Quantum Dot Market By Processing Technique (Colloidal Synthesis, Fabrication, Bio-Molecular Self-Assembly, and others), By Product Type (QD medical devices, QD displays, and others), By Material (Cadmium-Based Quantum Dots, Cadmium, and others), By Vertical (Consumer, Commercial, and others), By Application (Medical Devices, Displays, Solar Cells, and others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46596

-

May 2024

-

136

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

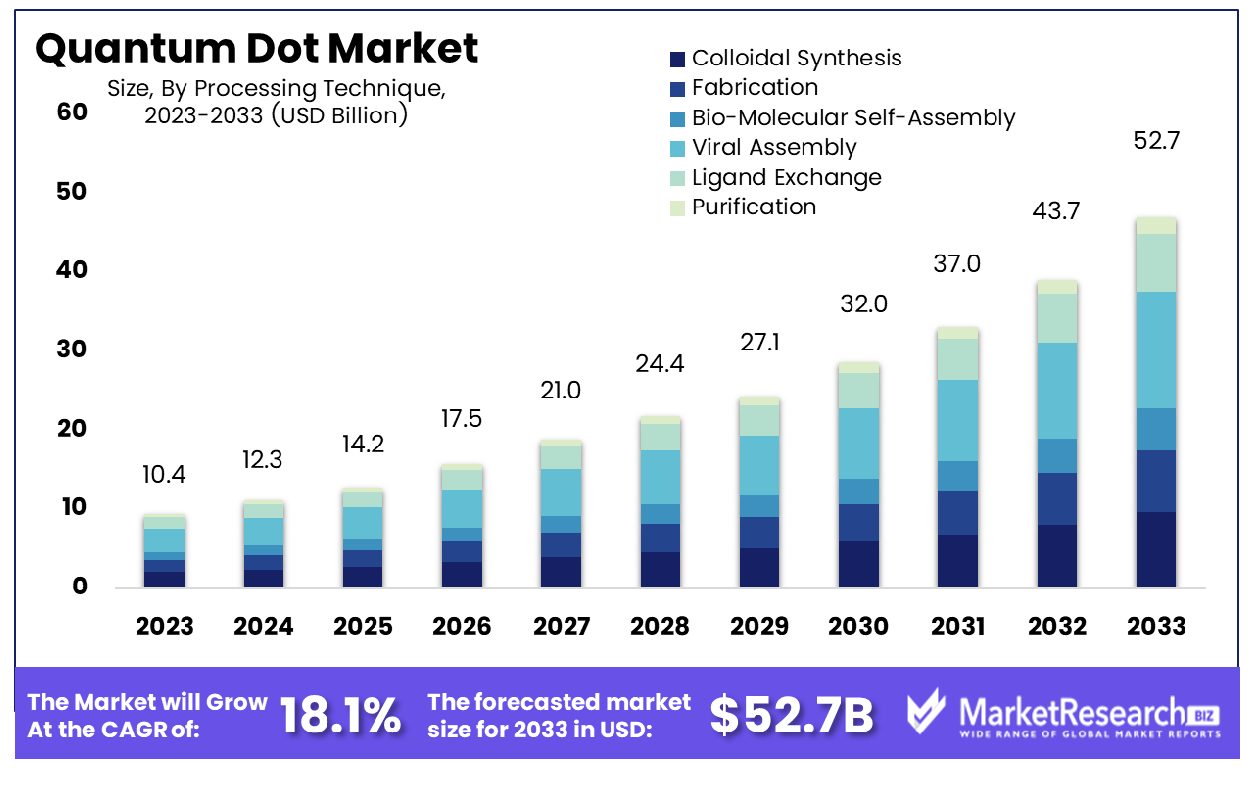

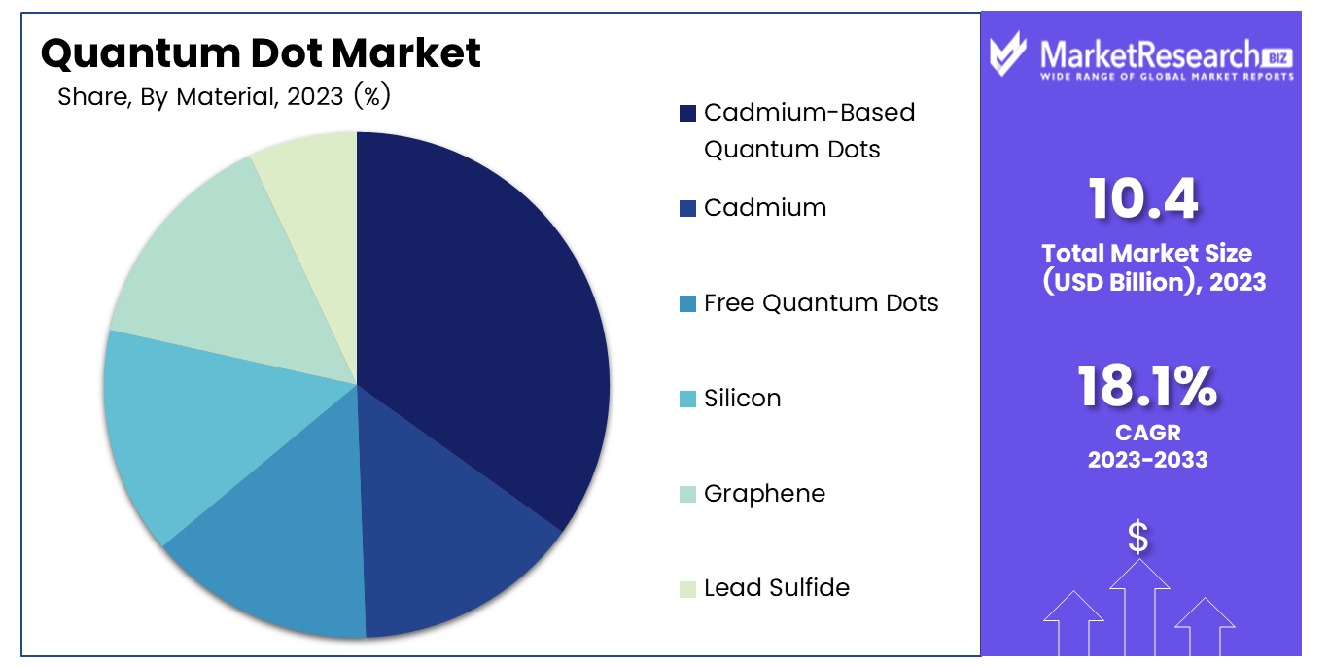

The Global Quantum Dot Market was valued at USD 10.4 Bn in 2023. It is expected to reach USD 52.7 Bn by 2033, with a CAGR of 18.1% during the forecast period from 2024 to 2033.

The Quantum Dot Market encompasses the development, production, and application of nanoscale semiconductor particles that exhibit unique quantum mechanical properties. Quantum dots (QDs) are renowned for their size-dependent optical and electronic characteristics, making them pivotal in enhancing display technologies, medical imaging, solar cells, and quantum computing. This market is driven by the increasing demand for high-resolution displays in consumer electronics, advancements in biotechnology for diagnostic tools, and the growing need for efficient renewable energy solutions. Continuous innovation and integration of QDs across various sectors highlight their transformative potential and underscore their strategic importance in future technological advancements.

The Quantum Dot Market is poised for significant growth, driven by rapid technological advancements and increasing applications across various sectors. Quantum dots (QDs) have transitioned from a nascent technology, with the first patent filed in 1988, to a critical component in modern innovations. For the initial two decades, the growth trajectory of QD research and development was gradual. However, 2001 marked a turning point with a 49.16% surge in the number of patents, reflecting heightened interest and breakthroughs in this field. The United States has emerged as the dominant leader, holding 41.6% of all QD patents from 1988 to 2016, underscoring its pivotal role in steering global advancements.

Analysts observe that the market's expansion is primarily driven by the burgeoning demand for high-resolution displays in consumer electronics, such as televisions, smartphones, and monitors, where QDs are integral for enhancing color accuracy and brightness. Additionally, the medical imaging sector benefits from the superior fluorescence properties of QDs, enabling more precise diagnostic tools. The renewable energy sector also stands to gain significantly, as QDs enhance the efficiency of solar cells, making them more viable for widespread adoption.

Continuous innovation, supported by substantial R&D investments and strategic collaborations, is expected to propel the market further. Companies are focusing on overcoming existing challenges, such as production scalability and environmental concerns related to heavy metal content in QDs. The convergence of technological advancements and market demand sets a robust foundation for sustained growth, positioning the Quantum Dot Market as a key area of interest for stakeholders looking to leverage cutting-edge technology for competitive advantage.

Key Takeaways

- Market Growth: The Global Quantum Dot Market was valued at USD 10.4 Bn in 2023. It is expected to reach USD 52.7 Bn by 2033, with a CAGR of 18.1% during the forecast period from 2024 to 2033.

- By Processing Technique: Colloidal Synthesis dominating 35% with its versatility and scalability in quantum dot production processes.

- By Product Type: QD displays is capturing 25%, driving advancements in vibrant and energy-efficient display technologies.

- By Material: Cadmium-Based Quantum Dots is dominating with 40%, despite environmental concerns, due to their superior optical properties.

- By Vertical: Consumer segment is dominating with 30%, driving demand for quantum dot-enabled electronics and displays.

- By Application: Displays securing 25%, driving advancements in vibrant and energy-efficient display technologies.

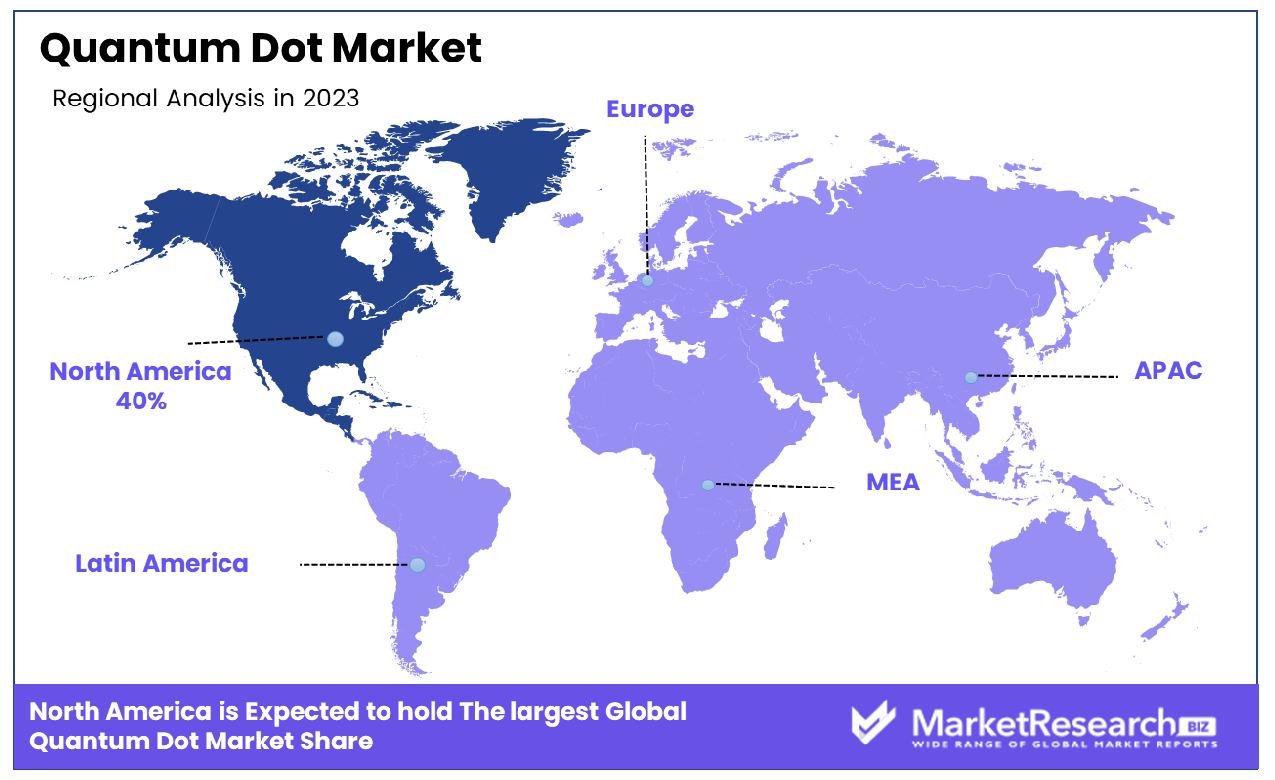

- Regional Dominance: North America leads the Quantum Dot market with a substantial 40% dominance, driven by strong investments in research and development, as well as a mature electronics industry.

- Growth Opportunity: A significant growth opportunity lies in the Quantum Dot market's expansion into emerging applications such as quantum computing, biotechnology, and environmental sensing, driven by ongoing technological advancements and increasing demand for novel solutions across industries.

Driving factors

Pioneering Renewable Energy Solutions

The integration of quantum dots in solar cells represents a pivotal driving factor for the quantum dot market. Quantum dots enhance the efficiency of solar cells by improving light absorption and converting more sunlight into electricity. This technological advancement aligns with the global push towards renewable energy solutions, presenting a substantial growth opportunity. The potential for quantum dot-enhanced solar cells to outperform traditional photovoltaic cells in efficiency and cost-effectiveness is a significant catalyst propelling market expansion.

Adoption in Displays

The adoption of quantum dots in displays, particularly in televisions and monitors, is revolutionizing the visual experience by providing vibrant colors and enhanced brightness. Quantum dots enable displays to produce a wider color gamut and higher energy efficiency, addressing the growing consumer demand for high-quality visual content. This trend is driving substantial investments from leading display manufacturers, thereby accelerating the adoption of quantum dot technology in the consumer electronics sector.

Enhancing Performance and Efficiency

The rising demand for optimized electronic devices with superior performance and energy efficiency is a crucial factor driving the quantum dot market. Quantum dots offer significant advantages in terms of electronic properties, enabling the development of advanced devices with improved functionalities. As consumers and industries alike seek more efficient and high-performing electronic solutions, the incorporation of quantum dots in various applications continues to gain momentum.

Diverse Applications

The versatility of quantum dots, with applications spanning from medical imaging to lighting, underscores their potential to transform various industries. This diverse applicability not only broadens the market horizon but also attracts substantial R&D investments aimed at discovering new and innovative uses for quantum dots. As industries continue to explore and harness the unique properties of quantum dots, the market is poised for expansive growth across multiple sectors.

Restraining Factors

Difficulty in Blue Quantum Dot Manufacturing

One of the significant challenges in the quantum dot market is the difficulty in manufacturing blue quantum dots, which are essential for achieving high-quality color displays. The complexity and precision required in producing stable and efficient blue quantum dots pose technical hurdles that can hinder market growth. Addressing these manufacturing challenges is crucial for the widespread adoption of quantum dot technology in displays and other applications.

A Barrier to Mass Adoption

The high cost associated with quantum dot production and integration is a notable restraining factor. The expensive raw materials and complex manufacturing processes contribute to the overall cost, making quantum dot-enhanced products less accessible to the mass market. Reducing production costs through technological advancements and economies of scale is essential to overcome this barrier and drive broader market penetration.

Regulatory and Safety Issues

Health concerns related to the use of cadmium in quantum dots pose significant regulatory and safety challenges. Cadmium is a toxic heavy metal, and its presence in consumer products raises environmental and health concerns. This has led to stringent regulations and the need for safer, cadmium-free alternatives. Developing and adopting cadmium-free quantum dots is imperative to mitigate health risks and comply with regulatory standards.

By Processing Technique Analysis

Colloidal Synthesis led By Processing Technique, capturing over 35%

In 2023, Colloidal Synthesis held a dominant market position in the Quantum Dot Market, specifically within the By Processing Technique segment. Capturing more than a 35% share, Colloidal Synthesis emerged as the leading method for quantum dot synthesis, offering significant advantages in terms of scalability, reproducibility, and cost-effectiveness.

Fabrication techniques followed closely behind, showcasing substantial growth potential within the market. With advancements in fabrication methods, such as lithography and etching, this segment displayed promising prospects for applications demanding precise control over quantum dot properties.

Bio-Molecular Self-Assembly emerged as another notable segment, leveraging biological processes to construct quantum dots with enhanced biocompatibility and functionalization capabilities. This technique found extensive utilization in biomedical imaging, drug delivery, and biosensing applications, thereby contributing to its notable market share.

Viral Assembly, though occupying a smaller share compared to other segments, exhibited a niche application in quantum dot synthesis. Leveraging biological templates provided by viruses, this technique offered unique opportunities for tailoring quantum dot properties with unprecedented precision, particularly in the realm of nanotechnology and optoelectronics.

Ligand Exchange and Purification techniques, while holding relatively smaller market shares, played crucial roles in enhancing the stability, optical properties, and overall quality of synthesized quantum dots. As demand for quantum dots with superior performance characteristics continued to rise across various industries, these segments witnessed steady growth and innovation to meet evolving market requirements.

By Product Type Analysis

QD displays dominated By Product Type, with more than 25%

In 2023, QD displays emerged as the frontrunner in the Quantum Dot Market's By Product Type segment, seizing a commanding share of more than 25%. This dominance underscored the widespread adoption of quantum dot technology in display applications, driven by its ability to deliver vibrant colors, high brightness, and energy efficiency.

Following closely behind, QD medical devices represented another significant segment within the market landscape. With advancements in nanotechnology, quantum dots found extensive utilization in medical imaging, biosensing, and targeted drug delivery systems, offering unprecedented precision and sensitivity in diagnostics and treatment modalities.

QD solar cells emerged as a pivotal segment, capitalizing on quantum dots' tunable optoelectronic properties to enhance the efficiency and performance of photovoltaic devices. Leveraging quantum dot-enabled solar cells promised to revolutionize renewable energy generation by boosting conversion efficiencies and reducing manufacturing costs.

QD photodetectors and sensors constituted a vital segment, catering to a diverse range of applications spanning from automotive and consumer electronics to industrial monitoring and environmental sensing. Quantum dot-based photodetectors and sensors offered superior sensitivity, wavelength selectivity, and response times, thereby driving their adoption across various sectors.

QD lasers showcased substantial growth potential within the market, fueled by their ability to deliver coherent light sources with exceptional brightness and spectral purity. Quantum dot lasers found applications in telecommunications, healthcare, and materials processing, promising advancements in data transmission speeds, multiplexed diagnostics, and precision manufacturing.

QD lighting solutions, particularly in LED technology, represented a burgeoning segment characterized by energy-efficient lighting alternatives with superior color rendering capabilities. Quantum dot-enabled LEDs offered broader color gamuts, longer lifespans, and reduced energy consumption compared to conventional lighting sources, driving their adoption in residential, commercial, and industrial settings.

Batteries and Energy-Storage Systems emerged as an innovative segment, leveraging quantum dot materials to enhance energy density, charge/discharge rates, and cycle stability in rechargeable batteries. Quantum dot-based energy storage solutions held promise for powering portable electronics, electric vehicles, and grid-scale energy storage applications.

QD transistors constituted a niche yet promising segment, exploring quantum dots' unique electronic properties for next-generation computing and electronics. Quantum dot transistors offered potential breakthroughs in low-power consumption, high-speed operation, and flexible device architectures, paving the way for novel computing paradigms and electronic devices.

QD tags represented an evolving segment, leveraging quantum dots' optical and chemical properties for advanced tagging, tracking, and authentication applications. Quantum dot tags offered superior performance in terms of brightness, photostability, and multiplexing capabilities, addressing the growing demand for secure and efficient product labeling and anti-counterfeiting solutions.

By Material Analysis

Cadmium-Based Quantum Dots held By Material, with over 40%.

In 2023, Cadmium-Based Quantum Dots asserted their dominance within the Quantum Dot Market's By Material segment, securing a substantial share of over 40%. This market leadership underscored the widespread utilization of cadmium-based quantum dots across various industries due to their exceptional optical properties and versatile applications.

Cadmium-Free Quantum Dots emerged as a notable contender within the market landscape, representing an environmentally friendly alternative to cadmium-based counterparts. With increasing regulatory restrictions on cadmium usage and growing environmental concerns, cadmium-free quantum dots gained traction, particularly in applications requiring non-toxic materials such as biomedical imaging and eco-friendly displays.

Silicon-based quantum dots constituted another significant segment, leveraging the abundance and compatibility of silicon in semiconductor manufacturing. Silicon quantum dots offered advantages in terms of scalability, compatibility with existing fabrication processes, and integration into electronic and optoelectronic devices, driving their adoption in photovoltaics, light-emitting diodes (LEDs), and biomedical applications.

Graphene-based quantum dots showcased promising prospects within the market, capitalizing on graphene's exceptional electronic, optical, and mechanical properties. Graphene quantum dots offered unique advantages such as high conductivity, tunable bandgaps, and biocompatibility, making them suitable for applications ranging from energy storage and sensing to biomedical imaging and quantum computing.

Lead Sulfide quantum dots represented a specialized segment within the market, known for their superior optical properties in the near-infrared (NIR) spectrum. Lead sulfide quantum dots found extensive utilization in applications such as infrared imaging, photodetectors, and telecommunications, where sensitivity and performance in the NIR range were critical requirements.

By Vertical Analysis

Cadmium-Based Quantum Dots held By Material, with over 30%.

In 2023, the Consumer vertical emerged as the frontrunner within the Quantum Dot Market's By Vertical segment, securing a commanding share of over 30%. This dominance highlighted the extensive integration of quantum dot technology into consumer electronics and related products, driven by increasing demand for high-resolution displays, energy-efficient lighting, and advanced imaging solutions among consumers.

The Commercial sector followed closely behind, representing a diverse range of applications across industries such as advertising, retail, hospitality, and corporate environments. Quantum dot technology found utilization in commercial displays, signage, and lighting solutions, offering superior performance, longevity, and energy efficiency compared to conventional alternatives.

Telecommunications emerged as another significant segment within the market landscape, leveraging quantum dot-enabled components and devices to enhance network infrastructure, data transmission, and telecommunications equipment. Quantum dot technology facilitated advancements in optical communications, signal processing, and high-speed data transfer, thereby driving its adoption in the telecommunications sector.

In the Healthcare vertical, quantum dots played a pivotal role in medical imaging, diagnostics, drug delivery, and therapeutics. Quantum dot-based imaging agents offered superior resolution, sensitivity, and multiplexing capabilities for applications such as cancer detection, molecular imaging, and targeted therapy, thereby contributing to improved patient outcomes and healthcare efficacy.

The Defense sector represented a niche yet crucial segment within the Quantum Dot Market, leveraging quantum dot technology for advanced sensing, imaging, and communication systems in military applications. Quantum dot-enabled devices and materials offered enhanced performance, durability, and security features, meeting the stringent requirements of defense and security applications.

Other verticals encompassed a diverse array of industries and applications where quantum dot technology found utilization, including automotive, aerospace, industrial manufacturing, and research laboratories.

By Application Analysis

Displays emerged as the leading segment within the Quantum Dot Market's By Application category, securing a dominant share of over 25%.

In 2023, Displays emerged as the leading segment within the Quantum Dot Market's By Application category, securing a dominant share of over 25%. This commanding position underscored the widespread adoption of quantum dot technology in display applications, driven by its ability to deliver vibrant colors, high resolution, and energy efficiency across various devices.

Following closely behind, Medical Devices represented another significant segment within the market landscape. Quantum dots found extensive utilization in medical imaging, biosensing, and targeted drug delivery systems, offering unprecedented precision, sensitivity, and biocompatibility for diagnostic and therapeutic applications in healthcare.

Solar Cells emerged as a pivotal segment, leveraging quantum dots' tunable optoelectronic properties to enhance the efficiency and performance of photovoltaic devices. Quantum dot-enabled solar cells promised to revolutionize renewable energy generation by boosting conversion efficiencies and reducing manufacturing costs, thereby addressing global energy challenges.

Photodetectors and Sensors constituted a vital segment, catering to a diverse range of applications spanning from automotive and consumer electronics to industrial monitoring and environmental sensing. Quantum dot-based photodetectors and sensors offered superior sensitivity, wavelength selectivity, and response times, driving their adoption across various sectors for precise detection and measurement purposes.

Lasers showcased substantial growth potential within the market, fueled by their ability to deliver coherent light sources with exceptional brightness and spectral purity. Quantum dot lasers found applications in telecommunications, healthcare, and materials processing, promising advancements in data transmission speeds, medical diagnostics, and precision manufacturing.

LED Lights represented a burgeoning segment characterized by energy-efficient lighting alternatives with superior color rendering capabilities. Quantum dot-enabled LEDs offered broader color gamuts, longer lifespans, and reduced energy consumption compared to conventional lighting sources, driving their adoption in residential, commercial, and industrial settings for enhanced illumination solutions.

Batteries and Energy Storage Systems emerged as an innovative segment, leveraging quantum dot materials to enhance energy density, charge/discharge rates, and cycle stability in rechargeable batteries. Quantum dot-based energy storage solutions held promise for powering portable electronics, electric vehicles, and grid-scale energy storage applications, thereby supporting the transition towards sustainable energy systems.

Transistors constituted a niche yet promising segment, exploring quantum dots' unique electronic properties for next-generation computing and electronics. Quantum dot transistors offered potential breakthroughs in low-power consumption, high-speed operation, and flexible device architectures, paving the way for novel computing paradigms and electronic devices.

The "Others" category encompassed a diverse array of applications and emerging technologies where quantum dot technology found utilization, including aerospace, automotive, telecommunications, and quantum computing.

Key Market Segments

By Processing Technique

- Colloidal Synthesis

- Fabrication

- Bio-Molecular Self-Assembly

- Viral Assembly

- Ligand Exchange

- Purification

By Product Type

- QD medical devices

- QD displays

- QD solar cells

- QD photodetectors/QD sensors

- QD lasers

- QD lighting (LED) solutions

- Batteries and Energy-Storage Systems

- QD transistors

- QD tags

By Material

- Cadmium-Based Quantum Dots

- Cadmium

- Free Quantum Dots

- Silicon

- Graphene

- Lead Sulfide

By Vertical

- Consumer

- Commercial

- Telecommunications

- Healthcare

- Defense

- Others

By Application

- Medical Devices

- Displays

- Solar Cells

- Photodetectors Sensors

- Lasers

- LED Lights

- Batteries and Energy Storage Systems

- Transistors

- Others

Growth Opportunity

Expansion in Defense, Aerospace, and Agriculture

The quantum dot market is poised for significant expansion into sectors such as defense, aerospace, and agriculture. In defense and aerospace, quantum dots can enhance imaging and sensor technologies, providing superior performance in challenging environments. In agriculture, quantum dots can improve plant growth monitoring and precision farming techniques. These new applications present lucrative growth opportunities for quantum dot technology, fostering innovation and market diversification.

Moisture Resistance in Displays

Moisture resistance is a critical attribute for the longevity and performance of quantum dot displays. Advances in moisture-resistant quantum dot materials enhance the durability and reliability of displays, particularly in high-humidity environments. This innovation not only improves product performance but also expands the applicability of quantum dots in diverse climatic conditions, driving market growth.

Innovation and Diversification

The continuous exploration of new applications for quantum dots in sectors such as healthcare, lighting, and biotechnology underscores their vast potential. Innovative uses, from advanced medical imaging techniques to energy-efficient lighting solutions, highlight the versatility of quantum dots. This ongoing innovation and diversification fuel market expansion and create new opportunities for growth and differentiation.

Latest Trends

Solar Cell Integration

The integration of quantum dots in solar cells is a key trend driving advancements in renewable energy technologies. Quantum dots enhance the efficiency and performance of solar cells, making them more competitive with traditional energy sources. This trend aligns with global sustainability goals and the increasing focus on clean energy solutions, positioning quantum dots as a critical component in the future of renewable energy.

Consumer Electronics Demand

The rising demand for high-performance consumer electronics, such as smartphones, tablets, and TVs, is a significant trend shaping the quantum dot market. Quantum dots offer superior display quality, energy efficiency, and color accuracy, meeting consumer expectations for premium electronic devices. This trend drives substantial investments in quantum dot technology, fostering innovation and market growth in the consumer electronics sector.

Revolutionizing Home Entertainment

The development of quantum dot-based TVs represents a transformative trend in the home entertainment market. Quantum dot technology enhances TV displays with richer colors, higher brightness, and improved energy efficiency, providing an unparalleled viewing experience. As leading manufacturers continue to innovate and launch quantum dot-based TVs, this trend is set to revolutionize the home entertainment landscape, driving substantial market growth.

Regional Analysis

North America emerges as the dominating region in the Quantum Dot market, commanding a substantial 40% share.

North America leads the Quantum Dot market with a dominating 40% share, driven by robust investments in research and development, as well as a well-established electronics industry. The region benefits from strong collaborations between academia, industry, and government institutions, fostering technological advancements and commercialization of quantum dot-based products. The presence of key end-user industries such as consumer electronics, healthcare, and defense further accelerates market growth in North America.

Europe emerges as a significant player in the Quantum Dot market, commanding a notable market share following North America. The region benefits from strong government support for scientific research and technological innovation, driving advancements in quantum dot materials and applications. Moreover, collaborations between academia and industry foster a conducive environment for market growth, with a growing emphasis on environmentally friendly quantum dot solutions.

Asia Pacific presents substantial growth opportunities in the Quantum Dot market, fueled by rapid industrialization, increasing consumer electronics demand, and strong government initiatives for technological innovation. The region benefits from a large consumer base and expanding end-user industries, driving demand for quantum dot-enabled products such as displays, solar cells, and medical devices.

While relatively smaller in market size compared to other regions, the Middle East & Africa region shows promising growth prospects in the Quantum Dot market. The region's focus on diversifying economies and adopting advanced technologies contributes to the adoption of quantum dot solutions in various applications, including electronics, healthcare, and energy. However, challenges such as limited access to technology and infrastructure may impact the pace of market growth in the region.

Latin America represents an emerging market for Quantum Dot technologies, characterized by increasing investments in research and development and growing awareness of quantum dot applications. Government initiatives to promote innovation and attract foreign investments further support market growth in Latin America. Despite challenges related to economic volatility and infrastructure limitations, the region presents lucrative opportunities for quantum dot manufacturers and technology providers.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global Quantum Dot (QD) market remains fiercely competitive with a lineup of key players driving innovation and market growth. Among these, several companies stand out for their significant contributions and strategic positioning within the industry.

NANOSYS, INC continues to be a prominent force, leveraging its expertise in QD technology to pioneer advancements in display applications, lighting, and biomedical imaging. With a strong focus on research and development, NANOSYS is well-positioned to maintain its market leadership.

Sigma-Aldrich Co., a key supplier of high-quality QD materials, plays a crucial role in the market ecosystem by providing essential components to researchers and manufacturers worldwide. Its wide product portfolio and robust distribution network ensure a steady supply chain for the industry.

Nanoco Technologies Limited remains a key player with its focus on commercializing QD technology across various sectors, including displays, lighting, and healthcare. Its strategic partnerships and licensing agreements bolster its market presence and drive adoption globally.

Thermo Fisher Scientific Inc., renowned for its analytical instruments and scientific expertise, contributes significantly to the QD market through its innovative solutions for QD characterization and synthesis, empowering researchers with essential tools for development and quality control.

The Dow Chemical Company's investments in QD manufacturing and application development underscore its commitment to driving market expansion. Its diverse product offerings and global reach enhance accessibility to QD-based technologies across industries.

Market Key Players

- NANOSYS, INC

- Sigma-Aldrich Co.

- Nanoco Technologies Limited

- Thermo Fisher Scientific Inc.

- The Dow Chemical Company

- Ocean NanoTech.

- QD Laser, Inc.

- NnCrystal US Corporation

- UbiQD Inc.

Recent Development

- In May 2024, IBM's Quantum Computing advancing AI algorithms, enhancing computational power for industries.

- In April 2024, Google's Quantum AI Lab pioneering quantum supremacy, unlocking new AI capabilities for transformative industry applications.

- In March 2024, Microsoft Quantum developing quantum-inspired algorithms, accelerating AI innovation across sectors.

Report Scope

Report Features Description Market Value (2023) USD 10.4 Bn Forecast Revenue (2033) USD 52.7 Bn CAGR (2024-2033) 18.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Processing Technique (Colloidal Synthesis, Fabrication, Bio-Molecular Self-Assembly, Viral Assembly, Ligand Exchange, Purification), By Product Type (QD medical devices, QD displays, QD solar cells, QD photodetectors/QD sensors, QD lasers, QD lighting (LED) solutions, Batteries and Energy-Storage Systems, QD transistors, QD tags), By Material (Cadmium-Based Quantum Dots, Cadmium, Free Quantum Dots, Silicon, Graphene, Lead Sulfide), By Vertical (Consumer, Commercial, Telecommunications, Healthcare, Defense, Others), By Application (Medical Devices, Displays, Solar Cells, Photodetectors Sensors, Lasers, LED Lights, Batteries and Energy Storage Systems, Transistors, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape NANOSYS, INC, Sigma-Aldrich Co., Nanoco Technologies Limited, Thermo Fisher Scientific Inc., The Dow Chemical Company, Ocean NanoTech., QD Laser, Inc., NnCrystal US Corporation, UbiQD Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- NANOSYS, INC

- Sigma-Aldrich Co.

- Nanoco Technologies Limited

- Thermo Fisher Scientific Inc.

- The Dow Chemical Company

- Ocean NanoTech.

- QD Laser, Inc.

- NnCrystal US Corporation

- UbiQD Inc.

Our Clients

View Our Licence Options