Global Portable Oxygen Concentrator Market By Product Type(Portable, Fixed), By Technology(Continuous Flow, Pulse Flow), By Indication(Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep Apnea, Others), By Application(Homecare, Travel, Hospital, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

49112

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

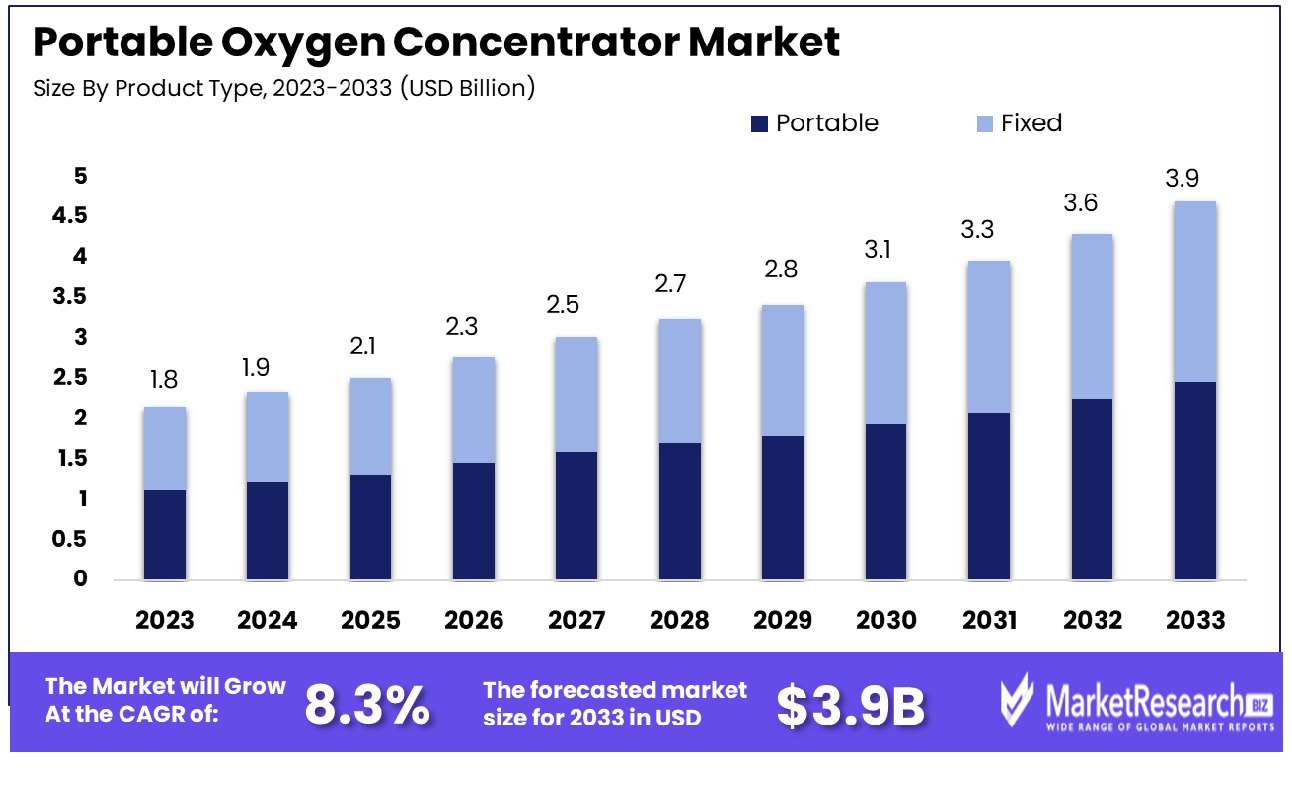

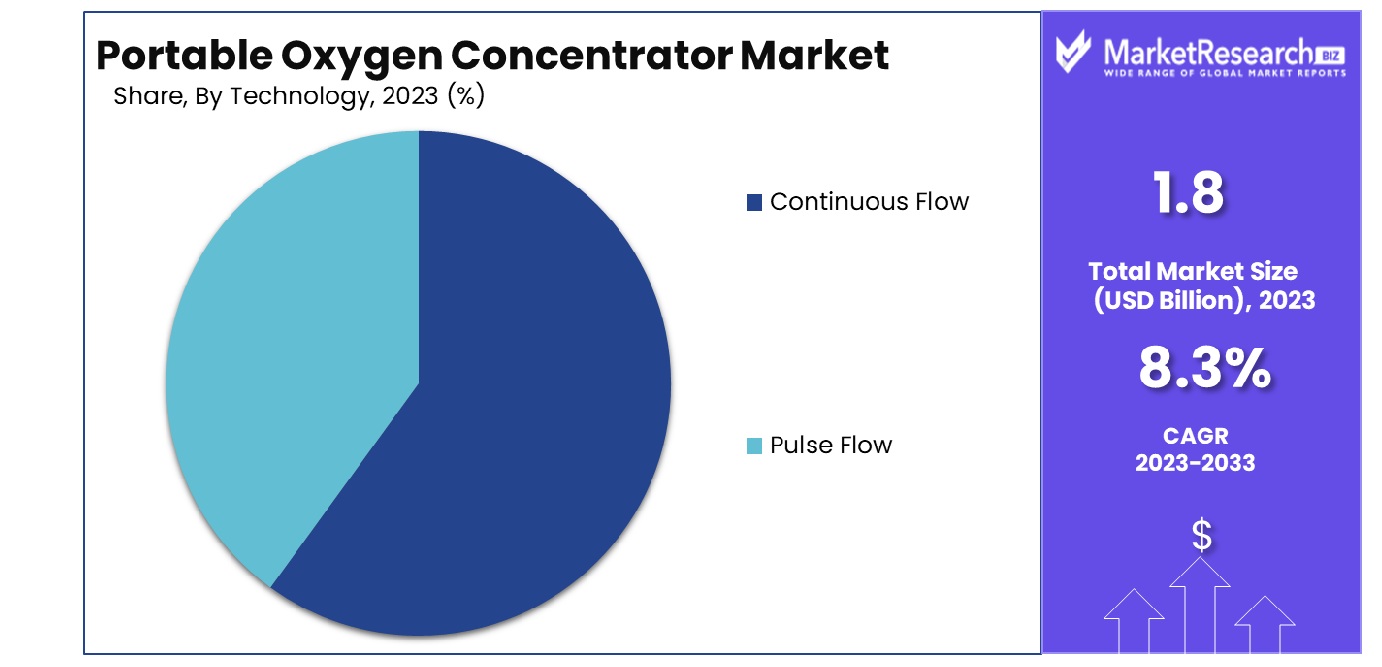

The Global Portable Oxygen Concentrator Market was valued at USD 1.8 billion in 2023. It is expected to reach USD 3.9 billion by 2033, with a CAGR of 8.3% during the forecast period from 2024 to 2033.

The portable oxygen concentrator market comprises devices designed to provide oxygen therapy to patients suffering from respiratory disorders such as chronic obstructive pulmonary disease (COPD) and pulmonary fibrosis. These lightweight, mobile units offer significant advantages over traditional oxygen tanks, enhancing patient mobility and quality of life.

As healthcare continues to advance towards home-based treatment, this market is experiencing substantial growth, driven by an aging global population and the rising prevalence of respiratory diseases. Key market players are focusing on technological innovations to improve device efficiency and portability, addressing the evolving needs of healthcare systems and patients alike.

The portable oxygen concentrator (POC) market is witnessing significant growth, primarily driven by technological advancements and an increasing prevalence of respiratory diseases. As healthcare paradigms shift towards more home-based and patient-centric models, the demand for portable oxygen solutions is expected to surge. These devices not only provide a lifeline for individuals with severe respiratory conditions but also offer enhanced mobility and independence, aligning with the broader trends towards outpatient care and aging in place.

From an operational cost perspective, the ongoing expense associated with the use of regular-flow 350-watt POCs, which are typically used continuously (24 hours/day), varies significantly across different U.S. states. The estimated annual electricity cost for these units ranges from $322 to $853, with a median cost of $322.

Notably, the operational costs decrease substantially when the devices are used for shorter durations, such as 12 or 8 hours per day. This variability in operational costs is an important consideration for both users and healthcare providers when making decisions about oxygen therapy management.

Furthermore, comparative studies, such as one involving the Eclipse 3 model, reveal that some POCs can deliver larger oxygen boluses and significantly enhance patient mobility. For instance, Eclipse 3 has been shown to allow patients to walk farther than other models, which is a critical advantage in terms of improving the quality of life for users (both p<0.01). This data underscores the importance of choosing the right POC model based on specific patient needs and lifestyle requirements, highlighting the necessity for continuous innovation and patient-focused engineering in the market.

Key Takeaways

- Market Growth: The Global Portable Oxygen Concentrator Market was valued at USD 1.8 billion in 2023. It is expected to reach USD 3.9 billion by 2033, with a CAGR of 8.3% during the forecast period from 2024 to 2033.

- By Product Type: Portable product type dominated with a significant 56.3% market share.

- By Technology: Continuous Flow technology leads remarkably, securing 68.1% of the market.

- By Indication: Chronic Obstructive Pulmonary Disease (COPD) indication prevails at 43.1% dominance.

- By Application: Homecare applications overwhelmingly lead, holding a 57.6% market share.

- Regional Dominance: Regional Dominance: leads with a 42.3% share in the Portable Oxygen Concentrator Market.

Driving factors

Increasing Prevalence of Respiratory Diseases

The escalating incidence of respiratory ailments globally serves as a primary catalyst for the expansion of the Portable Oxygen Concentrator Market. Chronic respiratory diseases, such as chronic obstructive pulmonary disease (COPD) and asthma, necessitate long-term oxygen therapy, which portable oxygen concentrators provide with greater ease and flexibility compared to traditional systems.

According to the World Health Organization, COPD is projected to become the third leading cause of death worldwide by 2030, underscoring the critical demand for effective and mobile oxygen therapy solutions. This growing burden of respiratory diseases directly correlates with increased adoption rates of portable oxygen concentrators, driving market growth.

Aging Global Population

An aging global population significantly contributes to the growth of the Portable Oxygen Concentrator Market. Older adults are more susceptible to respiratory conditions that require oxygen therapy, such as COPD and pulmonary fibrosis. The United Nations reports that the proportion of the global population over 60 years could reach nearly 22% by 2050.

This demographic shift increases the demand for healthcare solutions that enhance the quality of life, including mobile oxygen delivery systems. Portable oxygen concentrators offer the elderly more autonomy and mobility, thereby supporting a higher standard of living while managing chronic conditions.

Technological Advancements in Concentrator Design

Technological advancements in the design and functionality of portable oxygen concentrators have substantially driven their market adoption. Modern concentrators are not only lighter and more efficient but also feature enhanced battery life and quieter operation, which appeal to a broader range of users.

Innovations such as pulse dose technology—which delivers oxygen more efficiently based on breathing patterns—and smart capabilities for monitoring oxygen saturation levels enhance patient compliance and comfort. These technological improvements make portable oxygen concentrators a more attractive option for individuals seeking effective and convenient respiratory support, thus fueling market growth.

Restraining Factors

High Cost of Portable Oxygen Concentrators

The substantial cost associated with portable oxygen concentrators poses a significant barrier to their widespread adoption, impacting market growth negatively. These devices, essential for patients requiring continuous oxygen therapy, are often priced between $2,000 and $3,500, which can be prohibitive for many, especially in under-resourced or developing regions.

Insurance coverage limitations further exacerbate this issue, as not all plans fully cover the cost of these concentrators, forcing patients to bear a substantial portion of the expense out-of-pocket. This financial burden restricts accessibility for a large segment of the population who might otherwise benefit from the enhanced mobility and independence that these devices offer, thus restraining the market's expansion.

Regulatory and Operational Challenges

Regulatory and operational challenges further complicate the market dynamics for portable oxygen concentrators. These devices must comply with stringent safety and performance standards set by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). The process of obtaining approval can be lengthy and costly, discouraging innovation and delaying the introduction of new products into the market.

Additionally, operational challenges, including maintenance and repair services, which are essential for the reliable functioning of these devices, often present logistical difficulties. These factors combined create hurdles that not only limit market growth but also affect consumer confidence in adopting portable oxygen therapy solutions. Together, these restraining factors highlight the critical areas where market participants must focus to enhance affordability and streamline regulatory pathways to foster broader market acceptance and growth.

By Product Type Analysis

The portable segment held a dominant share of 56.3%.

In 2023, Portable held a dominant market position in the By Product Type segment of the Portable Oxygen Concentrator Market, capturing more than a 56.3% share. This segment's robust performance is primarily driven by the increasing demand for lightweight and mobile solutions among patients requiring long-term oxygen therapy. The flexibility offered by portable oxygen concentrators has been pivotal in enhancing patient mobility and quality of life, thereby fueling market growth.

On the other hand, the Fixed segment also showed significant activity, securing a substantial portion of the market. These devices are typically utilized in stationary, home-based settings, offering continuous oxygen supply with higher capacity systems. Despite their less versatile nature compared to portable models, fixed oxygen concentrators remain essential for patients with intensive oxygen needs, especially in elder care and severe respiratory conditions.

The market dynamics for portable oxygen concentrators are influenced by several factors including advancements in battery technology, which have extended the device's life and operational efficiency, making them more appealing to a broader demographic. Additionally, regulatory approvals and increased healthcare spending have facilitated the wider adoption of these devices across various regions.

Investment in innovation and expansion of distribution channels are critical strategies adopted by key players to capitalize on the growing demand for both portable and fixed oxygen concentrators. As the market continues to evolve, the interplay between technological advancements and consumer preferences will likely dictate future trends and opportunities within this sector.

By Technology Analysis

In terms of technology, continuous-flow oxygen concentrators led with 68.1%.

In 2023, Continuous Flow held a dominant market position in the By Technology segment of the Portable Oxygen Concentrator Market, capturing more than a 68.1% share. This technology's leading status can be attributed to its critical role in providing a steady stream of oxygen, which is essential for patients with severe respiratory conditions who require a constant and reliable oxygen supply. Continuous flow technology is particularly favored in clinical settings and among patients who need higher levels of oxygen, both during the day and at night.

Conversely, the Pulse Flow technology also holds a significant place in the market. This technology is engineered to deliver oxygen in bursts during the initial phase of inhalation, making it highly efficient and energy-saving for patients with moderate oxygen requirements. The lightweight and energy-efficient characteristics of pulse flow concentrators appeal to active patients, offering them greater mobility and convenience.

The market for portable oxygen concentrators is influenced by technological innovations aimed at enhancing patient compliance and comfort. Continuous Flow concentrators are increasingly being integrated with smart features like auto-adjust settings and detailed usage tracking, which enhances patient monitoring and device efficiency. Meanwhile, advancements in Pulse Flow technology focus on minimizing device size and improving battery life, catering to the lifestyle needs of mobile patients.

The growth trajectory of this market segment underscores the critical nature of technological adaptations in meeting diverse patient needs and expanding the application scope of oxygen concentrators. As the healthcare landscape continues to evolve, the demand for both Continuous and Pulse Flow technologies is expected to grow, driven by an aging population and rising respiratory ailments globally.

By Indication Analysis

Regarding indication, 43.1% of the market is dominated by Chronic Obstructive Pulmonary Disease (COPD).

In 2023, Chronic Obstructive Pulmonary Disease (COPD) held a dominant market position in the Indication segment of the Portable Oxygen Concentrator Market, capturing more than a 43.1% share. This prevalence is largely due to the high global incidence and severity of COPD, which necessitates reliable and continuous oxygen therapy to manage symptoms and improve quality of life. The persistent need for efficient oxygen delivery systems in managing COPD has spurred significant advancements in both product development and patient accessibility.

Asthma, another critical segment, also leverages portable oxygen concentrators, especially during severe asthma attacks which require immediate oxygen supplementation to prevent complications. However, the use of these devices in asthma is less frequent compared to COPD, as it is usually not part of the standard management protocol except in acute cases.

The Sleep Apnea segment represents a growing market driven by the increasing recognition of the condition and its impact on overall health. Oxygen concentrators are used alongside CPAP machines to ensure adequate oxygenation throughout the night in severe cases of sleep apnea.

The "Others" category encompasses various respiratory conditions and emergencies where portable oxygen therapy is essential. This includes conditions such as pulmonary fibrosis and acute respiratory distress syndrome (ARDS), where supplemental oxygen helps stabilize patients and improve outcomes.

By Application Analysis

Within applications, homecare usage of oxygen concentrators dominated at 57.6%.

In 2023, Homecare held a dominant market position in the By Application segment of the Portable Oxygen Concentrator Market, capturing more than a 57.6% share. This substantial market share is indicative of the growing preference for home-based healthcare solutions, where patients seek comfort and autonomy in managing chronic respiratory conditions. The increase in homecare usage is propelled by advancements in oxygen concentrator technology that offer quieter, more energy-efficient, and user-friendly devices, making long-term home oxygen therapy more viable and comfortable.

The Travel segment also represents a significant portion of the market, reflecting the increasing mobility of patients requiring oxygen therapy. Portable oxygen concentrators designed for travel are compact, lightweight, and FAA-approved, enabling patients to maintain their oxygen therapy while traveling, thus supporting an active lifestyle.

Hospitals constitute another key application area for portable oxygen concentrators, although their market share is smaller compared to home care. In hospital settings, these devices are primarily used for patient mobility and transport within the facility, rather than as a primary oxygen supply, contributing to their lower market penetration in this sector.

The "Others" category includes various non-traditional settings such as emergency medical services (EMS) and outpatient clinics, where portable units provide critical support in diverse clinical scenarios and short-term treatments.

Overall, the market is experiencing growth across all applications, driven by technological innovations that enhance portability, device functionality, and patient compliance, thereby broadening the scope of applications for portable oxygen concentrators.

Key Market Segments

By Product Type

- Portable

- Fixed

By Technology

- Continuous Flow

- Pulse Flow

By Indication

- Chronic Obstructive Pulmonary Disease (COPD)

- Asthma

- Sleep Apnea

- Others

By Application

- Homecare

- Travel

- Hospital

- Others

Growth Opportunity

Expansion into Emerging Markets

The expansion into emerging markets represents a significant growth opportunity for the global Portable Oxygen Concentrator Market in 2023. As healthcare infrastructure improves in these regions, coupled with increasing healthcare spending and rising awareness of respiratory conditions, there is a growing demand for medical devices that offer mobility and autonomy to patients.

Emerging markets such as India, China, and Brazil are experiencing rapid urbanization and lifestyle changes that contribute to the prevalence of respiratory diseases, thus driving the need for portable oxygen solutions. The key to capitalizing on this opportunity lies in creating affordable models tailored to the economic constraints and specific healthcare needs of these regions, along with establishing strong local partnerships to navigate market entry and distribution challenges effectively.

Integration of IoT and Connectivity Features

The integration of the Internet of Things (IoT) and connectivity features into portable oxygen concentrators is poised to revolutionize patient care, presenting substantial growth opportunities in 2023. By incorporating advanced sensors, these devices can monitor a patient’s oxygen levels and usage patterns in real time, transmitting data directly to healthcare providers for better disease management and personalized care plans.

Connectivity also enhances user convenience, allowing for remote troubleshooting and updates, which improves device reliability and patient trust. As the global focus shifts towards personalized and preventive healthcare, the market for smart, connected portable oxygen concentrators is expected to see robust growth. Companies that innovate to combine medical efficacy with advanced technology will likely gain a competitive edge in this evolving market landscape.

Latest Trends

Increased Focus on Lightweight and Compact Models

In 2023, the global Portable Oxygen Concentrator Market stands to benefit significantly from an increased focus on developing lightweight and compact models. The trend towards miniaturization addresses a critical consumer demand for more portable and less obtrusive medical devices that can be easily carried and used on the go. As technology advances, manufacturers can reduce the size and weight of these concentrators without compromising on their oxygen delivery efficiency or battery life.

This evolution is particularly appealing to a younger demographic of patients who lead active lifestyles and value discretion and mobility. By innovating in this area, companies can tap into a broader customer base, including those who might have previously been reluctant to use bulkier traditional oxygen therapy systems, thus driving market expansion.

Rising Adoption of Telehealth for Chronic Disease Management

The rising adoption of telehealth for chronic disease management presents a substantial growth opportunity for the portable oxygen concentrator market in 2023. With the increasing integration of digital health technologies, portable oxygen concentrators equipped with connectivity features can play a pivotal role in remote patient monitoring systems. These devices can collect and transmit data on oxygen usage and patient respiratory function directly to healthcare providers via telehealth platforms.

This capability allows for more timely and accurate adjustments to therapy, enhancing patient outcomes. Furthermore, the ongoing global health crisis has accelerated the acceptance of telehealth services, making it a favorable time for concentrator manufacturers to align their products with telehealth applications. This alignment not only meets current healthcare trends but also broadens the market reach to include health systems and insurers, enhancing the overall growth potential in the sector.

Regional Analysis

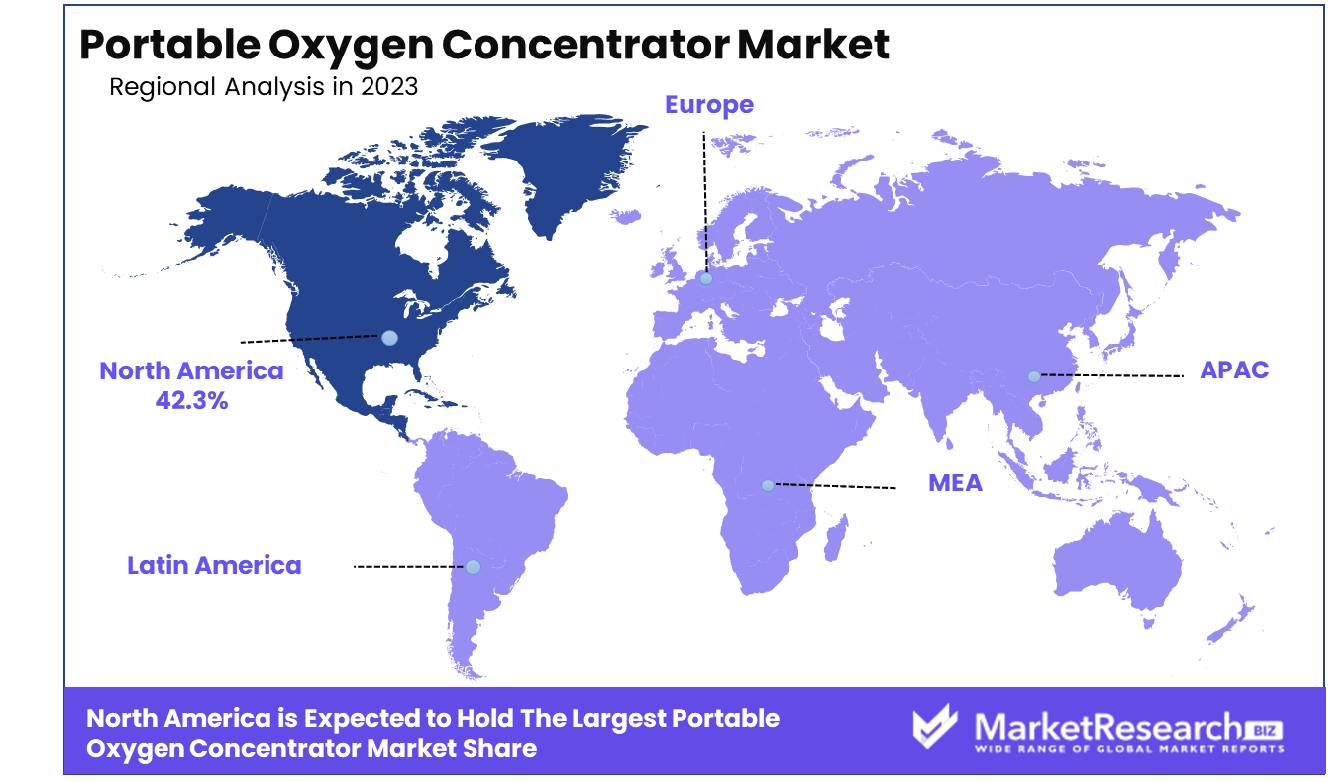

North America dominates the Portable Oxygen Concentrator Market, holding a significant 42.3% share of the global market.

The Portable Oxygen Concentrator Market is segmented into various regions, each displaying distinct growth dynamics and market penetration. North America is the dominant region, accounting for 42.3% of the global market. This high market share can be attributed to the advanced healthcare infrastructure, high prevalence of respiratory diseases, and substantial adoption of technologically advanced healthcare solutions in the United States and Canada.

In Europe, the market is driven by increasing healthcare expenditures, an aging population, and stringent regulations regarding healthcare quality. European countries have shown a keen interest in adopting portable solutions that offer patients independence and improve their quality of life, making Europe a significant market for these devices.

The Asia Pacific region presents the fastest growth opportunities, driven by improving healthcare infrastructures, rising disposable incomes, and increasing awareness about portable medical devices in countries like China, Japan, and India. The region's large population base and increasing prevalence of chronic diseases further amplify the demand for portable oxygen concentrators.

The markets in the Middle East & Africa and Latin America are emerging gradually. These regions show potential due to urbanization, rising healthcare standards, and the growing middle class. However, the high cost of devices and limited healthcare infrastructure remain challenges that need to be addressed to tap into the full market potential.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

CAIRE Inc., Chart Industries, Inc., and ResMed, all based in the US, are pioneering with robust technological advancements in oxygen concentrator functionality. Their commitment to integrating IoT features has enabled better patient monitoring and enhanced device usability, positioning them as leaders in both innovation and market share in North America.

Inogen, Inc. and Invacare Corporation continue to excel in expanding their global footprint by tapping into emerging markets with tailored products that meet specific regional healthcare needs. Inogen, known for its direct-to-consumer sales model, has effectively increased its market penetration by enhancing consumer access to portable oxygen solutions.

Koninklijke Philips N.V from the Netherlands and ResMed have made significant strides in integrating their devices with telehealth systems, aligning with the global shift towards remote healthcare. This strategy not only boosts patient adherence to oxygen therapy but also opens new avenues for data analytics in patient health management.

Emerging players like Nidek Medical (India) and Foshan Keyhub Electronic Industries Co. Ltd. (Guangdong) are critical in driving adoption in Asia Pacific by offering cost-effective devices suited to local economic conditions, thus broadening the market base.

GCE Group (Sweden) focuses on the European market, innovating in device miniaturization and user-friendly designs that appeal to a population with a high prevalence of chronic respiratory diseases and a growing elderly demographic.

Market Key Players

- Besco Medical Co., LTD (China)

- CAIRE Inc. (US)

- Chart Industries, Inc. (US)

- Drive DeVilbiss Healthcare (US)

- Foshan Keyhub Electronic Industries Co. Ltd. (Guangdong)

- GCE Group (Sweden)

- Inogen, Inc. (US)

- Inova Labs, Inc.

- Invacare Corporation (US)

- Koninklijke Philips N.V (Netherlands)

- Nidek Medical (India)

- O2 CONCEPTS LLC., (US)

- Oxus America, Inc. (Oxus)

- Philips Respironics (US)

- Precision Medical, Inc. (US)

- ResMed (US)

- Smith’s Medical, Inc. (US)

- Zadro Health Solutions (US)

Recent Development

- In August 2023, Foshan Keyhub Electronic Industries Co. Ltd. announced in August 2023, an expansion of its manufacturing operations with an additional $2 million investment to meet the growing global demand for portable oxygen concentrators. This expansion is expected to increase their production capacity by 20%.

- In July 2023, Chart Industries, Inc. celebrated the production of its 100,000th portable oxygen concentrator, a milestone that underscores the company’s commitment to providing advanced respiratory care solutions. The company also announced a $5 million investment plan to expand its production facilities in Georgia.

- In May 2023, Besco Medical Co., LTD, a leading provider of medical mobility and respiratory devices, introduced a new lightweight portable oxygen concentrator. This product aims to enhance mobility for patients requiring oxygen therapy, marking a significant enhancement in their product lineup.

Report Scope

Report Features Description Market Value (2023) USD 1.8 Billion Forecast Revenue (2033) USD 3.9 Billion CAGR (2024-2032) 8.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type(Portable, Fixed), By Technology(Continuous Flow, Pulse Flow), By Indication(Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep Apnea, Others), By Application(Homecare, Travel, Hospital, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Besco Medical Co., LTD (China), CAIRE Inc. (US), Chart Industries, Inc. (US), Drive DeVilbiss Healthcare (US), Foshan Keyhub Electronic Industries Co. Ltd. (Guangdong), GCE Group (Sweden), Inogen, Inc. (US), Inova Labs, Inc., Invacare Corporation (US), Koninklijke Philips N.V (Netherlands), Nidek Medical (India), O2 CONCEPTS LLC., (US), Oxus America, Inc. (Oxus), Philips Respironics (US), Precision Medical, Inc. (US), ResMed (US), Smith’s Medical, Inc. (US), Zadro Health Solutions (US) Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Besco Medical Co., LTD (China)

- CAIRE Inc. (US)

- Chart Industries, Inc. (US)

- Drive DeVilbiss Healthcare (US)

- Foshan Keyhub Electronic Industries Co. Ltd. (Guangdong)

- GCE Group (Sweden)

- Inogen, Inc. (US)

- Inova Labs, Inc.

- Invacare Corporation (US)

- Koninklijke Philips N.V (Netherlands)

- Nidek Medical (India)

- O2 CONCEPTS LLC., (US)

- Oxus America, Inc. (Oxus)

- Philips Respironics (US)

- Precision Medical, Inc. (US)

- ResMed (US)

- Smith’s Medical, Inc. (US)

- Zadro Health Solutions (US)

Our Clients

View Our Licence Options