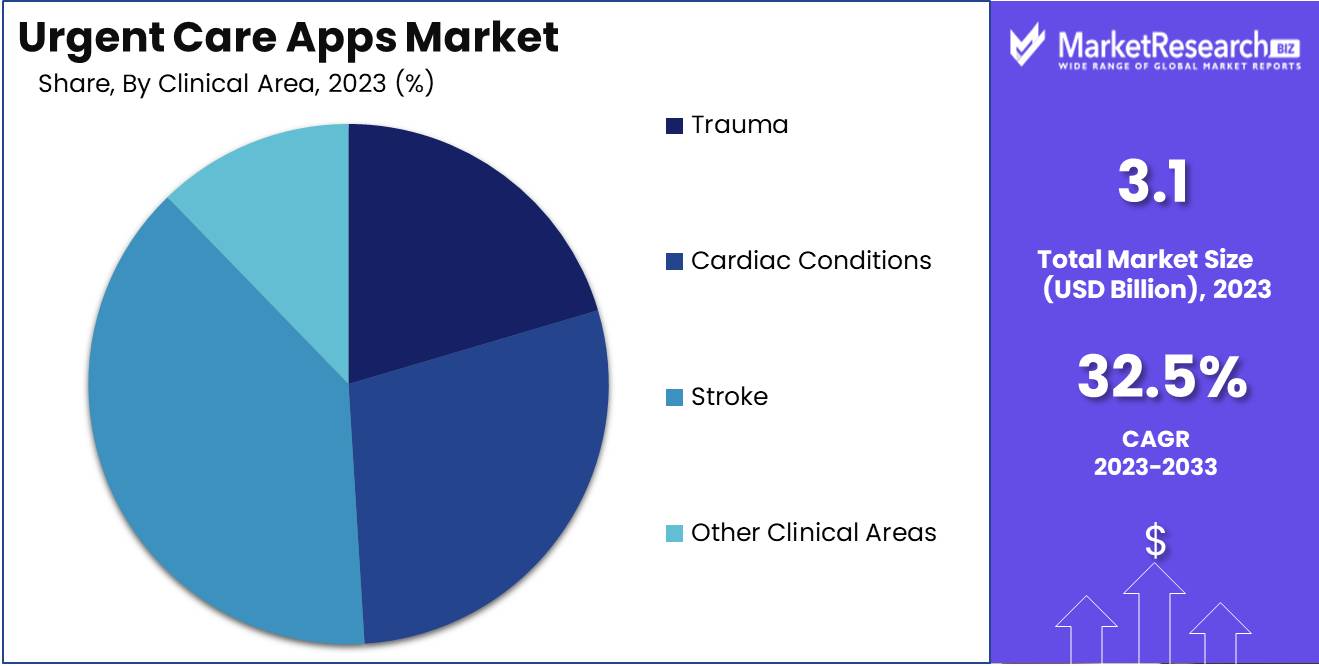

- By Clinical Area: Stroke-related applications dominate with 47.4%, reflecting the urgent need for rapid response and specialized care in stroke management.

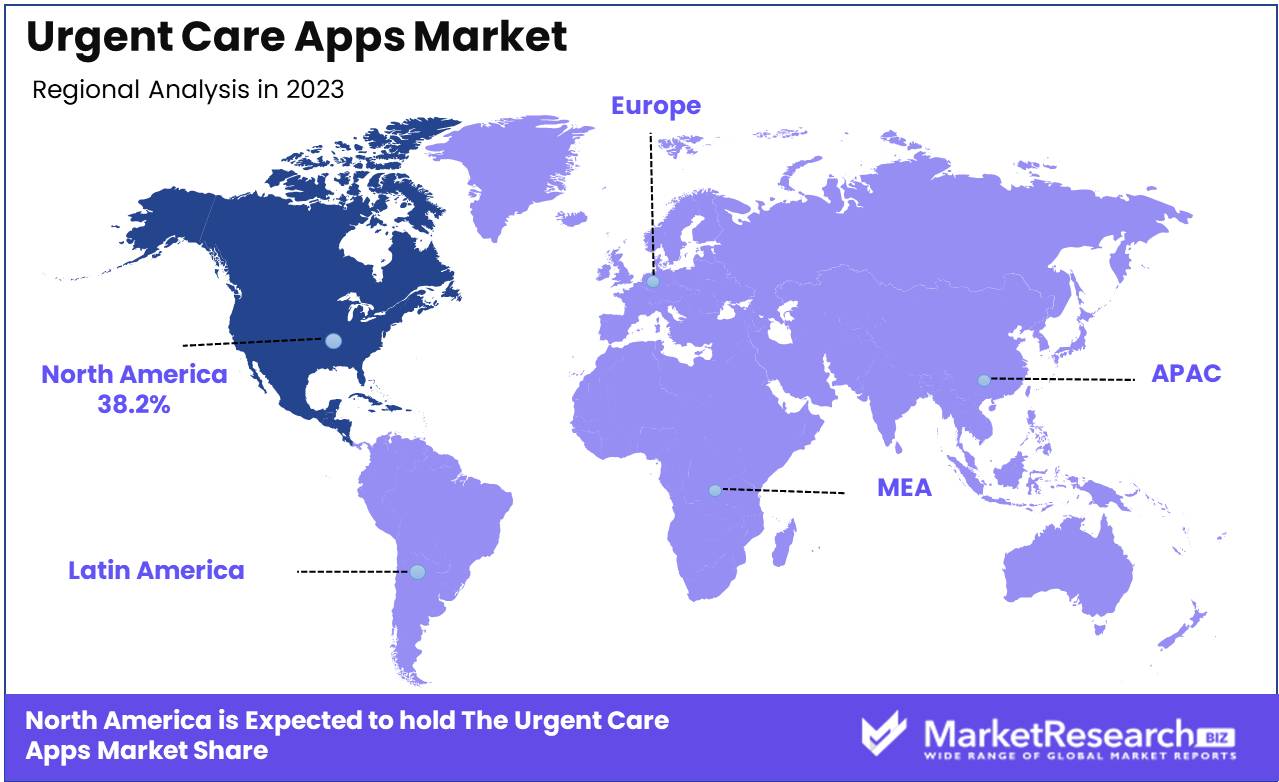

- Regional Dominance: North America commands 38.2% of the urgent care apps market, driven by advanced healthcare infrastructure and high adoption rates.

- Growth Opportunity: The urgent care apps market has significant growth potential through innovations in real-time patient monitoring, AI-driven diagnostics, and expanding access to telehealth services.

Driving factors

Patient-centered Care Preference and 4G/5G Adoption

The convergence of patient-centered care preference and the widespread adoption of 4G/5G networks has been a significant catalyst for the growth of the Urgent Care Apps Market. Patients today seek convenience, accessibility, and personalized healthcare experiences, which align perfectly with the capabilities offered by urgent care apps. With the advent of 4G and now 5G networks, users can access these apps seamlessly, enabling real-time consultations, symptom tracking, and appointment scheduling from the comfort of their homes or on the go. This convenience factor not only enhances patient satisfaction but also encourages more individuals to engage with urgent care services, thus expanding the market.

Moreover, the combination of patient-centered care and advanced network technologies has facilitated the development of innovative features within urgent care apps. These apps can now offer functionalities such as telemedicine consultations, remote monitoring of vital signs, and medication reminders, providing comprehensive healthcare solutions to users.

Rise in Chronic Conditions

The rise in chronic conditions globally has been a driving force behind the expansion of the Urgent Care Apps Market. As the prevalence of conditions such as diabetes, hypertension, and cardiovascular diseases continues to escalate, there is a growing need for convenient and efficient healthcare solutions to manage these conditions effectively. Urgent care apps offer patients with chronic illnesses a platform to monitor their health status regularly, receive timely interventions, and access educational resources to better manage their conditions. This proactive approach not only improves patient outcomes but also reduces the burden on traditional healthcare systems by preventing unnecessary emergency room visits.

Furthermore, the rise in chronic conditions has prompted healthcare providers and policymakers to explore innovative strategies for delivering care, including the integration of digital health technologies. Urgent care apps play a crucial role in this paradigm shift by serving as a bridge between patients and healthcare providers, facilitating continuous communication, and enabling remote management of chronic conditions.

Restraining Factors

Data Privacy and Security Concerns

Data privacy and security concerns represent significant challenges for the growth of the Urgent Care Apps Market. As the use of digital health platforms proliferates, patients and healthcare providers alike are increasingly wary of potential breaches of sensitive medical information. In an era where data breaches and cyberattacks are prevalent, ensuring the privacy and security of patient data is paramount for the widespread adoption of urgent care apps. Concerns regarding unauthorized access to personal health information, data breaches, and the potential misuse of sensitive medical data can erode trust in these platforms, hindering market growth.

Addressing data privacy and security concerns requires robust measures to safeguard patient information throughout the entire lifecycle of urgent care app usage. This includes implementing encryption protocols, access controls, secure authentication mechanisms, and compliance with stringent data protection regulations such as HIPAA (Health Insurance Portability and Accountability Act) in the United States. By prioritizing data privacy and security, urgent care app developers can instill confidence in both patients and healthcare providers, fostering greater adoption and utilization of these platforms.

Interoperability Issues Between Systems

Interoperability issues pose another challenge to the growth of the Urgent Care Apps Market, particularly concerning the seamless exchange of data between different healthcare systems and platforms. In the complex landscape of healthcare IT, numerous proprietary systems and electronic health record (EHR) platforms often lack interoperability, leading to fragmented data silos and inhibiting the efficient sharing of patient information. This lack of interoperability can impede the effectiveness of urgent care apps, as healthcare providers may struggle to access comprehensive patient records or coordinate care seamlessly across different platforms.

By Product Analysis

In the By Product segment of the Urgent Care Apps Market, In-hospital Communication Apps secured more than 41.2% market share, showing their dominance.

In 2023, In-hospital Communication Apps held a dominant market position in the By Product segment of the Urgent Care Apps Market, capturing more than a 41.2% share. This substantial market share underscores the critical role these apps play in enhancing communication and operational efficiency within hospital settings. The increasing demand for streamlined communication among healthcare professionals, driven by the necessity for quick and accurate information exchange, has significantly contributed to the dominance of In-hospital Communication Apps.

Emergency Care Triage Apps also played a pivotal role in the Urgent Care Apps Market. These apps facilitate the prioritization of patients based on the severity of their condition, ensuring that those in critical need receive prompt attention. The rise in emergency care visits and the need for efficient patient management systems have bolstered the adoption of these apps.

Post-hospital Apps focus on patient care continuity after discharge from healthcare facilities. These apps are designed to aid in recovery, monitor patient progress, and reduce the rate of hospital readmissions by providing patients with necessary resources and support. Although their market share is growing, it remains smaller compared to In-hospital Communication Apps.

By Clinical Area Analysis

Stroke captured over 47.4% market share in the Urgent Care Apps Market's By Clinical Area segment.

In 2023, Stroke held a dominant market position in the By Clinical Area segment of the Urgent Care Apps Market, capturing more than a 47.4% share. This significant market share underscores the critical role of urgent care apps in managing and addressing stroke cases promptly, as timely intervention is crucial in mitigating long-term effects and improving patient outcomes.

Trauma is another vital clinical area within the Urgent Care Apps Market, focusing on the immediate assessment and management of traumatic injuries. While Trauma apps play a crucial role in providing guidance to healthcare professionals in emergency situations, their market share remains lower compared to Stroke apps. However, with the rising incidence of accidents and injuries, the demand for Trauma apps is expected to grow steadily.

Cardiac Conditions encompass a range of urgent care needs related to heart health, including acute myocardial infarction, arrhythmias, and heart failure exacerbations. Urgent care apps tailored to cardiac emergencies aim to facilitate rapid diagnosis and treatment initiation, thereby improving patient outcomes. Despite their importance, Cardiac Conditions apps trail behind Stroke apps in market share, highlighting the prevalence and urgency of stroke cases in the urgent care setting.

The Other Clinical Areas segment encompasses a diverse range of urgent care needs, including respiratory distress, sepsis, and acute abdominal conditions. While these areas represent significant healthcare challenges, their individual market shares are smaller compared to Stroke, Trauma, and Cardiac Conditions apps. However, innovation and advancements in urgent care app technology continue to address the unique needs of these clinical areas, driving growth and adoption.

Key Market Segments

By Product

- Emergency Care Triage Apps

- In-hospital Communication Apps

- Post-hospital Apps

By Clinical Area

- Trauma

- Cardiac Conditions

- Stroke

- Other Clinical Areas

Growth Opportunity

Healthcare Provider Investments

Healthcare providers are significantly investing in digital health technologies to improve patient outcomes and streamline operations. The adoption of urgent care apps is a critical component of these investments. These apps facilitate rapid communication, efficient patient triage, and timely intervention, which are essential for managing acute care scenarios. The push for better healthcare delivery models is fueling the integration of urgent care apps into standard practice, thereby expanding their market potential.

Demand for Remote Monitoring and Telehealth

The COVID-19 pandemic has accelerated the adoption of remote monitoring and telehealth services. Patients and healthcare providers alike have recognized the convenience and efficacy of virtual consultations and remote patient management. Urgent care apps play a pivotal role in this ecosystem by providing immediate access to care, reducing the need for in-person visits, and enabling continuous health monitoring. This shift towards remote healthcare services is expected to drive the demand for urgent care apps, making them indispensable tools in the modern healthcare arsenal.

AI/ML Advancements for Diagnosis

Advancements in artificial intelligence (AI) and machine learning (ML) are revolutionizing the capabilities of urgent care apps. These technologies enhance diagnostic accuracy and decision-making processes, offering real-time insights and predictive analytics. AI-driven features in urgent care apps can assist in early diagnosis, personalized treatment plans, and proactive health management, thereby improving patient outcomes and satisfaction. The integration of AI and ML in urgent care apps not only boosts their functionality but also expands their appeal to both healthcare providers and patients.

Latest Trends

EHR Integration for Data Management

One of the most significant trends in the urgent care apps market is the integration of Electronic Health Records (EHR) for enhanced data management. EHR integration allows urgent care apps to seamlessly access and update patient medical histories, ensuring that healthcare providers have real-time, comprehensive data at their fingertips. This integration not only improves the accuracy and efficiency of patient care but also facilitates better coordination among healthcare providers.

As interoperability standards continue to evolve, the ability of urgent care apps to integrate with EHR systems will become increasingly critical, driving their adoption and utility in clinical settings.

Emphasis on Preventive Care and Wellness

Another major trend influencing the urgent care apps market is the growing emphasis on preventive care and wellness. Modern healthcare strategies are increasingly focused on preventing illnesses rather than merely treating them. Urgent care apps are evolving to support this shift by incorporating features that promote health monitoring, early detection of potential health issues, and wellness tracking.

These apps can offer personalized health insights, reminders for routine check-ups, and educational resources to encourage healthy lifestyles. By facilitating proactive health management, urgent care apps are aligning with broader healthcare objectives and improving patient outcomes.

Regional Analysis

North America leads the urgent care apps market, holding a 38.2% share.

North America dominates the urgent care apps market, accounting for 38.2% of the global share. This region's leadership can be attributed to its advanced healthcare infrastructure, high adoption rates of digital health technologies, and significant investments in healthcare innovation. The presence of leading market players and a strong focus on integrating cutting-edge solutions, such as AI and EHR systems, further propel the market. The United States, in particular, is a key driver with its emphasis on improving healthcare accessibility and patient outcomes through technology.

Europe represents a substantial portion of the urgent care apps market, driven by the increasing digitization of healthcare systems and supportive government policies. Countries like the United Kingdom, Germany, and France are leading adopters of urgent care apps, focusing on enhancing patient care and operational efficiency.

The Asia Pacific region is experiencing rapid growth in the urgent care apps market, fueled by rising healthcare needs, expanding smartphone penetration, and increasing awareness of digital health solutions. Countries such as China, India, and Japan are at the forefront of this expansion, with significant investments in healthcare infrastructure and technology.

In the Middle East & Africa, the urgent care apps market is gradually gaining traction, supported by improving healthcare infrastructure and growing investments in digital health. Countries like the UAE and South Africa are making strides in adopting health technologies to address the challenges of accessibility and efficiency in healthcare delivery.

Latin America is also emerging as a promising market for urgent care apps, with countries such as Brazil and Mexico leading the charge. The region's focus on enhancing healthcare services through technology, coupled with increasing smartphone usage and internet penetration, is propelling market growth.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global urgent care apps market is projected to experience robust growth in 2024, driven by technological advancements and increasing demand for immediate healthcare access. Key players such as AlayaCare, TigerConnect, and Brave Care, Inc. are at the forefront of this transformation, leveraging innovative solutions to enhance patient care and streamline communication between healthcare providers.

AlayaCare stands out with its comprehensive home healthcare software, which integrates telehealth, remote patient monitoring, and mobile apps to provide a holistic approach to urgent care. Its focus on improving clinical outcomes and operational efficiencies makes it a significant player in this market.

TigerConnect is another critical player, known for its secure messaging and collaboration platform. By facilitating real-time communication among healthcare teams, TigerConnect enhances the coordination of urgent care services, thereby improving patient outcomes and reducing response times.

Brave Care, Inc. targets pediatric urgent care, offering both virtual and in-person services tailored for children. Its user-friendly app provides parents with easy access to pediatric experts, making it a trusted choice for urgent child healthcare needs.

Zocdoc, Inc. has revolutionized patient access to healthcare providers through its online booking platform. By enabling patients to find and book urgent care appointments swiftly, Zocdoc reduces waiting times and enhances patient satisfaction.

Stryker Corporation and Allm Inc. are notable for their contributions to medical technology and telemedicine, respectively. Stryker’s innovations in emergency medical equipment complement the urgent care ecosystem, while Allm’s focus on telemedicine solutions facilitates remote diagnosis and treatment.

Teladoc Health, Inc. is a pioneer in virtual healthcare, offering extensive telehealth services that include urgent care. Its widespread adoption and integration with various healthcare systems underscore its pivotal role in the market.

Epic Systems Corporation provides a robust electronic health record (EHR) platform that supports urgent care operations. Its interoperability features ensure seamless information flow between urgent care providers and other healthcare facilities.

Johnson & Johnson, a healthcare giant, brings significant influence through its diverse portfolio and investment in digital health initiatives. Its entry into urgent care apps indicates a strategic move to leverage its vast resources and expertise in improving urgent care services.

Argusoft and other key players continue to innovate and adapt to the evolving needs of the urgent care sector, contributing to a competitive and dynamic market landscape.

Market Key Players

- AlayaCare

- TigerConnect

- Brave Care, Inc

- Zocdoc, Inc.

- Stryker Corporation

- Allm Inc.

- Teladoc Health, Inc.

- Epic Systems Corporation

- Johnson & Johnson

- Argusoft

- Other Key Players

Recent Development

- In October 2023, Mirvie pioneers early prediction of pregnancy complications using genomics and AI. The recent increase in maternal mortality rates highlights the urgent need for innovation and investment in maternal health solutions.

- In October 2023, Arvest Bank leverages Thought Machine's cloud-native core banking and Google Cloud's AI to enhance customer experience and fraud protection, transforming their digital banking services for improved customer interactions.

Report Scope

Report Features Description Market Value (2023) USD 3.1 Bn Forecast Revenue (2033) USD 48.2 Bn CAGR (2024-2033) 32.5% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Emergency Care Triage Apps, In-hospital Communication Apps, Post-hospital Apps), By Clinical Area (Trauma, Cardiac Conditions, Stroke, Other Clinical Areas) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape AlayaCare, TigerConnect, Brave Care, Inc, Zocdoc, Inc., Stryker Corporation, Allm Inc., Teladoc Health, Inc., Epic Systems Corporation, Johnson & Johnson, Argusoft, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- AlayaCare

- TigerConnect

- Brave Care, Inc

- Zocdoc, Inc.

- Stryker Corporation

- Allm Inc.

- Teladoc Health, Inc.

- Epic Systems Corporation

- Johnson & Johnson

- Argusoft

- Other Key Players

Our Clients

View Our Licence Options