Metal Stamping Market Based on Process (Blanking, Embossing, Bending, Other Process), Based on End-Use (Automotive, Aerospace, Consumer Electronics, Industrial Machinery, Other End-Uses), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

5252

-

May 2024

-

300

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

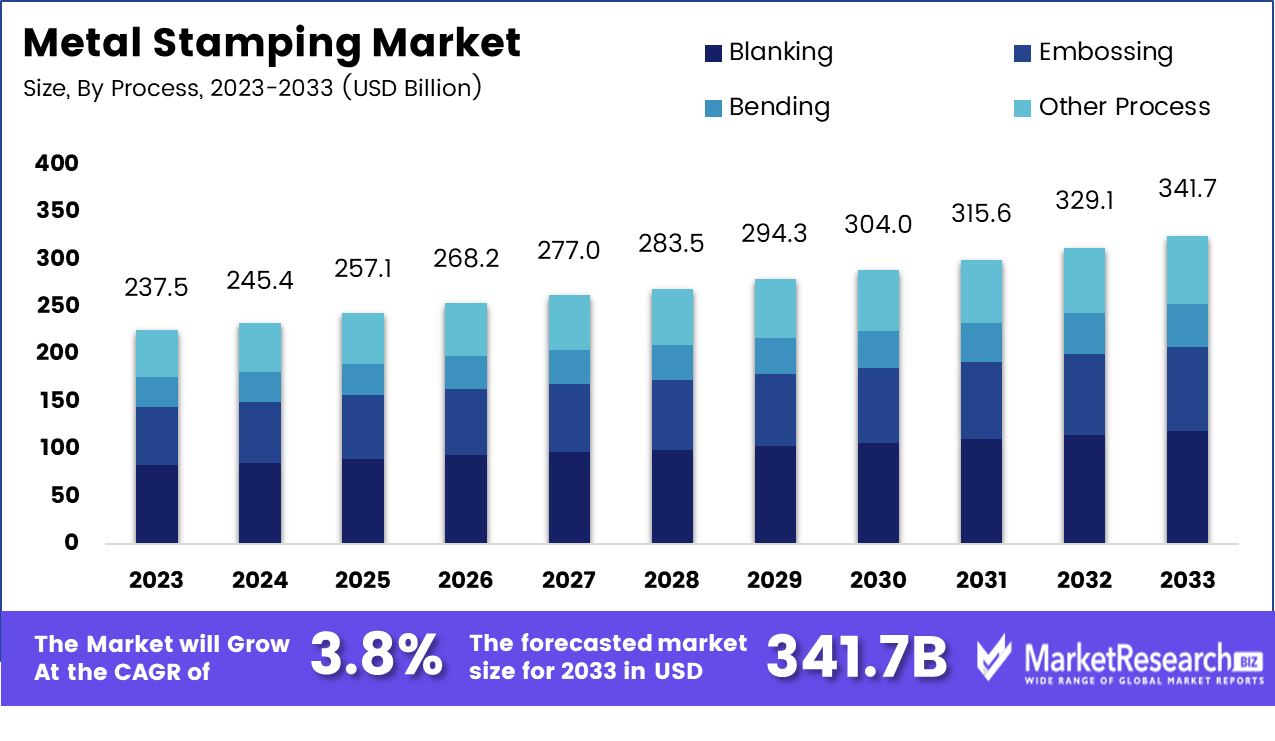

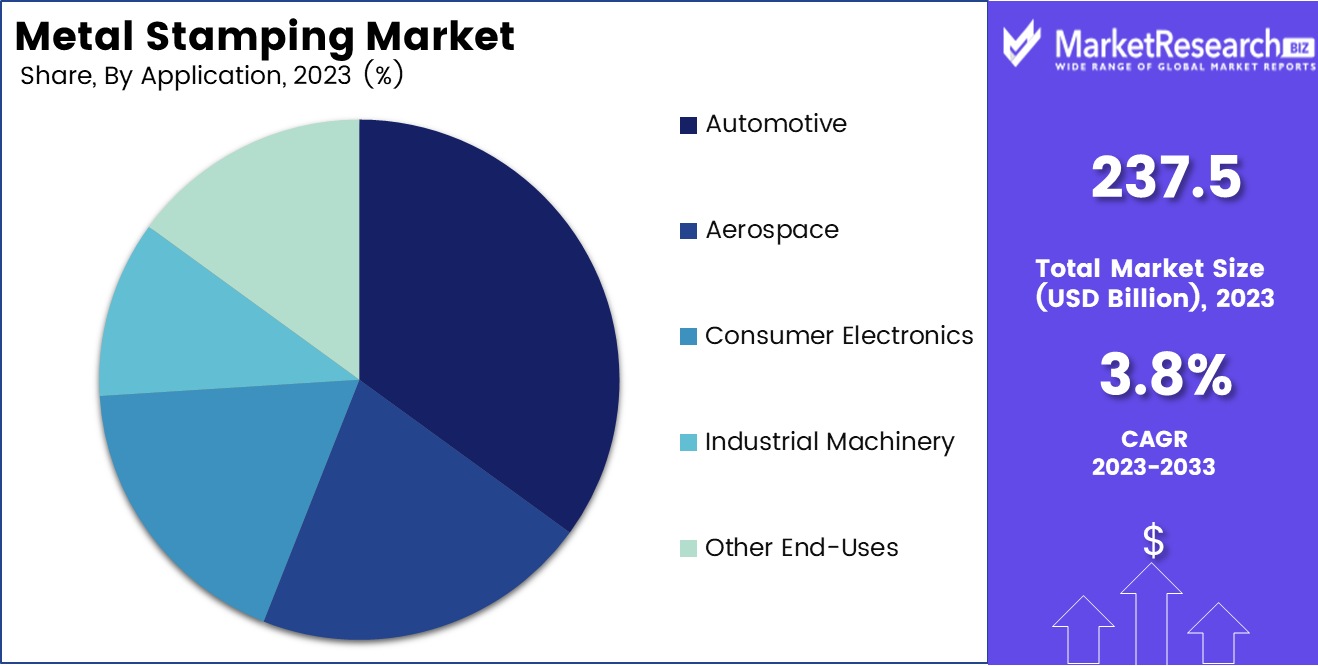

The Metal Stamping Market size is expected to be worth around USD 341.7 Bn by 2033 from USD 237.5 Bn in 2023, growing at a CAGR of 3.8% during the forecast period from 2024 to 2033.

The surge in demand for various applications and advanced technologies are some of the main driving factors for the metal stamping market expansion. Metal stamping is a versatile and efficient manufacturing process that takes flat metal coils and changes them into a précised shape and convoluted parts. This method is less costly and produces higher lead times which is beneficial for both short and long productions while maintaining the quality and accuracy of the manufactured products. There are several types of metal stamping such as mechanical presses, hydraulic presses, and servo presses.

Metal stamping is widely used in the electronic industry. Metal pressing is known for its high efficiency and cost-effectiveness; it has become one of the integral parts of the electronic as it offers unique precision for the intricate parts of electronic devices. Due to technological advances, metal stamping uses innovative methods and materials that ensure its position as an unreplaceable tool in the electronic manufacturing industry. Beyond its speed and efficiency, metal stamping provides substantial labor competencies. Automated stamping presses require minimal human interference which decreases the need for manual labor.

Metal stamping is widely used in the electronic industry. Metal pressing is known for its high efficiency and cost-effectiveness; it has become one of the integral parts of the electronic as it offers unique precision for the intricate parts of electronic devices. Due to technological advances, metal stamping uses innovative methods and materials that ensure its position as an unreplaceable tool in the electronic manufacturing industry. Beyond its speed and efficiency, metal stamping provides substantial labor competencies. Automated stamping presses require minimal human interference which decreases the need for manual labor.The automated stamping presses make sure of an unswerving production quality, which is free from human error. For example, ElectroWaves Solutions is a well-known firm for its wireless communication devices. They adopted the metal stamping method for generating electromagnetic shields. This process gave an enhanced device performance that led to a 15% surge in customer satisfaction rates. Moreover, NanoTech components used the precision of the metal stamping process to generate ultra-thin depots for their next-generation chips. The results were a product line that was not only more consistent but also more market competitive.

Metal stamping is a commonly used technique that has significant applications in daily life. There are several advantages of metal stamping such as it provides a high production rate, decreases labor, and maintains efficiency and costs. Metal stampings have intricate connectors that have the power to create electromagnetic shields that make sure to provide high device performance. The advanced technologies that are used in the metal stamping process will increase the demand in the coming years and will help in market expansion.

In recent years, there have been a lot of groundbreaking innovations in the metal stamping industry. These include the use of cutting-edge software for design and simulation, additive manufacturing techniques, and the introduction of robotics into the mix. The combination of these first-of-its-kind improvements has made the metal pressing process much more efficient and accurate, which has led to a decrease in production time and costs.

Key Takeaways

- Market Value: Metal Stamping Market size is expected to be worth around USD 341.7 Bn by 2033 from USD 237.5 Bn in 2023, growing at a CAGR of 3.8% during the forecast period from 2024 to 2033.

- Based on Process: The metal stamping market grows as demand for process blanking increases.

- Based on Application: The automotive sector drives robust growth in the metal stamping market.

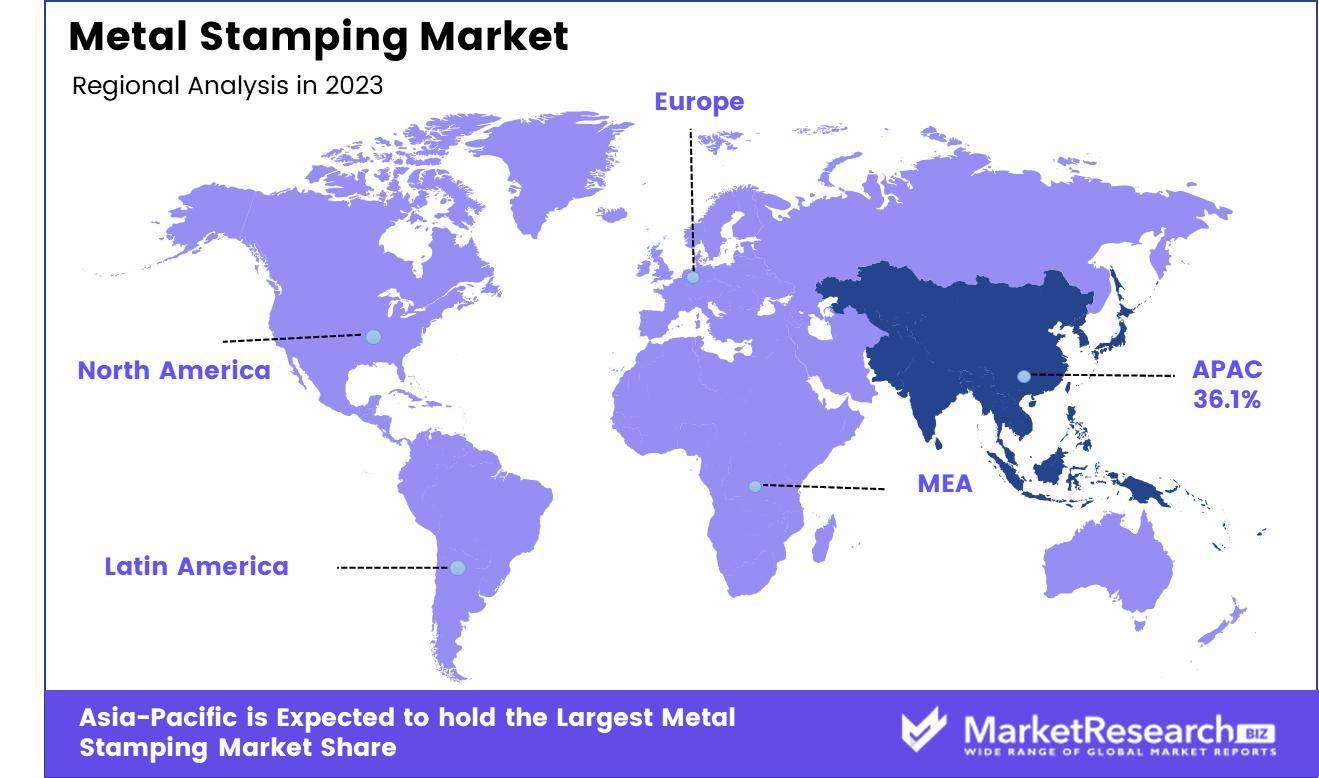

- Regional Analysis: Asia-Pacific dominates with a 36.1% share in the metal stamping market.

- Growth Opportunity: In 2023, the global metal stamping market is poised for growth through technological innovations and strategic partnerships, enhancing efficiency, precision, and market reach.

Driving factors

Rising Automotive Manufacturing: Catalyst for Robust Growth in Metal Stamping

The surge in automotive manufacturing globally acts as a primary driver for the metal stamping market. As vehicle production scales, the demand for precision-stamped metal parts—critical in car frames, engines, and assemblies—intensifies. This sector's growth is directly correlated with the proliferation of new automotive technologies and the increasing adoption of electric vehicles, which rely heavily on intricately stamped components for both structural and aesthetic purposes. The precision and cost-effectiveness of metal stamping make it indispensable in meeting the automotive industry's rigorous standards and production volumes.

Diverse Industrial Applications: Expanding Metal Stamping Frontiers

The application of metal stamping across various industries—including construction, medical, and automotive—significantly boosts its market demand. In construction, metal stamping is crucial for creating durable components used in heavy machinery and structural elements. The medical sector relies on stamped metal parts for surgical instruments and medical devices, where precision and reliability are paramount. By serving multiple industries, metal stamping benefits from diversified revenue streams and reduced market volatility, thus stabilizing its growth trajectory.

Commitment to Sustainability: Strengthening Market Position Through Eco-Friendly Practices

The focus on green production and sustainable practices in engineering has become a pivotal aspect of the metal stamping market. Manufacturers are increasingly adopting eco-friendly production techniques to reduce waste and energy consumption. This shift not only aligns with global environmental regulations but also appeals to a broader base of consumers and businesses looking to fulfill their corporate social responsibility. The emphasis on sustainability helps companies in the metal stamping market differentiate themselves and tap into new, eco-conscious customer segments, further driving market growth.

Restraining Factors

Fluctuating Raw Material Prices: A Volatility Challenge for the Metal Stamping Market

The metal stamping market is notably sensitive to fluctuations in raw material prices, primarily steel and aluminum, which are integral to the production process. Such volatility can lead to inconsistent production costs and uncertainty in pricing strategies for metal stamping manufacturers. When metal prices spike, the increased costs can compress profit margins unless companies pass these costs onto their customers, potentially reducing market competitiveness and demand. On the flip side, sudden drops in material costs, while beneficial in the short term, can lead to market instability and disrupt long-term planning. This economic unpredictability is a significant restraint, discouraging investment in new stamping technologies and capacity expansions, thus potentially stifling market growth.

Technological Limitations in Stamping Complexity: Constraining Market Expansion

Conventional metal stamping processes face inherent limitations in producing parts with complex features or interior cavities. This technical constraint restricts the application scope of metal stamping in industries that require intricate component designs, such as aerospace and high-tech electronics, where precision and innovation are crucial. As a result, these sectors often turn to alternative manufacturing technologies like CNC machining or additive manufacturing (3D printing), which can handle complex geometries more effectively. The inability of traditional stamping processes to evolve rapidly in terms of complexity management not only limits market penetration in high-value sectors but also curtails potential revenue streams, hindering overall market growth in the expanding advanced manufacturing landscape.

Process Analysis

The metal stamping market thrives on process blanking, enhancing precision and efficiency in component fabrication.

In 2023, Blanking held a dominant market position in the process-based segmentation of the Metal Stamping Market. As a critical foundational step in metal fabrication, blanking—the process of cutting larger sheet metal into more manageable pieces—has proven indispensable across various industries, including automotive, aerospace, and consumer electronics.

The supremacy of the blanking segment is largely attributed to its high efficiency and precision in producing consistent, high-volume parts. Blanking not only ensures a high degree of dimensional accuracy but also supports complex geometries and tight tolerances that are essential in advanced manufacturing sectors. This process is particularly valued in the automotive sector where the demand for intricate components with robust performance characteristics is escalating. As vehicles incorporate more sophisticated electronic systems, the need for precisely stamped parts, which blanking can reliably produce, becomes increasingly critical.

Furthermore, advancements in automation and press technology have enhanced the blanking process, making it more cost-effective and less labor-intensive. This technological evolution has expanded the capacity of manufacturers to meet growing market demands without compromising quality. The integration of computer-aided design (CAD) and computer-aided manufacturing (CAM) systems has further refined the blanking process, allowing for quicker setup times and lower material wastage, thereby improving overall operational efficiency.

Application Analysis

Automotive sector drives robust growth in the metal stamping market, leveraging advanced manufacturing techniques.

In 2023, Automotive held a dominant market position in the application-based segment of the Metal Stamping Market. This prominence is rooted in the extensive use of metal stamping in the production of automotive components, which are critical for vehicle assembly. Metal stamping processes such as blanking, embossing, and bending are integral to forming parts that meet the strict safety, durability, and precision requirements of the automotive industry.

The growth in the generative AI in the automotive sector's reliance on metal stamping is driven by the ongoing evolution in vehicle design and the increasing incorporation of lightweight materials to enhance fuel efficiency and reduce emissions. This has expanded the use of high-strength, lightweight alloys that require precise stamping techniques to maintain structural integrity and performance under the rigors of automotive use.

Additionally, the push towards electric cars (EVs) has further bolstered the metal stamping market within the automotive industry. EVs require more intricate and lightweight metal parts to optimize battery efficiency and range. As such, the demand for advanced stamping solutions capable of handling novel materials and complex designs is on the rise.

Technological advancements in stamping equipment, such as the integration of automation and improved die technologies, have also supported the automotive sector's dominant position in the market. These innovations allow for faster production times, higher quality outputs, and lower manufacturing costs, aligning with the automotive industry's goals of enhancing efficiency and reducing overheads.

Key Market Segments

Based on Process

- Blanking

- Embossing

- Bending

- Other Process

Based on Application

- Automotive

- Aerospace

- Consumer Electronics

- Industrial Machinery

- Other End-Uses

Growth Opportunity

Technological Innovation: Spearheading Market Expansion

The global metal stamping market stands on the brink of transformation in 2023, largely fueled by technological advances. Innovations such as high-speed stamping, automation, and integration of AI for precision control are set to redefine product quality and operational efficiency. These technological enhancements not only mitigate the challenges of complex part production but also significantly reduce waste and operational costs.

By embracing these advanced technologies, manufacturers can cater to the intricate design requirements of high-tech industries, thereby broadening their market reach and enhancing competitiveness. This focus on superior technology is expected to attract investment and drive substantial growth in sectors demanding higher precision and efficiency.

Strategic Partnerships: Expanding Horizons

Another significant opportunity in 2023 for the metal stamping market is the strategic focus on partnerships and collaborations. By aligning with peers and technology providers, companies can leverage shared expertise, technology transfer, and expanded production capabilities. This strategy is particularly potent in tapping into new geographical markets and sectors where local expertise and presence are crucial.

Collaborations can also facilitate entry into niche markets such as renewable energy components, where specialized stamping techniques are required. These partnerships not only diversify the product portfolio but also stabilize supply chains and enhance the adaptability of businesses to changing market conditions. Overall, by prioritizing technological innovation and strategic partnerships, the metal stamping market is well-positioned to capitalize on the expanding array of applications and global market demands in 2023.

Latest Trends

Embracing Lightweight Materials: Advancing Sustainability and Efficiency

A prominent trend within the 2023 metal stamping market is the shift towards lightweight materials, such as aluminum and advanced high-strength steel. This transition is driven by the growing demand for fuel efficiency and sustainability in the automotive industry, where lightweight metals contribute significantly to reduced vehicle weight and improved performance. Additionally, these materials offer enhanced structural integrity, which is crucial in safety-critical applications across various industries, including aerospace and consumer electronics.

By incorporating these advanced materials, metal stamping companies not only meet stricter environmental standards but also deliver higher-quality, durable products. This trend is expected to continue shaping the market dynamics, fostering innovation, and opening new opportunities in lightweight design applications.

Leveraging Industry 4.0: Transforming Production Landscapes

The integration of Industry 4.0 technologies marks another significant trend in the metal stamping sector for 2023. Technologies such as the Internet of Things (IoT), data analytics, and real-time monitoring systems are increasingly being adopted to enhance production efficiency and operational reliability. These technological advancements enable manufacturers to optimize stamping processes, reduce downtime, and predict maintenance needs, thereby minimizing operational costs and enhancing product quality.

The ability to monitor and analyze production in real time supports continuous improvement and helps companies maintain a competitive edge in a fast-evolving market. This strategic adoption of Industry 4.0 not only boosts productivity but also aligns with the push towards smart manufacturing and digital transformation in the industrial sector.

Regional Analysis

Asia-Pacific dominates with a 36.1% share in the global metal stamping market, showcasing significant growth.

In the global metal stamping market, Asia-Pacific is the leading region with a substantial 36.1% revenue share, driven primarily by robust industrial activities in China and India. The region benefits from strong growth in the automotive and electronics sectors, where metal stamping is crucial for component manufacturing.

North America follows as a significant player in the market, holding a dominant position due to its advanced manufacturing infrastructure and historical prowess in the automotive and aerospace industries. The region's emphasis on innovative manufacturing technologies and high-quality standards in production has solidified its role as a hub for metal stamping, particularly in the U.S., which hosts a dense network of suppliers and manufacturers.

Europe maintains a competitive stance in the metal stamping market, with a focus on the automotive sector and a growing demand for consumer electronics. The region's stringent environmental and quality regulations drive the need for high-precision metal stamping solutions, supporting a sophisticated manufacturing landscape.

The Middle East & Africa, though smaller in market size compared to other regions, is gradually expanding its metal stamping capabilities, with investments flowing into automotive and construction projects that demand stamped metal parts. This region is seeing increased activity due to infrastructural developments and an evolving industrial base.

Latin America, with its emerging economies, is witnessing growth in metal stamping driven by the automotive sector. The region is leveraging its cost-competitive labor market and growing local demand to attract investments from global automotive manufacturers, thereby enhancing its metal stamping industry.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

As we move into 2023, the global metal stamping market continues to be influenced significantly by key players such as CIE Automotive SA, Tower International, Inc., Shiloh Industries, Inc., Interplex Holdings Ltd., Oberg Industries LLC, Suzhou Cheersson Precision Metal Forming Co. Ltd., Clow Stamping Company Inc., Kapco Inc., Kenmode Tool & Engineering Inc., and Manor Tool & Manufacturing. These companies represent a diverse cross-section of the industry, each bringing unique strengths to the market.

CIE Automotive SA is renowned for its integrated approach to manufacturing, leveraging advanced technologies to produce high-precision metal components for the automotive industry. Their global footprint and commitment to sustainability position them as a leader in adapting to the evolving demands of the automotive sector.

Tower International, Inc., with its focus on complex metal structures for automotive applications, continues to drive innovation in lightweight materials and safety components, enhancing its competitiveness in the North American and European markets.

Shiloh Industries, Inc. is pivotal in promoting environmentally friendly manufacturing processes and products. Their expertise in lightweight solutions aligns with the global automotive industry's shift towards more fuel-efficient vehicles.

Interplex Holdings Ltd., known for its precision engineering capabilities, caters to the electronics and automotive industries, offering customized solutions that enhance the reliability and performance of metal-stamped parts.

Oberg Industries LLC and Suzhou Cheersson Precision Metal Forming Co. Ltd. focus on high-precision metal stamping and tooling solutions, crucial for the demanding specifications of the electronics and consumer goods industries.

Clow Stamping Company Inc. and Kapco Inc. are significant contributors to the North American market, with a strong emphasis on quality and service in heavy gauge stamping for industrial applications.

Kenmode Tool & Engineering Inc. and Manor Tool & Manufacturing excel in providing comprehensive metal stamping services from prototyping to production, supporting industries ranging from automotive to healthcare with their high-quality standards and innovative techniques.

Top Key Players in Metal Stamping Market

- CIE Automotive SA

- Tower International, Inc.

- Shiloh Industries, Inc.

- Interplex Holdings Ltd.

- Oberg Industries LLc

- Suzhou Cheersson Precision Metal Forming Co. Ltd.

- Clow Stamping Company Inc.

- Kapco Inc.

- Kenmode Tool & Engineering Inc.

- Manor Tool & Manufacturing.

Recent Development

- In February 2024, Spanish supplier Gestamp is set to construct a 460,000-square-foot facility in Chesterfield Township, which will supply parts to GM's Orion Assembly plant.

- In March 2024, Ge-Shen Corp Bhd, a plastic injection molding and metal stamping company, received a query from Bursa Malaysia regarding unusual market activity after its share price surged 24.3% following its announcement of acquiring a 60% stake in both Amity Research & Development Sdn Bhd and Amity Technical Services & Consultancy (M) Sdn Bhd to strengthen its presence in the E&E sector.

- In December 2023, Generation Growth Capital established American Consolidated Metals, a new metal manufacturing platform in the U.S. upper Midwest, integrating three acquired companies—Federal Tool & Engineering, BP Metals, and Rockford Specialties—to enhance manufacturing capabilities and market reach.

- In November 2023, Arconic Corporation completed the sale of its Russian operations to Promyshlennye Investitsii LLC. Arconic is an American company that manufactures aluminum and titanium products. The sale of its Russian operations was necessary due to the sanctions imposed on Russia by the United States and other countries.

- In January 2023, Interplex Holdings Pte. Ltd. acquired OCP Group, Inc. OCP Group is a custom connector and cable assembly company. This acquisition will help Interplex to expand its product offerings and reach new markets.

Report Scope

Report Features Description Market Value (2023) USD 237.5 Bn Forecast Revenue (2033) USD 341.7 Bn CAGR (2024-2033) 3.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered Based on Process(Blanking, Embossing, Bending, Other Process), Based on End-Use(Automotive, Aerospace, Consumer Electronics, Industrial Machinery, Other End-Uses) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Norbord Inc., Kronospan Limited, West Fraser Timber Co. Ltd., Timber Products Company, Weyerhaeuser Company, Georgia-Pacific LLC, Bucina DDD, spol. s r.o. (Ltd.), Sonae Indústria, Freres Lumber Co., Inc., Dongwha Enterprise Co., Ltd., Kastamonu Entegre, Hampton Affiliates, Duratex Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- CIE Automotive SA

- Tower International, Inc.

- Shiloh Industries, Inc.

- Interplex Holdings Ltd.

- Oberg Industries LLc

- Suzhou Cheersson Precision Metal Forming Co. Ltd.

- Clow Stamping Company Inc.

- Kapco Inc.

- Kenmode Tool & Engineering Inc.

- Manor Tool & Manufacturing.

Our Clients

View Our Licence Options