Metallurgical Coke Market By Type (Blast Furnace Coke, Foundry Coke, Others), By Ash Content (Low Ash Content and High Ash Content), By Application (Iron and Steel Production, Non-Ferrous Metal Production, Chemical Industry, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

17345

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

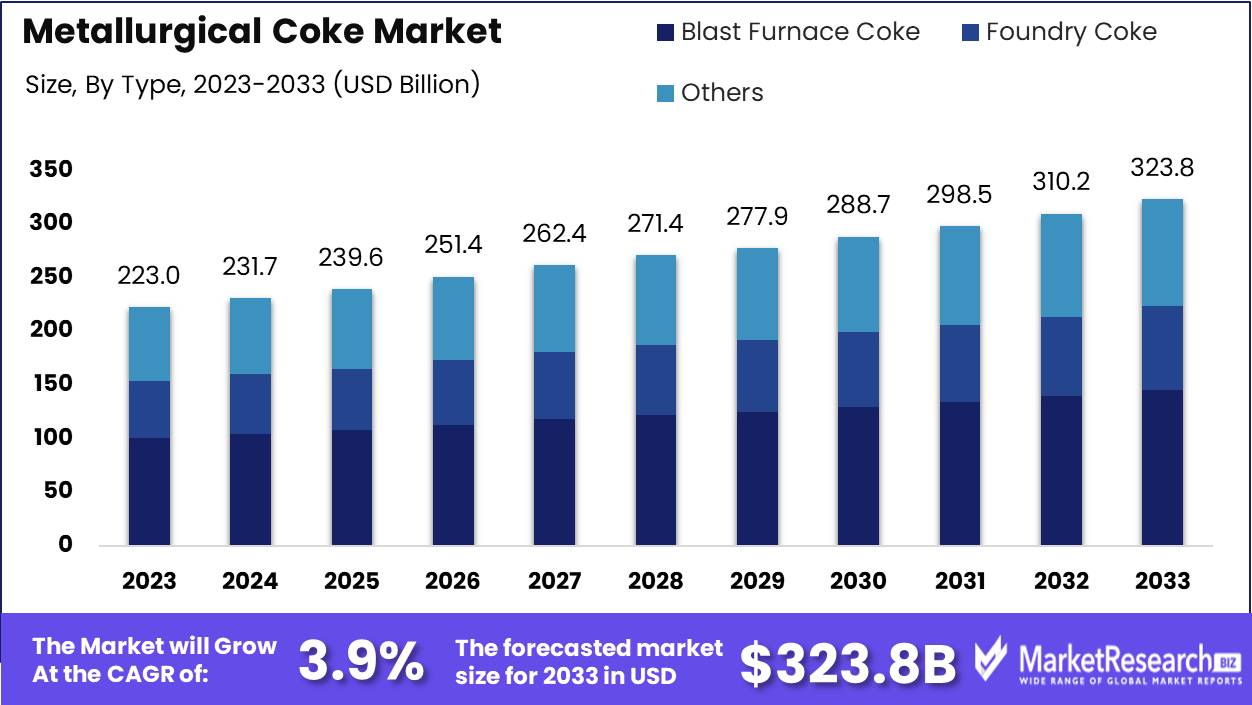

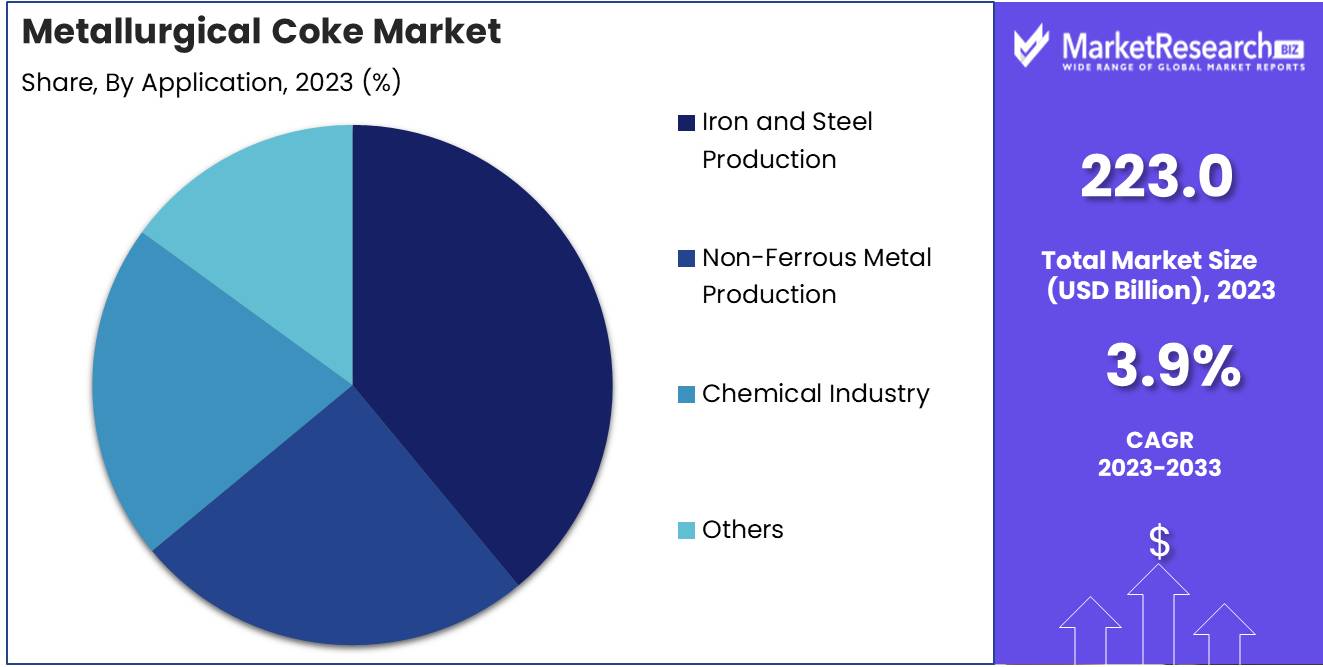

The Metallurgical Coke Market was valued at USD 223.0 billion in 2023. It is expected to reach USD 323.8 billion by 2033, with a CAGR of 3.9% during the forecast period from 2024 to 2033.

The Metallurgical Coke Market encompasses the production, distribution, and consumption of Coke, a vital carbon material derived from coal. This market is integral to the steel industry, as metallurgical coke serves as a key reducing agent and energy source in blast furnaces for iron smelting. The market is influenced by factors such as steel production demand, coal availability, and environmental regulations. Technological advancements and shifts towards sustainable practices are also shaping market dynamics.

The metallurgical coke market is poised for moderate growth over the next decade, underpinned by robust demand across key industries. One of the primary drivers is the rising steel production, which is crucial for the construction, automotive, and manufacturing sectors. The construction industry, particularly in emerging economies, is witnessing unprecedented growth due to extensive infrastructure projects. These developments necessitate a steady supply of steel, thereby increasing the demand for metallurgical coke. The automotive industry, striving to meet the rising consumer demand for vehicles, further amplifies the need for steel and consequently, metallurgical coke. Additionally, manufacturing activities globally are on an upswing, further reinforcing the demand for this essential component in steel production.

However, the industry faces challenges in the form of stringent environmental regulations. Governments worldwide are implementing stricter policies aimed at reducing carbon emissions and promoting cleaner alternatives. These regulations are compelling industries to adopt more sustainable practices, potentially affecting coke production. Despite these challenges, the metallurgical coke market is expected to maintain a steady growth trajectory, driven by the ongoing demand in critical sectors.

The industry's adaptability to evolving regulatory frameworks and advancements in cleaner production technologies will be pivotal in navigating these challenges and sustaining growth. As a result, market players are increasingly investing in research and development to innovate and align with environmental standards, ensuring compliance while meeting the rising demand for steel. This dual approach of adhering to regulations and fulfilling industrial requirements positions the metallurgical Coke market for sustainable growth in the coming years.

Key Takeaways

- Market Growth: The Metallurgical Coke Market was valued at USD 223.0 billion in 2023. It is expected to reach USD 323.8 billion by 2033, with a CAGR of 3.9% during the forecast period from 2024 to 2033.

- By Type: Blast Furnace Coke dominated the Metallurgical Coke Market segment.

- By Ash Content: Low Ash Content Coke dominates due to efficiency and environmental compliance.

- By Application: Iron and Steel Production dominated the Metallurgical Coke Market.

- Regional Dominance: Asia Pacific dominates the Metallurgical Coke Market with a 45% largest share.

- Growth Opportunity: The global metallurgical coke market is set to experience substantial growth in 2024, propelled by the increasing steel production in emerging economies and the rising demand from the glass industry.

Driving factors

Steel & Iron Industry Expansion Fuels Metallurgical Coke Market Growth

The metallurgical coke market is significantly propelled by the robust expansion of the steel and iron industry. Metallurgical coke, primarily used as a reducing agent in the smelting of iron ore in blast furnaces, is integral to steel production. As the steel demand continues to rise globally, driven by sectors such as construction, automotive, and infrastructure development, the need for metallurgical coke correspondingly increases. According to industry reports, the steel industry’s growth rate is projected to reach approximately 3-4% annually, which directly impacts the metallurgical coke market. The upward trend in steel production necessitates a stable and increased supply of metallurgical coke, ensuring its market growth.

Cost Efficiency Drives Demand for Metallurgical Coke

The increasing demand for materials that offer low operating and maintenance costs is another critical driver for the metallurgical coke market. Metallurgical coke is preferred due to its efficiency and cost-effectiveness in the steelmaking process. It reduces the overall energy consumption and operational costs in blast furnaces, making it an economically viable option for steel manufacturers. The emphasis on cost reduction and operational efficiency in the steel industry enhances the attractiveness of metallurgical coke. This trend is particularly significant in regions where steel production costs need to be minimized to maintain competitive pricing in the global market. Consequently, the focus on low operating and maintenance costs contributes to the sustained demand for metallurgical coke.

Technological Advancements in Coke-Making Enhance Market Potential

Improvements in coke-making technologies are crucial in driving the growth of the metallurgical coke market. Innovations such as advanced carbonization techniques and heat recovery systems have led to more efficient and environmentally friendly production processes. These technological advancements have resulted in higher-quality metallurgical coke with improved physical and chemical properties, meeting the stringent requirements of modern steelmaking. Additionally, the adoption of such technologies reduces emissions and enhances energy efficiency, aligning with global environmental regulations and sustainability goals. The integration of cutting-edge coke-making technologies not only boosts production capacity but also ensures a consistent supply of high-quality metallurgical coke, thereby supporting market expansion.

Restraining Factors

Availability of Substitute Coke Materials

The presence of alternative materials poses a significant challenge to the growth of the metallurgical coke market. Substitutes such as pulverized coal injection (PCI), natural gas, and biomass are increasingly being adopted by steel manufacturers due to their cost-effectiveness and reduced environmental impact. Pulverized coal injection, for instance, allows for a reduction in coke consumption, thereby decreasing the reliance on metallurgical coke. This shift is driven by both economic and regulatory incentives, as companies seek to lower production costs and adhere to stricter environmental standards. The increasing adoption of these substitutes is expected to limit the growth of the metallurgical coke market, as they provide a viable and often more sustainable alternative to traditional coke.

Environmental Concerns and Regulations

Environmental concerns and stringent regulations significantly restrain the growth of the metallurgical coke market. The production of metallurgical coke is associated with the release of various pollutants, including sulfur dioxide (SO2), nitrogen oxides (NOx), and particulate matter, which contribute to air pollution and pose health risks. Governments and environmental agencies worldwide are implementing stringent regulations to curb emissions from industrial processes, including coke production. Compliance with these regulations often requires substantial investment in pollution control technologies, increasing operational costs for coke manufacturers.

By Type Analysis

In 2023, Blast Furnace Coke dominated the Metallurgical Coke Market segment.

In 2023, Blast Furnace Coke held a dominant market position in the By Type segment of the Metallurgical Coke Market. Blast Furnace Coke is the most critical type due to its extensive use in the steelmaking process. Its high carbon content and physical strength make it essential for maintaining furnace stability and efficiency, thereby driving its substantial demand in the market.

Foundry Coke, on the other hand, is utilized primarily in foundries for casting iron and steel, contributing to the market's growth through its unique properties that improve molten metal quality. The Others category encompasses smaller segments such as domestic coke and other specialized types used in various industrial processes.

The dominance of Blast Furnace Coke is attributed to its vital role in the production of high-quality steel, which is indispensable for the construction, automotive, and infrastructure industries. The continuous advancements in steel production technologies and the increasing global demand for steel are expected to further bolster the growth of the Blast Furnace Coke segment.

By Ash Content Analysis

Low Ash Content Coke dominates due to efficiency and environmental compliance.

In 2023, Low Ash Content held a dominant market position in the By Ash Content segment of the Metallurgical Coke Market. Low Ash Content metallurgical coke is highly preferred in the steel manufacturing industry due to its superior performance in blast furnaces. This type of coke enhances the efficiency of the steel production process by reducing impurities and improving the quality of the final product. The demand for low ash-content coke is driven by stringent environmental regulations and the need for high-quality steel, which necessitates the use of cleaner coke with minimal impurities. Major steel-producing regions such as Asia Pacific, particularly China, and India, have significantly contributed to the growth of this segment, given their robust industrial activities and increasing investments in steel production infrastructure.

On the other hand, high-content Coke, while less favored, still holds a significant share in the market, particularly in regions where cost considerations outweigh performance criteria. High ash content coke is often utilized in applications where the quality of the final product is less critical, or where budget constraints limit the use of premium materials. This type of coke is more abundant and cheaper to produce, making it a viable option for smaller steel plants or secondary metallurgical processes. However, its usage is expected to decline gradually as industries move towards more sustainable and efficient production practices, aligning with global environmental standards and the increasing emphasis on reducing carbon footprints in industrial operations.

By Application Analysis

In 2023, Iron and Steel Production dominated the Metallurgical Coke Market.

In 2023, Iron and Steel Production held a dominant market position in the By Application segment of the Metallurgical Coke Market. This sector accounted for a significant share, driven by the continuous demand for high-quality steel in various industries, including construction, automotive, and manufacturing. The iron and steel production segment relies heavily on metallurgical coke for its role as a reducing agent and source of energy in blast furnaces, enhancing efficiency and output quality.

Non-ferrous metal Production, although not as dominant, also contributed substantially due to the rising demand for non-ferrous metals such as aluminum and copper, which require coke for smelting processes. The Chemical Industry utilized metallurgical coke in producing calcium carbide and other chemicals, marking its importance in the market.

Lastly, the 'Others' category, encompassing applications such as foundries and ferroalloy production, added to the market's overall dynamics. The broad application spectrum of metallurgical coke underscores its critical role in supporting various industrial processes, ensuring its sustained demand and market relevance.

Key Market Segments

By Type

- Blast Furnace Coke

- Foundry Coke

- Others

By Ash Content

- Low Ash Content

- High Ash Content

By Application

- Iron and Steel Production

- Non-Ferrous Metal Production

- Chemical Industry

- Others

Growth Opportunity

Increasing Steel Production in Emerging Economies

The global metallurgical coke market is poised for significant growth, driven predominantly by the surge in steel production within emerging economies. Countries such as India, China, and Brazil are expanding their industrial capabilities, thereby increasing the demand for high-quality coke. The steel industry, being the largest consumer of metallurgical coke, accounts for over 70% of its total usage. As these economies invest in infrastructure projects, the need for steel and consequently metallurgical coke will rise. According to the report, global steel production is expected to grow by 3%, with emerging economies contributing a substantial portion to this increase. This trend is anticipated to create robust growth opportunities for metallurgical coke manufacturers, as the supply chain for steel production intensifies.

Rising Demand from the Glass Industry

Another pivotal factor contributing to the expansion of the metallurgical coke market is the rising demand from the glass industry. Metallurgical coke is essential in the production of glass, serving as a source of carbon. The glass industry, particularly in regions like North America and Europe, is witnessing an uptick in demand due to the growing applications of glass in construction, automotive, and consumer goods. The global glass market is projected to grow by 5%, further amplifying the demand for metallurgical coke. This growth is fueled by increased consumer preference for sustainable and recyclable materials, where glass plays a crucial role. The synergy between the metallurgical coke and glass industries presents a promising avenue for market expansion, offering manufacturers an opportunity to diversify their customer base and stabilize revenue streams.

Latest Trends

Growing Demand from the Steel Industry

The steel industry, being one of the largest consumers of metallurgical coke, is set to significantly influence the market. With global steel production projected to rise, the demand for high-quality coke is expected to follow suit. This growth can be attributed to the expanding infrastructure projects and the automotive sector's resurgence. Emerging economies, particularly in Asia Pacific, are witnessing a robust steel demand, driven by urbanization and industrialization efforts. Consequently, metallurgical coke producers are likely to benefit from this trend, ensuring a steady supply to meet the burgeoning needs of steel manufacturers.

Rise in Construction Projects

The construction sector is poised for substantial growth further propelling the metallurgical coke market. As nations invest in rebuilding and expanding their infrastructure, the need for steel and by extension, metallurgical coke is anticipated to surge. Major construction projects, including residential, commercial, and industrial developments, are underway across various regions. This uptick in construction activities not only boosts the steel demand but also underscores the critical role of metallurgical coke in the steel production process. Governments' focus on sustainable and resilient infrastructure development will likely sustain this demand, driving market growth.

Regional Analysis

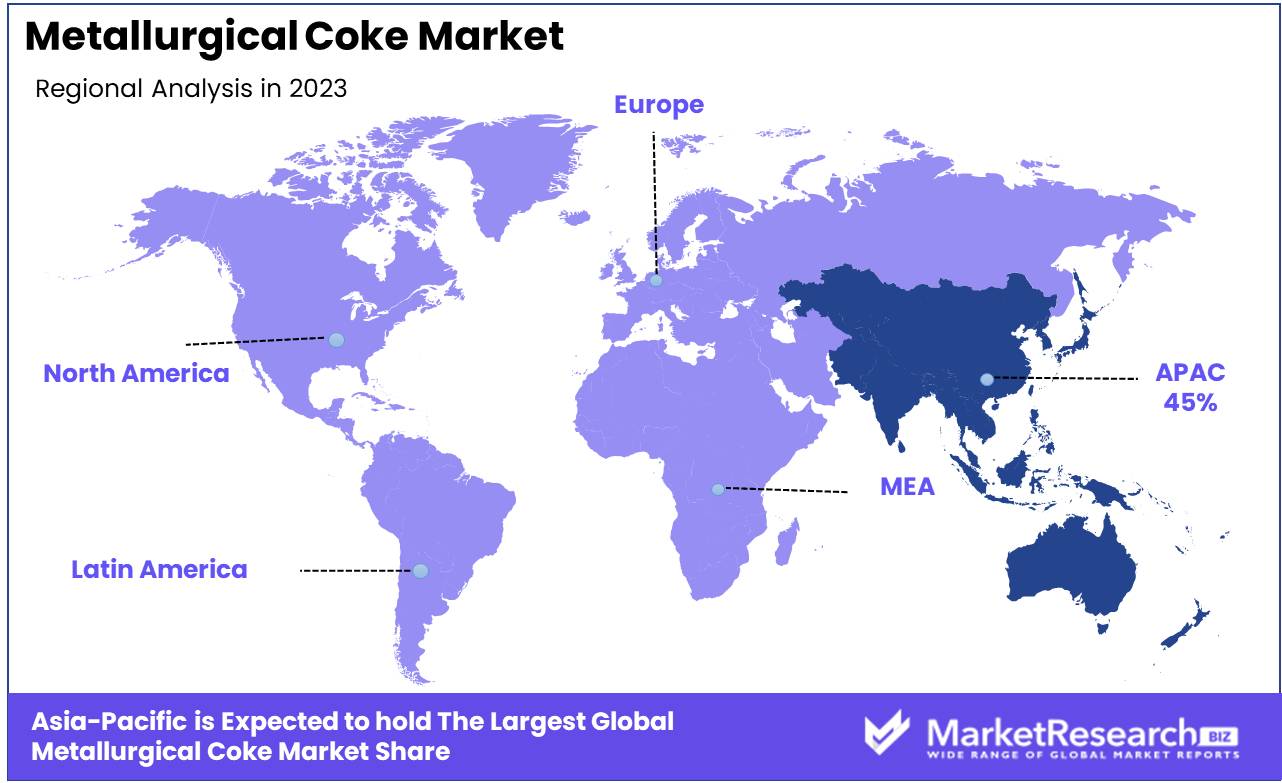

Asia Pacific dominates the Metallurgical Coke Market with a 45% share.

The Metallurgical Coke Market is segmented across several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. In North America, the market is driven by the robust steel production sector, with the United States and Canada being significant contributors. The region accounted for approximately 18% of the global market share in 2023. Europe follows closely, with countries such as Germany and the UK leading due to their advanced metallurgical industries, capturing around 22% of the market share.

Asia Pacific stands as the dominant region, commanding the largest market share of about 45% in 2023. This dominance is primarily attributed to China's substantial steel manufacturing capacity, along with significant contributions from India and Japan. The region's rapid industrialization and urbanization have further propelled demand. The Middle East & Africa region is witnessing moderate growth, supported by emerging industrial sectors in countries like South Africa and the UAE, accounting for around 8% of the market. Latin America, with Brazil and Mexico as key players, holds approximately 7% of the market share, driven by the development of their steel industries.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Metallurgical Coke Market is poised for significant advancements, driven by key industry players who continue to shape the market dynamics. ArcelorMittal remains a dominant force, leveraging its extensive global footprint and technological innovations to maintain a competitive edge. BlueScope Steel is expected to enhance its market position through strategic expansions and improved production efficiencies.

CHINA SHENHUA, as a major player in the coal and coke industry, is anticipated to capitalize on its integrated operations, ensuring a steady supply of high-quality metallurgical coke. ECL and GNCL are set to contribute significantly through their robust distribution networks and customer-centric approaches.

Baosteel Group, with its substantial production capacity and commitment to sustainability, is likely to remain a key influencer in the market. Hickman Williams & Company, known for its tailored solutions, is expected to strengthen its market presence by focusing on niche markets.

Jastrzębska Społka Weglowa (JSW) and Mechel are projected to benefit from their strategic locations and strong logistical capabilities. Nippon Steel Corporation's innovation-driven approach and OKK Koksovny, a.s.'s focus on high-quality production is anticipated to drive growth.

SunCoke Energy Inc. and POSCO are expected to leverage their technological advancements to enhance product quality and reduce environmental impact. Tata Steel and JSW's extensive market reach and continuous R&D investments are likely to sustain their competitive positions.

Market Key Players

- ArcelorMittal

- BlueScope Steel

- CHINA SHENHUA

- ECL

- GNCL

- Baosteel Group

- Hickman Williams & Company

- Jastrzębska Społka Weglowa (JSW)

- Mechel

- Nippon Steel Corporation

- OKK Koksovny, a.s.

- SunCoke Energy Inc.

- POSCO

- Tata Steel

- JSW

Recent Development

- In March 2024, ArcelorMittal, a leading global steel and mining company, announced a strategic partnership with a leading technology provider to enhance its metallurgical coke production capabilities. This partnership aims to integrate advanced carbon capture technologies, improving both efficiency and environmental sustainability.

- In January 2024, SunCoke Energy Inc. launched a new sustainability initiative aimed at reducing the carbon footprint of its metallurgical coke production. This initiative includes significant investments in renewable energy sources and the adoption of more energy-efficient technologies in their production processes.

- In February 2024, JSW Steel, a major Indian steel producer, completed a significant expansion of its coke production capacity. The expansion includes the addition of a new coke oven battery, increasing their production capacity by 1 million metric tons per year. This move is part of JSW Steel’s broader strategy to increase its steel production capabilities.

Report Scope

Report Features Description Market Value (2023) USD 223.0 Billion Forecast Revenue (2033) USD 323.8 Billion CAGR (2024-2032) 3.9% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Blast Furnace Coke, Foundry Coke, Others), By Ash Content (Low Ash Content and High Ash Content), By Application (Iron and Steel Production, Non-Ferrous Metal Production, Chemical Industry, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape ArcelorMittal, Bluescope Steel, CHINA SHENHUA, ECL, GNCL, Baosteel Group, Hickman Williams & Company, Jastrzębska Społka Weglowa (JSW), Mechel, Nippon Steel Corporation, OKK Koksovny, a.s., SunCoke Energy Inc., POSCO, Tata Steel, JSW Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- ArcelorMittal

- BlueScope Steel

- CHINA SHENHUA

- ECL

- GNCL

- Baosteel Group

- Hickman Williams & Company

- Jastrzębska Społka Weglowa (JSW)

- Mechel

- Nippon Steel Corporation

- OKK Koksovny, a.s.

- SunCoke Energy Inc.

- POSCO

- Tata Steel

- JSW

Our Clients

View Our Licence Options