Unidirectional Tapes Market Report By Material Type (Carbon Fiber, Glass Fiber, Aramid Fiber, Natural Fiber, Others), By Resin Type (Thermoset Resin, Thermoplastic Resin, Others), By Application (Aerospace, Automotive, Wind Energy, Sports and Recreation, Marine, Construction, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46198

-

May 2024

-

325

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

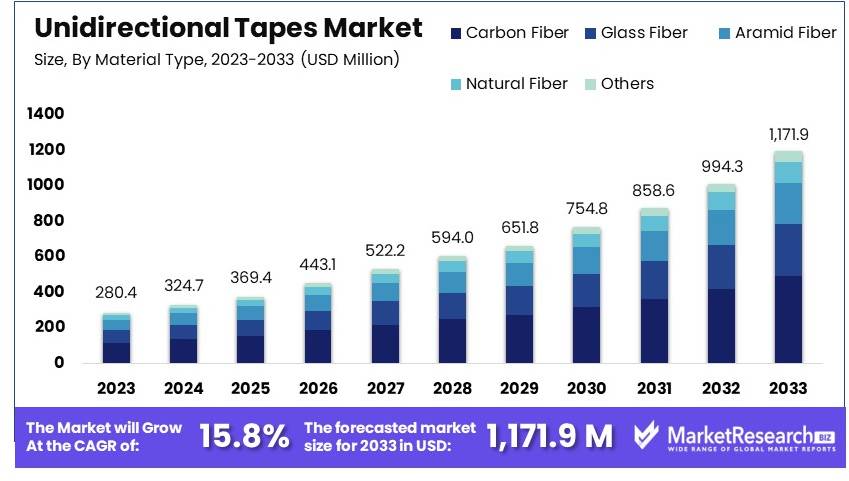

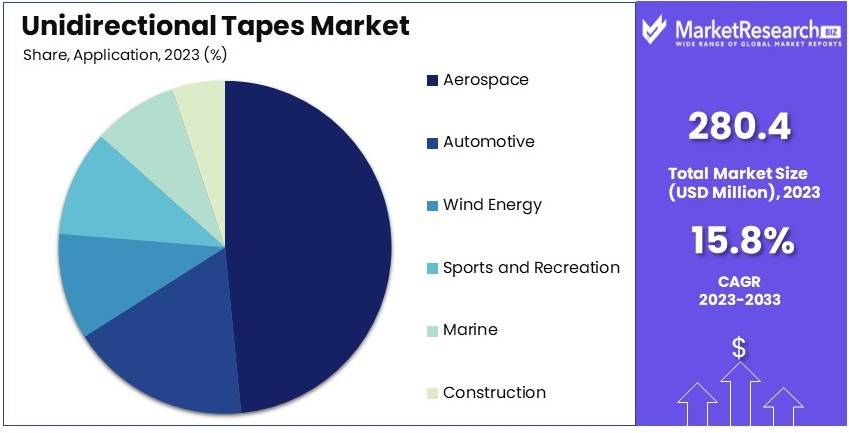

The Global Unidirectional Tapes Market size is expected to be worth around USD 1,171.9 million by 2033, from USD 280.4 million in 2023, growing at a CAGR of 15.8% during the forecast period from 2024 to 2033.

The Unidirectional Tapes Market refers to the segment of the composites industry dedicated to the production and utilization of tapes with fibers predominantly oriented in one direction. These tapes offer exceptional strength and stiffness properties, making them ideal for applications requiring high performance and lightweight materials, such as aerospace, automotive, and sports equipment.

Key drivers of this market include the demand for lightweight and durable materials, increasing adoption of composites in various industries, and advancements in manufacturing technologies. Companies operating in this market focus on product innovation, strategic partnerships, and expanding their presence in emerging economies to capitalize on growth opportunities.

The Unidirectional Tapes Market is poised for substantial growth in the coming years, driven by a confluence of factors including technological advancements, increasing demand for lightweight materials, and burgeoning applications in aerospace and automotive industries. With the United States leading the world in satellite launches and placement in orbit in 2023, the demand for high-performance materials such as unidirectional tapes is expected to surge.

The US accounted for a staggering 109 launch attempts in 2023, far surpassing other key players in the space industry. This robust activity underscores the need for materials that offer exceptional strength-to-weight ratios and durability, qualities that unidirectional tapes excel in providing.

Moreover, the recent report by SGL Group, a prominent manufacturer of unidirectional tapes, further corroborates the promising outlook for the market. Their projection of significant revenue and size growth aligns with the industry's upward trajectory, indicating ample opportunities for stakeholders across the value chain. As companies like SGL Group continue to innovate and expand their product offerings, the market is expected to witness heightened competition and a flurry of strategic partnerships aimed at capturing market share and driving innovation.

In this landscape, market participants must remain vigilant, continuously monitoring industry dynamics, technological advancements, and shifting consumer preferences. Adapting swiftly to emerging trends and leveraging data-driven insights will be paramount for success in this rapidly evolving market. As the demand for lightweight, high-performance materials continues to escalate, the Unidirectional Tapes Market presents lucrative opportunities for forward-thinking companies to capitalize on the burgeoning demand and carve out a competitive edge in the global marketplace.

Key Takeaways

- Market Value: The Global Unidirectional Tapes Market is expected to be worth around USD 1.5 Billion by 2033, from USD 280.4 Million in 2023, growing at a CAGR of 15.8% during the forecast period from 2024 to 2033.

- Material Type Analysis: Carbon fiber dominates with 42% due to its superior properties and high demand in aerospace and automotive industries. Its strength-to-weight ratio and stiffness make it ideal for critical applications.

- Resin Type Analysis: Thermoplastic resin dominates with 70.8% due to its recyclability and suitability for high-demand applications in automotive, aerospace, and wind energy industries.

- Application Analysis: Aerospace dominates with 47.3% due to extensive use in aircraft manufacturing and the industry's focus on fuel efficiency and lightweight components.

- North America dominates with 41.1% market share, driven by advanced aerospace and automotive sectors, and strong emphasis on technological innovation.

- Europe holds 32.5% market share, characterized by robust investments in aerospace and automotive industries, and stringent environmental regulations.

- Analyst Viewpoint: The unidirectional tapes market is poised for significant growth driven by increasing demand for lightweight and durable materials across various industries, including aerospace, automotive, and wind energy.

- Growth Opportunities: Key players can capitalize on the growing demand for thermoplastic resins and carbon fiber materials by expanding product portfolios, enhancing manufacturing capabilities, and targeting emerging applications in renewable energy and sports industries.

Driving Factors

Increasing Demand from the Aerospace Industry Drives Market Growth

The aerospace industry's demand for unidirectional tapes significantly drives market growth. These tapes are valued for their exceptional strength-to-weight ratio and resistance to fatigue and impact. They are used in manufacturing critical aircraft components, including fuselages, wings, and empennages, to enhance structural integrity and reduce overall weight. The incorporation of unidirectional tapes allows for improved fuel efficiency and performance in aircraft.

Major manufacturers like Boeing and Airbus heavily rely on these materials. For example, the use of unidirectional tapes in Boeing's 787 Dreamliner and Airbus's A350 XWB has contributed to weight reduction and improved fuel efficiency by approximately 20%. As the aerospace sector continues to prioritize fuel efficiency and performance, the demand for unidirectional tapes is expected to rise, fostering further market growth. Additionally, the trend toward producing more lightweight and durable aircraft components underscores the pivotal role of unidirectional tapes in the aerospace industry's future. This interaction with advancements in aerospace technology further propels the market, making it a critical factor in its expansion.

Adoption in Automotive Lightweighting Initiatives Drives Market Growth

The automotive industry's shift towards lightweighting to improve fuel efficiency and reduce emissions significantly drives the growth of the unidirectional tapes market. These tapes are increasingly used in the manufacturing of structural components such as body panels and chassis parts due to their strength and stiffness, which contribute to reducing the overall vehicle weight. Leading automakers, including Tesla and other electric vehicle manufacturers, use unidirectional tapes extensively in their car bodies.

For instance, the Model S and Model X from Tesla feature unidirectional tape components to maximize range and performance. The global automotive industry’s push for sustainability and regulatory compliance with emission standards has accelerated the adoption of lightweight materials. In 2023, the automotive lightweight materials market was valued at $76.1 billion, and the incorporation of unidirectional tapes is a key factor in this trend. This widespread adoption enhances the market for unidirectional tapes, as they play a crucial role in achieving the desired balance of strength, durability, and reduced weight in modern vehicles. This trend aligns with the broader industry shift towards sustainable practices, reinforcing the market's growth trajectory.

Advancement in Renewable Energy Technologies Drives Market Growth

The advancement in renewable energy technologies significantly drives the growth of the unidirectional tapes market. The increasing demand for renewable energy sources such as wind turbines and solar panels has led to the adoption of unidirectional tapes in manufacturing blades and structural components. These tapes provide superior strength and durability, essential for producing larger and more efficient wind turbine blades and solar panel frames.

Companies like Vestas and SunPower depend on unidirectional tapes to enhance the performance and longevity of their products. For instance, the global wind turbine market, which was valued at $94.8 billion in 2022, relies heavily on advanced materials like unidirectional tapes for optimal performance. As renewable energy installations increase worldwide, the demand for robust and durable components grows, further driving the market for unidirectional tapes. Additionally, the shift towards sustainable energy solutions and the need for high-performance materials in renewable energy applications underscore the critical role of unidirectional tapes. This interaction with the renewable energy sector’s growth amplifies the market's expansion, making it a key factor in the industry’s future.

Restraining Factors

High Cost of Raw Materials and Production Restrains Market Growth

The high cost of raw materials and production is a significant restraint on the unidirectional tapes market. Unidirectional tapes use high-performance fibers like carbon fiber and glass fiber, which are more expensive than traditional materials. The production process is also complex and requires specialized equipment, increasing the overall cost. This high expense limits adoption, particularly in industries with strict budget constraints.

For instance, the price of carbon fiber can be as high as $10 to $12 per pound, compared to steel at less than $1 per pound. This price disparity makes it challenging for industries such as automotive and construction to integrate unidirectional tapes widely. Smaller companies and emerging applications may struggle to afford these costs, further limiting market expansion. Therefore, the high cost of materials and production remains a significant barrier, hindering the broader adoption and growth of the unidirectional tapes market.

Stringent Regulatory Requirements Restrain Market Growth

Stringent regulatory requirements significantly restrain the growth of the unidirectional tapes market. The aerospace and automotive industries, in particular, face strict regulations to ensure the safety and reliability of products using these tapes. Compliance with these regulations is often time-consuming and costly.

For example, obtaining certifications for aerospace components can take several months and require extensive testing and documentation. This process can be especially burdensome for smaller manufacturers or those entering the market, as it adds to their operational costs and delays product launches. In 2023, the cost of regulatory compliance in the aerospace industry was estimated to add up to 15% to product development costs. These stringent requirements can slow down innovation and limit market entry, restricting the overall growth of the unidirectional tapes market. Hence, regulatory barriers are a considerable challenge that manufacturers must navigate to achieve market expansion.

Material Type Analysis

Carbon fiber dominates with 42% due to its superior properties and high demand in aerospace and automotive industries.

The material type segment of the unidirectional tapes market includes carbon fiber, glass fiber, aramid fiber, natural fiber, and others. Carbon fiber dominates this segment due to its superior strength-to-weight ratio, high stiffness, and excellent fatigue resistance. These characteristics make carbon fiber ideal for demanding applications in aerospace, automotive, and wind energy. In 2023, carbon fiber accounted for approximately 42% of the market share within the material type segment. Its extensive use in the aerospace industry, for instance, in the manufacturing of aircraft components like wings and fuselages, drives its dominance. The increasing focus on fuel efficiency and performance in the aerospace and automotive industries further bolsters the demand for carbon fiber.

Glass fiber is another significant material type in the unidirectional tapes market. While it does not match the strength and stiffness of carbon fiber, it offers good mechanical properties at a lower cost, making it suitable for applications where cost efficiency is a priority. Glass fiber is commonly used in construction, sports and recreation, and marine industries. Aramid fiber, known for its exceptional impact resistance and toughness, finds applications in defense, aerospace, and automotive sectors, although its market share is smaller compared to carbon and glass fibers.

Natural fibers and other materials are emerging as environmentally friendly alternatives. Natural fibers, such as flax and hemp, are increasingly used in automotive and construction applications due to their biodegradability and sustainability. While they currently hold a smaller market share, the rising emphasis on sustainability and environmental regulations is expected to drive their growth.

Resin Type Analysis

Thermoplastic resin dominates with 70.8% due to its recyclability and suitability for various high-demand applications.

The resin type segment of the unidirectional tapes market is categorized into thermoset resin, thermoplastic resin, and others. Thermoplastic resin is the dominant sub-segment, accounting for 70.8% of the market share. Thermoplastic resins offer several advantages, including recyclability, ease of processing, and excellent impact resistance. These characteristics make thermoplastic resins highly suitable for applications in the automotive, aerospace, and wind energy industries. The increasing focus on sustainability and recycling in various industries further drives the demand for thermoplastic resins. Additionally, thermoplastic resins' ability to be re-melted and re-formed enhances their appeal in manufacturing processes that require high efficiency and adaptability.

Thermoset resins, while not as dominant as thermoplastic resins, still hold a significant share of the market. Thermoset resins are known for their excellent thermal and chemical resistance, making them ideal for applications requiring high durability and stability. They are extensively used in aerospace, marine, and construction industries. However, the non-recyclable nature of thermoset resins poses a limitation in markets with stringent environmental regulations.

Other resin types, although representing a smaller market share, include hybrid resins and bio-based resins. Hybrid resins combine the properties of both thermoplastic and thermoset resins, offering enhanced performance characteristics. Bio-based resins, derived from renewable sources, are gaining traction due to the increasing emphasis on sustainability and reducing carbon footprint.

Application Analysis

Aerospace dominates with 47.3% due to extensive use in aircraft manufacturing and focus on fuel efficiency.

The application segment of the unidirectional tapes market includes aerospace, automotive, wind energy, sports and recreation, marine, construction, and others. The aerospace sector is the largest application segment, accounting for 47.3% of the market share. The extensive use of unidirectional tapes in manufacturing critical aircraft components, such as wings, fuselages, and empennages, drives this dominance. The aerospace industry's focus on reducing weight and improving fuel efficiency significantly boosts the demand for unidirectional tapes. Additionally, the increasing production of commercial and military aircraft further propels market growth.

The automotive sector is another crucial application segment. Unidirectional tapes are used to manufacture lightweight structural components, such as body panels and chassis parts, enhancing fuel efficiency and reducing emissions. The rise of electric vehicles and stringent emission regulations contribute to the growing demand for unidirectional tapes in the automotive industry.

Wind energy is an emerging application segment, driven by the increasing adoption of renewable energy sources. Unidirectional tapes are used in manufacturing wind turbine blades, offering superior strength and durability. The global shift towards sustainable energy solutions and the construction of larger and more efficient wind turbines fuel the demand for unidirectional tapes in this sector.

Other application segments, including sports and recreation, marine, and construction, also contribute to market growth. In sports and recreation, unidirectional tapes are used to manufacture high-performance sporting goods like golf clubs, hockey sticks, and bicycles. In the marine industry, these tapes are used to construct lightweight and durable boat hulls. The construction industry utilizes unidirectional tapes for strengthening concrete structures and reinforcing materials.

Key Market Segments

By Material Type

- Carbon Fiber

- Glass Fiber

- Aramid Fiber

- Natural Fiber

- Others

By Resin Type

- Thermoset Resin

- Thermoplastic Resin

- Others

By Application

- Aerospace

- Automotive

- Wind Energy

- Sports and Recreation

- Marine

- Construction

- Others

Growth Opportunities

Development of Advanced Composite Materials Offers Growth Opportunity

The development of advanced composite materials presents a significant growth opportunity for the unidirectional tapes market. Continuous research and advancements in materials science, such as new high-performance fibers, resins, and nanocomposites, enable the production of lighter, stronger, and more durable unidirectional tapes.

These advanced materials open up new applications and markets, especially in aerospace and defense, where weight reduction and enhanced performance are crucial. Companies like Hexcel and Toray Industries are leading this innovation by investing in next-generation carbon fiber and resin systems. For instance, Hexcel’s advancements in carbon fiber technology are expected to boost the aerospace sector, providing materials that improve fuel efficiency and reduce emissions. This ongoing innovation in composite materials significantly drives the market potential for unidirectional tapes.

Adoption in Additive Manufacturing (3D Printing) Offers Growth Opportunity

The adoption of unidirectional tapes in additive manufacturing (3D printing) offers a promising growth opportunity. Integrating these tapes into 3D printing processes allows the creation of complex shapes and structures with tailored strength and stiffness properties. This capability can revolutionize various industries, including aerospace, automotive, and medical devices.

Companies like Stratasys and Desktop Metal are exploring the use of unidirectional tapes in their 3D printing technologies. These advancements enable the production of lightweight, high-performance components with intricate geometries. For example, Stratasys’ use of unidirectional tapes in 3D printing has led to the production of more efficient and durable aerospace parts. This integration of unidirectional tapes in additive manufacturing significantly enhances the market’s growth potential.

Trending Factors

Sustainability and Circular Economy Are Trending Factors

Sustainability and the circular economy model are trending factors in the unidirectional tapes market. There is a growing emphasis on sustainable practices and the development of recyclable and eco-friendly unidirectional tapes. Companies like Solvay and Toray Industries are investing in bio-based and recyclable tapes, responding to the increasing demand for sustainable solutions.

For example, Solvay’s development of bio-based unidirectional tapes for automotive applications is driven by the industry's shift towards reducing carbon footprints. Additionally, the implementation of efficient recycling and reuse processes further supports market growth. This trend towards sustainability significantly influences the market, aligning with global efforts to promote environmentally friendly products and practices.

Digitalization and Industry 4.0 Are Trending Factors

Digitalization and Industry 4.0 concepts are trending factors in the unidirectional tapes market. The integration of digital technologies and automation in manufacturing processes, such as automated tape laying and fiber placement, optimizes production, reduces waste, and improves product quality.

Companies like Hexcel and Cytec Solvay Group are leveraging these technologies to enhance their manufacturing capabilities. For example, Hexcel’s use of digital twin simulations and predictive analytics in production processes has led to more efficient and higher-quality unidirectional tapes. This digital transformation in manufacturing supports the growing demand for high-quality composite products and drives market expansion. Digitalization significantly impacts the market by improving operational efficiency and product innovation.

Regional Analysis

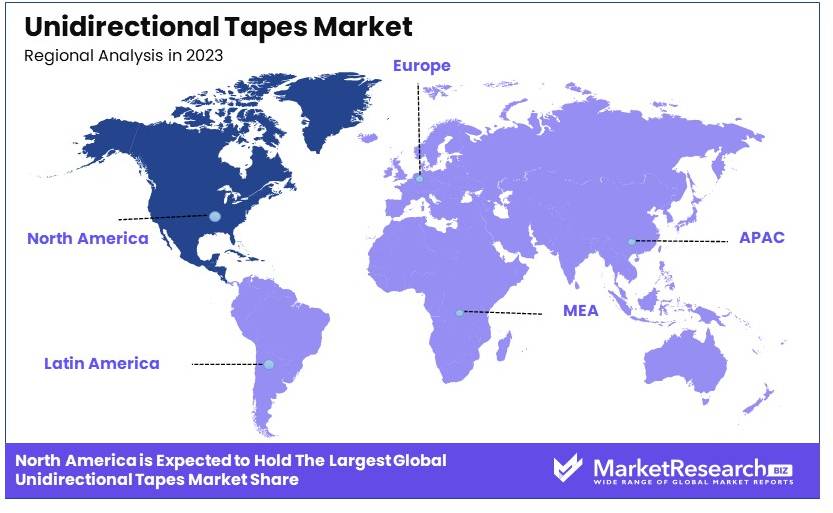

North America Dominates with 41.1% Market Share

North America holds a dominant position in the unidirectional tapes market, accounting for 41.1% of the market share. This dominance is driven by several key factors, including a strong aerospace industry, significant investments in research and development, and the presence of major market players such as Hexcel and Toray Industries. The region's advanced manufacturing capabilities and high demand for lightweight and high-performance materials in aerospace and automotive sectors further boost its market position.

Regional characteristics, such as robust infrastructure and a high level of technological adoption, positively influence market dynamics in North America. The region's well-established supply chain and regulatory support for advanced materials drive innovation and adoption of unidirectional tapes. Additionally, the growing emphasis on sustainability and the development of eco-friendly materials align with global trends, reinforcing the market's growth.

Market Share in Other Regions:

Europe: Europe accounts for 32.5% of the unidirectional tapes market share. The region's strong automotive industry and focus on lightweight materials drive its market position. Germany, in particular, leads with significant advancements in automotive manufacturing and materials science.

Asia Pacific: Asia Pacific holds 18.7% of the market share. The region's rapid industrialization, growing automotive and aerospace sectors, and increasing investments in renewable energy contribute to its market growth. China and Japan are key players in this region, driving demand for advanced composite materials.

Middle East & Africa: The Middle East & Africa region accounts for 5.1% of the market share. The region's growing construction industry and increasing investments in infrastructure projects contribute to the demand for unidirectional tapes, although the market is still developing compared to other regions.

Latin America: Latin America holds 2.6% of the market share. The region's market growth is driven by the automotive and construction sectors, with Brazil and Mexico being the primary contributors. However, economic challenges and lower technological adoption rates limit its market expansion.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the Unidirectional Tapes Market, key players such as SABIC, Hexcel Corporation, and Toray Industries, Inc. prominently influence market dynamics due to their extensive product offerings and global reach. These companies, alongside Evonik Industries AG and Solvay S.A., are pivotal in driving technological advancements and adoption of lightweight materials across various industries, including aerospace and automotive.

SABIC and Toray Industries, noted for their innovation in high-performance materials, lead in strategic market positioning by expanding their global footprint and investing in new production capabilities. Similarly, Hexcel Corporation and Celanese Corporation are crucial for their focus on R&D, enhancing the performance characteristics of unidirectional tapes.

Royal DSM and Arkema Group distinguish themselves through their commitment to sustainability and development of eco-friendly products, aligning with the growing demand for green manufacturing practices.

Smaller players like Owens Corning, TCR Composites, and Gurit Holding AG also contribute significantly by targeting niche applications and providing specialized solutions, which complements the broader range offered by larger firms.

Overall, the competitive landscape in the Unidirectional Tapes Market is characterized by a mix of innovation, strategic expansions, and a push towards sustainable practices, with each key player contributing uniquely to the industry’s growth and evolution.

Market Key Players

- SABIC

- Hexcel Corporation

- Evonik Industries AG

- Solvay S.A.

- Teijin Limited

- Celanese Corporation

- Royal DSM

- Owens Corning

- Arkema Group

- SGL Carbon

- Toray Industries, Inc.

- TCR Composites

- Gurit Holding AG

- Composites Evolution Ltd.

- 3M Company

Recent Developments

- On May 2024, SGL Group, a leading manufacturer of unidirectional (UD) tapes, released a report on the global UD tapes market, projecting significant revenue and size growth in the coming years.

- On January 2024, Avient, a global provider of specialized and sustainable material solutions, announced that it will debut its new Dyneema fiber at the upcoming JEC World 2023 trade show.

- On January 2023, the National Center for Advanced Materials Performance (NCAMP) qualified a new thermoplastic material system developed by Victrex, a leading provider of high-performance polymer solutions.

Report Scope

Report Features Description Market Value (2023) USD 280.4 Million Forecast Revenue (2033) USD 1,171.9 Million CAGR (2024-2033) 15.8% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material Type (Carbon Fiber, Glass Fiber, Aramid Fiber, Natural Fiber, Others), By Resin Type (Thermoset Resin, Thermoplastic Resin, Others), By Application (Aerospace, Automotive, Wind Energy, Sports and Recreation, Marine, Construction, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape SABIC, Hexcel Corporation, Evonik Industries AG, Solvay S.A., Teijin Limited, Celanese Corporation, Royal DSM, Owens Corning, Arkema Group, SGL Carbon, Toray Industries, Inc., TCR Composites, Gurit Holding AG, Composites Evolution Ltd., 3M Company Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- SABIC

- Hexcel Corporation

- Evonik Industries AG

- Solvay S.A.

- Teijin Limited

- Celanese Corporation

- Royal DSM

- Owens Corning

- Arkema Group

- SGL Carbon

- Toray Industries, Inc.

- TCR Composites

- Gurit Holding AG

- Composites Evolution Ltd.

- 3M Company

Our Clients

View Our Licence Options