Trivalent Chromium Finishing Market By System (Conversion Coatings, Plating, Passivation), By Application (Decorative, Functional), By End-use (Automotive, Oil & Gas, Aerospace, Hydraulics & Heavy Machinery, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46657

-

May 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

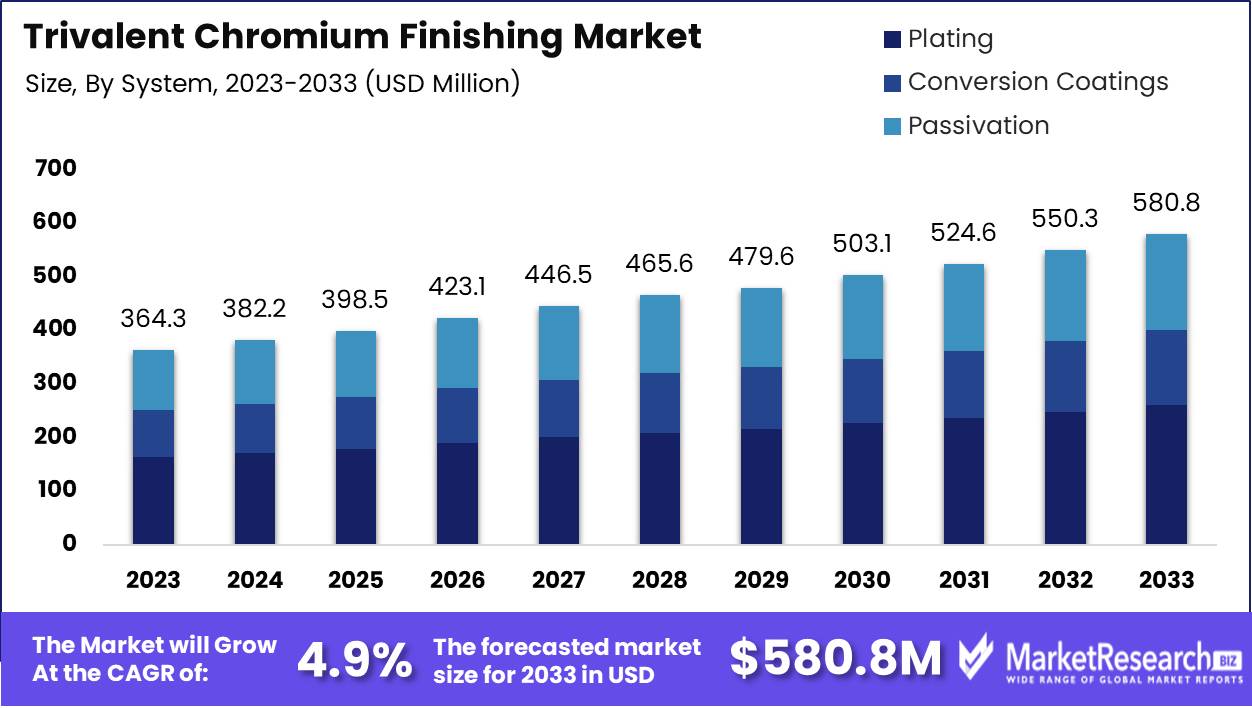

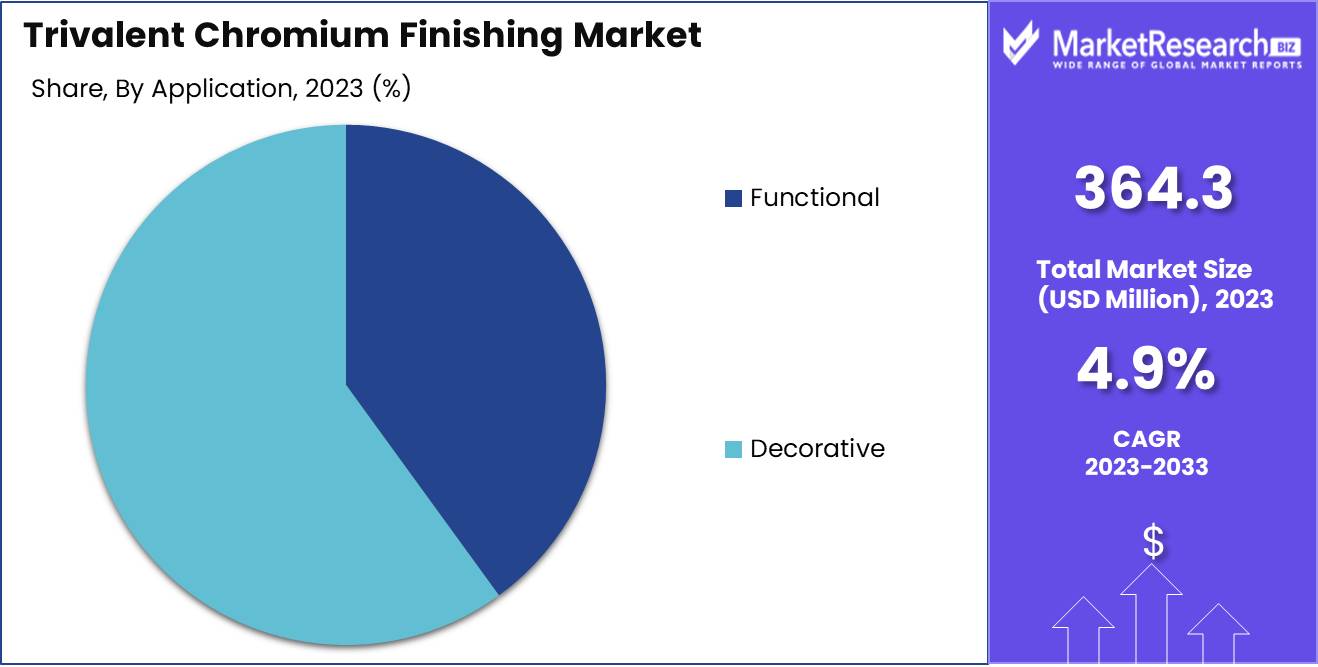

The Trivalent Chromium Finishing Market was valued at USD 364.3 million in 2023. It is expected to reach USD 580.8 million by 2033, with a CAGR of 4.9% during the forecast period from 2024 to 2033.

The Trivalent Chromium Finishing Market pertains to the industry segment focused on the application of trivalent chromium plating, a safer and environmentally friendly alternative to hexavalent chromium. This market encompasses various sectors, including automotive, aerospace, and consumer electronics, where trivalent chromium is utilized for its superior corrosion resistance, aesthetic appeal, and compliance with stringent environmental regulations. With a growing emphasis on sustainability and regulatory compliance, the market is poised for significant growth, driven by advancements in technology and increasing adoption across industries seeking to balance performance, safety, and environmental responsibility.

The Trivalent Chromium Finishing market is poised for significant growth, driven by increasing demand for environmentally friendly alternatives to traditional hexavalent chromium coatings. In 2022, the global market was valued at USD 325.20 million and experienced steady growth to USD 331.40 million by 2023. This upward trajectory is set to continue, with the market size projected to reach USD 342.83 million by year-end. Looking forward, revenue forecasts indicate robust expansion, with the market anticipated to achieve USD 477.84 million by 2032, reflecting a CAGR of 4.15% over the forecast period. Furthermore, the market's valuation in 2021 was USD 0.31 billion, with projections suggesting growth to USD 0.52 billion by 2030, at an accelerated CAGR of 5.8%.

Several factors underpin this growth trajectory. Key among them is the increasing regulatory pressure to adopt safer, less toxic coatings in various industries, including automotive, aerospace, and consumer goods. Trivalent chromium finishing offers a viable alternative, providing similar protective and aesthetic benefits without the associated health and environmental risks of hexavalent chromium.

Additionally, advancements in coating technologies and heightened awareness of sustainability issues are driving market adoption. As companies strive to meet stringent environmental standards and consumer demand for green products, the trivalent chromium finishing market is well-positioned for sustained growth. This alignment with global sustainability trends suggests a favorable outlook for stakeholders, presenting substantial opportunities for investment and innovation in the coming decade.

Key Takeaways

- Market Growth: The Trivalent Chromium Finishing Market was valued at USD 364.3 million in 2023. It is expected to reach USD 580.8 million by 2033, with a CAGR of 4.9% during the forecast period from 2024 to 2033.

- By System: Plating dominates the trivalent chromium finishing market with a 79.1% share in 2023.

- By Application: In 2023, Decorative dominated with 71.2% in the Trivalent Chromium Finishing Market.

- By End-use: In 2023, Automotive held a dominant market position with a 42.1% share.

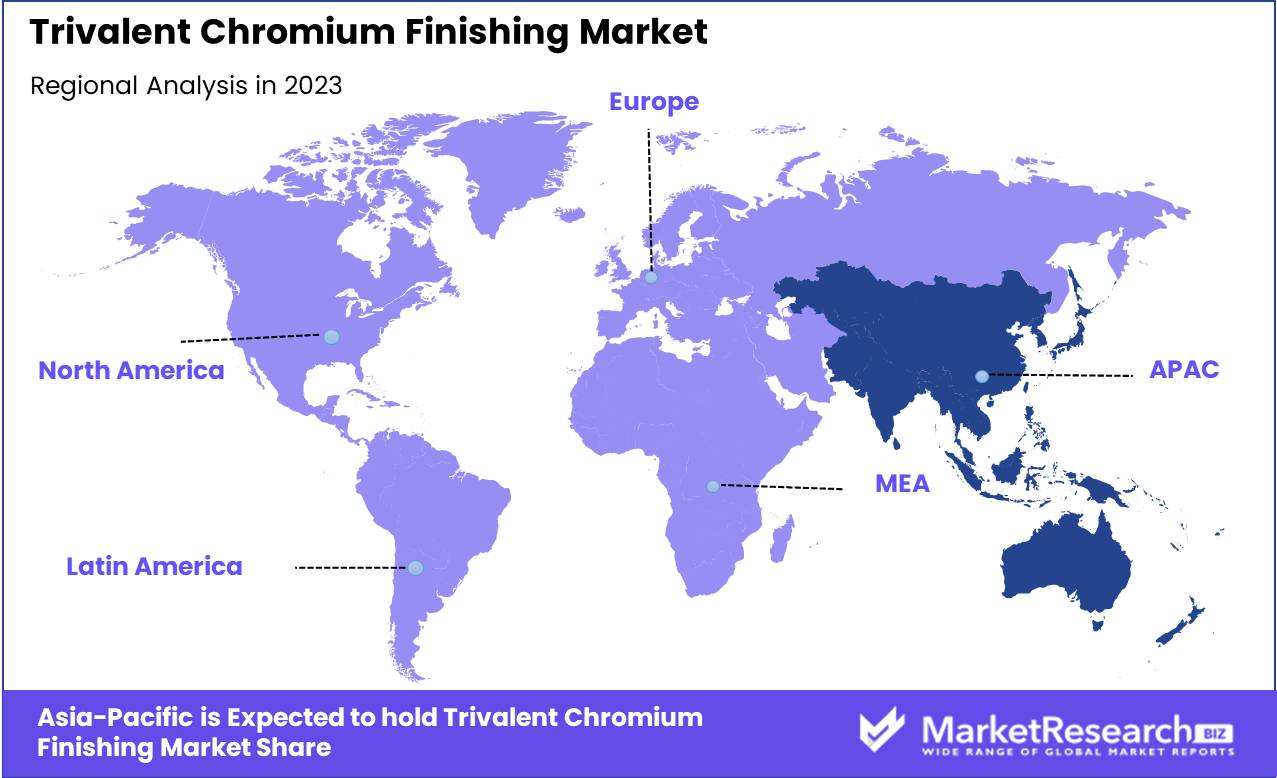

- Regional Dominance: Asia Pacific leads the Trivalent Chromium Finishing Market with a 46% share.

- Growth Opportunity: The global trivalent chromium finishing market will thrive in 2024, driven by automotive demand and safety awareness.

Driving factors

Growing Demand for Environmentally Friendly Coatings

The Trivalent Chromium Finishing Market is experiencing significant growth, primarily driven by increasing environmental concerns and stricter regulatory standards. Trivalent chromium, or Cr(III), coatings are gaining prominence as a safer alternative to hexavalent chromium (Cr(VI)) finishes, which are known for their toxicological and environmental risks. This shift is catalyzed by legislation such as the EU's REACH, and the U.S. EPA's regulations that limit the use of hazardous substances in manufacturing processes.

Trivalent chromium coatings not only meet these regulatory requirements but also offer superior corrosion resistance, durability, and aesthetic appeal, making them increasingly popular in various applications. This growing demand is reflected in the adoption of Cr(III)-based finishes across automotive, aerospace, and electronics industries, where environmental sustainability is now a critical component of product design and manufacturing strategy.

Expansion of End-Use Industries

The expansion of key end-use industries serves as a substantial growth lever for the Trivalent Chromium Finishing Market. Industries such as automotive, aerospace, and construction are integral to the increased consumption of Cr(III) coatings. The automotive sector, for example, utilizes trivalent chromium for decorative and protective purposes, enhancing vehicle longevity and appeal. As global automotive production and sales continue to rise, driven by economic growth and increasing consumer spending power, the demand for advanced finishing technologies like trivalent chromium also escalates.

Similarly, in aerospace, trivalent chromium is used to protect aircraft components from corrosion and wear, which is crucial for safety and performance. The ongoing expansion of the aerospace industry, fueled by rising air travel and military expenditure, further augments the market for chromium finishes. The construction industry also contributes to this trend, where Cr(III) coatings are employed in infrastructure projects for their corrosion resistance and durability.

Rise in Demand for Oil and Gas Industry Applications

The oil and gas industry's rebound and expansion significantly impact the demand for trivalent chromium finishes. In this sector, Cr(III) coatings are essential for ensuring the longevity and efficiency of equipment used in harsh environments, such as drilling rigs and pipelines. The protective properties of trivalent chromium safeguard against corrosion caused by exposure to extreme conditions and corrosive substances, thereby reducing maintenance costs and prolonging equipment life.

As the global demand for energy remains high, and exploration activities expand to more challenging environments, the oil and gas industry's need for durable and reliable coatings will continue to drive significant growth in the trivalent chromium market. This demand is particularly pronounced in emerging economies, where energy sector expansion is a critical component of national development strategies.

Restraining Factors

High Initial Investments Required to Set Up a Trivalent Chromium Finishing Facility

The high initial investments necessary to establish a trivalent chromium finishing facility pose a substantial barrier to the market's growth. These initial costs include expenditures on advanced equipment, compliance with stringent environmental regulations, and securing the necessary technical expertise. According to industry reports, setting up such a facility can cost several million dollars, a significant financial commitment for businesses, especially for small and medium-sized enterprises (SMEs).

This considerable capital requirement restricts the number of new entrants in the market, thereby limiting competition and innovation. As a result, existing players with the financial capability to bear these costs maintain a dominant position, potentially stifling overall market growth. Moreover, the high costs discourage potential investors who might otherwise contribute to expanding the market through new projects or technological advancements.

Frequent Maintenance Requirements

Frequent maintenance requirements of trivalent chromium finishing facilities further impede market growth by increasing operational costs and complexity. Maintenance is essential to ensure the equipment functions efficiently and to comply with environmental and safety regulations. However, this necessity translates into recurring expenses for facility operators, which can be substantial.

According to industry statistics, maintenance costs can account for up to 20% of the total operating expenses in a trivalent chromium finishing facility. These recurring costs add to the financial burden on companies, increasing the overall ownership cost. Regular maintenance activities can also lead to operational downtimes, affecting productivity and profitability.

By System Analysis

The Plating segment dominates the Trivalent Chromium Finishing Market with a 79.1% share in 2023.

In 2023, Plating held a dominant market position in the By System segment of the Trivalent Chromium Finishing Market, capturing more than a 79.1% share. This significant market presence is attributed to its widespread application across various industries, including automotive, aerospace, and electronics, where superior corrosion resistance and aesthetic appeal are critical. Conversion Coatings have seen steady adoption due to their cost-effective nature and environmental benefits, providing an eco-friendly alternative to traditional coatings. However, their market share remains comparatively lower due to limited high-performance applications.

Plating, as the leading segment, benefits from continuous advancements in trivalent chromium technology, which offers safer and more sustainable finishing solutions. The ongoing demand for high-quality, durable finishes in industrial applications further reinforces the dominance of the plating system in this market. Passivation processes, while essential for enhancing the longevity and performance of metals, occupy a smaller market share. The niche applications and specific industry requirements limit their broader adoption compared to conversion coatings and plating systems. Nevertheless, the passivation segment remains integral to industries where enhanced corrosion resistance is paramount.

By Application Analysis

In 2023, the Decorative segment dominated with 71.2% in the Trivalent Chromium Finishing Market.

In 2023, Decorative held a dominant market position in the By Application segment of the Trivalent Chromium Finishing Market, capturing more than a 71.2% share. This significant market share can be attributed to the rising consumer demand for aesthetically appealing and environmentally sustainable finishes across various industries, including automotive, electronics, and consumer goods. The decorative applications of trivalent chromium are favored for their superior appearance, resistance to tarnishing, and compliance with stringent environmental regulations, making them a preferred choice for manufacturers aiming to enhance product appeal while adhering to sustainability goals.

Functional applications of trivalent chromium, while not as dominant as decorative applications, still represent a critical segment of the market. These applications are essential in industries where corrosion resistance, durability, and hardness are paramount, such as aerospace, industrial machinery, and heavy equipment. The shift from hexavalent to trivalent chromium in these sectors is driven by regulatory pressures and the need for safer, more sustainable coating solutions. Although functional applications accounted for a smaller market share compared to decorative applications, their importance in high-performance and industrial settings underscores the versatile capabilities and growing acceptance of trivalent chromium finishes across diverse sectors.

By End-use Analysis

In 2023, the Automotive segment held a dominant market position with a 42.1% share.

In 2023, Automotive held a dominant market position in the By End-use segment of the Trivalent Chromium Finishing Market, capturing more than a 42.1% share. This leadership is driven by the automotive industry's continuous demand for advanced corrosion-resistant and environmentally friendly coatings. With increasing regulatory pressures and consumer preferences shifting towards sustainable practices, automotive manufacturers are extensively adopting trivalent chromium finishing for components such as exhaust systems, engine parts, and decorative trims.

Oil & Gas accounted for a significant portion of the market, leveraging trivalent chromium finishes to enhance the durability and lifespan of equipment exposed to harsh environments. The industry’s focus on minimizing maintenance costs and maximizing operational efficiency further propels the adoption of these finishes.

Aerospace also emerged as a key end-use sector, prioritizing lightweight and high-performance materials. Trivalent chromium coatings are preferred for their superior resistance to corrosion and wear, crucial for the reliability and safety of aerospace components. Hydraulics & Heavy Machinery benefit from the robustness of trivalent chromium finishes, which ensure extended service life and reduced downtime for machinery operating under extreme conditions. Others, including electronics and medical devices, are increasingly utilizing trivalent chromium finishes to meet stringent quality and safety standards, thereby contributing to the overall market expansion.

Key Market Segments

By System

- Conversion Coatings

- Plating

- Passivation

By Application

- Decorative

- Functional

By End-use

- Automotive

- Oil & Gas

- Aerospace

- Hydraulics & Heavy Machinery

- Others

Growth Opportunity

Increasing Demand from the Automotive Industry

The global trivalent chromium finishing market is poised for significant growth in 2024, driven primarily by the automotive industry’s burgeoning demand. As automotive manufacturers strive to meet stringent environmental regulations and enhance vehicle longevity, trivalent chromium finishes have emerged as a superior alternative to hexavalent chromium. This shift is propelled by the industry's commitment to reducing hazardous substances in their supply chains. Furthermore, the lightweight trend in automotive manufacturing necessitates coatings that offer high performance without compromising on weight, where trivalent chromium finishing provides an optimal solution.

Growing Awareness of Safety & Health

Safety and health considerations are increasingly influencing industrial processes, creating robust opportunities for trivalent chromium finishing. The rising awareness of the health risks associated with hexavalent chromium, known for its carcinogenic properties, has led to a regulatory clampdown across various regions. This regulatory environment favors the adoption of trivalent chromium, which is recognized for its lower toxicity and reduced environmental impact. As industries across the globe prioritize workplace safety and compliance with health regulations, the market for trivalent chromium finishing is set to expand.

Latest Trends

Increasing Adoption of Eco-Friendly Trivalent Chromium Coatings

As environmental regulations tighten globally, industries are increasingly shifting towards eco-friendly alternatives. Trivalent chromium coatings, known for their reduced toxicity compared to hexavalent chromium, are witnessing growing adoption. This shift is particularly pronounced in the automotive and aerospace sectors, where sustainability and regulatory compliance are critical. Companies are investing in green technologies to meet stringent environmental standards, driving demand for trivalent chromium solutions. The market is also benefitting from consumer preferences for environmentally responsible products, which further propels the transition to trivalent chromium coatings.

Technological Advancements in Trivalent Chromium Plating

Technological innovation is a key driver of growth in the trivalent chromium finishing market. Recent advancements have significantly enhanced the efficiency and quality of trivalent chromium plating processes. Developments in electroplating techniques and chemical formulations have improved coating uniformity, corrosion resistance, and adhesion properties. These improvements are making trivalent chromium coatings more competitive with traditional hexavalent chromium, particularly in high-performance applications. Additionally, innovations in automation and process control are optimizing production efficiencies and reducing operational costs, making trivalent chromium plating an increasingly viable option for a broader range of industries.

Regional Analysis

Asia Pacific leads the Trivalent Chromium Finishing Market with a 46% share.

The trivalent chromium finishing market exhibits distinct regional dynamics driven by industrial demand, regulatory frameworks, and economic conditions. In North America, the market is bolstered by robust automotive and aerospace sectors, with the U.S. and Canada investing heavily in environmentally friendly finishing technologies. Europe follows closely, propelled by stringent environmental regulations and substantial investment in sustainable manufacturing practices, particularly in Germany and the UK.

The Asia Pacific region dominates the market with a commanding 46% share, driven by rapid industrialization, expansive automotive production, and significant investments in manufacturing infrastructure in China, Japan, and South Korea. This region’s leadership is further supported by favorable government policies promoting eco-friendly technologies. In the Middle East & Africa, the market is growing steadily, fueled by burgeoning automotive and construction industries, especially in countries like the UAE and South Africa. Latin America, while smaller in market size, shows promising growth potential with increasing adoption of green technologies in Brazil and Mexico. Overall, the Asia Pacific region’s dominance is a testament to its industrial growth trajectory and proactive environmental policies, positioning it as the pivotal market for trivalent chromium finishing globally.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Trivalent Chromium Finishing Market in 2024 is characterized by significant contributions from a diverse array of key players, each bringing unique capabilities and market strategies. Companies such as Advanced Chemical Company and Astro-Chem Lab, Inc. leverage advanced chemical engineering and R&D to push the boundaries of sustainable finishing solutions. Atotech Deutschland GmbH stands out with its comprehensive electroplating and coating technologies, emphasizing efficiency and environmental compliance.

Chem Processing, Inc. and Chemeon Surface Technology, LLC focus on providing tailored surface treatment solutions, catering to specialized industry requirements. Columbia Chemical Corporation and Coventya Group are known for their robust product portfolios and global reach, ensuring consistent supply and innovation across markets.

Dipsol Chemicals Co., Ltd., and JCU Corporation offer a strong presence in the Asia-Pacific region, combining traditional expertise with modern technological advancements. Kakihara Industries Co., Ltd. and San-Ei Kagaku Co., Ltd. similarly drive innovation through localized knowledge and extensive experience in surface treatments.

In North America, MacDermid Incorporated and Ronatec C2C, Inc. lead with cutting-edge technology and customer-centric solutions. Sarrel Group and Sherwood Technology Ltd. enhance the market dynamics through strategic partnerships and continuous product development.

Market Key Players

- Advanced Chemical Company

- Astro-Chem Lab, Inc.

- Atotech Deutschland GmbH

- Chem Processing, Inc.

- Chemeon Surface Technology, LLC

- Columbia Chemical Corporation

- Coventya Group

- Dahlhausen Group

- Derivados del Fluor

- Dipsol Chemicals Co., Ltd.

- Interplex Industries Inc.

- JCU Corporation

- Kakihara Industries Co., Ltd.

- KCH Engineered Systems

- KCH Services Inc.

- MacDermid Incorporated

- Ronatec C2C, Inc.

- San-Ei Kagaku Co., Ltd.

- Sarrel Group

- Sherwood Technology Ltd.

Recent Development

- In May 2024, Covestro introduced "Discovery Resin," a high-performance, bio-based solution designed for exterior coatings. This product offers improved durability and reduced environmental impact, aligning with the increasing demand for sustainable and eco-friendly finishing solutions.

- In April 2024, ATI Inc. completed the expansion of its Vandergrift Operations. This expansion is aimed at enhancing the production capabilities of trivalent chromium finishing to meet the growing demand in various sectors, including automotive and industrial applications.

- In March 2024, MacDermid, Inc. announced the acquisition of Alent PLC, a move that integrated Alent’s operations into a new division called Performance Solutions. This strategic acquisition aims to enhance MacDermid’s innovation and service capabilities across the trivalent chromium finishing market.

Report Scope

Report Features Description Market Value (2023) USD 364.3 Million Forecast Revenue (2033) USD 580.8 Million CAGR (2024-2032) 4.9% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By System (Conversion Coatings, Plating, Passivation), By Application (Decorative, Functional), By End-use (Automotive, Oil & Gas, Aerospace, Hydraulics & Heavy Machinery, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Advanced Chemical Company, Astro-Chem Lab, Inc., Atotech Deutschland GmbH, Chem Processing, Inc., Chemeon Surface Technology, LLC, Columbia Chemical Corporation, Coventya Group, Dahlhausen Group, Derivados del Fluor, Dipsol Chemicals Co., Ltd., Interplex Industries Inc., JCU Corporation, Kakihara Industries Co., Ltd., KCH Engineered Systems, KCH Services Inc., MacDermid Incorporated, Ronatec C2C, Inc., San-Ei Kagaku Co., Ltd., Sarrel Group, Sherwood Technology Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Advanced Chemical Company

- Astro-Chem Lab, Inc.

- Atotech Deutschland GmbH

- Chem Processing, Inc.

- Chemeon Surface Technology, LLC

- Columbia Chemical Corporation

- Coventya Group

- Dahlhausen Group

- Derivados del Fluor

- Dipsol Chemicals Co., Ltd.

- Interplex Industries Inc.

- JCU Corporation

- Kakihara Industries Co., Ltd.

- KCH Engineered Systems

- KCH Services Inc.

- MacDermid Incorporated

- Ronatec C2C, Inc.

- San-Ei Kagaku Co., Ltd.

- Sarrel Group

- Sherwood Technology Ltd.

Our Clients

View Our Licence Options