Point-of-Care CT Imaging Market By Treatment (Compact CT scanners, Full-sized CT scanners), By Application (Neurology, Musculoskeletal, Respiratory, ENT, Others) By End-Use (Hospitals, Ambulatory Surgery Centers, Clinics, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

17120

-

May 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

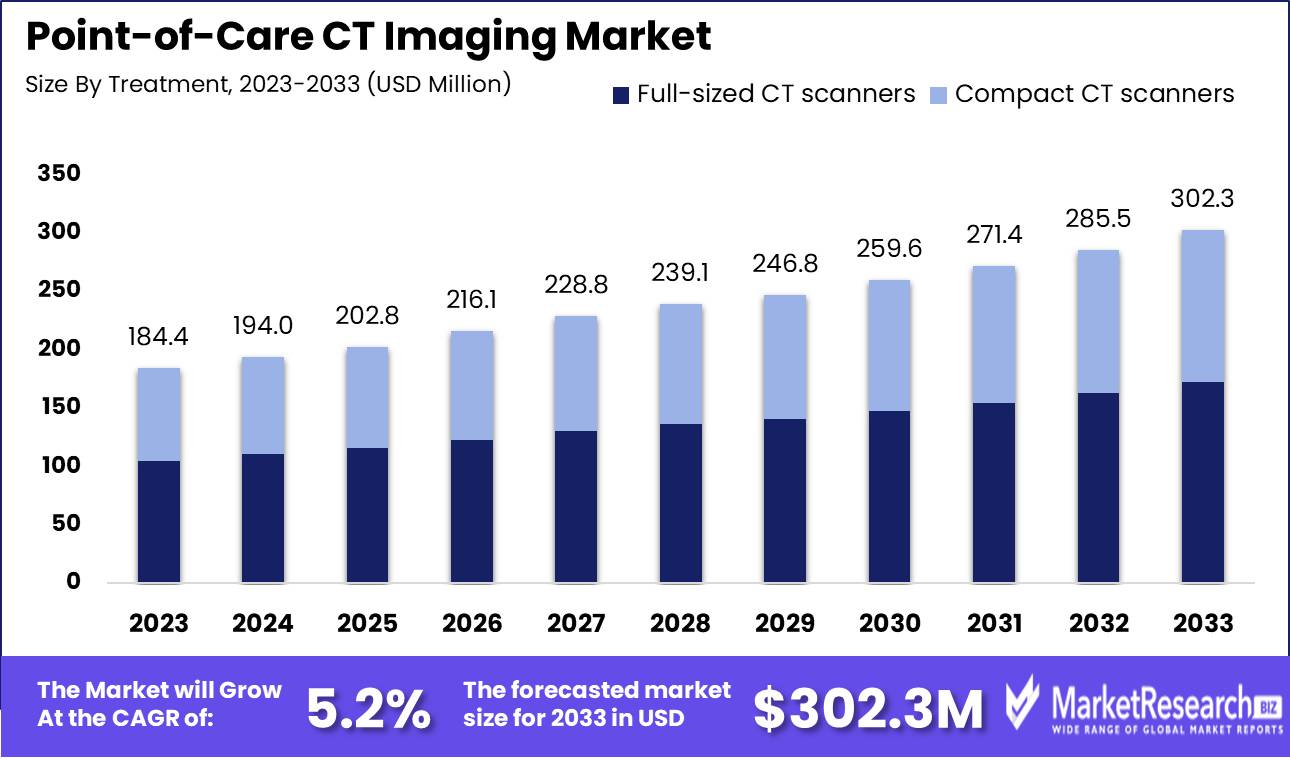

The Point-of-Care CT Imaging Market size is estimated at USD 184.4 Million in 2023 and is expected to reach USD 302.3 Million by 2033, growing at a CAGR of 5.2% during the forecast period 2024-2033.

The Point-of-Care CT Imaging Market encompasses advanced diagnostic technologies designed for immediate, bedside imaging. This market focuses on portable CT scanners that enable rapid diagnosis and treatment in diverse healthcare settings, including emergency departments, intensive care units, and operating rooms. Key drivers include the growing demand for timely and accurate diagnostics, advancements in imaging technology, and increasing applications in trauma and critical care. Market growth is further propelled by the need for enhanced patient outcomes and streamlined workflows.

The Point-of-Care CT Imaging Market is poised for significant growth, driven by the increasing demand for rapid and accurate diagnostic capabilities in critical care environments. As healthcare systems worldwide emphasize improved patient outcomes and operational efficiency, the adoption of portable CT imaging solutions is expanding. These devices offer the advantage of real-time imaging at the bedside, facilitating immediate clinical decisions and reducing the need for patient transfers. The market is further bolstered by advancements in imaging technology, including higher resolution capabilities and enhanced portability, making these devices indispensable in emergency departments, intensive care units, and operating rooms.

Supporting this growth trajectory, the broader medical imaging market is projected to reach USD 60 billion by 2033, with a compound annual growth rate (CAGR) of 5.4%. This robust expansion reflects the increasing investment in innovative imaging technologies and the integration of artificial intelligence (AI) and machine learning to enhance diagnostic accuracy and efficiency. Additionally, emerging markets such as India exhibit substantial growth potential. The Indian diagnostics market, valued at $10 billion in FY2021, is expected to double to $20 billion by FY26, growing at a compounded annual growth rate (CAGR) of 14%. This rapid growth underscores the expanding healthcare infrastructure and the rising demand for advanced diagnostic solutions. As the Point-of-Care CT Imaging Market evolves, it stands to benefit significantly from these broader trends, driving innovation and adoption across diverse healthcare settings.

Key Takeaways

- Market Growth: The Point-of-Care CT Imaging Market size is estimated at USD 184.4 Million in 2023 and is expected to reach USD 302.3 Million by 2033, growing at a CAGR of 5.2% during the forecast period 2024-2033.

- By Treatment: Full-sized CT scanners lead due to superior imaging; compact ones excel in portability.

- By Application: Neurology leads the Point-of-Care CT Imaging Market; diverse applications drive growth.

- By End-Use: In 2023, Hospitals dominated the Point-of-care CT imaging market by end-use.

- Regional Dominance: North America leads the Point-of-Care CT Imaging market with a 40% share.

- Growth Opportunity: The global PoC CT imaging market is set for growth due to AI integration and rising demand.

Driving factors

Increasing Demand for Point-of-Care CT Imaging Systems: Meeting the Needs of a Dynamic Healthcare Environment

The point-of-care CT imaging market is experiencing robust growth driven primarily by the escalating demand for immediate and accessible diagnostic solutions. This demand stems from the evolving landscape of healthcare, where rapid diagnosis and treatment initiation are critical for improving patient outcomes. Point-of-care (POC) CT systems offer significant advantages over traditional imaging modalities by providing real-time imaging at the patient's bedside, reducing the need for patient transportation to radiology departments.

Recent studies indicate that the adoption of POC CT imaging systems in emergency departments and intensive care units has led to a 20-30% reduction in patient transfer times, thereby expediting clinical decision-making processes and enhancing overall patient throughput.

Technological Advancements: Revolutionizing Point-of-Care CT Imaging with Cutting-Edge Innovations

Technological advancements are at the forefront of the growth observed in the point-of-care CT imaging market. Innovations in imaging technology have resulted in the development of compact, portable CT scanners that deliver high-resolution images comparable to those produced by conventional systems. These advancements include enhancements in detector technology, software algorithms for image reconstruction, and the integration of artificial intelligence (AI) for automated image analysis.

The incorporation of AI and machine learning into POC CT systems has revolutionized diagnostic accuracy and efficiency. AI-driven tools can quickly identify and highlight abnormalities, aiding clinicians in making more precise diagnoses. This is particularly beneficial in acute settings, such as stroke management, where timely intervention is critical.

Cost-Effectiveness and Efficiency: Delivering Value in Healthcare Delivery

The cost-effectiveness and operational efficiency of point-of-care CT imaging systems are significant factors contributing to their growing adoption. Traditional CT scanners require substantial capital investment, dedicated space, and specialized personnel. In contrast, POC CT systems are designed to be more affordable, with lower initial costs and reduced operational expenses, making them an attractive option for smaller healthcare facilities and outpatient settings.

The efficiency gains associated with POC CT imaging are equally compelling. By providing immediate diagnostic capabilities at the point of care, these systems minimize the need for patient transport, streamline workflows, and reduce the overall time to diagnosis and treatment. Studies have shown that the use of POC CT imaging can decrease the length of hospital stays by up to 15%, translating to significant cost savings for healthcare providers.

Restraining Factors

Regulatory Challenges: Impeding Market Expansion

Regulatory challenges significantly constrain the growth of the point-of-care CT imaging market. Regulatory bodies, such as the FDA in the United States and the EMA in Europe, impose stringent requirements on medical device approval processes. These regulations ensure patient safety and device efficacy but often result in prolonged approval timelines and increased manufacturer costs. Compliance with these regulations necessitates substantial investment in clinical trials and extensive documentation, which can be particularly burdensome for smaller companies and startups. This regulatory bottleneck delays the introduction of new products to the market, stifling innovation and limiting the overall segment growth potential of the industry.

Preference for Alternative Diagnostic Methods: A Competitive Hurdle

The preference for alternative diagnostic methods presents a formidable challenge to the growth of the point-of-care CT imaging market. Conventional imaging techniques such as MRI (Magnetic Resonance Imaging) and ultrasound are well-established in the clinical setting. They are often preferred due to their non-invasive nature and broader diagnostic capabilities. MRI, for instance, offers superior soft tissue contrast without exposure to ionizing radiation, making it a safer option for certain patient groups. Ultrasound, on the other hand, is widely used for its real-time imaging capabilities, portability, and lower cost.

Moreover, advancements in these alternative technologies continue to enhance their diagnostic precision and usability, further solidifying their position in the diagnostic landscape. For example, recent improvements in MRI technology have reduced scan times and increased image resolution, making it more competitive against CT imaging. Similarly, the development of portable ultrasound devices has expanded the segment scope of point-of-care diagnostics, encroaching on the market share of CT imaging devices.

By Treatment Analysis

Full-sized Poc CT scanners lead due to superior imaging; compact ones excel in portability.

In 2023, Full-sized CT scanners held a dominant market position in the "By Treatment" segment of the Point-of-Care CT Imaging Market. This supremacy is attributed to their advanced imaging capabilities, which ensure high diagnostic accuracy crucial for complex medical conditions. Full-sized CT scanners are preferred in settings requiring detailed imaging, such as hospitals and specialized clinics, where comprehensive diagnostic information is paramount.

Conversely, compact CT scanners, while growing in popularity, serve niche applications primarily due to their portability and ease of use in emergency or remote settings. These scanners offer rapid imaging solutions with adequate quality, making them ideal for urgent care scenarios and locations with limited space or infrastructure. The rise in demand for on-the-go diagnostic solutions has bolstered the adoption of compact CT scanners, yet their market share remains secondary to full-sized counterparts due to the latter's superior imaging resolution and versatility across a wider range of clinical applications.

By Application Analysis

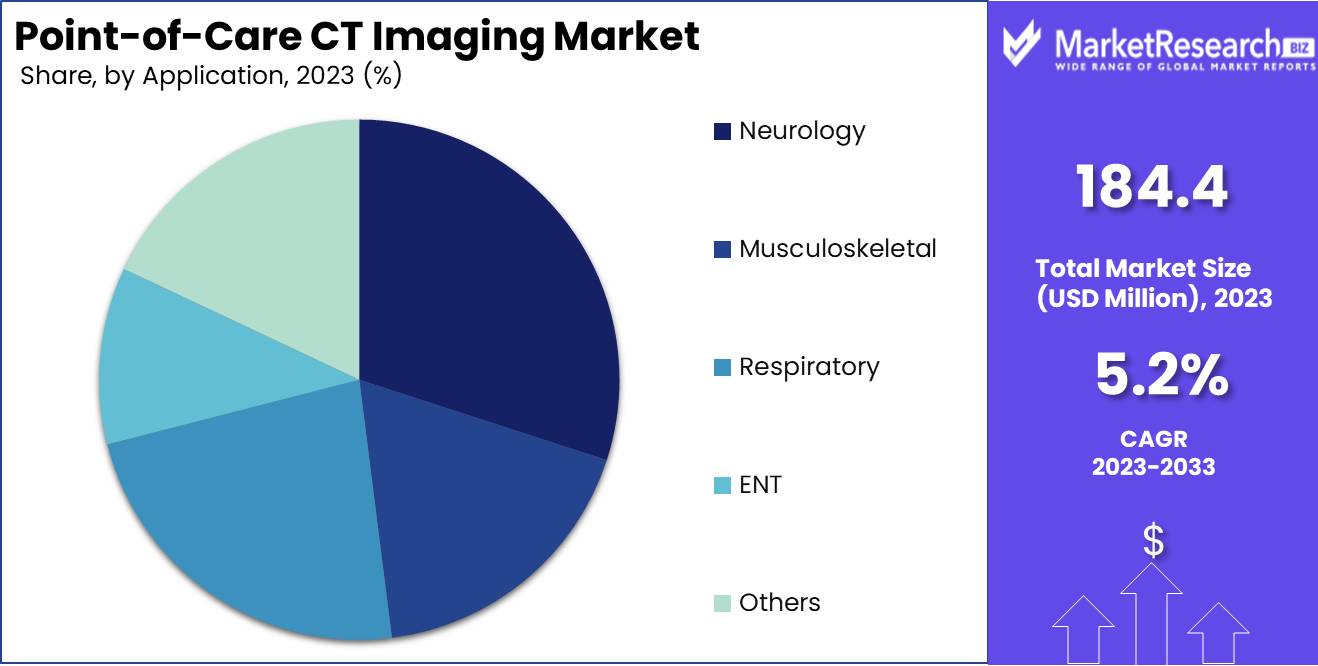

Neurology leads the Point-of-Care CT Imaging Market; diverse applications drive growth.

In 2023, Neurology held a dominant market position in the "By Application" segment of the Point-of-Care CT Imaging Market. This predominance can be attributed to the rising incidence of neurological disorders such as stroke, traumatic brain injuries, and neurodegenerative diseases, necessitating swift and accurate diagnostic tools. Neurology's leading share was bolstered by advancements in imaging technology, which have improved the detection and management of these conditions.

The musculoskeletal segment also demonstrated significant growth, driven by the increasing prevalence of sports injuries and orthopedic conditions that require precise imaging for diagnosis and treatment planning. The respiratory segment's expansion was propelled by the growing burden of chronic respiratory diseases like COPD and asthma, where point-of-care CT imaging aids in timely intervention and management.

ENT applications saw a surge due to the rising demand for accurate diagnosis of sinusitis, head and neck tumors, and other otolaryngological conditions. Finally, the "Others" category, encompassing various miscellaneous applications, continued to contribute to the market, supported by the versatility and expanding utility of point-of-care CT imaging across different medical specialties. Collectively, these segments underscore the diverse and critical role of point-of-care CT imaging in modern healthcare.

By End-Use Analysis

In 2023, Hospitals dominated the point-of-care CT imaging market by end-use.

In 2023, Hospitals held a dominant market position in the end-use segment of the Point-of-Care CT Imaging Market. This dominance can be attributed to several key factors. Hospitals are equipped with comprehensive diagnostic and treatment facilities, allowing them to fully leverage the advanced capabilities of point-of-care CT imaging technology. Their high patient volume ensures a steady demand for imaging services, making the integration of such systems both feasible and economically viable.

Ambulatory surgery centers (ASCs) also represent a significant segment. These centers benefit from the portability and rapid imaging capabilities of point-of-care CT systems, which enhance patient outcomes by providing immediate postoperative imaging and reducing the need for patient transfers to hospitals. Clinics, while smaller in scale, utilize point-of-care CT imaging to improve diagnostic accuracy and speed, particularly in outpatient settings. This facilitates more efficient patient management and enhances care delivery.

The "others" category includes specialized diagnostic centers and mobile imaging units, which utilize these systems to provide advanced imaging services in remote or underserved areas, thus broadening access to high-quality diagnostic imaging.

Key Market Segments

By Treatment

- Compact CT scanners

- Full-sized CT scanners

By Application

- Neurology

- Musculoskeletal

- Respiratory

- ENT

- Others

By End-Use

- Hospitals

- Ambulatory Surgery Centers

- Clinics

- Others

Growth Opportunity

Increasing Demand for Accessible and Efficient Medical Imaging Technologies

The global Point-of-Care (PoC) CT imaging market is poised for significant growth driven by the escalating demand for accessible and efficient medical imaging technologies. Healthcare systems worldwide are under increasing pressure to provide timely and accurate diagnoses, particularly in emergency and critical care settings. PoC CT imaging systems, known for their portability and rapid imaging capabilities, address these needs effectively. They facilitate immediate diagnosis and intervention, reducing the time between patient admission and treatment. This efficiency is critical in enhancing patient outcomes, particularly in stroke management, trauma cases, and intensive care units.

Incorporation of Artificial Intelligence

The integration of artificial intelligence (AI) into PoC CT imaging systems represents a transformative opportunity for market growth. AI algorithms enhance imaging precision, automate the detection of anomalies, and improve image quality, thereby increasing diagnostic accuracy. In 2024, we anticipate a significant uptick in AI-driven innovations within this market. AI's capability to analyze large datasets and identify patterns that may be imperceptible to the human eye augments the diagnostic process, enabling more personalized and effective treatment plans. Furthermore, AI integration can streamline workflow processes, reducing the burden on radiologists and improving operational efficiencies in healthcare facilities.

Latest Trends

Portable and Point-of-Care CT Scanners: Transforming Accessibility and Patient Care

The emergence of portable and point-of-care CT scanners is revolutionizing the CT imaging market in 2024. These devices are designed to provide immediate imaging capabilities at the patient's bedside or in remote locations, significantly enhancing accessibility. By minimizing the need for patient transport to imaging centers, these scanners reduce logistical challenges and associated costs. This trend is particularly beneficial for critical care, emergency rooms, and field applications, where rapid diagnosis can be life-saving.

The market is witnessing increased adoption due to technological advancements that ensure high-quality imaging comparable to traditional CT systems. Consequently, healthcare providers are better equipped to deliver timely, effective care, improving patient outcomes and operational efficiency.

Workflow Efficiency: Enhancing Operational Performance and Patient Throughput

In 2024, workflow efficiency remains a critical focus in the point-of-care CT imaging market. As healthcare providers seek to optimize operations amidst rising patient volumes and constrained resources, innovations in CT imaging workflows are paramount. Advanced software solutions, including AI-driven image processing and automated reporting, are streamlining the diagnostic process. These technologies reduce the time required for image acquisition, interpretation, and documentation, thereby accelerating patient throughput.

Moreover, integrated systems that seamlessly connect CT scanners with electronic health records (EHRs) are enhancing data management and accessibility. This integration facilitates quicker decision-making and improves coordination among healthcare professionals. By prioritizing workflow efficiency, the point-of-care CT imaging market is addressing the dual objectives of enhancing care quality and operational effectiveness.

Regional Analysis

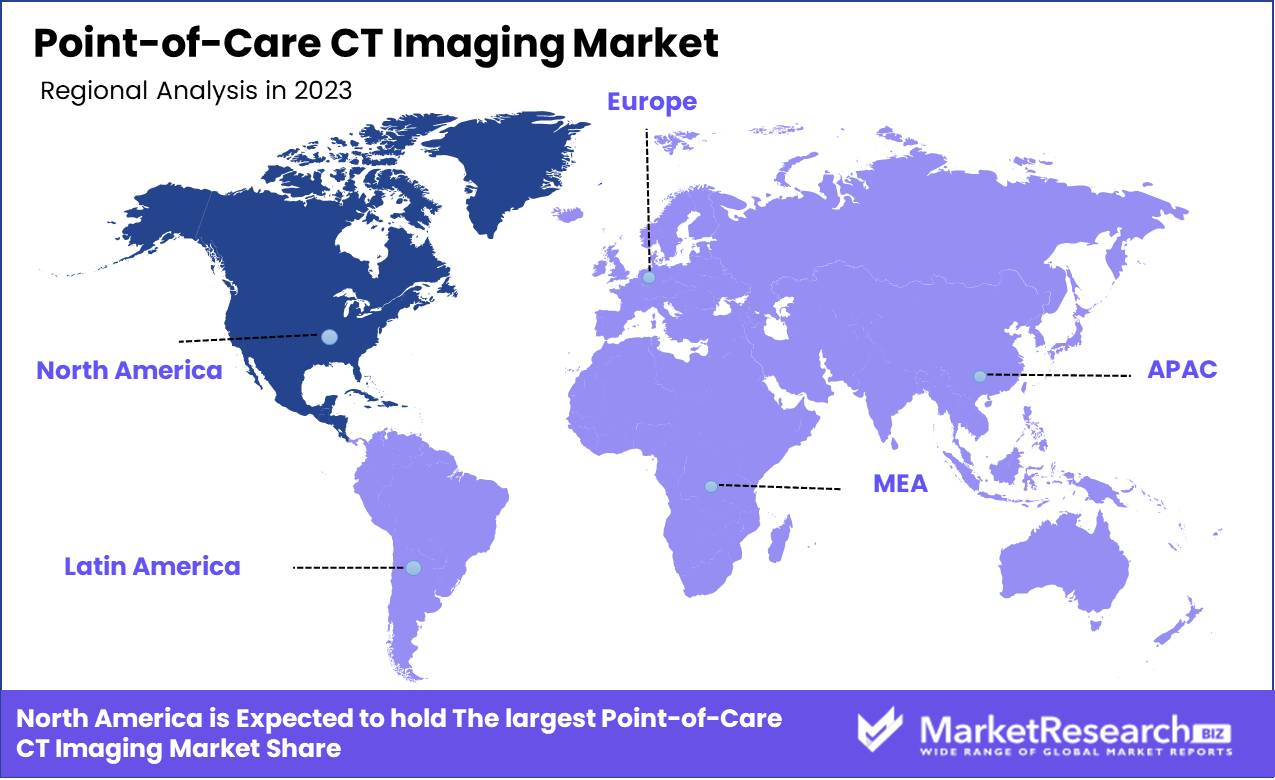

North America leads the Point-of-Care CT Imaging market with a 40% share.

The Point-of-Care CT Imaging market is witnessing significant growth across various regions, driven by technological advancements and increasing healthcare demands. North America dominates this market, accounting for approximately 40% of the global share, attributed to robust healthcare infrastructure, high adoption rates of advanced medical technologies, and supportive government initiatives. Europe follows closely, driven by increasing healthcare expenditures and the presence of key market players in countries like Germany, France, and the UK.

The Asia Pacific region is experiencing rapid growth, with a projected CAGR of over 8%, fueled by rising healthcare investments, expanding medical tourism in countries such as India and Thailand, and increasing awareness of advanced diagnostic techniques. The Middle East & Africa region, though currently less developed, is seeing steady growth due to improving healthcare facilities and rising incidences of chronic diseases. Latin America is also showing positive market trends, particularly in Brazil and Mexico, due to growing healthcare infrastructure and increased government spending on healthcare. North America's leadership in the market is underscored by its significant share, advanced healthcare system, and continuous innovation in medical imaging technologies.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Point-of-Care (POC) CT Imaging market is experiencing significant growth, driven by technological advancements and increasing demand for rapid diagnostic solutions. Key players in this market include industry giants and innovative companies that shape the competitive landscape.

Philips Healthcare and Siemens Healthcare GmbH are at the forefront, leveraging their extensive R&D capabilities and broad product portfolios. These companies focus on integrating AI and machine learning into POC CT systems, enhancing diagnostic accuracy and operational efficiency. GE Healthcare continues to innovate with its advanced imaging solutions, prioritizing user-friendly interfaces and compact designs to facilitate ease of use in diverse healthcare settings. Their commitment to continuous improvement and strong global presence solidifies their market position.

Samsung Medison and Mindray are expanding their market share through strategic investments in emerging markets and robust product offerings that combine high performance with cost efficiency. These companies capitalize on their expertise in ultrasound technology to enhance CT imaging solutions. FUJIFILM SonoSite, Inc. and Neurologica, a subsidiary of Samsung Electronics, emphasize portability and versatility in their POC CT imaging products, catering to the growing need for mobile healthcare services.

Esaote and Canon Medical Systems Corp. leverage their strong imaging advanced technology backgrounds to provide comprehensive solutions that address diverse clinical needs. Their focus on patient-centric innovations is a key differentiator. Xoran Technologies LLC specializes in compact, point-of-care CT systems that are particularly suited for ENT and dental applications, highlighting the niche opportunities within the market.

Market Key Players

- Philips Healthcare

- Siemens Healthcare GmbH

- GE Healthcare

- Samsung Medison

- Mindray

- FUJIFILM SonoSite, Inc.

- Neurologica

- Esaote

- Canon Medical Systems Corp.

- Xoran Technologies LLC

Recent Development

- In February 2024, Visage Imaging launched the Visage Ease VP, an imaging platform compatible with Apple's augmented reality headset. This innovation aims to improve the efficiency and accuracy of radiological analyses by allowing radiologists to interact with diagnostic images in an augmented reality environment.

- In February 2023, At the IRIA National Conference, FUJIFILM India announced the expansion of its healthcare imaging product range, introducing advanced diagnostic tools including MRI and ultrasound systems (Growth Plus Reports).

- In November 2022, GE HealthCare partnered with Sinopharm of China to develop and market non-premium CT and general imaging ultrasound solutions, aiming to improve medical equipment access in rural China (Growth Plus Reports).

Report Scope

Report Features Description Market Value (2023) USD 184.4 Million Forecast Revenue (2033) USD 302.3 Million CAGR (2024-2032) 5.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Treatment (Compact CT scanners, Full-sized CT scanners), By Application (Neurology, Musculoskeletal, Respiratory, ENT, Others) By End-Use (Hospitals, Ambulatory Surgery Centers, Clinics, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Philips Healthcare, Siemens Healthcare GmbH, GE Healthcare, Samsung Medison, Mindray, FUJIFILM SonoSite, Inc., Neurologica, Esaote, Canon Medical Systems Corp., Xoran Technologies, LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Philips Healthcare

- Siemens Healthcare GmbH

- GE Healthcare

- Samsung Medison

- Mindray

- FUJIFILM SonoSite, Inc.

- Neurologica

- Esaote

- Canon Medical Systems Corp.

- Xoran Technologies, LLC

Our Clients

View Our Licence Options