Methyl Methacrylate (MMA) Market Report By Application (Chemical Intermediates, Surface Coatings, Emulsion Polymer), By Grade (General Grade MMA, Optical Grade MMA, Industrial Grade MMA), By End-Use Industry (Construction, Automotive, Electronics, Medical, Packaging, Aerospace, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

6633

-

May 2024

-

324

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

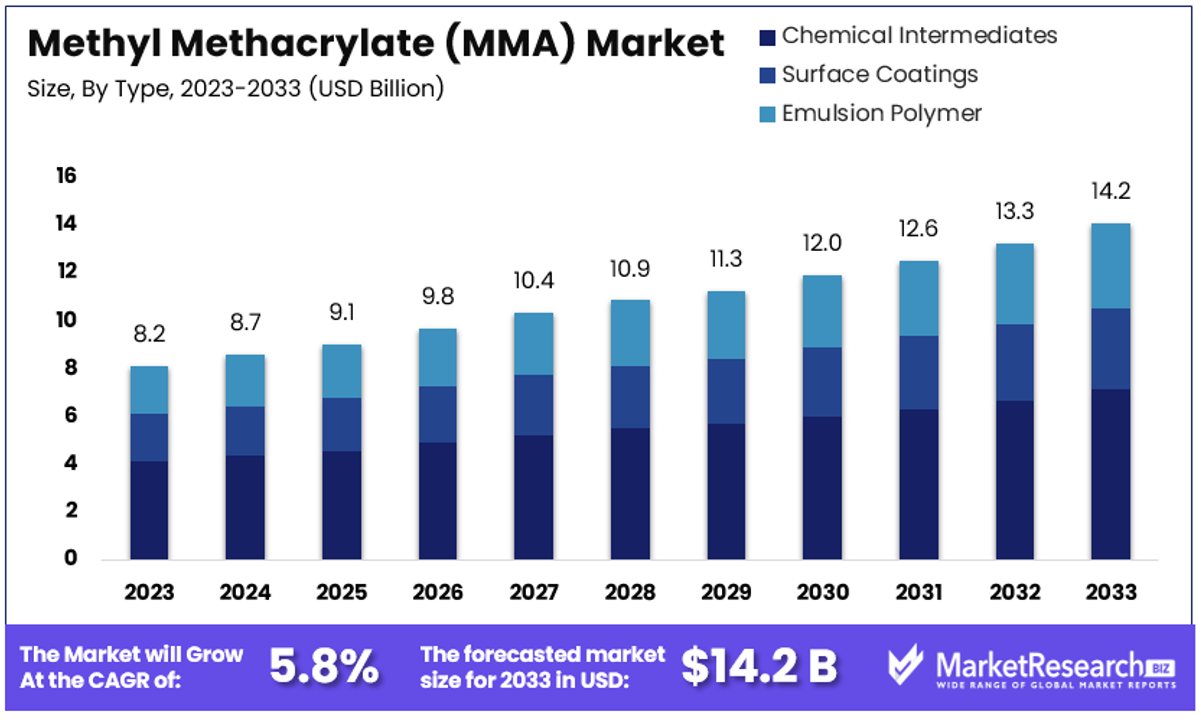

The Global Methyl Methacrylate (MMA) Market size is expected to be worth around USD 14.2 Billion by 2033, from USD 8.2 Billion in 2023, growing at a CAGR of 5.8% during the forecast period from 2024 to 2033.

The Methyl Methacrylate (MMA) Market involves the production and distribution of MMA, a versatile chemical used primarily as a building block in the manufacture of polymethyl methacrylate (PMMA) and other acrylic plastics. These materials are crucial for applications ranging from automotive parts to electronics and construction materials due to their clarity, durability, and weather resistance.

Key growth drivers include rising demand in sectors such as automotive and electronics, where durable, lightweight materials are essential. Industry leaders focus on innovation and environmental sustainability to meet global standards and consumer expectations, making this market critical for strategic decision-making in manufacturing and design sectors.

In the Methyl Methacrylate (MMA) Market, a detailed analysis reveals a sector poised for significant growth, driven largely by the expanding demands of the construction industry. As of the first quarter of 2023, the United States alone boasted over 919,000 construction establishments, employing around 8.0 million individuals and contributing nearly $2.1 trillion annually in construction outputs.

Notably, total construction spending in the U.S. reached approximately $1.98 trillion in August 2023, marking a 7.4% increase from the previous year. This growth is primarily fueled by a robust 17.6% year-over-year rise in nonresidential construction spending, although residential construction saw a decline of 3%.

These dynamics within the construction sector directly influence the demand for MMA, as it is a critical component in producing durable, high-performance acrylic plastics used extensively in nonresidential construction projects for applications like glazing, lighting fixtures, and signage. The increase in nonresidential construction spending indicates a heightened demand for MMA-based products, aligning with industry trends toward more sustainable and innovative building materials.

Given this backdrop, stakeholders in the MMA market must consider strategic investments in production capabilities to meet the rising demand. Furthermore, innovation in eco-friendly production processes and recycling technologies will be key to maintaining competitiveness and aligning with global sustainability goals. Companies positioned at the forefront of these initiatives are likely to see substantial growth opportunities as the market continues to evolve in response to construction industry trends and environmental considerations.

Key Takeaways

- Market Value: The Global Methyl Methacrylate (MMA) Market is forecasted to reach USD 14.2 billion by 2033, showing growth from USD 8.2 billion in 2023, with a CAGR of 5.8% during the forecast period from 2024 to 2033.

- Application Analysis: Chemical Intermediates dominate with 45% market share, crucial for diverse chemical synthesis processes across industries. Surface Coatings and Emulsion Polymer represent significant but smaller segments.

- Grade Analysis: General Grade MMA dominates with 55% market share, favored for its broad utility across multiple industries. Optical Grade and Industrial Grade MMA cater to specialized applications requiring specific properties.

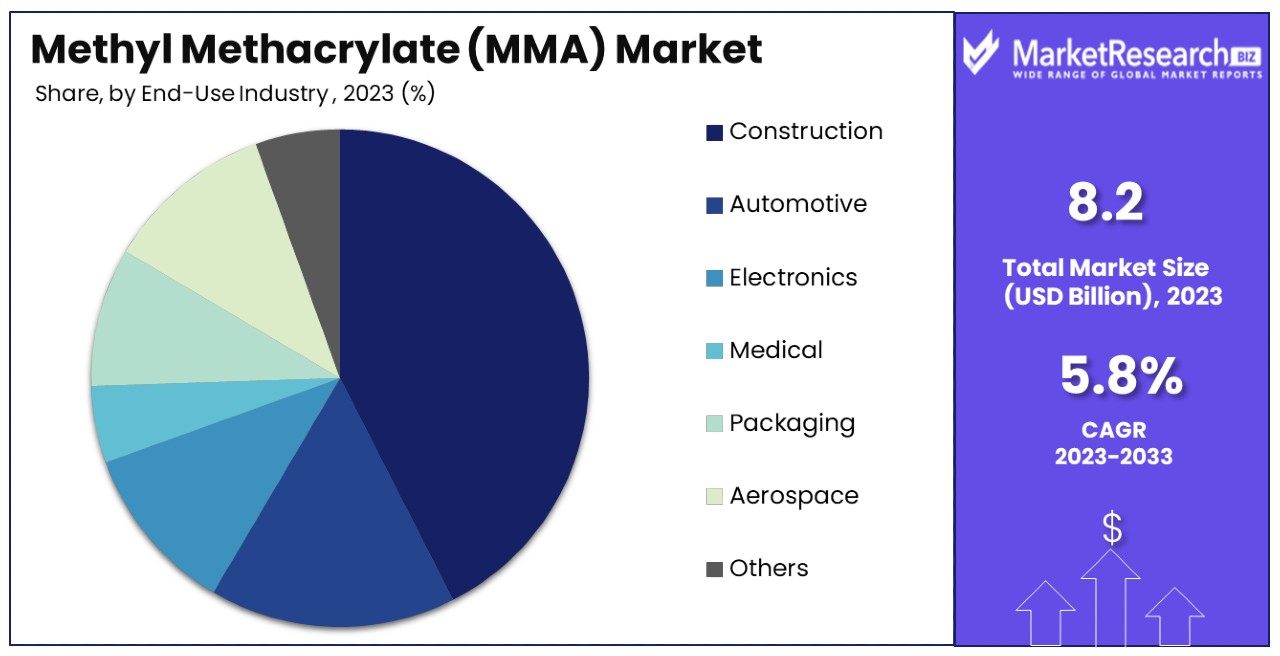

- End-Use Industry Analysis: Construction holds the largest share at 40% due to extensive use of MMA in building materials and design innovations. Other significant sectors include Automotive, Electronics, Medical, Packaging, Aerospace, and Others, each integrating MMA in various capacities.

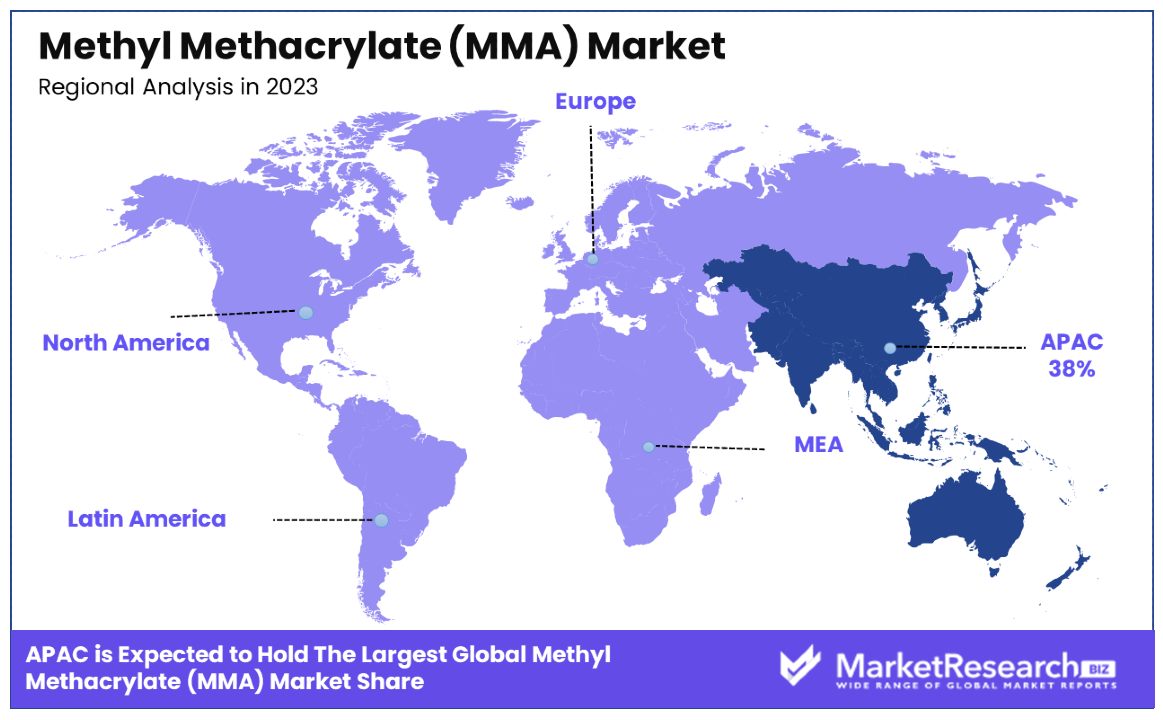

- APAC: Dominates the market with a 38% market share, driven by rapid industrialization, infrastructure development, and increasing demand for advanced materials.

- North America: Holds approximately 24% of the MMA market, reflecting strong demand from diverse industries and technological innovation.

- Analyst Viewpoint: Analysts foresee sustained growth in the MMA market, fueled by expanding applications in construction, automotive, electronics, medical, packaging, aerospace, and other sectors.

- Growth Opportunities: Growth opportunities lie in developing innovative MMA grades tailored to specific industry needs, expanding market presence in emerging regions, and leveraging technological advancements to enhance product performance and sustainability.

Driving Factors

Increasing Demand from the Construction Industry Drives Market Growth

The construction industry significantly influences the Methyl Methacrylate (MMA) market, primarily through the demand for polymethyl methacrylate (PMMA). PMMA's versatility is evident in its use in polymer concrete, building panels, and architectural glazing, vital for modern construction. Emerging economies are pivotal in this growth, with infrastructure development projects rapidly increasing.

For instance, in countries like China and India, urbanization and economic growth spur construction activities, thereby boosting MMA consumption. This demand is reflected in the statistics, showing a marked increase in MMA uptake as aligned with construction booms in these regions. The synergy between MMA's properties and construction needs underpins this sector's profound impact on the overall MMA market.

Rising Applications in Automotive and Transportation Sectors Drives Market Growth

MMA's role in the automotive and transportation sectors is increasingly critical due to its applications in automotive glazing, protective coatings, and lightweight components. The automotive industry's shift towards safety, fuel efficiency, and aesthetic enhancements leverages PMMA's benefits, such as weight reduction and improved performance characteristics.

Lightweight PMMA components contribute to vehicles' fuel efficiency and reduced carbon emissions, aligning with global sustainability goals. For example, the adoption of PMMA in producing lightweight automotive parts has been linked to an approximate 10% improvement in fuel efficiency. This factor's interaction with environmental and economic trends significantly propels MMA market growth.

Expanding Use in Renewable Energy Applications Drives Market Growth

The renewable energy sector, especially solar energy, has become a prominent consumer of MMA-based products. PMMA is integral in manufacturing critical solar panel components like photovoltaic module backsheets and encapsulants. Its excellent optical properties and durability make it ideal for enduring the harsh conditions solar panels face.

As the adoption of solar energy expands globally, the demand for MMA increases correspondingly. This trend is supported by global initiatives toward renewable energy sources, reflecting a compound annual growth rate (CAGR) of approximately 8% in the solar sector, which in turn drives the MMA market. The interaction between MMA's advantageous properties and the burgeoning solar industry exemplifies how renewable energy applications are crucial to MMA's market expansion.

Restraining Factors

Stringent Environmental Regulations Restrain Market Growth

Stringent environmental regulations significantly limit the Methyl Methacrylate (MMA) market's growth. The production and use of MMA involve regulations aimed at minimizing human health and environmental risks. These include controls on emissions, stringent waste management practices, and rigorous product safety standards, which collectively raise operational costs for manufacturers.

For example, the limitations on MMA use in sensitive applications like toys and medical devices restrict market opportunities. These regulations force companies to invest heavily in compliance measures, directly affecting profitability and slowing down innovation in MMA applications, ultimately restraining market expansion.

Competition from Alternative Materials Restrains Market Growth

MMA's market growth is also challenged by competition from alternative materials such as polycarbonates, polyvinyl chloride (PVC), and glass. These materials are often more cost-effective and available, making them attractive to industries that traditionally rely on MMA. For instance, the superior durability and safety of polycarbonates in automotive and aerospace applications can divert demand away from MMA-based products.

Additionally, ongoing advancements in material science continually introduce new substitutes that may offer better properties or lower environmental impacts. This competitive pressure from alternatives not only limits the current demand for MMA but also poses a long-term threat to its market share.

Application Analysis

Chemical Intermediates dominate with 45% due to their critical role in diverse chemical synthesis processes.

The application segment of the Methyl Methacrylate (MMA) Market is diverse, with Chemical Intermediates taking a leading position due to their essential role in producing various chemical compounds. These intermediates are pivotal in synthesizing numerous high-value products in industries such as pharmaceuticals, automotive, and electronics, which rely heavily on advanced chemical processes. This sub-segment's dominance is driven by the increasing demand for performance chemicals in these sectors. For example, MMA-derived intermediates are crucial in producing polymers and resins with specific characteristics required for high-performance applications.

On the other hand, Surface Coatings and Emulsion Polymer represent significant but smaller segments. Surface Coatings utilize MMA for its excellent weather resistance and aesthetic properties, commonly applied in automotive and construction industries. Emulsion Polymers are used in paints, adhesives, and sealants, benefiting from MMA's ability to improve durability and bonding properties. Although these segments are smaller compared to Chemical Intermediates, they contribute substantially to the overall market by fulfilling critical roles in their respective industries, supporting durability and enhancing performance of end products.

Grade Analysis

General Grade MMA dominates with 55% due to its broad utility across multiple industries.

In the Grade segment of the MMA market, General Grade MMA stands out as the predominant sub-segment, widely used due to its versatility and compatibility with numerous applications ranging from plastics manufacturing to coatings. Its dominance is bolstered by its cost-effectiveness and the broad scope of applications in industrial, automotive, and construction sectors, where it is utilized for its strength and clarity.

Optical Grade and Industrial Grade MMA, while smaller in market share, cater to specialized applications that require specific properties. Optical Grade MMA, for example, is essential in high-quality optical applications like lenses and LCD panels due to its superior optical clarity and light transmission characteristics. Industrial Grade MMA is tailored for applications requiring enhanced resistance to harsh chemicals and high temperatures, typical in industrial environments. Although these grades cater to niche markets, their importance is growing as technological advancements and new material requirements emerge in the optics and industrial sectors.

End-Use Industry Analysis

Construction dominates with 40% due to extensive use of MMA in building materials and design innovations.

The End-Use Industry segment of the MMA market is extensively driven by the Construction industry. This sector's substantial share is primarily due to the widespread use of MMA in producing construction materials like PMMA, which is favored for its strength, durability, and aesthetic flexibility. MMA's role in innovative architectural designs—offering light transmission and weather resistance—makes it indispensable in modern construction projects.

Other significant sectors such as Automotive, Electronics, Medical, Packaging, Aerospace, and Others also integrate MMA in various capacities. In Automotive, MMA contributes to manufacturing lightweight and durable components, crucial for fuel efficiency and safety standards. Electronics utilize MMA for components that require high optical clarity and insulation properties. The Medical sector uses MMA in applications where sterility and clarity are vital, such as in surgical devices and implants. Packaging solutions benefit from MMA's durability and clarity, enhancing product safety and shelf appeal. In Aerospace, MMA is used for cabin windows and external panels. These sectors, while not as dominant as Construction, are integral to the MMA market, continuously driving its expansion through diverse and evolving applications.

Key Market Segments

By Application

- Chemical Intermediates

- Surface Coatings

- Emulsion Polymer

By Grade

- General Grade MMA

- Optical Grade MMA

- Industrial Grade MMA

By End-Use Industry

- Construction

- Automotive

- Electronics

- Medical

- Packaging

- Aerospace

- Others

Growth Opportunities

Emerging Applications in 3D Printing and Additive Manufacturing Offer Growth Opportunity

The adoption of MMA-based materials, especially PMMA, in the 3D printing and additive manufacturing sectors opens significant growth avenues for the MMA market. PMMA's qualities such as high transparency, durability, and ease of processing align perfectly with the requirements of advanced 3D printing technologies like stereolithography (SLA) and fused deposition modeling (FDM). These features make it ideal for creating detailed prototypes, complex parts, and robust end-use products across various industries, from automotive to consumer goods.

Companies like Formlabs and Stratasys are increasingly incorporating PMMA-based resins into their offerings, enhancing the utility and adoption of 3D printing solutions. This trend not only broadens the applications of MMA but also drives its market demand, as the 3D printing industry itself is projected to grow significantly, with an expected global market value exceeding $40 billion by 2024.

Increasing Demand from the Healthcare and Medical Sectors Offers Growth Opportunity

The healthcare and medical sectors provide a robust growth opportunity for the MMA market, driven by the increasing use of PMMA in medical applications. PMMA's biocompatibility, superior optical properties, and ease of sterilization make it ideal for manufacturing various medical devices such as dental prosthetics, medical implants, and intraocular lenses.

The demand for these products is surging, propelled by an aging global population and a rise in chronic health conditions that necessitate advanced medical interventions. For instance, companies like Evonik and Arkema are capitalizing on this trend by supplying MMA-based materials for the production of critical medical devices. The medical sector's expanding requirements are expected to significantly boost the MMA market, with the medical polymers market projected to reach billions in the coming years, ensuring a sustained demand for MMA materials.

Trending Factors

Adoption of Advanced Manufacturing Technologies Are Trending Factors

The integration of advanced manufacturing technologies within the MMA industry is a significant trending factor. Technologies like automation, the Internet of Things (IoT), and Industry 4.0 principles are increasingly employed to enhance efficiency, minimize waste, and improve product quality.

For example, Mitsubishi Chemical Corporation utilizes IoT-based systems to optimize operations in their MMA production facilities, leading to better resource management and cost savings. This technological adoption not only streamlines production processes but also aligns with the broader industrial trend towards digital transformation. The incorporation of these advanced technologies is crucial in maintaining competitiveness and addressing the evolving demands of the market, making it a central trend in the industry's growth strategy.

Emphasis on Lightweight and High-Performance Materials Are Trending Factors

The demand for lightweight and high-performance materials is a prevailing trend across multiple industries, influencing the MMA market significantly. MMA-based materials like PMMA are increasingly valued for their excellent strength-to-weight ratios and superior optical and weathering properties. This trend is particularly evident in industries such as automotive, aerospace, and construction, where the reduction of weight is crucial for enhancing fuel efficiency and reducing emissions.

For instance, the automotive industry's shift towards PMMA-based glazing and lightweight components is driven by regulatory pressures to lower carbon footprints and improve vehicle performance. This trend not only supports the growing environmental sustainability movements but also highlights the expanding roles of MMA materials in high-performance applications, affirming their importance in the market's future trajectory.

Regional Analysis

APAC Dominates with 38% Market Share

The Asia-Pacific (APAC) region holds a dominant position in the Methyl Methacrylate (MMA) Market due to several key factors. Firstly, rapid industrialization and urbanization in major economies such as China, India, and South Korea drive substantial demand for MMA in construction and automotive industries. Additionally, the presence of a robust manufacturing base, especially in chemicals and electronics, further fuels the consumption of MMA. High economic growth rates in these countries also contribute to increased investment and development activities, bolstering the demand for MMA-based products.

The dynamics of the APAC region are characterized by a large and growing manufacturing sector, coupled with increasing infrastructural developments. This region benefits from competitive manufacturing costs and favorable government policies, which attract significant foreign investments. The expansion of industries that extensively use MMA, such as electronics and automotive, is particularly notable in this region, underpinning its significant market share.

Regional Market Shares:

- North America: North America holds approximately 24% of the MMA market. The region’s market share is supported by advanced manufacturing sectors and rising demand for high-performance plastics in automotive and electronics.

- Europe: Europe accounts for about 20% of the MMA market. The market is driven by stringent environmental regulations promoting lightweight materials and high-performance polymers in various applications.

- Middle East & Africa: This region has a smaller share of around 8%, but it is growing due to increased investment in infrastructure and the gradual expansion of industrial sectors.

- Latin America: Holding roughly 10% of the market, Latin America is seeing growth in the MMA market driven by its expanding automotive and construction industries.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Methyl Methacrylate (MMA) market is led by several major players. Mitsubishi Chemical Holding Corporation is a key player with strong global operations and a wide range of MMA products, giving them a significant market influence.

Arkema Group is known for its innovative solutions and strong European presence, enhancing its strategic position and market impact.

LG Chem and Lotte Chemical Corp have substantial influence in the Asian market, with robust production capacities and advanced technologies, boosting their market roles.

DowDuPont Inc. combines extensive chemical expertise and a broad product portfolio, positioning them as a major player in the MMA market.

Sumitomo Chemical Company Limited and Sumitomo Chemicals Co., Ltd. are recognized for their strong technological capabilities and global reach, contributing to their significant market influence.

Henkel AG and Permabond LLC focus on high-performance adhesives and sealants, leveraging their expertise to maintain a strong position in the MMA market.

Heilongjiang Zhongmeng Longxin Chemical Co., Ltd. and NIPPON SHOKUBAI CO. are prominent in Asia, known for their production capabilities and market reach.

Lord Corporation and Huntsman Corporation have a strong presence in the industrial and automotive sectors, enhancing their strategic market positions.

Monómeros del Vallés S.L., Kowa India Pvt., and S.K. Panchal and Co. are notable for their regional influence and specialized products.

Overall, these companies drive market dynamics through innovation, strategic global positioning, and extensive production capabilities, shaping the competitive landscape of the MMA market.

Market Key Players

- Huntsman Corporation

- Arkema Group

- Sumitomo Chemical Company Limited

- Heilongjiang Zhongmeng Longxin Chemical Co., Ltd.

- Mitsubishi Chemical Holding Corporation

- Henkel AG &

- Sumitomo Chemicals Co., Ltd.

- Lord Corporation

- LG Chem

- DowDuPont, Inc.

- Monómeros del Vallés S.L.

- Kowa India Pvt.

- NIPPON SHOKUBAI CO.

- S.K. Panchal and Co.

- Permabond LLC

- Lotte Chemical Corp

Recent Developments

- On April 2024, Europe faced a severe shortage of Methyl Methacrylate (MMA) due to limited imports, disruptions in the Red Sea, and manufacturers prioritizing existing contracts. SAME Chemicals emerged as a reliable distributor with available MMA supplies.

- In February 2024, Mitsubishi Chemical America announced plans for a new MMA plant in the US, with a final investment decision expected in the second quarter. The plant, named MCA Geismar Site, is set to produce 350,000 tonnes/year using the Alpha process technology, with a potential start-up in 2028.

- On August 2023, Evonik signed an agreement to supply a custom catalyst for Röhm's new MMA production plant in Texas, USA, scheduled to open in 2024. This plant will utilize the LiMA technology, known for its sustainability advantages and efficient resource use in MMA production.

- Roehm announced a price increase for MMA and methacrylate monomer-based products in the United States, effective November 1, 2023, to address industry challenges. This decision aligns with broader industry trends and reflects the complex dynamics of the methacrylate market, emphasizing the interplay between competition, production costs, and market demand.

Report Scope

Report Features Description Market Value (2023) USD 8.2 Billion Forecast Revenue (2033) USD 14.2 Billion CAGR (2024-2033) 5.8% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Application (Chemical Intermediates, Surface Coatings, Emulsion Polymer), By Grade (General Grade MMA, Optical Grade MMA, Industrial Grade MMA), By End-Use Industry (Construction, Automotive, Electronics, Medical, Packaging, Aerospace, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Huntsman Corporation, Arkema Group, Sumitomo Chemical Company Limited, Heilongjiang Zhongmeng Longxin Chemical Co., Ltd., Mitsubishi Chemical Holding Corporation, Henkel AG &, Sumitomo Chemicals Co., Ltd., Lord Corporation, LG Chem, DowDuPont Inc., Monómeros del Vallés S.L., Kowa India Pvt., NIPPON SHOKUBAI CO., S.K. Panchal and Co., Permabond LLC, Lotte Chemical Corp Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Huntsman Corporation

- Arkema Group

- Sumitomo Chemical Company Limited

- Heilongjiang Zhongmeng Longxin Chemical Co., Ltd.

- Mitsubishi Chemical Holding Corporation

- Henkel AG &

- Sumitomo Chemicals Co., Ltd.

- Lord Corporation

- LG Chem

- DowDuPont, Inc.

- Monómeros del Vallés S.L.

- Kowa India Pvt.

- NIPPON SHOKUBAI CO.

- S.K. Panchal and Co.

- Permabond LLC

- Lotte Chemical Corp

Our Clients

View Our Licence Options