Over-the-Top (OTT) Market By OTT Services(Managed Services, Online Services), By Type(OTT Media services, OTT Communication services, OTT Applications services), By Platform(Smartphones, Smart TVs, Laptops Desktops and Tablets, Others), By Component(Solution, Services), By Deployment Type(Cloud, On-Premise) By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

42816

-

Jan 2022

-

156

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Over-the-Top (OTT) Market Size, Share, Trends Analysis

- Driving Factors

- Restraining Factors

- Over-the-Top (OTT) Market Segmentation Analysis

- Industry Segments

- Growth Opportunities

- Over-the-Top (OTT) Market Regional Analysis

- Over-the-Top (OTT) Industry by Region

- Over-the-Top (OTT) Market Key Player Analysis

- Over-the-Top (OTT) Industry Key Players

- Over-the-Top (OTT) Market Recent Development

- Report Scope

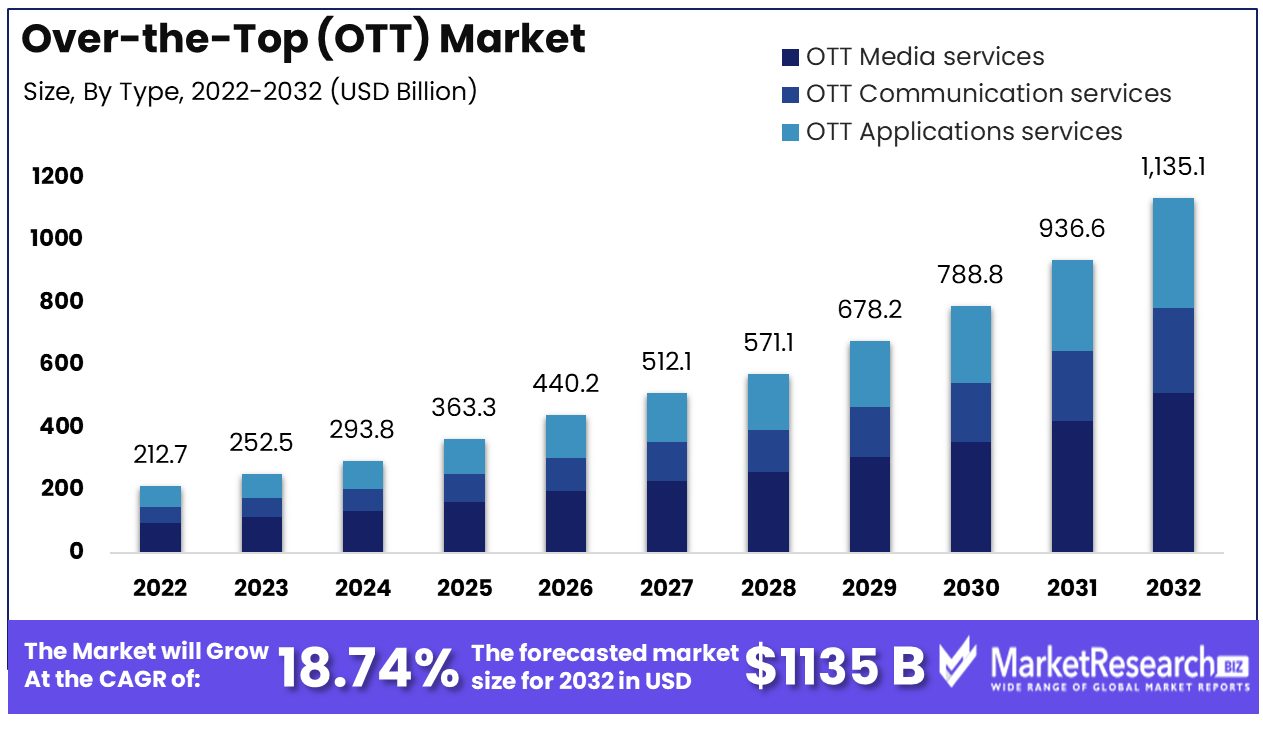

The Over-the-Top (OTT) Market was valued at USD 212.69 billion in 2022. It is expected to reach USD 1135.1 billion by 2032, with a CAGR of 18.74% during the forecast period from 2023 to 2032.

The surge in demand for online content subscriptions and change in customer preference are some of the main driving factors for the over-the-top market growth. Over the top (OTT) is the content providers that supply streaming media as a single product directly to the audiences over the internet through telecommunications and broadcast televisions, the providers traditionally act as an intermediate between the content producers and consumers. The word “over” depicts the supply over the top of these old middlemen. It has become one of the most vital elements of the television and video industry.

OTTs signify the delivery of video and TV content via the internet, without needing audiences to subscribe to the old and traditional cable or satellite pay-tv services such as Sky, Virgin Media, and many more.

According to Nielsen in April 2022, viewers are spending more than 30% of their total television time watching over-the-top video content. Likewise, according to a campaign India article in Dec 2022, India has crossed up to 43 crore OTT viewers, out of which 11.9 crore are paid subscribers. 65% of the paid subscribers are male audiences.

While the main six metros account for only 10% of the total OTT audiences, these numbers surged to 33% when it comes to paid subscriptions. As per Ormax OTT audience report in 2022, around 23% of the older viewers are continuing to stream content which is a change from their old, traditional satellite TV to the OTT content.

One of the main reasons for the rise of OTT platforms is the consumer’s preferences. Earlier consumers were limited to traditional satellite TV which has restrained content but as OTT has arrived in the television market, consumers now have a lot of choices for the content.

There are several OTT platforms like Netflix, Amazon Prime, Hotstar, Hulu, and many others that are spending ample amounts of money on producing new and original content that can draw more consumer attention. The cost of generating high-quality original content will surge and it will become more difficult for traditional TV networks to compete in the market. This demand will increase in the coming years by expanding the over-the-top market growth.

Driving Factors

Media and Entertainment Demand Catalyzes OTT Growth

The escalating demand for diverse and accessible media and entertainment is a primary driver of the Over-the-Top (OTT) Market's expansion. With the increasing appetite for on-demand content, ranging from movies and TV shows to podcasts and live streaming, OTT platforms are experiencing a surge in consumer engagement. This trend reflects the shift in audience preferences towards digital, convenient, and personalized media consumption. As this demand continues to grow, the OTT market is expected to expand correspondingly, adapting to and capitalizing on evolving consumer entertainment consumption habits.

Smart Devices Penetration Enhances OTT Accessibility

The widespread adoption of smart devices, such as smartphones, tablets, and smart TVs, is significantly driving the growth of the OTT market. These devices provide the primary means for accessing OTT services, facilitating easy and anytime access to a wide range of digital content. The growing penetration of these devices, especially in regions with improving internet connectivity, is broadening the audience base for OTT services, making them more mainstream. This increasing accessibility is likely to continue propelling the market growth, with OTT services becoming an integral part of daily media consumption.

Subscription Services Demand Boosts OTT Market

Consumers are increasingly favoring the subscription model for its cost-effectiveness, the convenience of uninterrupted viewing, and access to extensive content libraries. This model has proven successful for major OTT players, attracting a steady revenue stream while providing users with diverse and quality content. The trend towards subscription services indicates a sustainable growth trajectory for the OTT market, with more consumers adopting this model for their entertainment needs.

Emerging Markets Offer New Opportunities for OTT

The extension of OTT services into emerging markets represents a significant growth opportunity for the industry. As internet penetration improves and disposable incomes rise in these regions, more consumers are gaining access to OTT platforms. This expansion into new geographical areas is not only increasing the subscriber base but also encouraging the diversification of content to cater to varied regional tastes and preferences. The growth in these markets suggests a vast potential for OTT services, with emerging economies becoming key contributors to the global OTT market's expansion.

Restraining Factors

High Costs of OTT Platforms May Impede Market Expansion

Over-the-top (OTT) market growth may be significantly hindered by the high costs associated with various platforms that operate over-the-top services. As the market becomes more saturated with numerous services, each requiring its subscription fee, consumers may experience subscription fatigue.

This can lead to hesitancy in adopting new OTT services, particularly in price-sensitive markets. The cumulative expense of maintaining multiple subscriptions can be substantial, prompting users to limit the number of services they subscribe to or revert to more cost-effective alternatives. Consequently, the high cost of OTT platforms could restrict their broader market expansion and consumer adoption.

Intense Competition from Traditional Broadcasting and Cable Industries

Intense competition from traditional broadcasting and cable industries also presents a challenge to the adoption of OTT services. Despite the shift towards digital streaming, traditional television, and cable services remain significant players in the market, especially in regions with established infrastructure and customer bases.

These traditional mediums often offer bundled packages and exclusive content, which can be appealing to certain audiences. Moreover, in areas with limited internet access or bandwidth constraints, traditional broadcasting remains a more reliable source of entertainment. This competition can slow down the shift towards OTT services, as consumers weigh the benefits and drawbacks of transitioning from traditional television to streaming platforms.

Over-the-Top (OTT) Market Segmentation Analysis

Online Services

OTT media services encompassing the streaming of videos, audio files, and digital media content are currently the dominant force in the OTT market. This segment's ascendancy is anchored in the seismic shift in consumer preferences towards on-demand, personalized content. Factors fueling its growth include the proliferation of high-speed internet, advancements in streaming technologies, and the increasing production of diverse, high-quality content. The competitive landscape is characterized by intense rivalry among key players, leading to continuous innovation and strategic partnerships.

This segment includes messaging, voice, and video call services offered over the Internet. Despite being overshadowed by media services, OTT communication holds a substantial market share, driven by the ubiquity of smartphones and the global shift towards remote work and digital communication. Its growth reflects an evolving communication paradigm, with potential for further expansion as technology integrates more seamlessly into daily life.

OTT application services, encompassing various cloud-based applications and platforms, represent a growing segment. These services are gaining traction due to their flexibility, scalability, and cost-effectiveness. This segment is poised for growth, especially in the business domain, as organizations increasingly adopt digital transformation strategies.

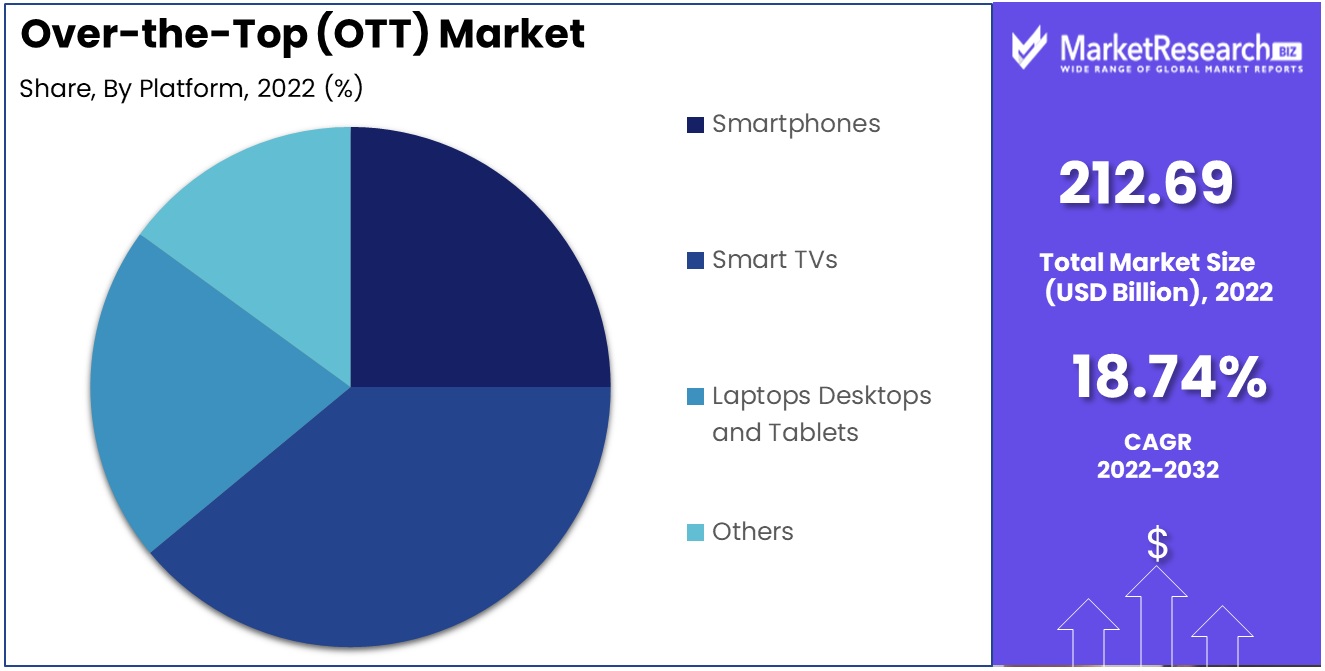

By Platform

Smartphones are the dominant platform for OTT services, primarily due to their pervasive use and portability. The integration of advanced features, high-speed internet connectivity, and a growing ecosystem of apps have made smartphones the primary access point for OTT content. This segment's growth is propelled by continuous technological advancements in smartphone capabilities and the increasing affordability of devices in emerging markets.

Smart TVs are gaining prominence in the OTT market, offering a more immersive viewing experience. The integration of OTT apps directly into TV sets and the growing consumer preference for larger, high-definition screens for streaming content are significant growth drivers.

This segment, though less dominant than smartphones, remains significant for OTT services, especially for longer viewing sessions and professional communication. The versatility of these devices in supporting diverse content formats and their widespread use in professional and academic settings underpin their steady market presence. Other platforms such as gaming consoles and streaming devices also contribute to the OTT market. While their market share is smaller, they offer niche opportunities and enhance the overall ecosystem.

By Component

The solution segment, comprising the core technology and software that enable OTT services, holds a dominant position. This segment's growth is underpinned by continuous technological advancements, the need for robust content management systems, and effective content delivery networks. The focus on enhancing user experience, personalization, and integrating advanced features like AI and machine learning for content recommendation and analytics are key drivers.

Services related to the deployment, maintenance, and optimization of OTT solutions constitute a critical but less dominant segment. This includes professional services like consulting, integration, and support. As the OTT market matures, the role of these services becomes increasingly important, especially in maintaining service quality and customer satisfaction.

By Deployment Type

Cloud deployment is the leading approach in the OTT market, offering scalability, flexibility, and cost-efficiency. The segment's growth is driven by the increasing adoption of cloud-based solutions across industries, enabling OTT providers to rapidly scale their services and content delivery. The proliferation of cloud computing technologies and the expansion of global cloud infrastructure are fundamental to this segment's dominance.

On-premise deployment, while less prevalent in the current OTT landscape, is relevant for specific applications where control over infrastructure and data security are paramount. This segment caters to organizations with specific regulatory or operational requirements.

Industry Segments

By OTT Services

- Managed Services

- Online Services

By Type

- OTT Media services

- OTT Communication services

- OTT Applications services

By Platform

- Smartphones

- Smart TVs

- Laptops Desktops and Tablets

- Others

By Component

- Solution

- Services

By Deployment Type

- Cloud

- On-Premise

By Content Type

- Voice Over IP

- Text and Images

- Video

- Others

By Revenue Model

- Subscription

- Procurement

- Rental

- Others

By Vertical

- Media & Entertainment

- Education & Training

- Health & Fitness

- IT & Telecom

- E-Commerce

- BFSI

- Government

- Others

Growth Opportunities

Increasing Demand for Video Streaming Services Bolsters Growth in OTT Market

The escalating demand for video streaming services is a key driver of growth in the Over-the-Top (OTT) market. Consumers are increasingly favoring OTT platforms for their diverse content offerings, convenience, and personalized viewing experiences. The trend towards cord-cutting and the preference for on-demand content over traditional broadcast television are fueling this demand. The proliferation of original content, along with the expansion of international and niche genres, is attracting a wider audience to these platforms. This growing consumer preference for streaming services reflects a substantial market expansion opportunity, as OTT platforms continue to reshape the entertainment and media landscape.

Over-the-Top (OTT) Market Regional Analysis

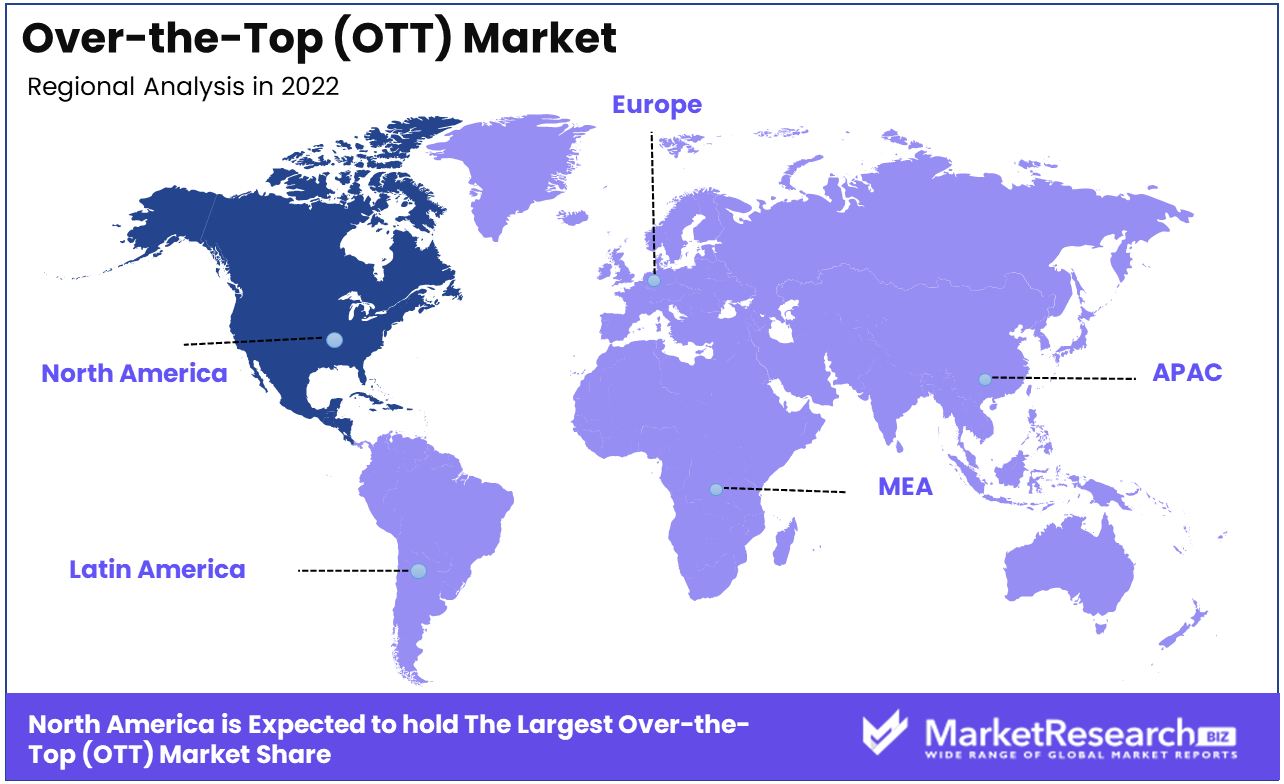

North America Dominates with 46.20% Market Share in Over-the-Top (OTT) Market

North America holds an estimated 46.20% share in the Over-the-Top (OTT) Market, driven mainly by high internet penetration rates, widespread usage of smartphones and smart devices, and major service providers providing these products in this region. The United States and Canada have a strong culture of digital content consumption, which includes streaming movies, TV shows, and other media content. Additionally, the high disposable incomes in these countries enable consumers to spend more on entertainment services, thereby fueling the OTT market.

The market dynamics in North America are influenced by the increasing demand for diverse and high-quality content, leading to significant investments in original content creation by OTT platforms. The growth in cord-cutting, where consumers prefer internet streaming services over traditional cable TV, further bolsters the OTT market. Competition within the region, marked by newcomers entering and existing companies expanding, is intensifying market dynamics. The integration of advanced technologies like AI for personalized content recommendations and 4K streaming capabilities also plays a crucial role.

Europe is a Growing Market with Diverse Content Preferences

Europe’s OTT market is growing, driven by the region's diverse content preferences and increasing adoption of digital streaming services. Market growth is further enabled by high-speed internet expansion and smart device penetration. European countries are also focusing on local content creation, catering to a wide range of linguistic and cultural audiences.

Asia-Pacific's Rapid Expansion with Rising Internet Penetration

In Asia-Pacific, the OTT market is experiencing rapid expansion, fueled by rising internet penetration and the proliferation of mobile devices. Countries like China, India, and Japan are witnessing a surge in digital content consumption. Asia-Pacific's rising middle class and increasing affordability of internet services have contributed to an explosive expansion in OTT markets. Consumer preferences for local content coupled with global players entering this space define the Asia-Pacific market landscape.

Over-the-Top (OTT) Industry by Region

North America

- The US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of the Middle East & Africa

Over-the-Top (OTT) Market Key Player Analysis

In the Over-the-Top (OTT) Market, a rapidly growing sector within digital entertainment and media, the companies listed are key players shaping the future of content consumption. Google LLC, Apple Inc., and Amazon.com, Inc. are market giants offering diverse OTT services, including video streaming and cloud-based solutions. Their extensive ecosystems and technological capabilities have a significant impact on market trends and consumer preferences.

AT&T Intellectual Property and Comcast, with their strong foothold in telecommunications and media, have expanded into OTT services, leveraging their existing customer base and content libraries. Hulu, LLC, a joint venture involving major media companies, stands out for its unique content offerings and original productions, contributing to the diversity and competitiveness of the market.

STAR (India) and BT (U.K.) represent significant regional players, catering to specific demographic and cultural preferences, reflecting the market's global diversity. Twitter, Inc., and Facebook, primarily social media platforms, have ventured into the OTT space, capitalizing on their massive user bases and integrating video content into their services.

Over-the-Top (OTT) Industry Key Players

- Google LLC

- Apple Inc.

- Amazon.com, Inc.

- AT&T Intellectual Property.

- STAR

- Twitter, Inc.

- Hulu, LLC

- Comcast

- BT

- Cox Communications, Inc.

- Verizon Media

- TalkTalk TV Entertainment Limited

- Deutsche Telekom AG

- Akamai Technologies

- Fandango

- Snagfilms Inc.

- iNDIEFLIX Group Inc.

- Xperi

- Crackle, Inc.

- Brightcove Inc.

Over-the-Top (OTT) Market Recent Development

- In September 2023, the Department of Telecommunications (DoT) in India made a significant decision not to categorize OTT platforms and apps as telecommunications services in the forthcoming Telecom Bill.

- In 2023, Tata Elxsi continued to innovate in the OTT space with its TEPlay solution. TEPlay is a pre-integrated, highly scalable, and secure end-to-end OTT video delivery platform designed to offer exceptional video experiences.

- In December 2023, Google settled the class action lawsuit filed against it by US states and consumers. The company will pay $700 million, with $630 million going to consumers and $70 million to a fund for states. This settlement resolves allegations that Google had a monopoly over app distribution on Android through its Play Store.

- In July 2023, the Department of Social Development (DSD) announced its plans to launch its own OTT platform, named DSDTV. DSD's objective is to use this platform to provide social development and welfare services to the South African public, including child support, old age, and disability grants.

Report Scope

Report Features Description Market Value (2023) USD 212.69 Billion Forecast Revenue (2033) USD 1135.1 Billion CAGR (2024-2032) 18.74% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By OTT Services(Managed Services, Online Services), By Type(OTT Media services, OTT Communication services, OTT Applications services), By Platform(Smartphones, Smart TVs, Laptops Desktops and Tablets, Others), By Component(Solution, Services), By Deployment Type(Cloud, On-Premise), By Content Type(Voice Over IP, Text and Images, Video, Others), By Revenue Model(Subscription, Procurement, Rental, Others), By Vertical(Media & Entertainment, Education & Training, Health & Fitness, IT & Telecom, E-Commerce, BFSI, Government, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Google LLC (U.S.), Apple Inc. (U.S.), Amazon.com, Inc. (U.S.), AT&T Intellectual Property. (U.S.), STAR (India), Twitter, Inc. (U.S.), Hulu, LLC (U.S.), Comcast (U.S.), BT (U.K.), Cox Communications, Inc. (U.S.), Facebook (U.S.), Verizon Media (U.S.), TalkTalk TV Entertainment Limited (U.K.), Deutsche Telekom AG (Germany), Akamai Technologies (U.S.), Fandango (U.S.), Snagfilms Inc. (U.S.), iNDIEFLIX Group Inc. (U.S.), Xperi (U.S.), Crackle, Inc. (U.S.), Brightcove Inc. (U.S.) Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

Our Clients

View Our Licence Options