Smart Grid Cyber Security Market By Security Type (Application Security, Endpoint Security, Database Security, Network Security), By Solution (Antivirus and antimalware, Firewall, Identity and Access Management (IAM), Encryption, Others), By Service (Professional Service and Managed Service), By Deployment Type (Cloud and On-Premises), By Application (Smart Meters, Smart Application, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

49308

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

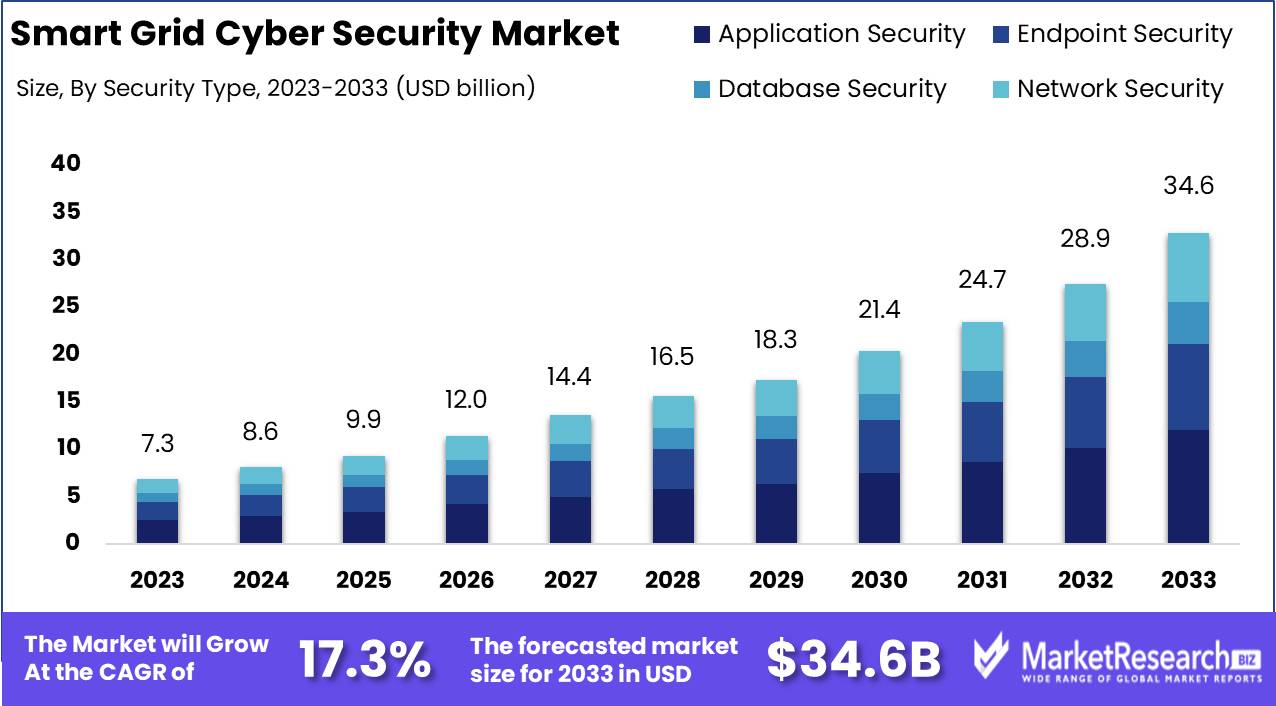

The Smart Grid Cyber Security Market was valued at USD 7.3 billion in 2023. It is expected to reach USD 34.6 billion by 2033, with a CAGR of 17.3% during the forecast period from 2024 to 2033.

The Smart Grid Cyber Security Market encompasses technologies, solutions, and services designed to safeguard the critical infrastructure of smart grids against cyber threats. As smart grids integrate advanced communication networks and digital technologies to enhance electricity distribution and management, the need for robust cyber security measures becomes paramount. This market addresses the protection of data integrity, confidentiality, and availability, ensuring reliable and secure grid operations.

The Smart Grid Cyber Security Market is witnessing a significant growth driven by the increasing frequency and sophistication of cyber threats targeting critical infrastructure. The proliferation of smart grid technology, which enables real-time monitoring and control of electricity distribution, has inadvertently expanded the attack surface for cybercriminals. This rise in cyber-attacks on smart grid infrastructure necessitates robust and resilient cyber security measures.

Additionally, the integration of advanced technologies such as artificial intelligence (AI) and machine learning is revolutionizing cyber security solutions, enabling predictive threat detection and proactive mitigation strategies. These technologies not only enhance the efficiency and effectiveness of cyber security measures but also allow for the rapid identification and neutralization of potential threats before they can inflict significant damage.

However, the deployment of these advanced cyber security solutions comes with substantial implementation costs, posing a financial challenge for many utilities and smart grid operators. The significant initial investment required for comprehensive cyber security infrastructure can be a barrier, particularly for smaller entities with limited budgets. Despite this, the increasing collaboration between cyber security providers and smart grid operators is fostering innovation and facilitating the development of cost-effective solutions. These partnerships are essential in creating a secure smart grid environment, as they combine the expertise of cyber security specialists with the operational knowledge of grid operators.

Key Takeaways

- Market Growth: The Smart Grid Cyber Security Market was valued at USD 7.3 billion in 2023. It is expected to reach USD 34.6 billion by 2033, with a CAGR of 17.3% during the forecast period from 2024 to 2033.

- By Security Type: Application Security dominated Smart Grid Cyber Security Market segments.

- By Solution: Antivirus and Antimalware dominated Smart Grid Cyber Security solutions.

- By Service: Professional Service dominated Smart Grid Cyber Security Market services.

- By Deployment Type: Cloud dominated the Smart Grid Cyber Security Market.

- By Application: Smart Meters dominated the Smart Grid Cyber Security Market.

- Regional Dominance: North America leads the Smart Grid Cyber Security Market with a 35% largest share.

- Growth Opportunity: The convergence of smart grid technology adoption and the demand for integrated IT and cyber security solutions presents a robust growth opportunity for the global smart grid cyber security market.

Driving factors

Increasing Cyber Threats: Catalyzing the Demand for Robust Smart Grid Cyber Security Solutions

The surge in cyber threats targeting critical infrastructure, particularly smart grids, has been a significant driver for the Smart Grid Cyber Security Market. As smart grids become more prevalent, they also become more attractive targets for cyber-attacks due to their vital role in energy distribution and management. According to industry reports, there has been a noticeable increase in the number of cyber-attacks on energy infrastructure, with a 35% rise in such incidents reported over the past five years. This alarming trend has prompted utility companies and grid operators to prioritize the implementation of comprehensive cybersecurity measures. The increasing frequency and sophistication of these attacks underscore the necessity for advanced security solutions, driving the market growth significantly.

Growing Demand for Energy Efficiency: Enhancing the Need for Secure Smart Grid Implementations

The growing emphasis on energy efficiency is another crucial factor propelling the Smart Grid Cyber Security Market. Smart grids are designed to optimize energy distribution and consumption, leading to substantial improvements in energy efficiency. As governments and organizations strive to meet stringent energy efficiency goals and reduce carbon footprints, the deployment of smart grids is expanding rapidly. This expansion, however, brings about a heightened need for cyber security to protect the complex network of sensors, meters, and communication systems integral to smart grid operations.

In 2023, global investments in smart grid technology reached $250 billion, a testament to the escalating demand for energy-efficient solutions. The necessity to secure these investments and ensure uninterrupted and efficient energy distribution significantly boosts the demand for robust cyber security measures in the smart grid sector.

Adoption of Renewable Energy Sources: Necessitating Advanced Cyber Security Measures for Smart Grids

The integration of renewable energy sources into the energy grid has been a pivotal driver for the Smart Grid Cyber Security Market. As countries worldwide strive to reduce reliance on fossil fuels and transition to sustainable energy solutions, the adoption of renewable energy sources such as wind, solar, and hydropower is accelerating. This shift towards a more decentralized and variable power generation landscape necessitates the implementation of smart grids to manage the intermittent nature of renewable energy effectively.

Consequently, the increased complexity and interconnectedness of smart grids elevate the risk of cyber threats. According to recent data, the global renewable energy capacity increased by 10% in 2023, emphasizing the growing scale of renewable integration. To safeguard the integrity and reliability of these smart grids against cyber-attacks, substantial investments in cyber security solutions are imperative, driving the market growth further.

Restraining Factors

Complexity of Integration: A Barrier to Rapid Adoption

The complexity of integrating smart grid cyber security solutions poses a significant challenge to the market's growth. This complexity arises from the need to harmonize new security technologies with existing grid infrastructure, which is often outdated and not initially designed with modern cybersecurity requirements in mind. The integration process involves a thorough understanding of both the operational technology (OT) used in grid systems and the information technology (IT) necessary for robust cybersecurity measures. This dual requirement necessitates specialized expertise, which can be scarce, leading to higher costs and longer implementation times. Consequently, utility companies might be hesitant to invest in comprehensive cyber security solutions due to the perceived complexity and resource demands, thereby restraining market growth.

Evolving Cyber Threats: Driving Continuous Innovation and Market Demand

While evolving cyber threats are a restraining factor due to the persistent need for adaptation and upgrading of security measures, they also act as a significant driver for the smart grid cyber security market. The increasing sophistication and frequency of cyber attacks on critical infrastructure, including smart grids, underscore the urgency for advanced and adaptive security solutions. According to industry reports, the frequency of cyber attacks on energy utilities has been rising steadily, necessitating continuous innovation in cyber security technologies.

The dynamic nature of cyber threats requires that smart grid cyber security systems remain agile and responsive, incorporating the latest in threat detection, mitigation, and response strategies. This constant evolution places a considerable burden on security providers and utility companies to stay ahead of potential vulnerabilities, increasing operational costs and necessitating ongoing investment in research and development. While this relentless pressure can strain resources, it simultaneously stimulates market growth by creating a consistent demand for state-of-the-art security solutions.

By Security Type Analysis

In 2023, Application Security dominated Smart Grid Cyber Security Market segments.

In 2023, Application Security held a dominant market position in the By Security Type segment of the Smart Grid Cyber Security Market. This segment's prominence can be attributed to the increasing reliance on software applications for grid management, which necessitates robust security measures to protect against potential vulnerabilities and cyber threats. Application Security encompasses measures such as code analysis, application testing, and firewall implementation, which are critical in safeguarding the integrity of smart grid applications.

Following closely is Endpoint Security, which plays a crucial role in protecting individual devices connected to the smart grid, such as smart meters and control systems. The rise in remote work and the proliferation of IoT devices have further emphasized the importance of securing endpoints against unauthorized access and malware.

Database Security is another significant segment, focused on protecting the vast amounts of data generated and stored within smart grids. This includes encryption, access controls, and regular monitoring to prevent data breaches and ensure data integrity.

Lastly, Network Security remains vital for protecting the communication pathways within the smart grid infrastructure. This involves securing network protocols, implementing intrusion detection systems, and ensuring secure data transmission to prevent cyber attacks and ensure the uninterrupted operation of the grid.

By Solution Analysis

In 2023, Antivirus and Antimalware dominated Smart Grid Cyber Security solutions.

In 2023, Antivirus and Antimalware held a dominant market position in the By Solution segment of the Smart Grid Cyber Security Market. This segment encompasses various essential cybersecurity solutions aimed at protecting smart grid infrastructures from potential cyber threats. Antivirus and Antimalware solutions are pivotal in detecting, preventing, and mitigating malware attacks, ensuring the integrity and security of smart grid systems. Their prominence is driven by the increasing sophistication of cyber-attacks and the critical need for robust protection mechanisms.

Firewall solutions also play a crucial role, providing a first line of defense by monitoring and controlling incoming and outgoing network traffic based on predetermined security rules. Identity and Access Management (IAM) systems are integral for ensuring that only authorized personnel have access to sensitive grid information, thereby preventing unauthorized access and potential breaches.

Encryption technologies are vital for securing data in transit and at rest, ensuring that even if data is intercepted, it remains unreadable to unauthorized entities. Security and Vulnerability Management solutions are essential for identifying, assessing, and addressing potential vulnerabilities within the grid infrastructure.

Intrusion Detection System/Intrusion Prevention System (IDS/IPS) solutions are crucial for monitoring network traffic for suspicious activities and taking immediate action to prevent potential threats. Distributed Denial of Service (DDoS) protection solutions safeguard smart grid systems from overwhelming attacks aimed at disrupting services. Lastly, other solutions, including advanced threat intelligence and response systems, contribute to a comprehensive security strategy, ensuring the resilience and reliability of smart grid infrastructures against an evolving cyber threat landscape.

By Service Analysis

In 2023, Professional Service dominated Smart Grid Cyber Security Market services.

In 2023, Professional Service held a dominant market position in the Professional Service segment of the Smart Grid Cyber Security Market. This leadership can be attributed to the increasing reliance on advanced security solutions to protect critical infrastructure from cyber threats. Professional services encompass a range of offerings, including consulting, integration, and support services, which are crucial for implementing and maintaining robust cybersecurity frameworks. The sector benefits from heightened awareness of cyber risks and regulatory mandates, driving demand for expert services to ensure compliance and safeguard operations. The rise of sophisticated cyber-attacks targeting smart grids has underscored the need for professional intervention, leading utilities and energy companies to seek specialized expertise.

Managed services also showed significant growth, driven by the need for continuous monitoring and management of security systems. However, the professional service segment's comprehensive approach, offering tailored solutions and strategic guidance, remains the preferred choice for organizations seeking to enhance their cyber resilience. This trend is expected to continue as the complexity of cyber threats evolves, necessitating advanced professional services to protect the smart grid infrastructure effectively.

By Deployment Type Analysis

In 2023, The Cloud dominated the Smart Grid Cyber Security Market.

In 2023, Cloud held a dominant market position in the By Deployment Type segment of the Smart Grid Cyber Security Market. This segment witnessed significant growth due to the increasing adoption of cloud-based solutions across various industries. Cloud-based deployment offers enhanced scalability, flexibility, and cost-efficiency, making it the preferred choice for many organizations. The rapid digital transformation and the rising need for real-time data access and analysis have further propelled the demand for cloud-based smart grid cyber security solutions. Additionally, the integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) in cloud platforms has strengthened security measures, thereby attracting more users.

On-premises deployment, although still relevant, saw comparatively slower growth. This segment is often favored by organizations with stringent regulatory requirements and those with concerns over data privacy and control. However, the high initial costs and the need for continuous maintenance and upgrades have limited its adoption. Despite these challenges, the on-premises segment remains crucial for specific use cases where direct control over the infrastructure is paramount.

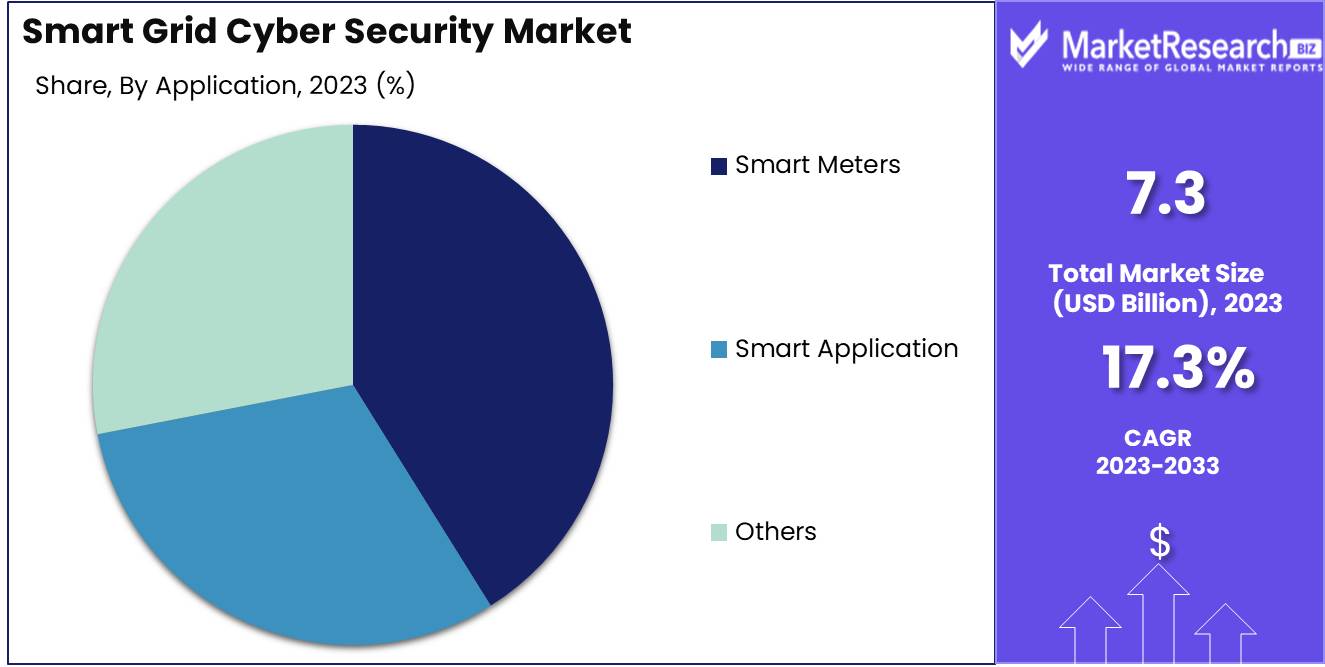

By Application Analysis

Smart Meters dominated the Smart Grid Cyber Security Market.

In 2023, Smart Meters held a dominant market position in the By Application segment of the Smart Grid Cyber Security Market. This can be attributed to the increasing adoption of smart meters globally, which has necessitated robust cybersecurity measures to protect sensitive data and ensure the integrity of grid operations. The integration of smart meters into energy distribution systems has exposed them to potential cyber threats, driving the demand for advanced cybersecurity solutions.

Smart Applications emerged as a significant segment due to the widespread implementation of smart grid applications such as demand response, distributed energy resources, and advanced distribution management systems. These applications enhance grid efficiency and reliability but also require comprehensive security measures to safeguard against cyber threats.

Other categories include various components like smart transformers, intelligent appliances, and electric vehicle infrastructure, which also contribute to the overall demand for cybersecurity solutions in the smart grid ecosystem. The growing complexity and interconnectedness of smart grid components necessitate a holistic approach to cybersecurity, ensuring all elements are protected from potential cyber-attacks.

Key Market Segments

By Security Type

- Application Security

- Endpoint Security

- Database Security

- Network Security

By Solution

- Antivirus and antimalware

- Firewall

- Identity and Access Management (IAM)

- Encryption

- Security and vulnerability management

- Intrusion Detection System/Intrusion Prevention System (IDS/IPS)

- Distributed Denial of Service (DDoS)

- Others

By Service

- Professional Service

- Managed Service

By Deployment Type

- Cloud

- On-Premises

By Application

- Smart Meters

- Smart Application

- Others

Growth Opportunity

Increasing Adoption of Smart Grid Technology

The global smart grid cyber security market is poised for substantial growth, driven by the increasing adoption of smart grid technology. As utilities and energy providers continue to modernize their infrastructure, the integration of advanced smart grid technologies becomes imperative. These technologies enhance the efficiency, reliability, and sustainability of energy distribution systems but also introduce new vulnerabilities. The need to protect these complex systems from cyber threats creates significant opportunities for growth in the smart grid cyber security market. Utilities are expected to invest heavily in robust security solutions to safeguard their networks, data, and critical infrastructure.

Integrated Offerings of Smart Grid IT and Cyber Security

Another critical factor contributing to the market’s growth is the trend toward integrated offerings of smart grid IT and cyber security. As the smart grid landscape evolves, there is an increasing demand for comprehensive solutions that provide seamless integration of IT systems and cyber security measures. This integration ensures that cyber security is not an afterthought but a foundational aspect of smart grid deployment. Vendors that can offer end-to-end solutions, encompassing both IT and security, are likely to see increased demand. These integrated solutions provide better protection against sophisticated cyber attacks, thereby enhancing the overall security posture of smart grids.

Latest Trends

Integration of AI and Machine Learning: Enhancing Predictive Capabilities

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into smart grid cyber security is anticipated to be a pivotal trend. AI and ML technologies offer advanced predictive capabilities, enabling the identification of potential threats and anomalies in real time. By leveraging large datasets, these technologies can enhance the accuracy and speed of threat detection, significantly reducing response times. The ability to predict and preempt cyber threats will be crucial in safeguarding the smart grid infrastructure against increasingly sophisticated cyber-attacks. This trend is expected to drive substantial investments in AI and ML-based security solutions, fostering innovation and collaboration among technology providers and grid operators.

Focus on Network Security: Fortifying Communication Channels and Data Integrity

As the smart grid becomes more interconnected, the focus on network security will intensify. Ensuring the security of communication channels and the integrity of data transmitted across the grid will be paramount. Network security solutions will need to address vulnerabilities that arise from the increased connectivity of grid components, including smart meters, sensors, and control systems. Enhanced encryption techniques, robust authentication protocols, and continuous monitoring will be essential in protecting the grid from cyber intrusions. This focus on network security will drive the adoption of comprehensive security frameworks that encompass both legacy and modern grid infrastructures, ensuring a holistic approach to cyber defense.

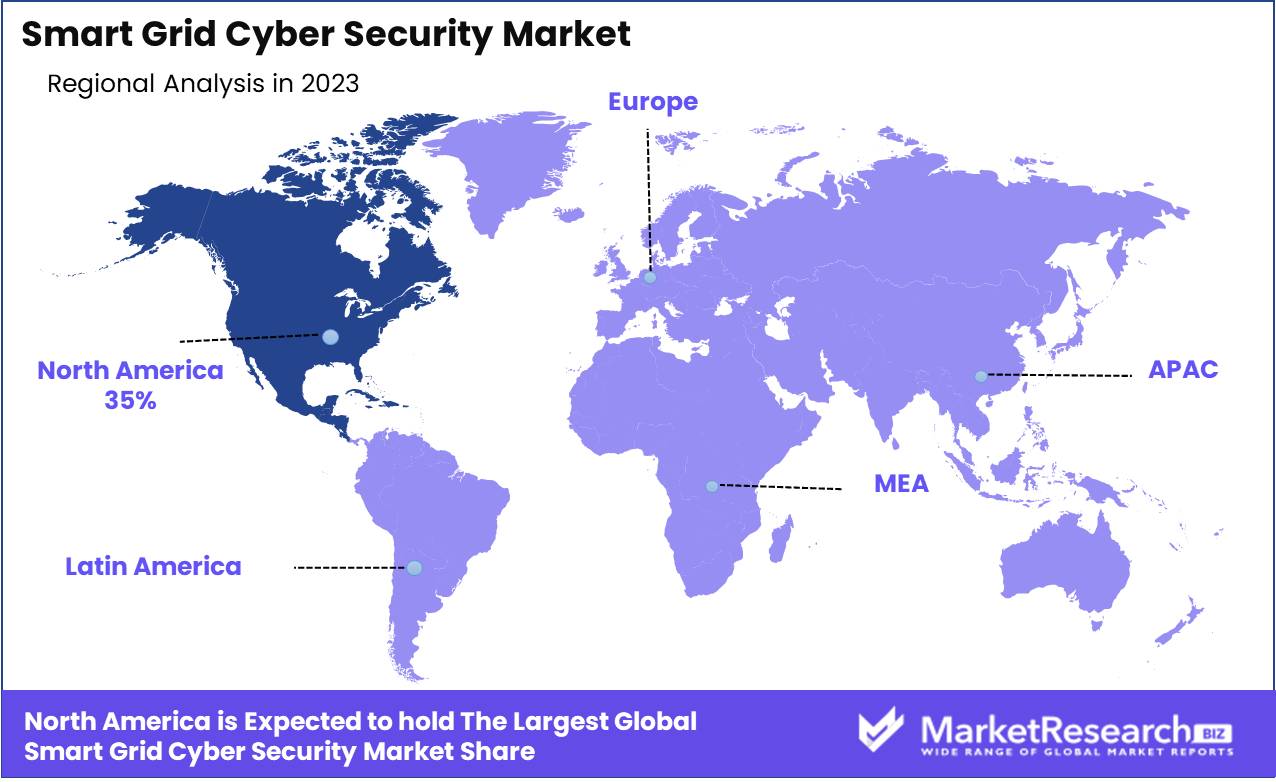

Regional Analysis

North America leads the Smart Grid Cyber Security Market with a 35% largest share.

The Smart Grid Cyber Security Market exhibits varied dynamics across different regions. In North America, the market is the most advanced, driven by significant investments in smart grid infrastructure and stringent regulatory frameworks aimed at securing energy networks. The region holds the dominant share, accounting for approximately 35% of the global market in 2023. The presence of key players and robust government initiatives further bolster this market.

Europe follows closely, driven by the European Union's focus on energy security and integration of renewable energy sources. The European market benefits from substantial funding for cyber security solutions in smart grids, contributing to a significant market share. Asia Pacific is experiencing rapid growth, fueled by increasing urbanization, rising electricity demand, and substantial investments in smart grid technologies by countries such as China and India. The market in this region is projected to witness the highest growth rate.

In the Middle East & Africa, the adoption of smart grid cyber security solutions is gaining momentum, albeit at a slower pace, due to the increasing need for energy security and the gradual deployment of smart grid systems. Latin America shows promising growth prospects, particularly in countries like Brazil and Mexico, where government initiatives and international collaborations are driving market expansion.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Smart Grid Cyber Security Market is anticipated to witness substantial growth driven by key players such as BAE Systems Plc, IBM Corporation, IOActive, Lockheed Martin Corporation, and others. Each of these companies brings a unique set of capabilities and strategic initiatives that collectively enhance the market's robustness.

BAE Systems Plc is likely to leverage its advanced defense-grade cybersecurity solutions to safeguard smart grids from evolving threats. IBM Corporation's extensive expertise in AI and cloud computing positions it as a leader in providing innovative and scalable cybersecurity solutions tailored for smart grids. IOActive's focus on high-risk cyber environments will continue to drive advancements in penetration testing and security assessments.

Lockheed Martin Corporation's deep-rooted experience in critical infrastructure protection ensures its significant contribution to securing smart grid systems. AlertEnterprise is expected to offer comprehensive security convergence solutions, integrating cyber and physical security measures.

AlienVault Inc., a subsidiary of AT&T, is anticipated to enhance threat detection and response capabilities through its unified security management solutions. Black and Veatch's engineering expertise will likely support the integration of robust cyber security measures into smart grid infrastructure projects. Cisco Systems Inc. remains pivotal with its advanced network security solutions that ensure the seamless and secure operation of smart grids.

McAfee-Intel is expected to fortify endpoint security, while Honeywell will focus on industrial cybersecurity solutions. Entergy's experience as a utility company provides practical insights into grid security challenges. HP's broad IT security portfolio will support various aspects of smart grid protection. Lastly, N-Dimension Solutions will continue to specialize in cyber protection for utility networks, enhancing overall market security standards.

Market Key Players

- BAE Systems Plc

- IBM Corporation

- IOActive

- Lockheed Martin Corporation

- AlertEnterprise

- AlienVault Inc.

- Black and Veatch

- Cisco Systems Inc.

- McAfee-Intel

- Honeywell

- Entergy

- HP

- N-Dimension Solutions

Recent Development

- In April 2024, IBM and Cisco announced a collaboration to develop integrated cybersecurity solutions for smart grids. The partnership aims to leverage IBM's expertise in security intelligence and Cisco's networking capabilities to provide comprehensive protection against cyber threats to smart grid networks.

- In March 2024, Eaton introduced advanced cybersecurity solutions tailored for smart grid applications. These solutions focus on protecting smart grid systems from sophisticated cyber threats by incorporating enhanced encryption, network security, and continuous monitoring features.

- In February 2024, ENISA released a new report emphasizing a risk-based approach for implementing smart grid cyber security measures. The report outlines 40 security measures categorized into three levels of sophistication across ten domains, aimed at enhancing the resilience and security of smart grid infrastructures in Europe.

Report Scope

Report Features Description Market Value (2023) USD 7.3 Billion Forecast Revenue (2033) USD 34.6 Billion CAGR (2024-2032) 17.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Security Type (Application Security, Endpoint Security, Database Security, Network Security), By Solution (Antivirus and antimalware, Firewall, Identity and Access Management (IAM), Encryption, Others), By Service (Professional Service and Managed Service), By Deployment Type (Cloud and On-Premises), By Application (Smart Meters, Smart Application, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape BAE Systems Plc, IBM Corporation, IOActive, Lockheed Martin Corporation, AlertEnterprise, AlienVault Inc., Black and Veatch, Cisco Systems Inc., McAfee-Intel, Honeywell, Entergy, HP, N-Dimension Solutions Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- BAE Systems Plc

- IBM Corporation

- IOActive

- Lockheed Martin Corporation

- AlertEnterprise

- AlienVault Inc.

- Black and Veatch

- Cisco Systems Inc.

- McAfee-Intel

- Honeywell

- Entergy

- HP

- N-Dimension Solutions

Our Clients

View Our Licence Options