Mobility as a Service Market By Service Type (Ride Hailing, Car Sharing, Micromobility, Bus Sharing, Train Services), By Operating System (Android, iOS, Others), By Transportation Type (Private, Public), By Solution Type (Technology Platforms, Payment Engines, Navigation Solutions, Telecom Connectivity Providers, Ticketing Solutions, Insurance Services), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

13776

-

June 2023

-

103

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

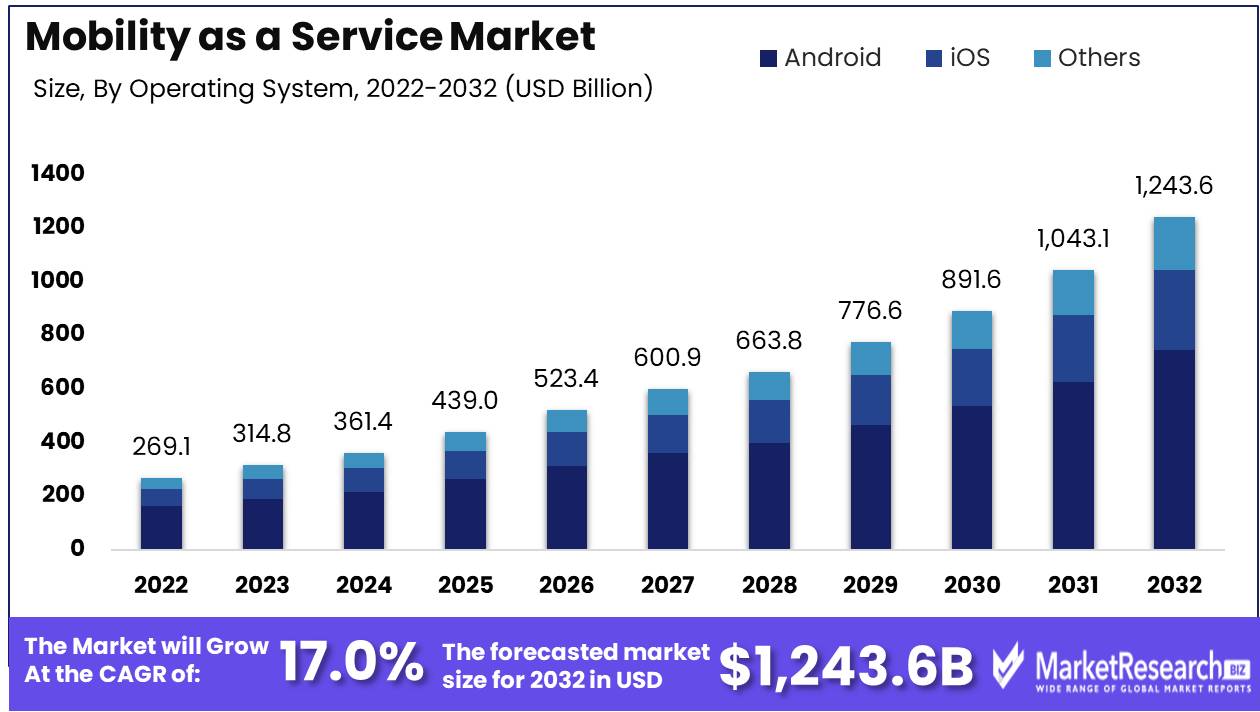

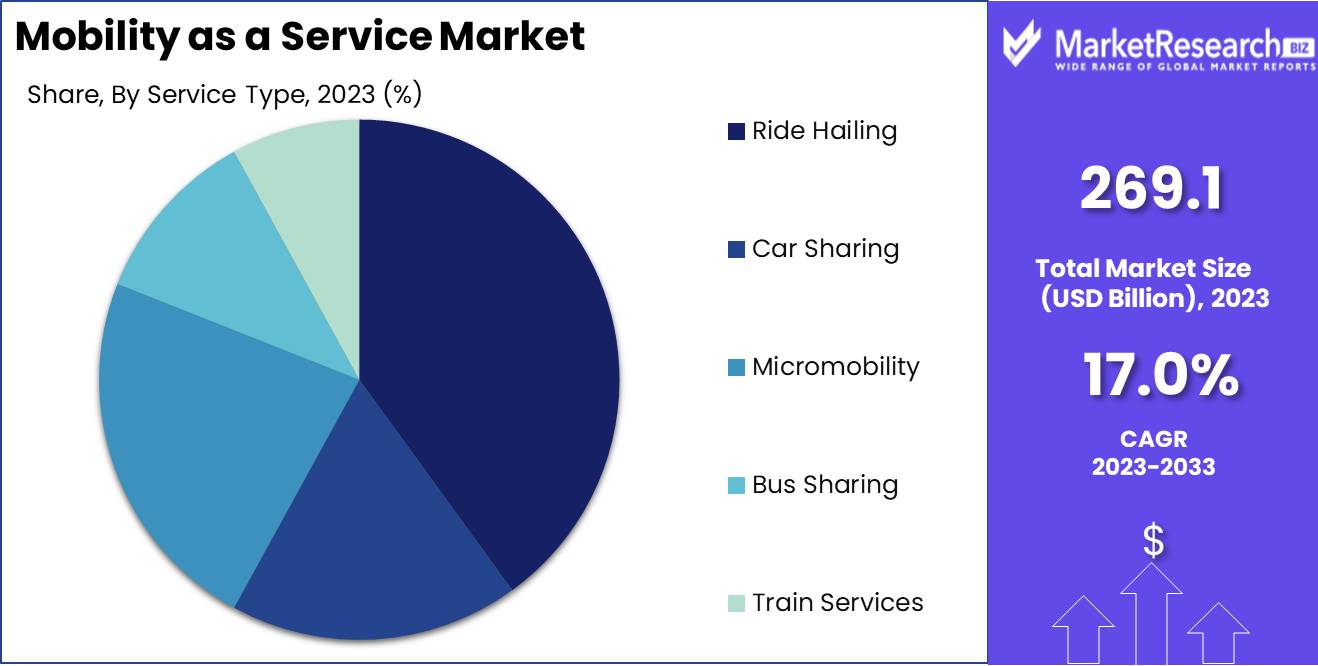

The Global Mobility as a Service Market was valued at USD 269.1 Bn in 2023. It is expected to reach USD 1243.6 Bn by 2033, with a CAGR of 17% during the forecast period from 2024 to 2033.

The Mobility as a Service (MaaS) Market involves the integration of various transportation services into a single accessible on-demand platform. MaaS aims to simplify urban and regional travel by combining public transit, ride-sharing, car rentals, bike-sharing, and other mobility services into a cohesive digital interface. This market is driven by advancements in technology, increasing urbanization, and the growing need for sustainable and efficient transportation solutions.

MaaS enhances user convenience and optimizes travel efficiency, positioning itself as a transformative solution in the evolving landscape of urban mobility. The Mobility as a Service (MaaS) Market is poised for substantial growth, driven by the increasing demand for integrated and sustainable transportation solutions. MaaS offers a seamless blend of various transportation modes, such as public transit, ride-sharing, bike-sharing, and car rentals, into a single accessible platform.

MaaS enhances user convenience and optimizes travel efficiency, positioning itself as a transformative solution in the evolving landscape of urban mobility. The Mobility as a Service (MaaS) Market is poised for substantial growth, driven by the increasing demand for integrated and sustainable transportation solutions. MaaS offers a seamless blend of various transportation modes, such as public transit, ride-sharing, bike-sharing, and car rentals, into a single accessible platform.This integration simplifies urban and regional travel, providing users with efficient, cost-effective, and environmentally friendly mobility options. MaaS was first conceptualized in the 1990s, with a notable trial conducted in Gothenburg, Sweden under a monthly subscription model, demonstrating its potential to revolutionize transportation. The launch of the world's first MaaS platform, the Whim app, in Helsinki, Finland in 2017, marked a significant milestone, showcasing the practical application and consumer acceptance of MaaS solutions.

The market's growth is further propelled by advancements in digital technology, data analytics, and real-time information systems, which enhance the functionality and user experience of MaaS platforms. As urbanization continues to rise, the need for efficient transportation networks becomes increasingly critical, positioning MaaS as a viable solution to reduce congestion, lower emissions, and improve overall travel efficiency.

T success of MaaS hinges on the ability to provide a seamless, user-friendly experience that integrates diverse mobility services with real-time updates and streamlined payment systems. As the market evolves, stakeholders must prioritize sustainable practices and user-centric approaches to maintain growth momentum and address the challenges of modern urban mobility. The competitive landscape will likely see intensified innovation and strategic partnerships as companies strive to enhance their service offerings and expand their footprint in this dynamic market.

Key Takeaways

- Market Value: The Global Mobility as a Service Market was valued at USD 269.1 Bn in 2023. It is expected to reach USD 1243.6 Bn by 2033, with a CAGR of 17% during the forecast period from 2024 to 2033.

- By Service Type: Ride Hailing leads with a 40% market share, driven by urbanization and the convenience of app-based transportation.

- By Operating System: Android dominates the market with a 60% share, reflecting its widespread adoption and user base.

- By Transportation Type: Private transportation services hold a 55% market share, favored for their flexibility and personalized options.

- Regional Dominance: Europe commands the market with a 41.2% share, supported by advanced infrastructure and strong governmental support for sustainable mobility solutions.

- Growth Opportunity: Integration of electric and autonomous vehicles into MaaS platforms presents significant growth opportunities.

Driving factors

Increasing Traffic Congestion

Increasing traffic congestion is a major driver for the growth of the Mobility as a Service (MaaS) market. Urbanization and population growth have led to a surge in vehicle ownership, resulting in severe traffic congestion in cities worldwide. MaaS offers a solution to these congestion challenges by integrating various modes of transportation—such as public transit, ride-sharing, bike-sharing, and car rental—into a single accessible platform. This integration not only reduces the number of vehicles on the road but also optimizes traffic flow by promoting efficient use of available transport options.

By providing real-time data and predictive analytics, MaaS platforms help users make informed decisions about their travel routes and modes, thereby reducing individual reliance on private cars. This shift from private vehicle ownership to shared mobility services is crucial for managing traffic congestion effectively and enhancing urban mobility.

Cost-Effectiveness and Convenience for Users

The cost-effectiveness and convenience offered by MaaS platforms are critical factors driving their adoption. Traditional car ownership entails significant expenses, including purchase costs, maintenance, insurance, and fuel. MaaS, on the other hand, provides a pay-as-you-go model that allows users to access various transportation services without the financial burden of owning a vehicle. This substantial cost-saving potential makes MaaS an attractive option for many users, particularly in urban areas where the availability of diverse transport modes is higher.

MaaS platforms enhance convenience by offering seamless travel planning, booking, and payment options through a single app. Users can effortlessly switch between different modes of transportation, such as buses, trains, ride-shares, and bikes, without the hassle of managing multiple tickets or payment methods. The integration of services and real-time updates ensures a smooth and efficient travel experience, catering to the modern consumer's demand for convenience and efficiency.

Restraining Factors

Lack of Standardization

The lack of standardization poses a significant challenge to the growth of the Mobility as a Service (MaaS) market. MaaS relies on the integration of various transportation services, including public transit, ride-sharing, bike-sharing, and car rentals, into a unified platform. However, the absence of standardized protocols and interfaces between these services can hinder seamless integration.

Different transportation providers use varying technologies and operational frameworks, creating compatibility issues when trying to combine services on a single platform. This fragmentation can lead to inefficiencies and reduced user experience, as consumers may face difficulties accessing and transitioning between different modes of transportation smoothly.

Data Privacy Issues

Data privacy issues represent another significant barrier to the adoption and growth of the MaaS market. MaaS platforms collect vast amounts of data from users, including personal information, travel patterns, payment details, and location data. While this data is essential for optimizing services and providing personalized experiences, it raises concerns about user privacy and data security.

Consumers are increasingly aware of and sensitive to how their data is collected, stored, and used. High-profile data breaches and misuse of personal information in various sectors have heightened these concerns, making data privacy a critical factor for MaaS providers to address. Regulatory frameworks like the General Data Protection Regulation (GDPR) in Europe impose strict requirements on data handling, and non-compliance can result in significant penalties and loss of consumer trust.

By Service Type Analysis

Ride hailing services constitute 40% of the market by service type.

In 2023, Ride Hailing held a dominant market position in the By Service Type segment of the Mobility as a Service (MaaS) Market, capturing more than a 40% share. The prominence of Ride Hailing services can be attributed to their convenience, flexibility, and widespread availability. The integration of advanced technology, such as real-time tracking, seamless payment options, and user-friendly mobile applications, has significantly enhanced the user experience, leading to a surge in demand. Major ride-hailing companies have expanded their service networks, providing reliable and efficient transportation solutions in urban and suburban areas alike.

Car Sharing, while holding a smaller market share, continues to be an important segment within the MaaS market. This service type appeals to cost-conscious consumers who prefer the flexibility of accessing a vehicle without the responsibilities of ownership. Car Sharing is particularly popular in densely populated urban areas where parking space is limited, and the cost of vehicle ownership is high.

Micromobility, which includes services such as bike-sharing and e-scooters, represents a growing segment within the MaaS market. This service type is highly favored for short-distance travel, providing a convenient and environmentally friendly alternative to traditional transportation modes. The increasing implementation of dedicated infrastructure, such as bike lanes and e-scooter docking stations, supports the growth of micromobility services.

Bus Sharing, although capturing a smaller portion of the market, plays a crucial role in providing affordable and accessible transportation solutions. Bus sharing services are particularly important in regions with limited public transportation infrastructure, offering an economical alternative to private vehicle usage. The integration of technology, such as mobile apps for booking and real-time tracking, enhances the user experience and operational efficiency of bus-sharing services.

Train Services, while representing a smaller segment within the MaaS market, are essential for long-distance and intercity travel. Train services are highly valued for their reliability, speed, and capacity to transport a large number of passengers. The development of high-speed rail networks and the modernization of existing train infrastructure further support the demand for train services within the MaaS ecosystem.

By Operating System Analysis

Android operating systems dominate with 60% of the market by operating system.

In 2023, Android held a dominant market position in the By Operating System segment of the Mobility as a Service (MaaS) Market, capturing more than a 60% share. The dominance of Android can be attributed to its extensive user base, affordability of Android devices, and widespread availability across diverse geographic regions. Android's open-source nature allows for greater flexibility and customization, which has led to the development of numerous MaaS applications tailored to meet the specific needs of different markets. Additionally, the broad compatibility of Android with various hardware and software ecosystems enhances its attractiveness to both users and developers.

iOS, while maintaining a significant presence, holds a smaller share in the By Operating System segment. iOS is favored for its robust security features, seamless integration with other Apple products, and a high level of user engagement. The premium user base of iOS often translates to higher spending on MaaS services, making it an important segment despite its smaller market share. The ecosystem's strong emphasis on user experience and consistent performance across devices supports the continued growth of MaaS applications on the iOS platform.

Others, including alternative operating systems and proprietary systems used by specific MaaS providers, represent a smaller portion of the market. These operating systems cater to niche segments or specific regions where they hold a competitive advantage. Although their market share is relatively minor, they contribute to the overall diversity and resilience of the MaaS market by offering specialized solutions.

By Transportation Type Analysis

Private transportation accounts for 55% of the market by transportation type.

In 2023, Private held a dominant market position in the By Transportation Type segment of the Mobility as a Service (MaaS) Market, capturing more than a 55% share. The preference for Private transportation within the MaaS market can be attributed to the increasing demand for convenience, flexibility, and personalized travel experiences. Private transportation options, such as ride-hailing and car-sharing services, offer users the ability to travel on their own schedule, without the constraints of fixed routes and schedules. The proliferation of mobile apps that facilitate easy booking, payment, and real-time tracking has further enhanced the appeal of Private transportation services.

Public transportation, while holding a significant share, represents a smaller portion of the By Transportation Type segment. Public transportation services, including bus sharing, train services, and other mass transit options, are essential for providing cost-effective and environmentally friendly mobility solutions. These services are critical in densely populated urban areas and regions with developed public transit infrastructure. The integration of MaaS platforms with public transportation systems has improved accessibility and convenience for users, encouraging the adoption of public transport options.

Key Market Segments

By Service Type

- Ride Hailing

- Car Sharing

- Micromobility

- Bus Sharing

- Train Services

By Operating System

- Android

- iOS

- Others

By Transportation Type

- Private

- Public

By Solution Type

- Technology Platforms

- Payment Engines

- Navigation Solutions

- Telecom Connectivity Providers

- Ticketing Solutions

- Insurance Services

Growth Opportunity

Advancements in Digital Technologies

Advancements in digital technologies are transforming the MaaS landscape, offering new avenues for innovation and service improvement. Technologies such as artificial intelligence (AI), machine learning, and big data analytics enable MaaS providers to offer personalized, efficient, and seamless travel experiences. AI and machine learning algorithms can optimize route planning, predict demand patterns, and enhance real-time decision-making, thereby improving service reliability and user satisfaction.

The integration of Internet of Things (IoT) devices across transportation modes enhances connectivity and data collection, facilitating better coordination and management of mobility services. For instance, smart sensors and connected vehicles provide real-time traffic updates, vehicle health monitoring, and predictive maintenance, ensuring higher service quality and safety. By leveraging these digital advancements, MaaS providers can offer more responsive and user-centric solutions, driving higher adoption rates.

Shift Towards Fleet Electrification

The shift towards fleet electrification presents a significant growth opportunity for the MaaS market. As governments worldwide implement stricter emissions regulations and promote sustainable transportation, the adoption of electric vehicles (EVs) within MaaS platforms is accelerating. Electric fleets not only reduce environmental impact but also offer cost advantages due to lower operational and maintenance costs compared to traditional combustion engine vehicles.

MaaS providers that invest in electrifying their fleets can benefit from regulatory incentives, such as tax breaks and subsidies, while also appealing to eco-conscious consumers. Cities like Oslo and Amsterdam are leading the way in electrification initiatives, providing infrastructure support and incentives for EV adoption. By integrating electric vehicles into their services, MaaS providers can enhance their sustainability credentials and attract a growing base of environmentally aware users.

Latest Trends

Integration of Multiple Transportation Modes

The integration of multiple transportation modes is a key trend that enhances the attractiveness and utility of MaaS platforms. By incorporating various modes of transport—such as public transit, ride-sharing, bike-sharing, and car rentals—into a single platform, MaaS providers can offer seamless, end-to-end travel solutions.

This multimodal integration allows users to plan, book, and pay for their journeys using a single app, improving convenience and efficiency. Cities like Helsinki and Vienna are pioneering multimodal MaaS platforms that facilitate easy transitions between different transportation modes, reducing travel time and enhancing user satisfaction.

Subscription-Based Business Models

The rise of subscription-based business models is transforming how users engage with MaaS services. These models provide users with flexible, cost-effective access to a range of transportation options for a fixed monthly fee. Subscription plans can be tailored to individual needs, offering unlimited rides on public transit, discounted rates for ride-sharing, and free minutes for bike-sharing.

This approach not only simplifies budgeting for users but also encourages frequent use of MaaS services, leading to higher user retention and increased revenue stability for providers. Companies like Whim and Citymapper are already successfully implementing subscription-based models, reflecting a shift towards sustained user engagement and loyalty.

Regional Analysis

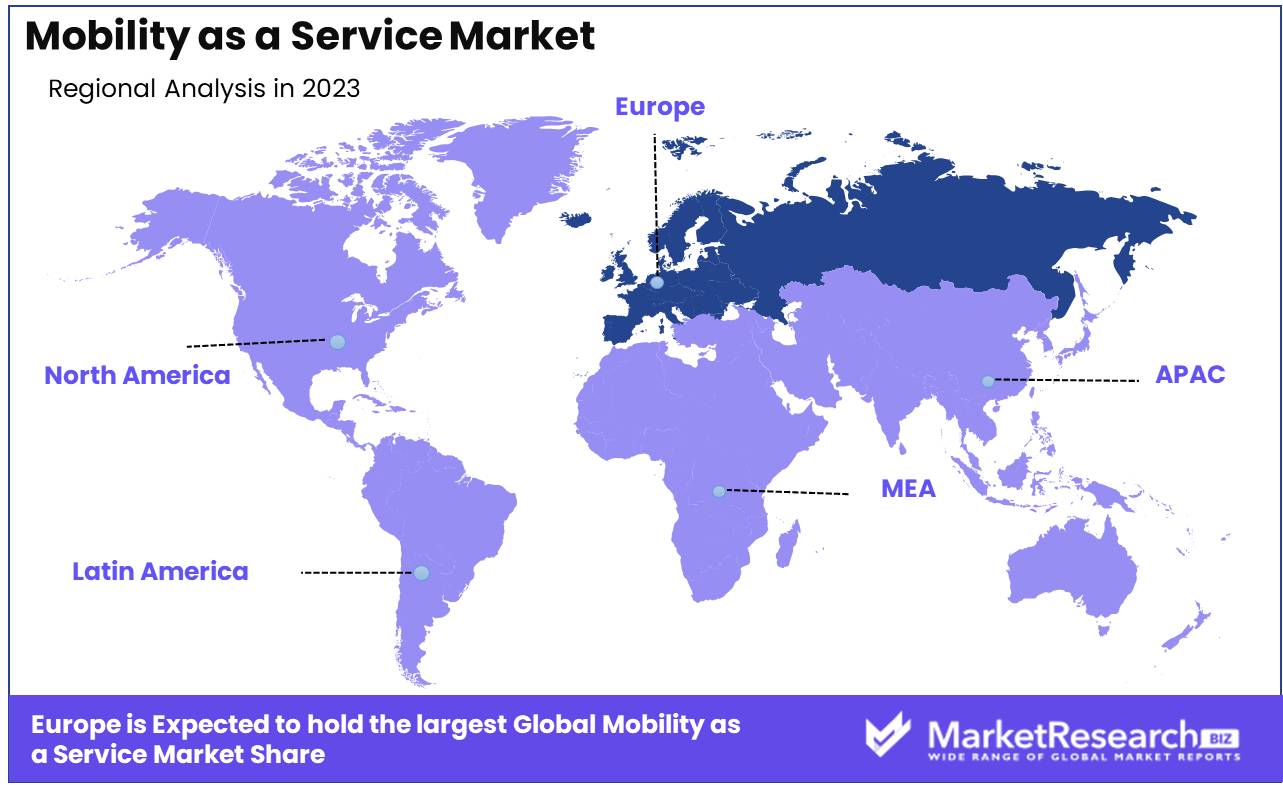

The Mobility as a Service (MaaS) market showcases distinct regional trends, with Europe leading the global landscape, holding a substantial 41.2% market share. Europe's dominance is attributed to advanced transportation infrastructure, progressive regulatory frameworks, and a high degree of urbanization. Countries such as Germany, the UK, and France are at the forefront, where integrated mobility solutions are increasingly adopted to enhance urban transport efficiency and reduce environmental impact.

In North America, the MaaS market is driven by technological advancements and the increasing adoption of smart city initiatives. The United States and Canada are key markets, with a growing emphasis on reducing traffic congestion and improving urban mobility.

Asia Pacific represents a rapidly growing market, fueled by the region's expanding urban population and significant investments in smart city projects. China, Japan, and India are notable markets where rising disposable incomes and increasing smartphone penetration drive the demand for seamless and efficient mobility services.

The Middle East & Africa region, though smaller in market size, is experiencing steady growth in the MaaS sector. Urbanization and a growing middle class in countries like the UAE and South Africa drive the demand for advanced mobility solutions.

Latin America is witnessing gradual growth in the MaaS market, with Brazil and Mexico being key contributors. The increasing urbanization and the need for efficient public transportation systems drive the demand for MaaS solutions.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global Mobility as a Service (MaaS) market is witnessing significant evolution, driven by leading companies that are innovating and expanding their offerings. Uber Technologies Inc. and Didi Chuxing Technology Co., Ltd. continue to dominate the market with their extensive global footprints and comprehensive mobility solutions. Uber’s continuous investment in autonomous vehicles and partnerships with public transportation systems underscores its commitment to redefining urban mobility. Didi Chuxing, leveraging its massive user base in China, is also making strategic moves to expand internationally, particularly in emerging markets.

Lyft Inc. remains a key player in North America, focusing on sustainable mobility solutions, including bike-sharing and electric vehicles. The company's emphasis on green transportation aligns with growing environmental awareness among consumers.

Gett, Inc. and mytaxi are significant players in Europe, offering tailored solutions that integrate traditional taxis with modern app-based booking systems. These companies are capitalizing on Europe’s strong regulatory support for MaaS and advanced urban infrastructure.

Ola Cabs and MERU Cabs lead the MaaS market in India, catering to the unique needs of the region with affordable and reliable services. Ola's expansion into electric vehicles and MERU's emphasis on safety and customer service position them strongly in a rapidly growing market.

BlaBlaCar, Careem, and Yandex.Taxi (Yandex N.V.) are making significant strides in the carpooling and ride-sharing segments. BlaBlaCar’s focus on long-distance carpooling, Careem’s dominance in the Middle East, and Yandex.Taxi’s integration with Russia's extensive digital ecosystem highlight their strategic advantages.

Kakao Corp. and LeCab SAS are key players in the Asian and European markets, respectively. Kakao's integration with its messaging app offers a seamless user experience in South Korea, while LeCab focuses on premium services in France.

Via Transportation Inc., Addison Lee Limited, Flywheel Software, Inc., Easy Taxi Serviços Ltd., and Gocatch are expanding their market presence through innovative services and strategic partnerships, enhancing the overall user experience and operational efficiency.

Market Key Players

- Uber Technologies Inc.

- Didi Chuxing Technology Co., Ltd.

- Lyft Inc.

- Gett, Inc.

- Mytaxi

- Ola Cabs

- BlaBlaCar

- Careem

- Kakao Corp.

- Addison Lee Limited

- MERU Cabs

- Via Transportation Inc.

- Yandex N.V. (Yandex.Taxi)

- LeCab SAS

- Ingogo PTY LTD

- Flywheel Software, Inc.

- Easy Taxi Serviços Ltd.

- Gocatch

Recent Development

- In June 2024, South Korea’s Kolon Group plans an additional 12.4 billion won investment in Papa Mobility, a ride-hailing service for disadvantaged people, bringing total investment to 32.9 billion won, aiming for eventual acquisition.

- In May 2024, Siemens Mobility is investing €150m to expand its Dortmund-Eving depot, aiming to increase capacity and serve more train types. The new service centre will employ 250 staff by 2026.

Report Scope

Report Features Description Market Value (2023) USD 269.1 Bn Forecast Revenue (2033) USD 1243.6 Bn CAGR (2024-2033) 17% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Service Type (Ride Hailing, Car Sharing, Micromobility, Bus Sharing, Train Services), By Operating System (Android, iOS, Others), By Transportation Type (Private, Public), By Solution Type (Technology Platforms, Payment Engines, Navigation Solutions, Telecom Connectivity Providers, Ticketing Solutions, Insurance Services) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Uber Technologies Inc., Didi Chuxing Technology Co., Ltd., Lyft Inc., Gett, Inc., Mytaxi, Ola Cabs, BlaBlaCar, Careem, Kakao Corp., Addison Lee Limited, MERU Cabs, Via Transportation Inc., Yandex N.V. (Yandex.Taxi), LeCab SAS, Ingogo PTY LTD, Flywheel Software, Inc., Easy Taxi Serviços Ltd., Gocatch, Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Uber Technologies Inc.

- Didi Chuxing Technology Co., Ltd.

- Lyft Inc.

- Gett, Inc.

- Mytaxi

- Ola Cabs

- BlaBlaCar

- Careem

- Kakao Corp.

- Addison Lee Limited

- MERU Cabs

- Via Transportation Inc.

- Yandex N.V. (Yandex.Taxi)

- LeCab SAS

- Ingogo PTY LTD

- Flywheel Software, Inc.

- Easy Taxi Serviços Ltd.

- Gocatch

Our Clients

View Our Licence Options