Open RAN Security Market By Component (Hardware, Software, Services), By Unit (Radio Unit, Distributed Unit, Centralized Unit), By Deployment (Private, Hybrid Cloud, Public Cloud), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51077

-

September 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

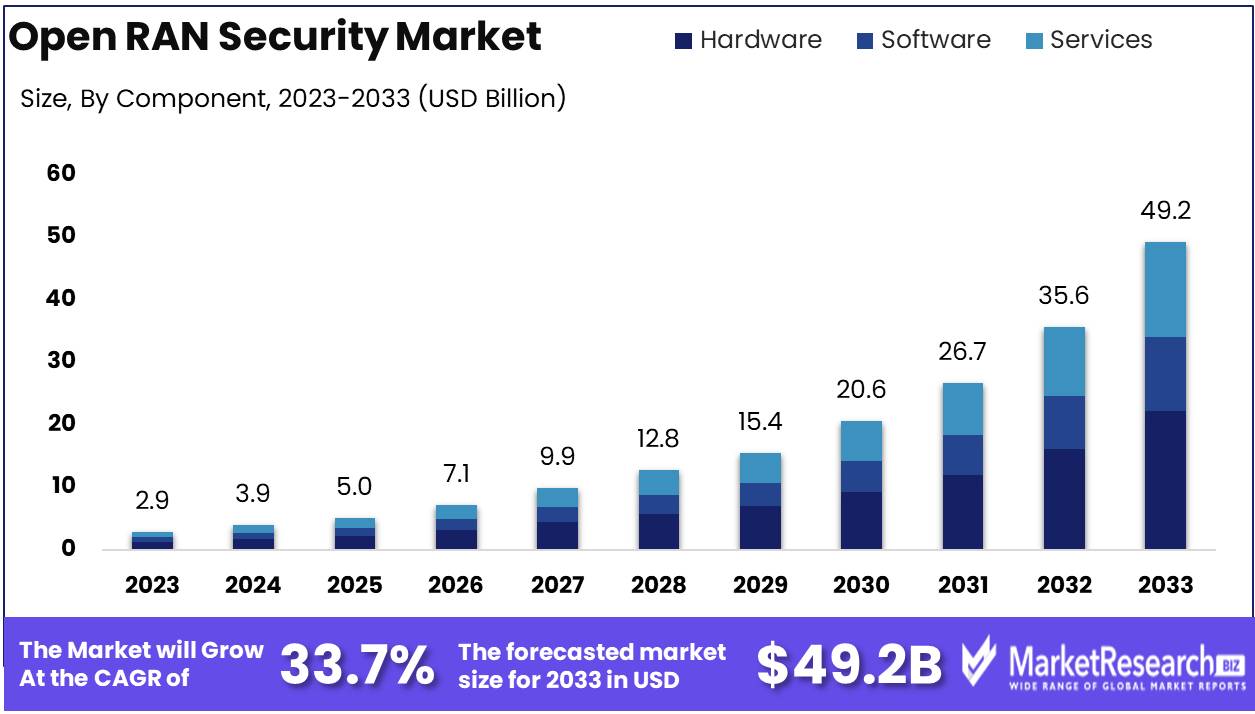

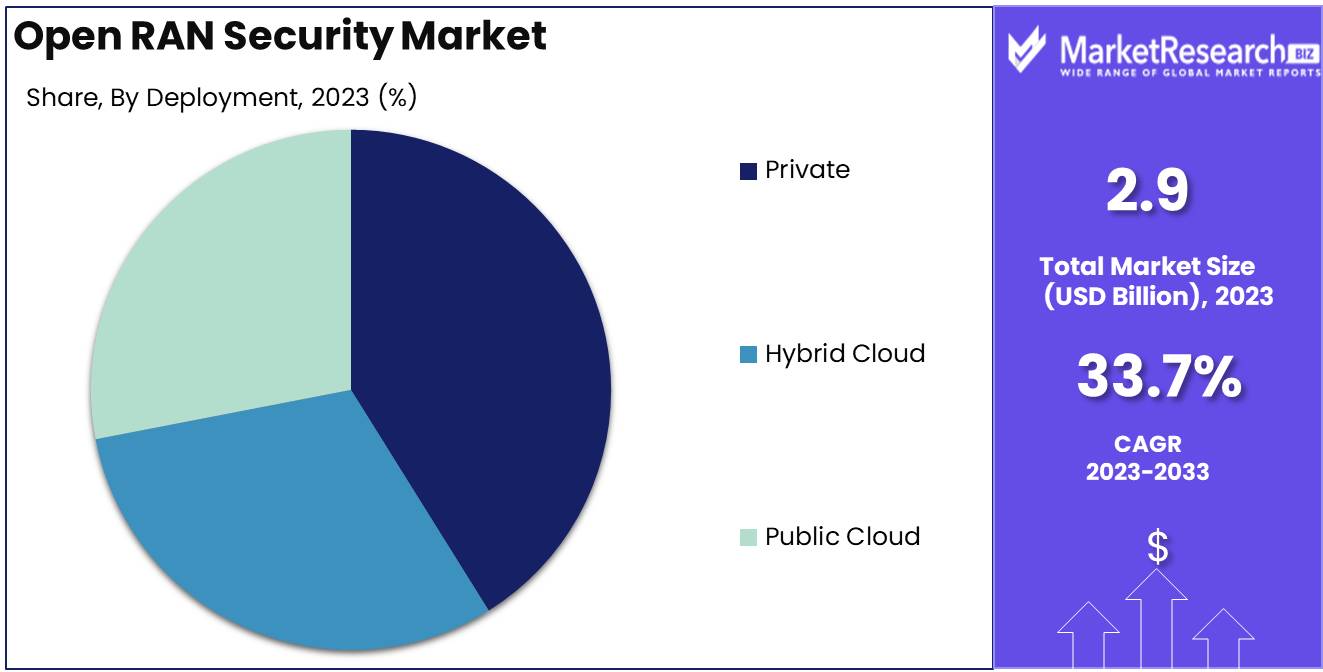

The Open RAN Security Market was valued at USD 2.9 billion in 2023. It is expected to reach USD 49.2 billion by 2033, with a CAGR of 33.7% during the forecast period from 2024 to 2033.

The Open RAN Security Market focuses on safeguarding the rapidly evolving Open Radio Access Network (RAN) architecture, which promotes interoperability and innovation in telecom networks. As Open RAN disaggregates traditional network components, security becomes crucial to protect against cyber threats and vulnerabilities. This market includes solutions designed to secure interfaces, ensure data privacy, and prevent unauthorized access across distributed network elements.

The Open RAN security market is poised for significant growth as the global rollout of 5G accelerates. The adoption of Open RAN architecture, while promising cost efficiencies and increased vendor diversity, introduces new complexities in security integration. This complexity is further amplified by the modular nature of Open RAN, where multiple vendors supply different components of the network. As 5G expands, this decentralized approach to network architecture inherently creates more points of vulnerability, elevating the need for robust security measures. However, the lack of standardization across Open RAN components remains a critical challenge, as inconsistent security protocols could compromise the integrity of the entire network.

The rapid evolution of technology in this space necessitates continuous adaptation to emerging threats, with security frameworks needing to keep pace with advancements in network capabilities. Regulatory bodies are also playing an increasingly pivotal role, as governments and international agencies develop stringent security standards to mitigate risks associated with Open RAN implementations.

Consequently, regulatory influence will likely shape the adoption and security strategies of operators and vendors alike. As the Open RAN security market matures, its growth will be closely tied to how effectively the industry addresses these challenges particularly in harmonizing security standards and integrating comprehensive, scalable solutions that safeguard next-generation network infrastructure.

Key Takeaways

- Market Growth: The Open RAN Security Market was valued at USD 2.9 billion in 2023. It is expected to reach USD 49.2 billion by 2033, with a CAGR of 33.7% during the forecast period from 2024 to 2033.

- By Component: Hardware dominated the Open RAN Security market components.

- By Unit: The Radio Unit dominated the Open RAN Security Market.

- By Deployment: Private cloud deployment dominated the Open RAN Security Market.

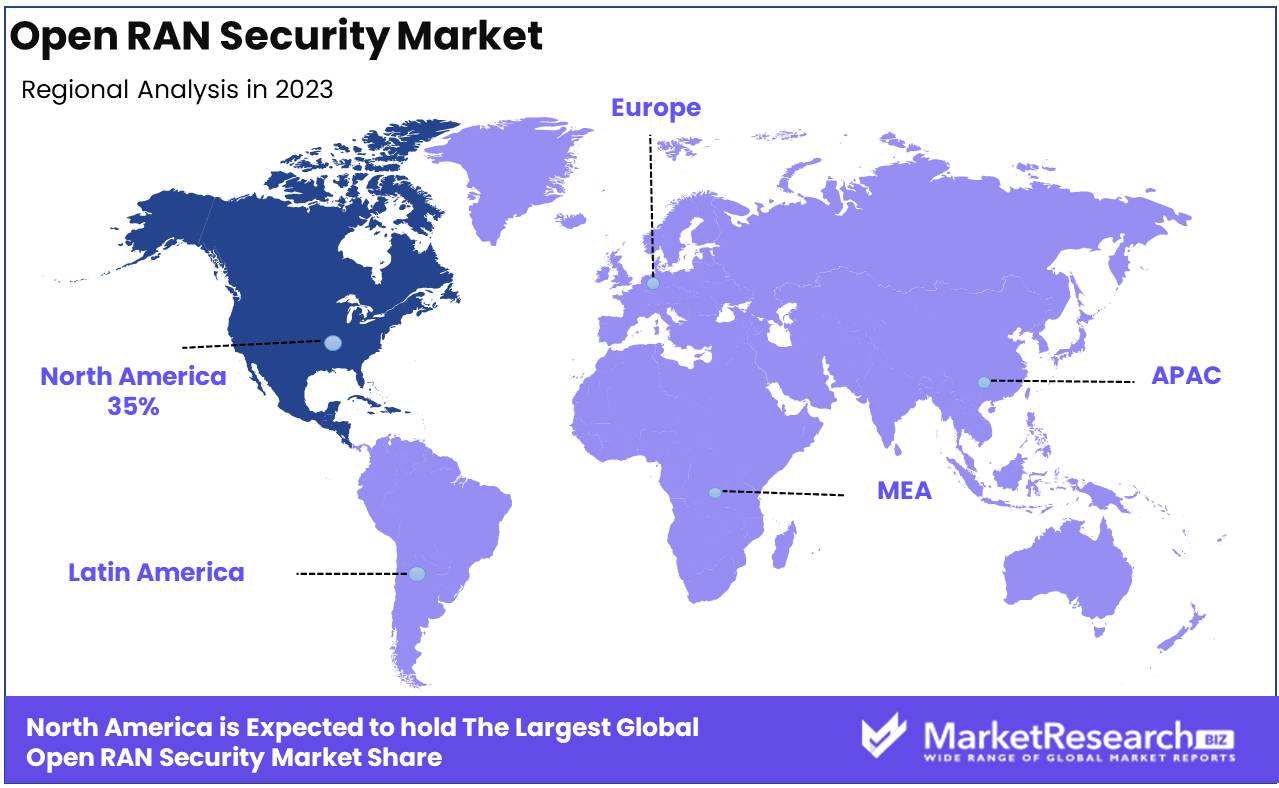

- Regional Dominance: North America dominates the Open RAN Security Market with a 35% largest share.

- Growth Opportunity: The global Open RAN security market will be driven by increasing network flexibility demands and 5G adoption, creating significant opportunities for cybersecurity providers to address emerging challenges.

Driving factors

Rise in Adoption of Multi-Vendor Deployment Approach Boosts Flexibility and Innovation

The increasing adoption of a multi-vendor deployment approach within the telecommunications sector is significantly contributing to the growth of the Open RAN security market. Open RAN architectures enable network operators to integrate hardware and software from different vendors, promoting innovation, reducing vendor lock-in, and enhancing overall network flexibility. This multi-vendor environment also brings challenges related to ensuring secure interoperability between components, which drives demand for enhanced security solutions tailored to Open RAN ecosystems.

A more diverse and modular vendor environment requires comprehensive security strategies to mitigate potential vulnerabilities that arise from integrating disparate systems. As operators prioritize secure and seamless interoperability, the market for Open RAN security is poised to expand, with significant investments being directed toward securing network interfaces, controlling access points, and monitoring data integrity across multi-vendor environments. This dynamic has resulted in a growing demand for robust security frameworks that can adapt to the evolving needs of these flexible and multi-source networks, propelling market growth.

Surge in Adoption of Enterprise Network Infrastructure Increases Security Needs

The widespread adoption of enterprise network infrastructure has created a favorable environment for the growth of the Open RAN security market. With enterprises increasingly relying on Open RAN to build private 5G networks and modernize their communication infrastructure, the security risks associated with these deployments have come into sharper focus. Enterprise networks, especially those in critical sectors such as healthcare, manufacturing, and financial services, require high levels of security to protect sensitive data, ensure operational continuity, and comply with industry regulations.

Open RAN's promise of cost efficiency and scalability is driving enterprises to adopt this architecture for their networks. However, these benefits come with a heightened need for advanced security solutions. The distributed nature of Open RAN deployments, which span multiple geographical locations and vendor systems, increases the complexity of network security. Consequently, organizations are investing heavily in security solutions designed to safeguard their Open RAN networks against cyberattacks, unauthorized access, and other threats. The demand for these advanced security measures has become a key driver of growth in the Open RAN security market as enterprises seek to protect their infrastructure from emerging vulnerabilities.

Rise in Government Initiatives for the Development of Open RAN Encourages Market Expansion

Government initiatives promoting the development and adoption of Open RAN technologies are playing a critical role in driving the growth of the Open RAN security market. Numerous governments, particularly in regions such as North America and Europe, have launched programs and provided financial support to accelerate the deployment of Open RAN as part of broader 5G development strategies. For instance, the U.S. and European Union have both committed significant funding towards Open RAN research and development, recognizing its potential to enhance network diversity and reduce reliance on a small number of dominant equipment suppliers.

These initiatives are not only advancing Open RAN adoption but also emphasizing the importance of security. As governments encourage the rollout of Open RAN networks, they are simultaneously placing strong emphasis on developing stringent security standards to protect national communication infrastructures from cyber threats. The growing focus on regulatory compliance and cybersecurity measures by governments is driving demand for security solutions tailored specifically for Open RAN deployments, further fueling the market’s expansion. In particular, government-funded projects often mandate the use of certified security solutions, providing a significant boost to the security segment within the Open RAN ecosystem.

Restraining Factors

High Integration Cost and Complexity: A Major Barrier to Widespread Adoption

One of the key restraining factors in the growth of the Open RAN Security Market is the high cost and complexity associated with integration. Open RAN systems rely on interoperability between multiple hardware and software components sourced from various vendors. Ensuring that these components work seamlessly together requires sophisticated integration processes, which are not only expensive but also technically challenging.

This complexity leads to extended deployment times, as additional resources must be allocated for testing, validation, and fine-tuning of the various Open RAN elements. Many telecom operators, particularly in emerging markets, may find the costs prohibitive and the level of expertise required a significant barrier to entry. This has slowed down the pace of Open RAN implementation, consequently impacting the security market for these systems.

The lack of standardization in Open RAN architecture further exacerbates the integration challenge. Different vendors may implement diverse protocols or features, increasing the risk of security vulnerabilities during the integration process. As a result, the market for Open RAN security solutions has been constrained by the slow adoption of Open RAN itself, limiting potential revenue growth.

Vendor Management Challenges: Increased Security Risks and Operational Hurdles

Open RAN systems operate with multiple vendors providing various components, from hardware to software and security solutions. Managing a multi-vendor environment introduces significant operational complexity, particularly when ensuring cohesive security standards across different platforms. Vendor fragmentation poses challenges in terms of accountability and coordination, making it difficult to establish a unified security framework.

Telecom operators are tasked with managing several vendors, each with its proprietary systems and protocols. This complicates the security landscape as inconsistent security measures across vendors increase the risk of potential vulnerabilities being exploited. For instance, if one vendor's software does not meet stringent security requirements, it could compromise the entire Open RAN system.

Furthermore, vendor-related security challenges create additional pressure on operators to invest in monitoring, auditing, and updating systems, leading to higher operational costs. This adds another financial burden, which is already compounded by high integration costs, making some operators hesitant to fully commit to Open RAN deployments.

By Component Analysis

In 2023, Hardware dominated the Open RAN Security market components.

In 2023, Hardware held a dominant market position in the By Component segment of the Open RAN Security Market. The hardware segment's dominance can be attributed to the rising demand for specialized security components such as secure processors, encryption hardware, and custom chips designed for Open RAN infrastructures. These physical devices ensure the integrity and confidentiality of communications, particularly as telecom networks move towards disaggregated and open architectures. The adoption of advanced hardware solutions is driven by their ability to provide robust security measures against cyber threats targeting critical network infrastructure.

Software solutions also gained considerable traction, leveraging advanced algorithms, AI, and machine learning to enhance threat detection, incident response, and vulnerability management. Open RAN’s software-defined nature demands continuous monitoring, making software-based security critical for real-time protection.

Finally, Services in the form of managed security services and consulting saw significant growth. These services provide organizations with tailored support, from vulnerability assessments to ongoing monitoring and compliance, addressing the complexities of securing disaggregated network elements. The services segment is increasingly critical as telecom operators look for end-to-end security solutions.

By Unit Analysis

In 2023, The Radio Unit dominated the Open RAN Security Market.

In 2023, The Radio Unit (RU) held a dominant market position in the Open RAN Security Market across the By Unit segment, comprising the Radio Unit, Distributed Unit, and Centralized Unit categories. The Radio Unit's growth is driven by its essential role in ensuring secure communication between end-user devices and network infrastructure. With Open RAN architectures expanding, the RU remains crucial for integrating secure, multi-vendor systems, thus becoming a focal point for cybersecurity efforts. The increasing adoption of 5G technologies further escalates the demand for secure Radio Units, as they enable encrypted data transmission while addressing the security vulnerabilities inherent in open interfaces.

The Distributed Unit (DU), which manages layer 1 and layer 2 functions, plays a vital role in offloading security tasks from the Centralized Unit and securing the network’s edge. Its ability to ensure secure, low-latency communication at local points of the network positions it for growth.

Finally, the Centralized Unit (CU) oversees higher-layer protocols and centralized control, integrating advanced security features to protect data as it transits across the core network. Combined, these units create a robust security ecosystem within Open RAN deployments.

By Deployment Analysis

In 2023, Private cloud deployment dominated the Open RAN Security Market.

In 2023, The Private cloud deployment segment held a dominant market position in the Open RAN Security Market. This dominance can be attributed to the growing need for enhanced data privacy and control within organizations. Enterprises in sectors such as telecommunications, defense, and banking increasingly opted for private cloud infrastructure to ensure secure and reliable Open RAN deployments. The private cloud offers organizations better control over their network security, reducing the risks of cyberattacks and unauthorized access. Furthermore, the rising adoption of Open RAN technology by large organizations with existing private cloud infrastructure has also bolstered the segment's growth.

The hybrid cloud deployment segment, although slightly behind, showed significant growth due to its flexibility. Organizations leveraged a combination of public and private cloud environments to balance cost, scalability, and security needs in Open RAN security.

The public cloud deployment segment witnessed moderate growth, driven by the demand for scalable, cost-effective solutions. However, concerns regarding data privacy and compliance continue to limit its widespread adoption in security-sensitive industries, although its low-cost benefits are expected to increase its future market share.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Unit

- Radio Unit

- Distributed Unit

- Centralized Unit

By Deployment

- Private

- Hybrid Cloud

- Public Cloud

Growth Opportunity

Growing Demand for Network Flexibility and Compatibility

The global Open RAN security market is poised for significant growth, driven by the increasing demand for network flexibility and compatibility. Open RAN architectures offer operators the flexibility to choose components from different vendors, which reduces dependency on traditional, proprietary solutions. This shift toward a disaggregated network infrastructure creates new security challenges but also opens up vast opportunities for cybersecurity providers to develop solutions tailored for Open RAN systems. As telecom operators look to increase operational agility, the demand for security solutions that ensure the integrity, confidentiality, and availability of these flexible networks is expected to surge.

Accelerating Adoption of 5G Technology

The rapid deployment of 5G technology is another key driver in the growth of the Open RAN security market. As telecom operators expand their 5G infrastructure, there is an increasing need for robust security solutions that can protect the enhanced data flows and new applications made possible by 5G. Open RAN architectures, often used in conjunction with 5G, require advanced security protocols to address the increased threat surface. The global push toward 5G, especially in regions such as North America, Europe, and Asia-Pacific, is expected to create substantial demand for Open RAN security solutions, presenting lucrative opportunities for industry stakeholders.

Latest Trends

Focus on Security Solutions

A heightened focus on security solutions in Open Radio Access Networks (RAN) is expected to shape the market. As more telecom operators adopt Open RAN architectures, security concerns surrounding the disaggregation of network components will intensify. Vendors and operators are projected to prioritize end-to-end security frameworks to safeguard against evolving cyber threats, including data breaches and denial-of-service attacks. The shift from traditional, integrated systems to open, multi-vendor environments increases the potential attack surface, driving demand for advanced security tools that ensure the integrity, confidentiality, and availability of network infrastructure.

Integration of AI and Machine Learning

Artificial intelligence (AI) and machine learning (ML) technologies are anticipated to play a pivotal role in enhancing Open RAN security. These technologies will enable more effective threat detection, prevention, and response by analyzing vast amounts of network data in real-time. AI-driven analytics will allow for the rapid identification of anomalous behavior, while machine learning algorithms will improve predictive capabilities, reducing the risk of both known and emerging threats. More operators are likely to integrate AI/ML solutions into their security infrastructure to achieve autonomous, self-optimizing networks, thus minimizing manual intervention and reducing response times to potential security incidents.

Regional Analysis

North America dominates the Open RAN Security Market with a 35% largest share.

The Open RAN Security Market exhibits varying growth dynamics across key regions, with North America dominating the market, accounting for approximately 35% of the global market share. This leadership can be attributed to the region's advanced telecommunications infrastructure, strong investment in 5G deployment, and the presence of key market players such as Cisco Systems and Mavenir. The U.S. government’s initiatives to secure its telecom networks further bolster the demand for Open RAN security solutions.

In Europe, the market is growing steadily due to increasing government support for open architecture and stringent cybersecurity regulations. Countries like Germany and the UK are leading the adoption, driven by the rollout of 5G networks and the European Union’s focus on securing digital infrastructures.

The Asia Pacific region is witnessing significant growth, driven by major economies such as China, Japan, and South Korea. The rapid 5G deployment, coupled with increasing cybersecurity threats, fuels the demand for robust Open RAN security solutions. Asia Pacific is projected to witness the highest CAGR, estimated at over 10% during the forecast period.

In the Middle East & Africa and Latin America, market growth remains gradual but is expected to accelerate as 5G networks expand and regional governments emphasize network security. These regions are anticipated to experience increased adoption as they further develop their telecom infrastructures.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Open RAN Security Market in 2024 is expected to witness substantial growth, driven by increased deployment of 5G networks and the rising need for secure, scalable, and flexible network infrastructures. Key players in the market are positioning themselves to address security vulnerabilities associated with the disaggregation of traditional network elements.

Mavenir, Altiostar, and Parallel Wireless are at the forefront of innovation, offering software-centric solutions that are critical to enabling secure Open RAN architectures. Their focus on virtualization and cloud-native security models places them as leaders in safeguarding open interfaces and data integrity across RAN components.

NEC Corporation and Fujitsu are playing pivotal roles in integrating robust security features into Open RAN hardware, ensuring compatibility with various security frameworks while enhancing network resilience. Their long-standing expertise in telecommunications equipment strengthens their position in the global market.

Qualcomm, Intel Corporation, and ZTE Corporation are focusing on securing the semiconductor and chipset level, addressing potential hardware vulnerabilities. Their advanced security features embedded within their processors ensure data confidentiality and integrity, crucial for the secure transmission of information.

Cisco, VMware, and Nokia are contributing through their expertise in network management and virtualization. Their solutions are integral to creating secure, multi-vendor Open RAN ecosystems by addressing network slicing and threat management challenges.

Samsung and Airspan Networks are enhancing the market's security landscape by focusing on integrated solutions that provide end-to-end protection, from the edge to the core, ensuring a comprehensive defense mechanism for Open RAN environments.

Market Key Players

- Mavenir

- Altiostar

- Parallel Wireless

- Radisys

- NEC Corporation

- Qualcomm

- Samsung

- Airspan Networks

- Fujitsu

- NEC Corporation

- Cisco

- Nokia

- Intel Corporation

- ZTE Corporation

- VMware

Recent Development

- In January 2024, Ericsson announced that it would introduce support for open fronthaul across its Cloud RAN and radio portfolios starting in 2024. This development will enhance network flexibility and bolster security by enabling better integration with open RAN standards, particularly in areas where multiple vendors operate together in a disaggregated architecture. This is crucial as open interfaces often come with increased security considerations due to the multi-vendor environment.

- In May 2024, the U.S. National Telecommunications and Information Administration (NTIA) announced a second round of funding from its Wireless Innovation Fund. This $420 million initiative is focused on supporting the development and commercialization of Open RAN radio units. The program aims to foster competition in the telecommunications supply chain and ensure secure, open, and interoperable network architectures.

- In September 2023, The National Security Agency (NSA) and the Cybersecurity and Infrastructure Security Agency (CISA) released an updated report on Open RAN security considerations. This guidance, developed through the Enduring Security Framework (ESF), highlights the security risks and mitigations specific to Open RAN, focusing on issues like multi-vendor integration, cloud-based 5G cores, and AI/ML-based optimization apps. The report aims to help network operators better secure their Open RAN deployments.

Report Scope

Report Features Description Market Value (2023) USD 2.9 Billion Forecast Revenue (2033) USD 49.2 Billion CAGR (2024-2032) 33.7% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Hardware, Software, Services), By Unit (Radio Unit, Distributed Unit, Centralized Unit), By Deployment (Private, Hybrid Cloud, Public Cloud) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Mavenir, Altiostar, Parallel Wireless, Radisys, NEC Corporation, Qualcomm, Samsung, Airspan Networks, Fujitsu, NEC Corporation, Cisco, Nokia, Intel Corporation, ZTE Corporation, VMware] Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Mavenir

- Altiostar

- Parallel Wireless

- Radisys

- NEC Corporation

- Qualcomm

- Samsung

- Airspan Networks

- Fujitsu

- NEC Corporation

- Cisco

- Nokia

- Intel Corporation

- ZTE Corporation

- VMware

Our Clients

View Our Licence Options