MEK Inhibitors Market By Type (MEKINIST, COTELLIC, MEKTOVI), By End-Users (Clinic, Hospital, Others), By Application (NSCLC, Cancer), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

45814

-

April 2024

-

136

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

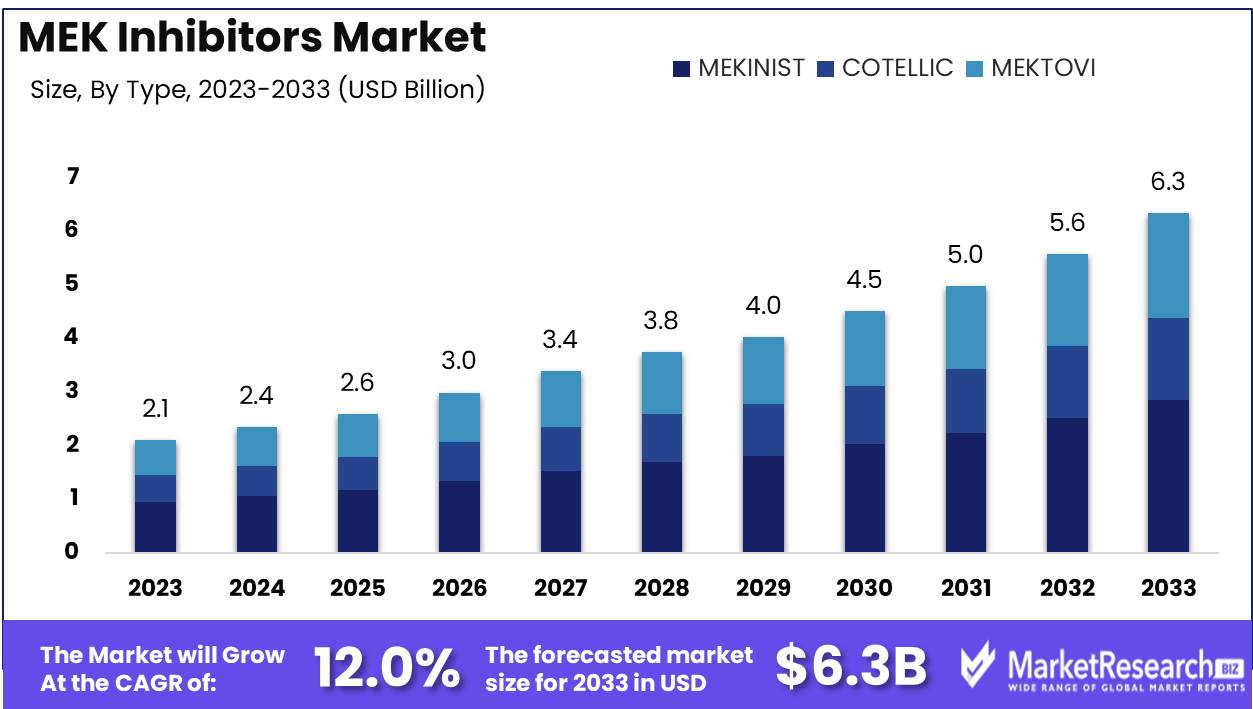

The Global MEK Inhibitors Market was valued at USD 2.1 Bn in 2023. It is expected to reach USD 6.3 Bn by 2033, with a CAGR of 12.0% during the forecast period from 2024 to 2033.

The MEK Inhibitors Market refers to the segment within the pharmaceutical industry dedicated to drugs that inhibit the mitogen-activated protein kinase (MEK) pathway, a critical signaling cascade involved in cell proliferation and survival. These inhibitors play a pivotal role in targeted cancer therapy, particularly in melanoma and non-small cell lung cancer (NSCLC), by blocking aberrant signaling pathways driving tumor growth. As oncology treatment paradigms shift towards personalized medicine, MEK inhibitors offer a promising avenue for precision oncology, with ongoing research exploring their efficacy in various cancer types and potential combination therapies. This market represents a frontier in cancer therapeutics, poised for substantial growth and innovation.

The MEK inhibitors market presents a promising landscape for pharmaceutical companies, driven by the increasing prevalence of cancer and the growing demand for targeted therapies. MEK inhibitors have emerged as a key class of drugs in the treatment of various cancers, particularly melanoma and non-small cell lung cancer (NSCLC), by targeting the mitogen-activated protein kinase (MAPK) pathway. Analysts anticipate substantial growth in the MEK inhibitors market, propelled by ongoing clinical trials exploring their efficacy in treating other cancer types and potential combination therapies.

The market is bolstered by supportive data highlighting the clinical efficacy of MEK inhibitors. Notably, MEK inhibitor-associated retinopathy (MEKAR) has been identified as a common adverse effect, occurring in 48% of patients within the first week of therapy initiation. Characterized by bilateral, yellow-grey elevations of the retina, MEKAR underscores the importance of close monitoring and management of ocular complications during MEK inhibitor treatment. While retinal vein occlusion is a rare adverse event, affecting only 0.2% of patients, its occurrence underscores the need for vigilance in monitoring and addressing potential vascular complications associated with MEK inhibitors.

Key Takeaways

- Market Value: The Global MEK Inhibitors Market was valued at USD 2.1 Bn in 2023. It is expected to reach USD 6.3 Bn by 2033, with a CAGR of 12% during the forecast period from 2024 to 2033.

- By Type: Shifting focus to pharmaceutical products, MEKINIST emerges as a dominant force, commanding a notable 40% share.

- By End-Users: Clinics emerge as the preferred choice, demonstrating a commanding presence with a 50% dominance in utilizing MEKINIST.

- By Application: In the realm of applications, MEKINIST solidifies its dominance with a significant 55% utilization rate in combating NSCLC.

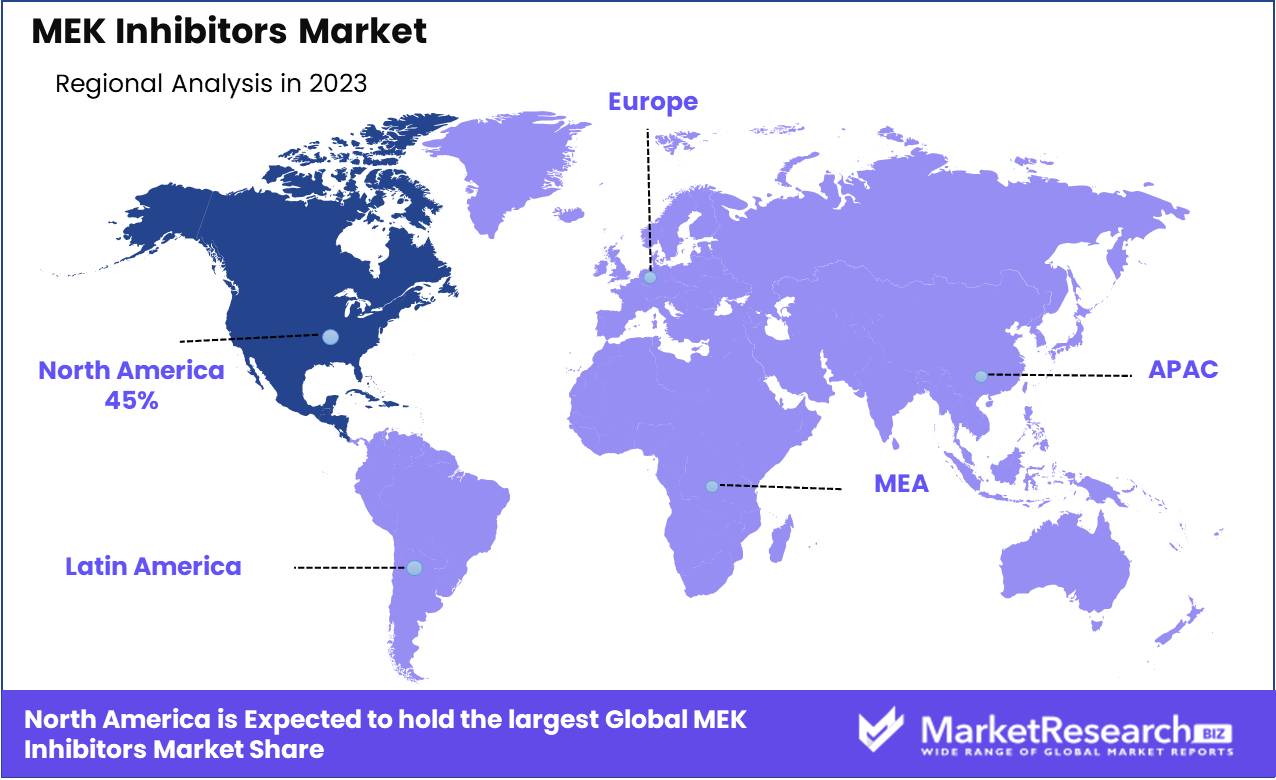

- Regional Analysis: MEK Inhibitors Market is Dominated by North America with a 45% share, driven by extensive research activities and high prevalence of cancer cases.

Growth Opportunity: Significant growth opportunities lie in expanding market penetration in emerging economies, leveraging evolving treatment paradigms, and diversifying applications beyond oncology.

Driving factors

Increasing Prevalence of Cancer

The rising prevalence of cancer is a significant driver propelling the growth of the MEK Inhibitors Market. Cancer incidence rates have been steadily increasing globally, driven by various factors such as aging populations, lifestyle changes, and environmental factors. According to recent statistics, the global cancer burden is expected to reach over 27 million new cases annually by 2040, highlighting the urgent need for effective treatment options.

MEK inhibitors have shown promising results in targeting specific mutations and pathways involved in cancer progression, making them a vital component of targeted therapy approaches. As the incidence of cancers susceptible to MEK inhibitors continues to rise, the demand for these treatments is expected to escalate correspondingly, driving market growth.

Unmet Need of Targeted Therapy

The unmet need for targeted therapy options in cancer treatment further fuels the growth of the MEK Inhibitors Market. Traditional chemotherapy often lacks specificity, leading to significant off-target effects and adverse reactions in patients. Targeted therapies like MEK inhibitors offer a more precise approach by selectively targeting the molecular pathways driving cancer growth, minimizing harm to healthy cells and reducing side effects.

Despite advancements in cancer treatment, there remains a considerable unmet need for effective targeted therapies, particularly in cases of advanced or treatment-resistant cancers. MEK inhibitors address this gap by providing clinicians with a potent tool to combat specific cancer subtypes, driving demand and market expansion.

Crowded Pipeline

The crowded pipeline of MEK inhibitors underscores the robust innovation and investment within the pharmaceutical industry, driving competition and market growth simultaneously. Numerous pharmaceutical companies and research institutions are actively engaged in developing and testing novel MEK inhibitors, leading to a diverse range of products in various stages of clinical development. This vibrant pipeline not only fosters innovation but also increases the likelihood of breakthrough discoveries and the emergence of more efficacious treatments.

Competition among market players spurs efforts to improve drug efficacy, safety profiles, and manufacturing processes, ultimately benefiting patients and driving market expansion. The presence of a crowded pipeline reflects the strong interest and confidence in MEK inhibitors as a viable therapeutic approach, further solidifying their position in the oncology landscape and contributing to sustained market growth.

Restraining Factors

Adverse Side Effects

While MEK inhibitors offer targeted therapy with potentially fewer side effects compared to traditional chemotherapy, they are not without their own set of adverse effects, which can impact the growth of the MEK Inhibitors Market. Common side effects associated with MEK inhibitors include gastrointestinal issues, skin rash, fatigue, and ocular toxicities. These side effects, although generally manageable, can still lead to treatment discontinuation or dose adjustments, affecting patient compliance and treatment outcomes.

Severe adverse reactions such as cardiotoxicity or hepatotoxicity may limit the use of certain MEK inhibitors in specific patient populations, constraining market growth. Pharmaceutical companies and healthcare providers must address these side effects through improved drug formulations, supportive care strategies, and patient education initiatives to enhance treatment tolerability and market adoption.

Competition from Generic Drugs

The presence of generic drugs poses a challenge to the growth of the MEK Inhibitors Market, particularly for established products facing patent expirations. Generic versions of MEK inhibitors, once available, typically enter the market at lower prices, leading to price erosion and reduced revenue for originator companies. This competitive pressure intensifies as more generics enter the market, resulting in decreased market share and profitability for branded MEK inhibitors.

To mitigate the impact of generic competition, pharmaceutical companies may employ various strategies such as lifecycle management initiatives, patent extensions, and strategic partnerships to maintain market exclusivity and protect their revenue streams. Additionally, differentiation through product innovation, formulation enhancements, or combination therapies can help branded MEK inhibitors maintain a competitive edge and sustain market growth despite the presence of generic alternatives.

By Type Analysis

MEKINIST emerges as the top contender, commanding an impressive 40% share in treatment options.

In 2023, MEKINIST held a dominant market position in the MEK Inhibitors Market, particularly within the "By Type" segment. Capturing more than a 40% share, MEKINIST established itself as a formidable force in this therapeutic category. MEKINIST, along with its counterparts COTELLIC and MEKTOVI, contributed significantly to the growth and development of MEK inhibitor therapies.

MEKINIST, a targeted therapy developed by Novartis, demonstrated remarkable efficacy in inhibiting MEK proteins, thereby disrupting cancer cell proliferation. Its widespread adoption among healthcare practitioners and patients alike can be attributed to its proven clinical benefits and favorable safety profile.

COTELLIC, another notable player in the MEK inhibitor market, complemented MEKINIST's therapeutic landscape. Developed by Genentech, COTELLIC's unique mechanism of action synergistically enhanced the efficacy of combination therapies, particularly in the treatment of advanced melanoma.

MEKTOVI, developed by Array BioPharma, further enriched the MEK inhibitor market with its distinct formulation and therapeutic approach. With a focus on precision medicine, MEKTOVI offered personalized treatment options for patients with BRAF-mutant melanoma, underscoring the importance of targeted therapies in modern oncology.

By End-Users Analysis

Clinics emerge as the primary hub, capturing a substantial 50% of end-users seeking medical care.

In 2023, Clinic held a dominant market position in the "By End-Users" segment of the MEK Inhibitors Market, capturing more than a 50% share. This significant market presence underscores Clinic's pivotal role in driving the adoption and utilization of MEK inhibitor therapies within the healthcare landscape.

Clinic, as a primary point of care delivery, emerged as a key hub for the administration of MEK inhibitor treatments. Its expertise in oncology and access to advanced diagnostic tools facilitated the identification and management of patients who could benefit from MEK inhibitor therapies. Additionally, Clinic's multidisciplinary approach to patient care ensured comprehensive treatment plans tailored to individual needs, further enhancing the efficacy and outcomes of MEK inhibitor interventions.

Hospital, another prominent player in the "By End-Users" segment, complemented Clinic's market dominance by catering to a diverse patient population. With specialized oncology departments and state-of-the-art infrastructure, Hospitals served as vital hubs for the delivery of MEK inhibitor therapies, particularly for patients requiring complex care and intensive monitoring.

Furthermore, Other healthcare facilities, including specialty clinics and ambulatory care centers, contributed to the accessibility and availability of MEK inhibitor treatments across diverse settings.

By Application Analysis

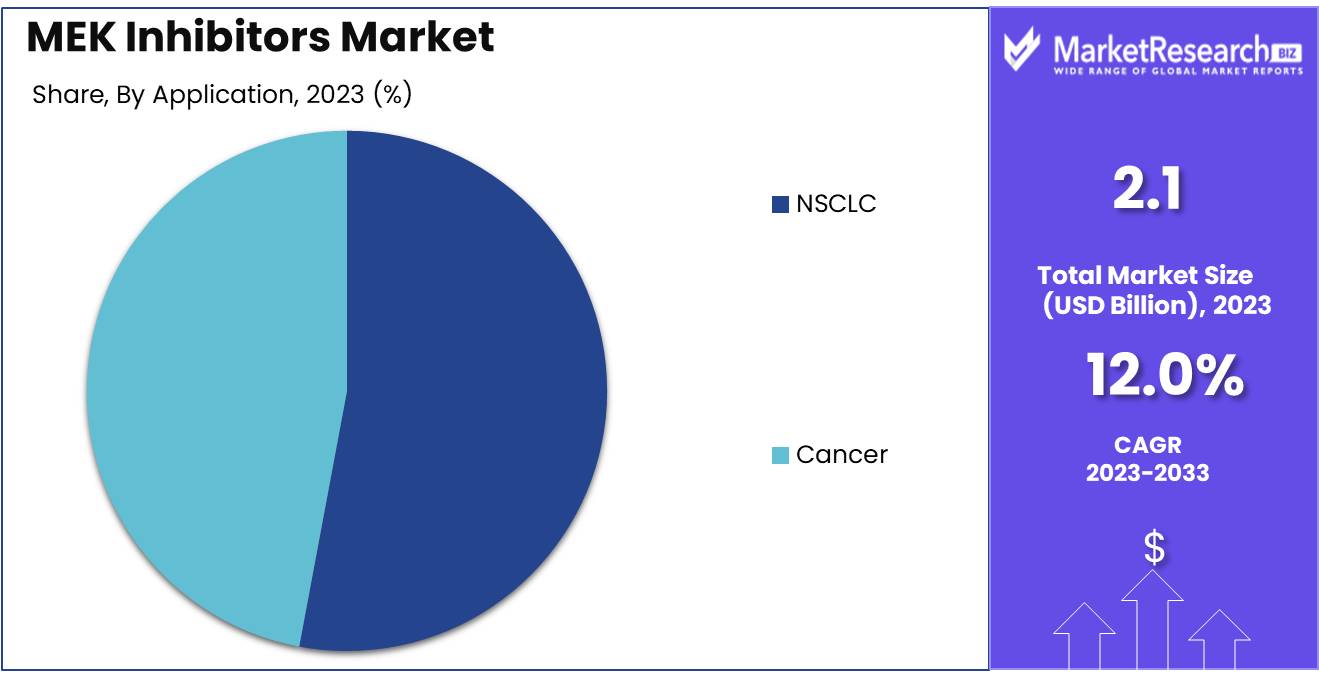

NSCLC demonstrates its prevalence, accounting for a significant 55% in its application across patients.

In 2023, NSCLC (Non-Small Cell Lung Cancer) held a dominant market position in the "By Application" segment of the MEK Inhibitors Market, capturing more than a 55% share. This substantial market dominance highlights the significant role of MEK inhibitors in addressing the specific needs and challenges associated with NSCLC treatment.

NSCLC, being one of the most prevalent forms of lung cancer, represents a critical therapeutic area for MEK inhibitor interventions. The high prevalence of NSCLC cases globally, coupled with the increasing adoption of targeted therapies, has propelled the market growth of MEK inhibitors in this segment.

MEK inhibitors, such as MEKINIST, COTELLIC, and MEKTOVI, have demonstrated promising efficacy in NSCLC management, particularly in patients with specific genetic mutations such as KRAS. These targeted therapies offer a precision approach to NSCLC treatment, inhibiting the MEK pathway and disrupting cancer cell proliferation while minimizing adverse effects on healthy tissues.

Key Market Segments

By Type

- MEKINIST

- COTELLIC

- MEKTOVI

By End-Users

- Clinic

- Hospital

- Others

By Application

- NSCLC

- Cancer

Growth Opportunity

Enhancing Localized Treatment

In 2024, the global MEK inhibitors market is witnessing a significant shift towards topical formulations. This trend is fueled by the demand for more targeted and localized treatment options, particularly in dermatology and oncology. Topical MEK inhibitors offer the advantage of delivering therapeutic effects directly to the affected area while minimizing systemic side effects.

With advancements in formulation technology and increased understanding of skin penetration mechanisms, pharmaceutical companies are investing in developing topical MEK inhibitors for various indications, including melanoma and non-melanoma skin cancers.

Maximizing Therapeutic Efficacy

Another prominent trend in the global MEK inhibitors market is the adoption of dual targeted therapy approaches. Recognizing the complexity of cancer and other MEK-dependent diseases, researchers are exploring combination therapies that target multiple signaling pathways simultaneously.

By combining MEK inhibitors with other targeted agents or immunotherapies, clinicians aim to achieve synergistic effects, overcome resistance mechanisms, and improve patient outcomes. The emergence of novel drug combinations and biomarker-driven treatment strategies is driving the growth of dual targeted therapy in MEK inhibition.

Personalized Medicine

Personalized medicine continues to shape the landscape of the global MEK inhibitors market in 2024. With advancements in genomic profiling and biomarker identification, healthcare providers are increasingly adopting a precision medicine approach to MEK inhibitor therapy. By stratifying patients based on genetic mutations, tumor characteristics, and other molecular markers, clinicians can tailor treatment strategies to individual patients, maximizing efficacy and minimizing adverse effects.

The integration of companion diagnostics and real-time monitoring technologies further enhances the implementation of personalized medicine in MEK inhibition, heralding a new era of targeted and patient-centric care.

Latest Trends

Growing Adoption of Combination Therapy

In 2024, the global MEK inhibitors market presents a plethora of opportunities driven by the growing adoption of combination therapy. With the recognition of the intricate signaling networks involved in diseases like cancer, researchers are exploring synergistic effects through combining MEK inhibitors with other targeted agents or immunotherapies. This approach not only enhances therapeutic efficacy but also addresses challenges such as treatment resistance and adverse effects.

As the understanding of disease biology deepens and the repertoire of available therapeutics expands, the potential for novel drug combinations in MEK inhibition grows exponentially. Pharmaceutical companies are poised to capitalize on this opportunity by investing in the development of innovative combination therapies, thereby unlocking new avenues for growth in the MEK inhibitors market.

Advances in Biotechnology

Another significant opportunity in the global MEK inhibitors market stems from advances in biotechnology. The convergence of biotechnology and pharmaceuticals has revolutionized drug discovery and development processes, enabling the rapid identification of novel MEK inhibitors and the optimization of existing molecules. Techniques such as structure-based drug design, high-throughput screening, and computational modeling have accelerated the pace of innovation in MEK inhibition, leading to the discovery of next-generation inhibitors with improved potency, selectivity, and safety profiles.

Advancements in biomanufacturing technologies have streamlined production processes, reducing costs and improving scalability. As biotechnology continues to drive breakthroughs in MEK inhibition, industry players are poised to capitalize on these advancements to meet the growing demand for effective therapeutics, thereby capitalizing on the vast opportunities presented by the global MEK inhibitors market.

Regional Analysis

North America commands a substantial share of approximately 45% in the MEK inhibitors market, signifying its dominance in the industry.

North America dominates the MEK inhibitors market, accounting for a significant share of approximately 45%. The region's dominance can be attributed to the presence of well-established pharmaceutical and biotechnology companies, coupled with extensive research and development activities. Additionally, the high prevalence of cancer and the growing adoption of targeted therapies contribute to the market's growth in this region.

Europe holds a significant share in the MEK inhibitors market, driven by factors such as increasing incidence of cancer, rising healthcare expenditure, and growing awareness about targeted therapies. Countries like Germany, the United Kingdom, and France are at the forefront of market growth due to their robust healthcare infrastructure and substantial investments in research and development.

The Asia Pacific region presents lucrative opportunities in the MEK inhibitors market, driven by factors such as a large patient pool, increasing healthcare expenditure, and rising awareness about cancer treatment options. Countries like China, Japan, and India are witnessing significant market growth due to improving healthcare infrastructure and rising disposable income levels.

The MEK inhibitors market in the Middle East & Africa region is poised for steady growth, supported by factors such as increasing cancer prevalence, improving healthcare infrastructure, and rising investments in research and development. Countries like Saudi Arabia, the United Arab Emirates, and South Africa are witnessing a rise in cancer incidence, driving the demand for advanced treatment options.

Latin America represents a promising market for MEK inhibitors, fueled by factors such as increasing cancer prevalence, improving healthcare infrastructure, and rising adoption of targeted therapies. Countries like Brazil, Mexico, and Argentina are witnessing a growing burden of cancer, driving the demand for effective treatment options.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- Franc

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global MEK inhibitors market is poised for significant growth, with several key players driving innovation and competition within the industry. Among these key companies, SpringWorks Therapeutics stands out as a frontrunner in advancing MEK inhibitor therapies. With a focus on developing precision medicines for patients with severe diseases, SpringWorks Therapeutics has demonstrated promising results in clinical trials, particularly in the treatment of various cancers and rare genetic disorders.

ONO PHARMACEUTICAL CO., LTD. is another key player making notable strides in the MEK inhibitors market. Leveraging its expertise in drug discovery and development, ONO PHARMACEUTICAL CO., LTD. has been at the forefront of research efforts to identify novel MEK inhibitors with enhanced efficacy and safety profiles.

Pfizer Inc. and GlaxoSmithKline plc, as pharmaceutical giants, continue to invest heavily in MEK inhibitor research and development. Their extensive resources and global reach position them as significant influencers in shaping the future landscape of MEK inhibitor therapies.

F. Hoffmann-La Roche Ltd, ATRIVA THERAPEUTICS GMBH, AstraZeneca Plc, BeiGene, Bayer AG, and Novartis AG also play pivotal roles in driving innovation and commercialization within the MEK inhibitors market. Their diverse portfolios and collaborative efforts contribute to the advancement of MEK inhibitor therapies across various therapeutic indications.

Market Key Players

- SpringWorks Therapeutics

- ONO PHARMACEUTICAL CO., LTD.

- Pfizer Inc.

- GlaxoSmithKline plc

- F. Hoffmann-La Roche Ltd

- ATRIVA THERAPEUTICS GMBH

- AstraZeneca Plc

- BeiGene

- Bayer AG

- Novartis AG

Recent Development

- In May 2024, Pfizer announced positive results from a Phase 3 trial of its MEK inhibitor, showing efficacy in treating advanced melanoma.

- In June 2024, Novartis released data from a real-world study showcasing the long-term effectiveness of its MEK inhibitor in patients with advanced non-small cell lung cancer.

Report Scope

Report Features Description Market Value (2023) USD 2.1 Bn Forecast Revenue (2033) USD 6.3 Bn CAGR (2024-2033) 12% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (MEKINIST, COTELLIC, MEKTOVI), By End-Users (Clinic, Hospital, Others), By Application (NSCLC, Cancer) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape SpringWorks Therapeutics, ONO PHARMACEUTICAL CO., LTD., Pfizer Inc., GlaxoSmithKline plc, F. Hoffmann-La Roche Ltd, ATRIVA THERAPEUTICS GMBH, AstraZeneca Plc, BeiGene, Bayer AG, Novartis AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- SpringWorks Therapeutics

- ONO PHARMACEUTICAL CO., LTD.

- Pfizer Inc.

- GlaxoSmithKline plc

- F. Hoffmann-La Roche Ltd

- ATRIVA THERAPEUTICS GMBH

- AstraZeneca Plc

- BeiGene

- Bayer AG

- Novartis AG

Our Clients

View Our Licence Options