Polycarbonate Sheet Market By Type (Solid, Multiwall, Corrugated, Others), By End-Use Industry (Building & Construction, Electrical & Electronics, Automotive & Transportation, Aerospace & Defense, Packaging, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

9365

-

August 2024

-

231

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

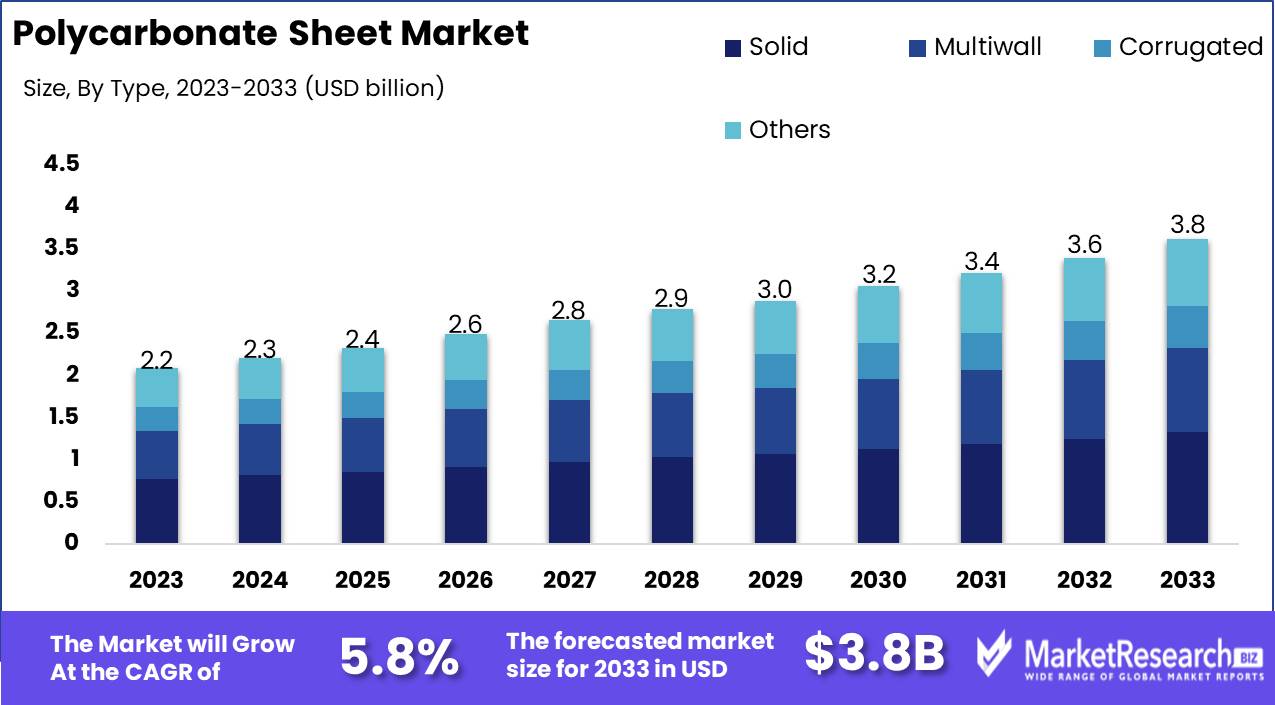

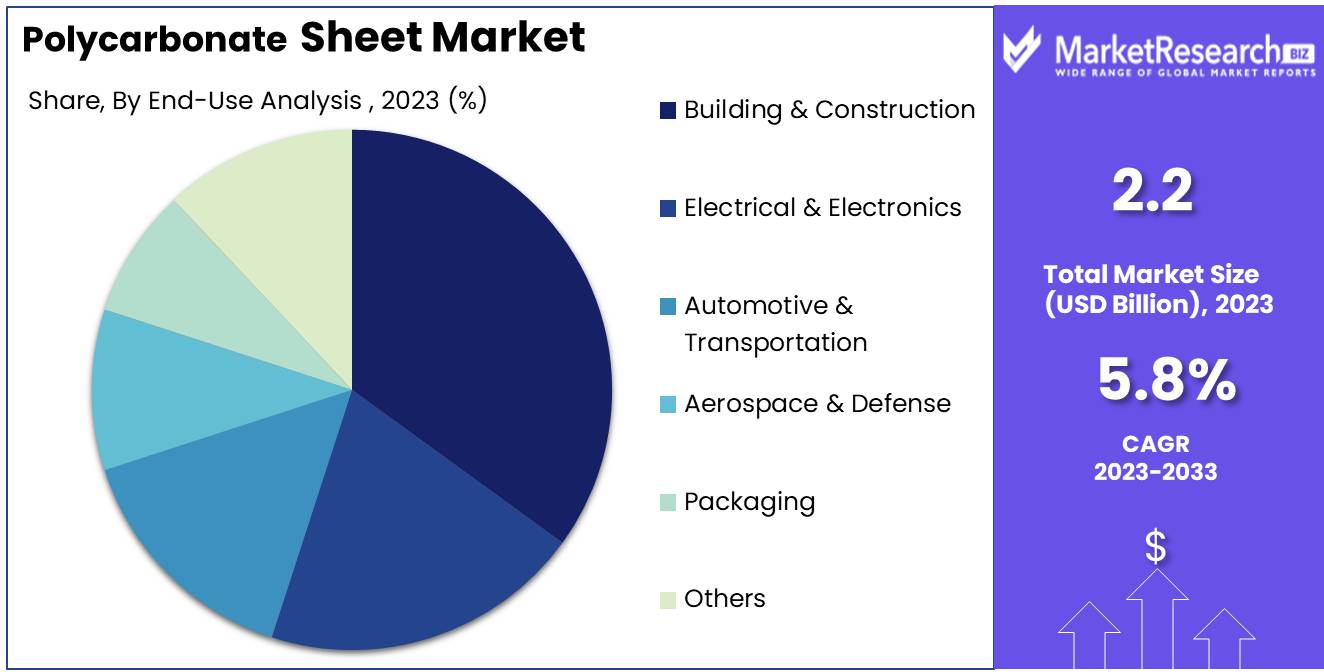

The Polycarbonate Sheet Market was valued at USD 2.2 billion in 2023. It is expected to reach USD 3.8 billion by 2033, with a CAGR of 5.8% during the forecast period from 2024 to 2033.

The polycarbonate sheet market encompasses the production and distribution of durable, high-performance thermoplastic sheets used across various industries. Polycarbonate sheets are known for their exceptional impact resistance, optical clarity, and thermal insulation properties. These attributes make them ideal for applications in construction, automotive, and electronics, among others. The market's growth is driven by increasing demand for lightweight, shatter-resistant materials in architectural glazing, signage, and protective barriers.

The polycarbonate sheet market is poised for substantial growth, driven primarily by increasing demand in the construction sector and the expansion of the automotive industry. The construction sector's escalating need for lightweight, durable, and energy-efficient materials has significantly bolstered the consumption of polycarbonate sheets, which are favored for their impact resistance and thermal insulation properties. Concurrently, the automotive industry's rapid advancement in technology and design has heightened the demand for polycarbonate sheets, particularly in applications such as automotive glazing and interior components, where strength and clarity are crucial.

However, the market faces challenges, notably the high cost of raw materials, which impacts overall profitability and pricing structures. Despite these challenges, the polycarbonate sheet market is expected to exhibit positive long-term growth. The ongoing innovations in material science and production technologies are anticipated to mitigate some cost pressures and enhance product performance, supporting sustained market expansion. Analysts foresee that the sector will continue to benefit from technological advancements and evolving industry demands, positioning it favorably for future growth. The combination of robust demand drivers and continuous improvements in material efficiencies underscores the market’s promising outlook in the coming years.

Key Takeaways

- Market Growth: The Polycarbonate Sheet Market was valued at USD 2.2 billion in 2023. It is expected to reach USD 3.8 billion by 2033, with a CAGR of 5.8% during the forecast period from 2024 to 2033.

- By Type: Solid polycarbonate sheets led the market with robustness.

- By End-Use Industry: Building & Construction led the Polycarbonate Sheet Market's growth.

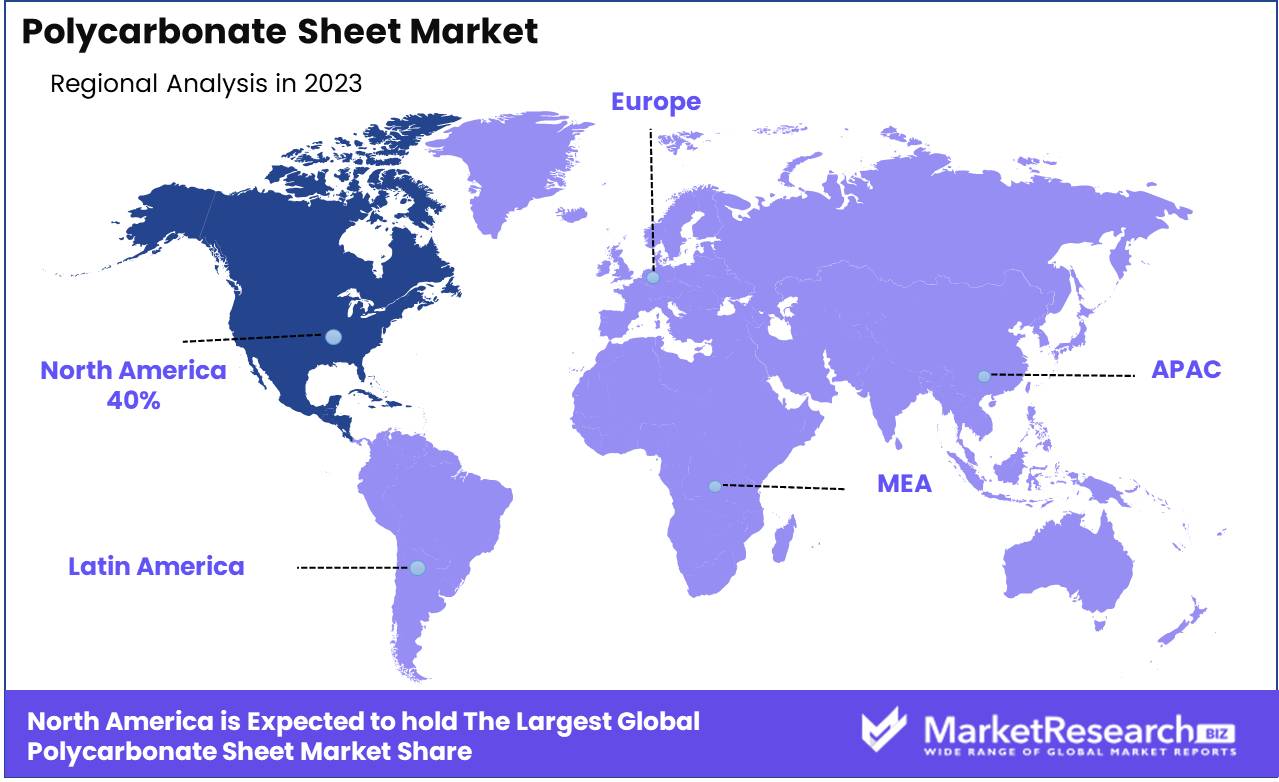

- Regional Dominance: North America dominates with a 40% largest market share, driven by growth.

- Growth Opportunity: The global polycarbonate sheet market is set to benefit from increased demand in both the building and construction industry and the automotive sector.

Driving factors

Robust Growth Driven by Increasing Demand from the Construction Industry

The construction industry has witnessed significant growth, driven by rapid urbanization and infrastructure development across various regions. Polycarbonate sheets, known for their durability, impact resistance, and lightweight properties, are increasingly favored in the construction sector for applications such as roofing, cladding, and glazing. These sheets provide excellent insulation, light transmission, and UV protection, making them an ideal choice for modern building designs.

The rise in sustainable construction practices also contributes to the demand, as polycarbonate sheets are recyclable and contribute to energy efficiency in buildings. According to recent market analysis, the construction sector's contribution to the polycarbonate sheet market is expected to grow at a compound annual growth rate (CAGR) of 6.5% over the next five years, underscoring its critical role in driving market expansion.

Automotive Industry Growth Fueling Demand for Polycarbonate Sheets

The automotive industry is experiencing robust growth, driven by increasing vehicle production and consumer demand for lightweight and fuel-efficient vehicles. Polycarbonate sheets are extensively used in the automotive sector for manufacturing components such as headlamp lenses, sunroofs, and interior panels due to their high impact resistance, clarity, and thermal stability.

The trend towards electric vehicles (EVs) further amplifies the demand, as manufacturers seek materials that contribute to overall weight reduction and energy efficiency. Market reports indicate that the automotive sector's demand for polycarbonate sheets is projected to increase at a CAGR of 7.2%, highlighting the significant impact of automotive industry growth on the polycarbonate sheet market.

Technological Advancements Enhancing Polycarbonate Sheet Applications

Technological advancements in the production and processing of polycarbonate sheets are pivotal in expanding their applications and improving product performance. Innovations such as multi-wall polycarbonate sheets, which offer superior insulation properties, and the development of UV-protected sheets extend the usability and lifespan of polycarbonate products. Advances in extrusion and coating technologies have led to the production of sheets with enhanced surface hardness, scratch resistance, and anti-fogging properties, broadening their application scope across various industries.

The integration of nanotechnology in polycarbonate sheet manufacturing has also resulted in improved material properties, such as increased strength and thermal stability. These technological strides not only enhance product quality but also drive market growth by opening new avenues for application and increasing consumer confidence in polycarbonate solutions. The market is expected to see a 6.8% CAGR attributed to these technological innovations.

Restraining Factors

Environmental Impact of Polycarbonate Sheets

The environmental impact of polycarbonate sheets poses a significant restraint on market growth. Polycarbonate sheets are derived from petrochemical sources, which involve energy-intensive processes and contribute to greenhouse gas emissions. Additionally, these sheets are not biodegradable, leading to concerns about their disposal and long-term environmental effects. The accumulation of polycarbonate waste can lead to environmental pollution, prompting regulatory bodies to impose stricter environmental standards and guidelines.

In response to growing environmental concerns, many companies are investing in research and development to create more eco-friendly alternatives or improve the recycling processes for polycarbonate sheets. Despite these efforts, the environmental drawbacks remain a substantial barrier to market growth, as consumers and industries increasingly prioritize sustainability and eco-friendliness in their material choices. This shift towards greener alternatives can limit the demand for polycarbonate sheets and challenge market expansion.

Availability of Alternative Materials

The availability of alternative materials is another critical factor affecting the growth of the polycarbonate sheet market. A range of alternative materials, such as acrylic sheets, fiberglass, and glass, offer comparable or superior properties to polycarbonate sheets in terms of durability, clarity, and resistance to environmental factors. These alternatives often present advantages like enhanced recyclability, lower environmental impact, and cost-effectiveness.

For example, acrylic sheets are known for their high impact resistance and optical clarity, often being preferred in applications requiring superior transparency. Fiberglass is valued for its durability and resistance to extreme environmental conditions. As the market for these alternatives grows, driven by technological advancements and increasing consumer awareness, the demand for polycarbonate sheets may face pressure.

By Type Analysis

In 2023, Solid polycarbonate sheets led the market with robustness.

In 2023, The Solid segment held a dominant market position in the Polycarbonate Sheet Market. Solid polycarbonate sheets are widely recognized for their robustness, clarity, and excellent impact resistance, making them a preferred choice in various applications including construction, automotive, and signage. This segment benefits from its superior mechanical properties and versatility, which cater to high-demand sectors requiring durable and transparent materials.

Multiwall polycarbonate sheets also represent a significant portion of the market, valued for their thermal insulation properties and lightweight nature. They are often used in greenhouse panels, skylights, and roofing due to their energy efficiency and structural strength.

Corrugated polycarbonate sheets, while less dominant than solid and multiwall types, are valued for their rigidity and cost-effectiveness. They are commonly used in industrial and agricultural settings where structural support and resistance to environmental elements are critical.

The Others segment, which includes specialized and custom polycarbonate sheets, completes the market with niche applications and unique requirements, although it holds a smaller share compared to the primary types.

By End-Use Industry Analysis

In 2023, Building & Construction led the Polycarbonate Sheet Market's growth.

In 2023, The Building & Construction sector held a dominant market position in the Polycarbonate Sheet Market. This segment's significant share is attributed to the growing demand for durable, lightweight, and high-performance materials in construction applications. Polycarbonate sheets are widely used in architectural glazing, skylights, roofing, and facades due to their excellent impact resistance, thermal insulation properties, and UV protection. The increasing emphasis on energy-efficient and sustainable building practices has further driven the adoption of polycarbonate sheets in construction projects, enhancing their market prominence.

The Electrical & Electronics segment also played a substantial role, owing to the material's superior electrical insulation properties and versatility. Polycarbonate sheets are utilized in the production of electronic housings, circuit board covers, and protective panels, meeting the industry’s demand for high-performance and durable components.

The Automotive & Transportation sector leveraged polycarbonate sheets for their lightweight and shatter-resistant qualities, which contribute to vehicle safety and fuel efficiency. In Aerospace & Defense, the material’s high impact resistance and clarity made it ideal for aircraft windows and protective covers.

In the Packaging sector, polycarbonate sheets are used for their transparency and strength, making them suitable for high-quality packaging solutions. The “Others” segment includes diverse applications, reflecting the material’s broad versatility across various industries.

Key Market Segments

By Type

- Solid

- Multiwall

- Corrugated

- Others

By End-Use Industry

- Building & Construction

- Electrical & Electronics

- Automotive & Transportation

- Aerospace & Defense

- Packaging

- Others

Growth Opportunity

Building and Construction Demand

The global polycarbonate sheet market is poised for substantial growth in 2024, driven significantly by the escalating demand in the building and construction sector. Polycarbonate sheets, known for their durability, impact resistance, and light transmission properties, are increasingly favored for various applications including roofing, facades, and skylights. The trend towards energy-efficient and sustainable building materials aligns with the characteristics of polycarbonate sheets, which offer excellent thermal insulation and UV resistance. As urbanization continues and the construction of green buildings accelerates, the demand for polycarbonate sheets is expected to rise, providing ample growth opportunities for market players.

Automotive Industry Applications

Another key growth driver for the polycarbonate sheet market is the expanding use of these materials in the automotive industry. Polycarbonate sheets are gaining traction in automotive applications due to their lightweight nature, which contributes to fuel efficiency and reduced emissions. They are increasingly used in automotive glazing, lighting, and interior components, offering enhanced design flexibility and improved safety features. The shift towards electric and hybrid vehicles, which prioritize weight reduction and performance efficiency, further supports the growing adoption of polycarbonate sheets in this sector. As automotive manufacturers continue to innovate and seek materials that balance performance with sustainability, polycarbonate sheets are well-positioned to meet these evolving requirements.

Latest Trends

Rising Demand in Electrical & Electronics Industry

The polycarbonate sheet market is experiencing notable growth driven by increased demand from the electrical and electronics sectors. Polycarbonate sheets are favored in this industry due to their excellent electrical insulation properties, high impact resistance, and durability. As electronic devices become more advanced, the need for protective enclosures, insulation components, and durable housings is expanding. Polycarbonate sheets, with their lightweight and transparent qualities, are increasingly used in the manufacturing of electrical enclosures and circuit board covers, contributing to their growing market share. This trend is further supported by advancements in electronics technology, which require higher standards of protection and functionality, thus fueling the demand for polycarbonate materials.

Expanding Use in the Aerospace & Defense Sector

Another significant trend is the expanding use of polycarbonate sheets within the aerospace and defense sector. Polycarbonate sheets are valued in this sector for their high strength-to-weight ratio, clarity, and resistance to impact and extreme temperatures. These properties make them ideal for applications such as aircraft windows, cockpit enclosures, and ballistic shields. As the aerospace industry continues to focus on improving fuel efficiency and performance, the lightweight nature of polycarbonate sheets presents a strategic advantage.

Moreover, the defense sector’s need for robust and reliable materials to ensure safety and durability in harsh conditions further drives the adoption of polycarbonate sheets. This growing trend underscores the material’s versatility and its increasing role in critical applications.

Regional Analysis

North America dominates with a 40% largest market share, driven by growth.

North America holds a dominant position in the global polycarbonate sheet market, primarily driven by robust industrial growth, high demand for durable and lightweight materials, and significant investments in infrastructure and construction projects. In 2023, North America accounted for approximately 40% of the global market share, reflecting its strong market presence. The United States, in particular, remains a key contributor due to its advanced manufacturing capabilities and growing use of polycarbonate sheets in automotive, electronics, and building applications.

Europe is another significant market, characterized by stringent regulatory standards and a strong emphasis on environmental sustainability. The region represents about 30% of the global market, with notable growth in the construction and automotive sectors. Countries such as Germany and France lead in the adoption of polycarbonate sheets for their energy-efficient properties.

Asia Pacific is experiencing rapid market expansion, driven by industrialization, urbanization, and increasing construction activities. This region is projected to exhibit the highest growth rate, contributing around 25% to the global market, with China and India as key growth drivers.

Middle East & Africa and Latin America also contribute to the market, though at a smaller scale, with regional growth driven by emerging infrastructure projects and increasing industrial applications.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global polycarbonate sheet market is characterized by a competitive landscape with several key players demonstrating strong market presence and technological innovation.

Sabic continues to be a major force in the market, leveraging its extensive expertise in polycarbonate materials to drive innovation and enhance product offerings. Its focus on high-performance applications and sustainable solutions solidifies its position as a market leader.

Covestro AG maintains its competitive edge through continuous research and development efforts, particularly in improving the durability and optical clarity of polycarbonate sheets. The company’s emphasis on sustainability aligns with the growing demand for eco-friendly materials. Trinseo S.A. stands out with its diverse product portfolio and strategic focus on expanding its polycarbonate sheet applications, catering to various end-use industries such as automotive and construction.

Teijin Limited and Mitsubishi Gas Chemical Company, Inc. are also pivotal players, known for their advanced material technologies and strong regional presence. Their investments in enhancing polycarbonate sheet properties ensure they remain key contributors to market growth. Evonik Industries AG and Suzhou Omay Optical Materials Co., Ltd. focus on specialty applications and innovative solutions, while Plazit-Polygal Group and Arla Plast Ab strengthen their market positions through high-quality products and efficient manufacturing processes.

3A Composite, Uvplastic Material Technology Co., Ltd., Jiaxing Innovo Industries Co., Ltd., Polyvalley Technology Co., Ltd., Emco Industrial Plastics, Spolytech, and MG Polyplast Industries Pvt. Ltd adds to the market's dynamism with its regional and technological contributions, addressing specific industry needs and regional demands.

Overall, these companies drive the polycarbonate sheet market forward through innovation, sustainability, and strategic expansion, each contributing to the sector's growth and development.

Market Key Players

- Sabic

- Covestro AG

- Trinseo S.A.

- Teijin Limited

- Mitsubishi Gas Chemical Company, Inc.

- Evonik Industries AG

- Suzhou Omay Optical Materials Co., Ltd.

- Plazit-Polygal Group

- Arla Plast Ab

- 3A Composite

- Uvplastic Material Technology Co., Ltd

- Jiaxing Innovo Industries Co., Ltd

- Polyvalley Technology Co., Ltd

- Emco Industrial Plastics

- Spolytech

- MG Polyplast Industries Pvt. Ltd

Recent Development

- In March 2024, Covestro announced the launch of a new line of polycarbonate sheets with enhanced UV resistance and increased durability. This innovation is aimed at expanding their market share in the construction and automotive sectors, where high-performance materials are increasingly in demand.

- In February 2024, Teijin Limited unveiled a partnership with a leading solar panel manufacturer to develop advanced polycarbonate sheets designed for solar panel applications. This collaboration aims to enhance the efficiency and lifespan of solar panels, capitalizing on the growing renewable energy market.

- In January 2024, Sabic introduced a new recycling program for polycarbonate sheets as part of their sustainability initiative. The program focuses on collecting and recycling used polycarbonate sheets to produce new ones, significantly reducing environmental impact and aligning with global sustainability goals.

Report Scope

Report Features Description Market Value (2023) USD 2.2 Billion Forecast Revenue (2033) USD 3.8 Billion CAGR (2024-2032) 5.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Solid, Multiwall, Corrugated, Others), By End-Use Industry (Building & Construction, Electrical & Electronics, Automotive & Transportation, Aerospace & Defense, Packaging, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Sabic, Covestro AG, Trinseo S.A., Teijin Limited, Mitsubishi Gas Chemical Company, Inc., Evonik Industries AG, Suzhou Omay Optical Materials Co., Ltd., Plazit-Polygal Group, Arla Plast Ab, 3A Composite, Uvplastic Material Technology Co., Ltd, Jiaxing Innovo Industries Co., Ltd, Polyvalley Technology Co., Ltd, Emco Industrial Plastics, Spolytech, MG Polyplast Industries Pvt. Ltd Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Sabic

- Covestro AG

- Trinseo S.A.

- Teijin Limited

- Mitsubishi Gas Chemical Company, Inc.

- Evonik Industries AG

- Suzhou Omay Optical Materials Co., Ltd.

- Plazit-Polygal Group

- Arla Plast Ab

- 3A Composite

- Uvplastic Material Technology Co., Ltd

- Jiaxing Innovo Industries Co., Ltd

- Polyvalley Technology Co., Ltd

- Emco Industrial Plastics

- Spolytech

- MG Polyplast Industries Pvt. Ltd

Our Clients

View Our Licence Options