Global Pruritus Drugs Market By Product(Oral, Topical, Parenteral), By Application(Oncological Pruritus, Hematologic Pruritus, Renal Pruritus, Endocrine Pruritus, Cholestatic Pruritus), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

45461

-

May 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

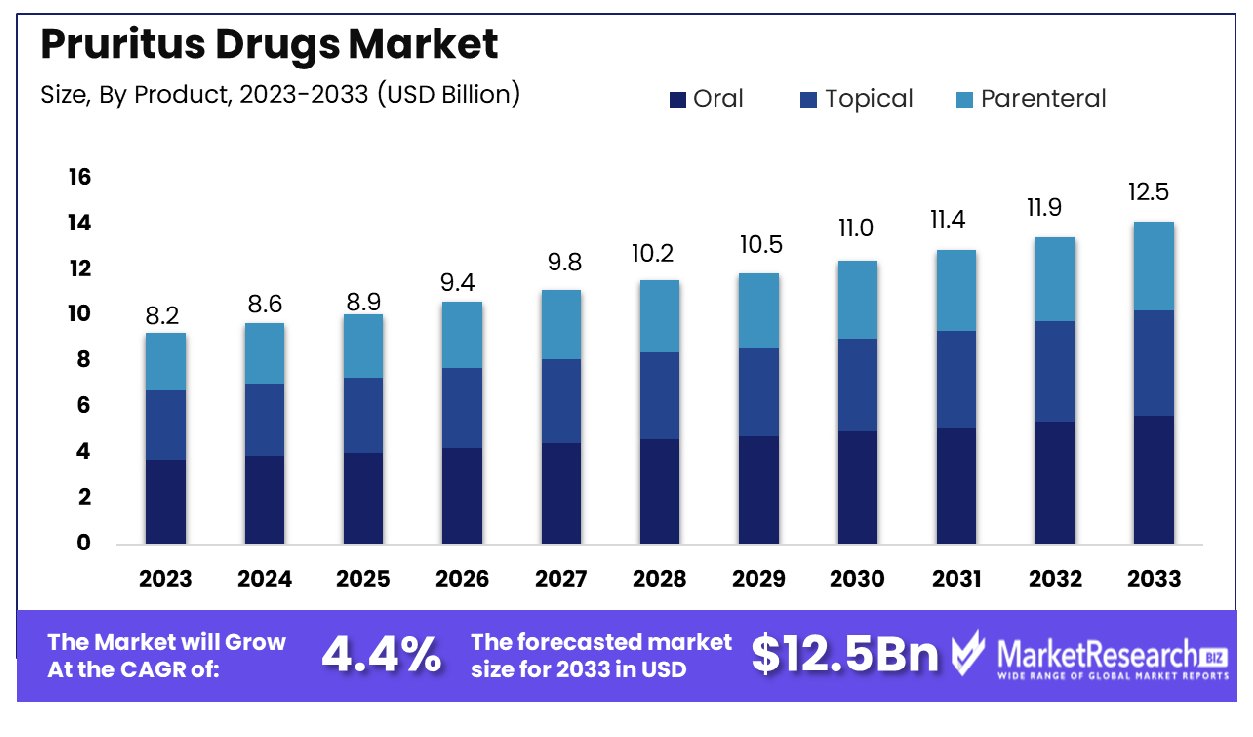

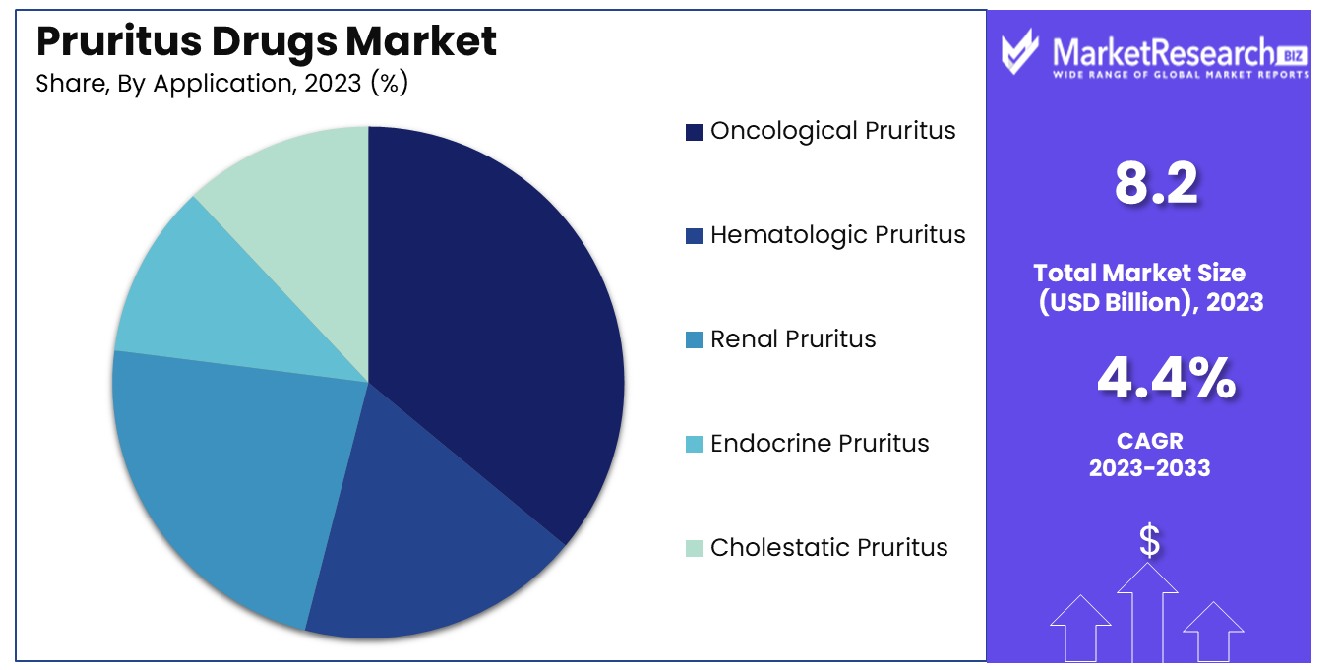

The Global Pruritus Drugs Market was valued at USD 8.2 billion in 2023. It is expected to reach USD 12.5 billion by 2033, with a CAGR of 4.4% during the forecast period from 2024 to 2033.

The Pruritus Drugs Market comprises pharmaceuticals designed to alleviate itching associated with various dermal conditions, including dermatitis, psoriasis, and allergic reactions. As pruritus can significantly impair quality of life, the demand for effective treatments is persistent across healthcare settings. This market segment addresses needs spanning topical agents, antihistamines, corticosteroids, and newer biologics that target underlying inflammatory processes.

Executives such as Product Managers should note the market's potential for expansion driven by increasing dermatological diagnoses and the development of innovative, patient-centric therapies. Strategic investment in this area promises growth and opportunities for differentiation in a competitive landscape.

The Pruritus Drugs Market is poised for substantial growth, fueled by a persistent demand for effective treatments across various pruritus-related conditions. An analysis reveals that pruritus, particularly when associated with primary biliary cholangitis, is often inadequately addressed, with approximately 33% of patients suffering from clinically significant pruritus not receiving the necessary treatment. This under-treatment highlights a significant gap in the current market offerings and presents a robust opportunity for pharmaceutical companies to introduce or improve pruritus-specific therapies.

Furthermore, the global burden of atopic dermatitis, a common cause of pruritus, continues to expand. In 2022, it was reported that around 223 million individuals worldwide were affected by this condition, including about 43 million children between the ages of 1 to 4 years. This demographic subset represents a particularly acute market segment that could benefit from pediatric-appropriate pruritus treatments, which are currently limited in both availability and efficacy.

Given these factors, the market for pruritus drugs is not only growing but also evolving with a marked shift towards developing treatments that can offer relief across a broader spectrum of symptoms and patient demographics. Companies venturing into this space can capitalize on the unmet medical needs by leveraging advanced R&D, strategic partnerships, and patient-centric treatment approaches. The potential for market expansion and profitability appears promising, contingent on the industry’s ability to innovate and address these critical gaps in care.

Key Takeaways

- Market Growth: The Global Pruritus Drugs Market was valued at USD 8.2 billion in 2023. It is expected to reach USD 12.5 billion by 2033, with a CAGR of 4.4% during the forecast period from 2024 to 2033.

- By Product: Oral formulations dominated the market with a 60% share.

- By Application: Oncological pruritus accounted for 32% of market dominance.

- Regional Dominance: North America holds a 46% share of the global pruritus drugs market.

- Growth Opportunity: The global pruritus drugs market is expanding with advancements in targeted therapies and increasing demand for topical and oral corticosteroids, driven by efficacy and evolving patient needs.

Driving factors

Increasing Prevalence of Skin Diseases

The increasing prevalence of skin diseases globally acts as a primary catalyst for the growth of the Pruritus Drugs Market. Dermatological conditions such as eczema, psoriasis, and atopic dermatitis, which often manifest with pruritus (itching), have been reported with rising incidence rates.

This trend significantly drives the demand for effective pruritus treatments. As the number of individuals suffering from these conditions grows, so does the patient pool requiring medical interventions for itch relief, thereby expanding the market size for pruritus drugs.

Streamlining of Regulatory Approvals and Licensing

The standardization and streamlining of regulatory approvals and licensing processes significantly enhance the pruritus drugs market's growth potential. By simplifying and expediting the regulatory framework, pharmaceutical companies can reduce the time and resources required to bring new pruritus treatments to market.

This efficiency not only speeds up product launches but also encourages companies to invest in the development of new and improved pruritus therapies, knowing that the pathway to market approval is becoming increasingly navigable.

Mergers, Acquisitions, and Partnerships

Mergers, acquisitions, and strategic partnerships within the pharmaceutical industry have proven to be decisive factors in the development and distribution of pruritus treatments. These collaborations often result in enhanced research and development capabilities, sharing of technological expertise, and expanded distribution networks, which collectively boost the market's growth.

By combining resources and expertise, companies can accelerate the development of innovative pruritus drugs and expand their reach to untapped markets, further driving market expansion.

Restraining Factors

Side Effects of Existing Medications

One significant restraint in the pruritus drugs market is the side effects associated with existing medications. Many current pruritus treatments come with a range of potential side effects, from mild discomforts like dry skin and dizziness to more severe reactions such as immune system suppression when using corticosteroids.

These adverse effects can deter patients from continuing or initiating therapy, directly impacting patient compliance and the overall demand for these drugs. The fear of side effects can also influence healthcare providers' prescribing behaviors, potentially restricting the market's expansion.

High Cost of Treatment

The high cost of pruritus treatments poses another substantial barrier to market growth. Advanced therapies, particularly those involving newer pharmaceutical formulations or biologics, can be prohibitively expensive, making them inaccessible to a significant portion of the potential patient base, especially in less developed regions.

This economic factor not only limits the market size directly by reducing the number of patients who can afford these treatments but also indirectly by influencing insurance coverage and reimbursement policies, which may not favor high-cost treatments unless they demonstrate clear cost-benefit advantages.

By Product Analysis

The oral segment dominated the market, accounting for 60% of total sales.

In 2023, the Pruritus Drugs Market was notably segmented into three primary delivery forms: Oral, Topical, and Parenteral. Oral medications held a dominant market position within this category, capturing more than 60% of the market share. This substantial share can be attributed to the preference for oral drugs due to their ease of administration and efficacy in managing systemic pruritic conditions.

Topical treatments, while less prevalent than oral formulations, also play a critical role in the management of pruritus, particularly for localized symptoms. These formulations are favored for their direct application, which minimizes systemic exposure and potential side effects. Despite their targeted approach, topical treatments accounted for a smaller segment of the market.

Parenteral routes, typically reserved for more severe or refractory cases of pruritus, constituted the smallest market segment. These formulations are usually administered in a clinical setting, limiting their use to cases where oral and topical treatments are ineffective.

The dominance of oral pruritus drugs is further reinforced by ongoing advancements in pharmaceutical formulations, which improve bioavailability and patient compliance, thus supporting market growth. Additionally, the development of newer agents that can effectively target underlying causes of pruritus via systemic routes continues to drive preference for oral medications.

By Application Analysis

Oncological pruritus led, representing 32% of the overall market share.

In 2023, the Pruritus Drugs Market was segmented by application into Oncological Pruritus, Hematologic Pruritus, Renal Pruritus, Endocrine Pruritus, and Cholestatic Pruritus. Oncological Pruritus held a dominant market position, capturing more than a 32% share. This prevalence is primarily due to the high incidence of pruritus as a common symptom in cancer patients, often resulting from either the malignancy itself or as a side effect of oncological treatments such as chemotherapy and radiation.

Hematologic Pruritus, associated with disorders such as polycythemia vera, also constituted a significant portion of the market. The need for specific treatments targeting the underlying hematologic causes of itch contributes to the segment’s robust presence in the market landscape.

Renal Pruritus, is prevalent in patients with chronic kidney disease or those on dialysis, and Endocrine Pruritus, often linked with thyroid dysfunctions, represents other critical segments. These conditions frequently necessitate long-term management strategies, underpinning steady demand within the pruritus therapeutics market.

Cholestatic Pruritus, which occurs in conditions affecting bile flow such as primary biliary cholangitis, though a smaller segment, is notably driven by the lack of effective treatments for the underlying liver conditions, thus highlighting an area of unmet medical need and opportunity for drug development.

The segmentation of the market by application underscores the diverse etiologies of pruritus and the necessity for specialized therapeutic approaches tailored to the pathophysiology of each condition, thereby driving the development and adoption of targeted pruritus drugs.

Key Market Segments

By Product

- Oral

- Topical

- Parenteral

By Application

- Oncological Pruritus

- Hematologic Pruritus

- Renal Pruritus

- Endocrine Pruritus

- Cholestatic Pruritus

Growth Opportunity

Opportunities in the Development of Novel Targeted Therapies for Pruritus

The global pruritus drugs market is poised for transformation as opportunities abound in the development of novel targeted therapies. These innovative treatments focus on addressing the underlying causes of pruritus with increased specificity and fewer side effects compared to traditional therapies. The shift towards targeted therapies can be attributed to advancements in understanding the pathophysiology of pruritus, which have unveiled new molecular targets.

This development not only promises enhanced efficacy but also reduces the burden of side effects, a crucial factor in patient compliance and satisfaction. The introduction of these novel drugs is expected to catalyze market growth, as they meet the unfulfilled needs of patients seeking more effective and safer treatment options.

Rising Demand for Topical and Oral Corticosteroids in Pruritus Treatment

Parallel to the innovation in targeted therapies, there is a rising demand for topical and oral corticosteroids, driven by their established efficacy in managing pruritus symptoms. These medications remain a cornerstone in pruritus treatment, particularly for conditions like atopic dermatitis and psoriasis, where inflammation plays a significant role.

The demand is further buoyed by the development of formulations that minimize systemic absorption and side effects. As the prevalence of allergic reactions and autoimmune diseases continues to rise globally, the demand for these corticosteroids is expected to surge, supporting the overall growth of the pruritus drugs market. This trend underscores the market's expansion as it adapts to the evolving healthcare needs and preferences of a growing patient population.

Latest Trends

Increased Interest in Non-Prescription Medications for Pruritus

In 2023, the global pruritus drugs market is witnessing a significant shift towards non-prescription medications. This trend is driven by a growing consumer preference for over-the-counter (OTC) options that allow for self-treatment of pruritus without the need for medical supervision. OTC medications are becoming increasingly popular due to their perceived safety, convenience, and cost-effectiveness.

Manufacturers are responding to this demand by expanding their portfolios of OTC pruritus treatments, which are formulated to meet stringent safety standards while providing effective symptom relief. This shift is not only democratizing pruritus treatment but also stimulating market growth as accessibility to these treatments broadens.

Role of Digital Therapeutics in Managing Pruritus

Concurrently, there is an emerging trend in the pruritus drugs market involving the integration of digital therapeutics. These innovative solutions, including mobile applications and wearable devices, are designed to manage pruritus through non-pharmacological means. Digital therapeutics offer personalized treatment options based on user input, leveraging technology to track symptoms, trigger factors, and treatment efficacy.

This approach supports self-management and can be used in conjunction with traditional medications, enhancing overall treatment outcomes. The adoption of digital therapeutics is expanding as patients and healthcare providers recognize their potential to provide real-time, data-driven insights into pruritus management, marking a forward-thinking development in the market landscape.

Regional Analysis

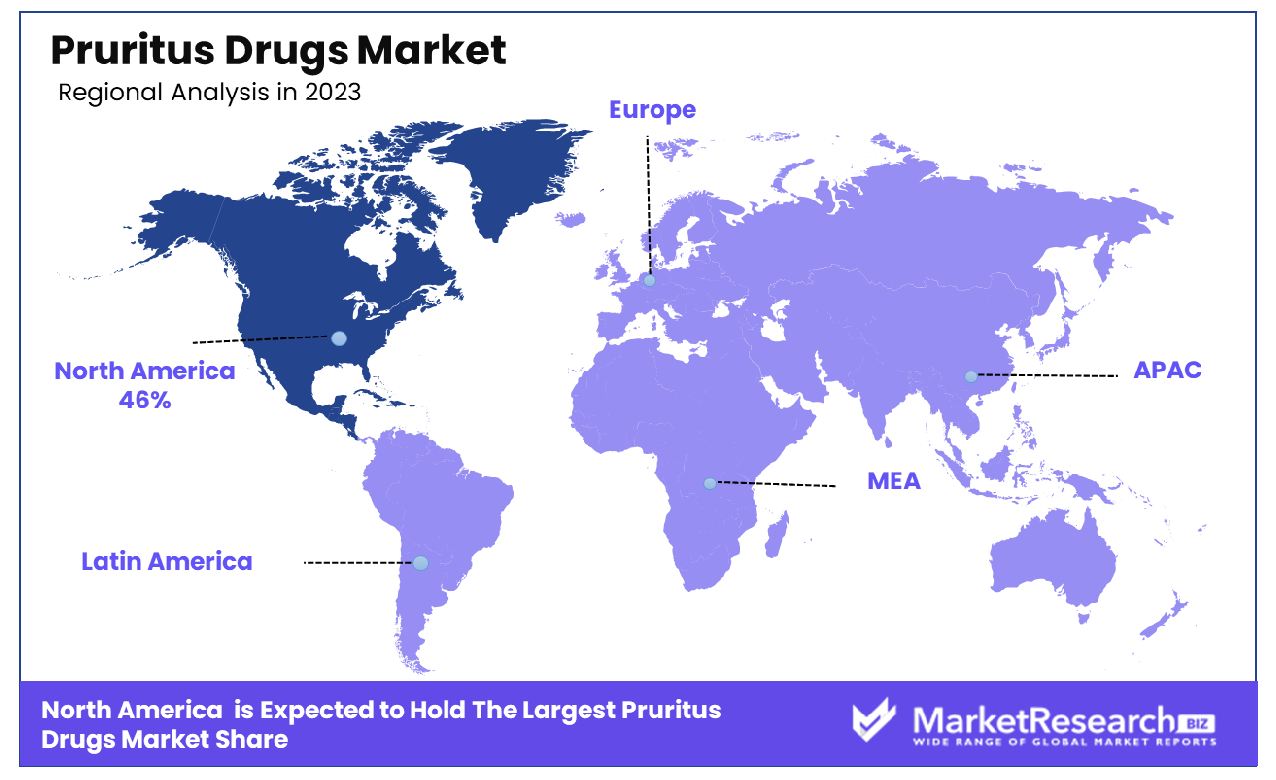

North America holds a 46% share of the global pruritus drugs market, leading in demand.

The global pruritus drugs market exhibits varied dynamics across different regions, reflecting distinct healthcare infrastructures, regulatory landscapes, and patient demographics. North America dominates the market, accounting for 46% of the global share. This substantial market presence is fueled by advanced healthcare systems, high awareness of treatment options, and the presence of major pharmaceutical companies engaged in pruritus drug development.

Europe follows as a significant player, driven by robust healthcare policies and a growing elderly population susceptible to skin conditions that cause pruritus. The region benefits from favorable reimbursement scenarios and strong initiatives promoting skin health, which bolster the demand for pruritus medications.

The Asia Pacific region is identified as the fastest-growing segment within the pruritus drugs market. This growth is propelled by increasing healthcare expenditure, rising awareness of dermatological conditions, and the expanding presence of international pharmaceutical companies. Countries like China and India are pivotal markets, due to their large populations and increasing access to healthcare services.

The Middle East & Africa, and Latin America regions, though smaller in market share, are emerging as potential growth areas. These regions are experiencing gradual growth due to improved healthcare infrastructure, rising disposable incomes, and an increasing prevalence of dermatological disorders. Public health initiatives and an expanding generic drugs market are supporting the growth in these regions.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global pruritus drugs market will be shaped by strategic initiatives and diverse portfolios of key players. AbbVie Inc., renowned for its innovative approaches, continues to lead with targeted therapies that address underlying causes of pruritus. Similarly, Astellas Pharma Inc. and Eli Lilly and Co. are at the forefront due to their commitment to developing next-generation biologics with improved efficacy and safety profiles.

Almirall SA and Bristol-Myers Squibb Co. stand out for their robust pipelines in dermatological research, focusing on new molecular targets. Cara Therapeutics Inc., on the other hand, has gained attention with its novel kappa opioid receptor agonists that offer a unique mechanism of action to treat pruritus without the side effects associated with traditional treatments.

In the Asia-Pacific region, companies like Sun Pharmaceutical Industries Ltd. and Cipla Ltd. are expanding their market presence by leveraging cost-effective production and extensive distribution networks. These companies are vital in making pruritus medications more accessible in emerging markets.

Glenmark Pharmaceuticals Ltd., Lupin Ltd., and Ipca Laboratories Ltd. contribute significantly to the generic drugs segment, offering affordable alternatives to patented medications. This approach is crucial in regions where cost constraints are a major barrier to accessing healthcare.

Merck and Co. Inc., Novartis AG, and Pfizer Inc. continue to dominate through their extensive research and development capabilities. These companies are investing heavily in new drug formulations and delivery systems to enhance the patient experience.

Roivant Sciences Ltd., Sanofi SA, and GlaxoSmithKline Plc are exploring digital therapeutics and advanced drug delivery systems to complement their pharmaceutical offerings, thereby enhancing treatment efficacy and patient compliance.

Market Key Players

- AbbVie Inc.

- Almirall SA

- Astellas Pharma Inc.

- Bristol-Myers Squibb Co.

- Cara Therapeutics Inc.

- Eisai Co. Ltd.

- Eli Lilly and Co.

- Glenmark Pharmaceuticals Ltd.

- Ipca Laboratories Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Roivant Sciences Ltd.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Cipla Ltd.

- GlaxoSmithKline Plc

- Lupin Ltd.

Recent Development

- In April 2024, Livmarli was recommended for Canadian reimbursement by the CADTH committee, aiding Alagille syndrome patients with pruritus. Mirum Pharmaceuticals' CEO Chris Peetz lauds the decision, aiming for wider access across provinces.

- In March 2024, the FDA approved Mirum Pharmaceuticals' LIVMARLI for cholestatic pruritus in PFIC patients aged 5 and above. Phase III MARCH trial data support the breakthrough therapy, advancing treatment options.

Report Scope

Report Features Description Market Value (2023) USD 8.2 Billion Forecast Revenue (2033) USD 12.5 Billion CAGR (2024-2032) 4.4% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Oral, Topical, Parenteral), By Application(Oncological Pruritus, Hematologic Pruritus, Renal Pruritus, Endocrine Pruritus, Cholestatic Pruritus) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape AbbVie Inc., Almirall SA, Astellas Pharma Inc., Bristol-Myers Squibb Co., Cara Therapeutics Inc., Eisai Co. Ltd., Eli Lilly and Co., Glenmark Pharmaceuticals Ltd., Ipca Laboratories Ltd., Merck and Co. Inc., Novartis AG, Pfizer Inc., Roivant Sciences Ltd., Sanofi SA, Sun Pharmaceutical Industries Ltd., Cipla Ltd., GlaxoSmithKline Plc, Lupin Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- AbbVie Inc.

- Almirall SA

- Astellas Pharma Inc.

- Bristol-Myers Squibb Co.

- Cara Therapeutics Inc.

- Eisai Co. Ltd.

- Eli Lilly and Co.

- Glenmark Pharmaceuticals Ltd.

- Ipca Laboratories Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Roivant Sciences Ltd.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Cipla Ltd.

- GlaxoSmithKline Plc

- Lupin Ltd.

Our Clients

View Our Licence Options