Global Medical Polymer Market By Product(Fibers & Resins(PVC, PP, PE, PS, Others), Medical Elastomers(Styrene Block Copolymer, Rubber latex, Others), Biodegradable Polymers, Polyhydroxyalkanoate (PHA), Others), By Application(Medical Device Packaging, Medical Components, Orthopedic Soft Goods, Wound Care, Cleanroom Supplies, BioPharm Devices, Mobility Aids, Sterilization & Infection Prevention, Tooth Implants, Other Implants, Others), By Processing Method(Blow Fill Seal, Extrusion Blow Molding, Others), By Region And Companies - Industry Segment Out

-

46063

-

May 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

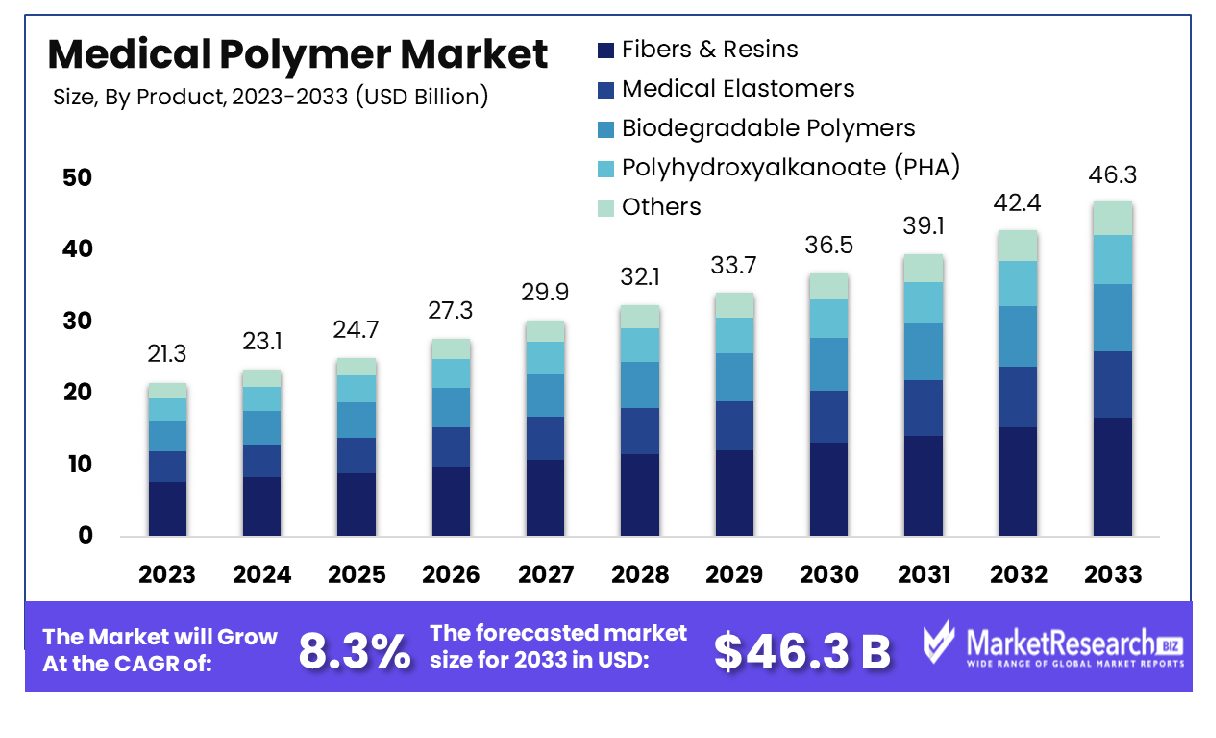

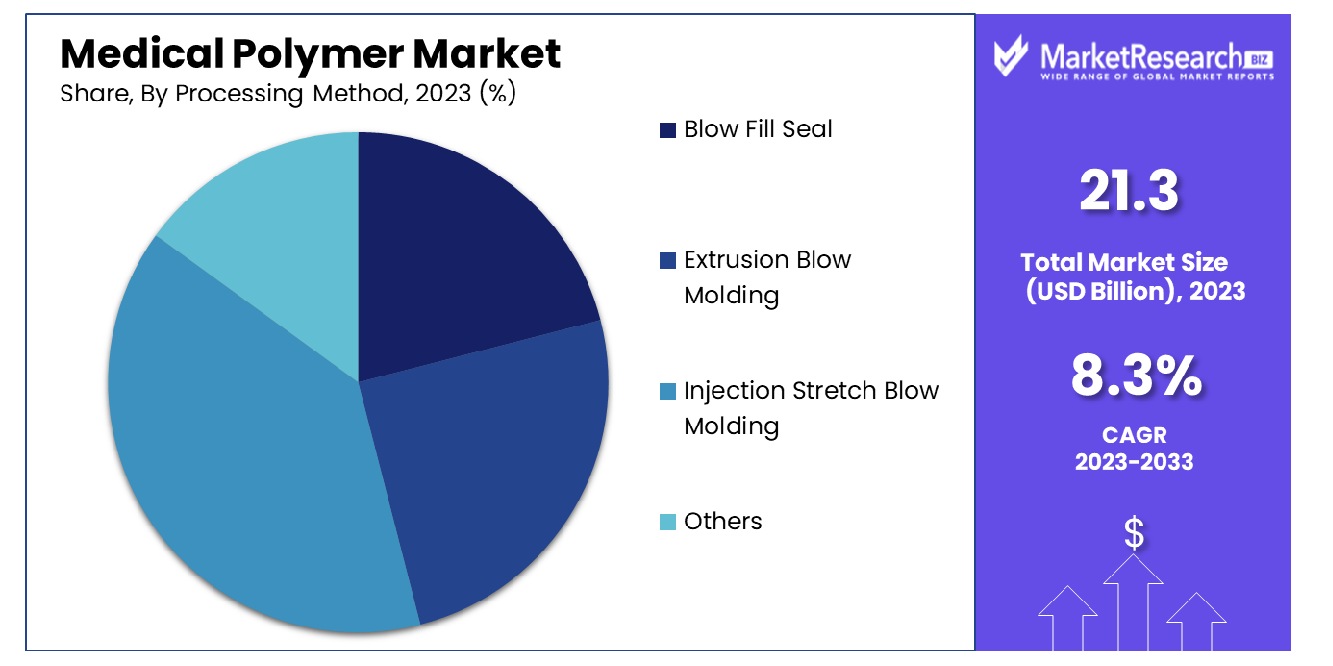

The Global Medical Polymer Market was valued at USD 21.3 billion in 2023. It is expected to reach USD 46.3 billion by 2033, with a CAGR of 8.3% during the forecast period from 2024 to 2033.

The Medical Polymer Market encompasses materials engineered for use in the healthcare sector. These polymers are favored for their versatility, biocompatibility, and durability, making them essential in the manufacture of a broad range of medical devices and packaging. This market is critical as it supports innovations in patient care through the development of advanced medical instruments and implantable devices.

Key stakeholders, including Product Managers, should note its strategic importance in driving advancements in medical technologies, ensuring compliance with stringent health regulations, and adapting to evolving demands for high-quality, safe medical products.

The Medical Polymer Market is poised for significant growth, driven by the increasing demand for advanced medical devices and the rising prevalence of chronic conditions necessitating long-term medical interventions. Polymers are crucial in healthcare, offering unique properties that make them indispensable for a wide range of applications, from disposable syringes to sophisticated implantable devices. Their biocompatibility and ease of sterilization enhance patient safety and operational efficiencies in medical procedures.

A pivotal aspect of this market's expansion is its robust production metrics, particularly evident in regions like India. In the fiscal year 2022-23, up to September, India produced approximately 12,471 thousand metric tons of polymers, marking a compound annual growth rate (CAGR) of 7.68% from 2017-18 to 2021-22. This growth underscores the country’s strengthening capacity to meet both domestic and global demand for medical-grade polymers.

Additionally, the production of major chemicals, which are essential in the synthesis of many specialty polymolecules, was recorded at 6,487 thousand metric tons during the same period, with a CAGR of 3.58%. These figures highlight the increasing scale and sophistication of India’s chemical production capabilities, which are vital for the medical polymer sector.

As the market continues to evolve, strategic investments in production capabilities and technology will be crucial. For stakeholders, particularly at the executive level, the focus should be on leveraging these growth trends to enhance supply chain robustness and capitalize on emerging opportunities in the global healthcare market.

Key Takeaways

- Market Growth: The Global Medical Polymer Market was valued at USD 21.3 billion in 2023. It is expected to reach USD 46.3 billion by 2033, with a CAGR of 8.3% during the forecast period from 2024 to 2033.

- By Product: Fibers & resins held the majority share at 54.3% market dominance.

- By Application: Medical components led the application sector with 42.3% dominance.

- By Processing Method: Injection stretch blow molding dominated processing at 33.2%.

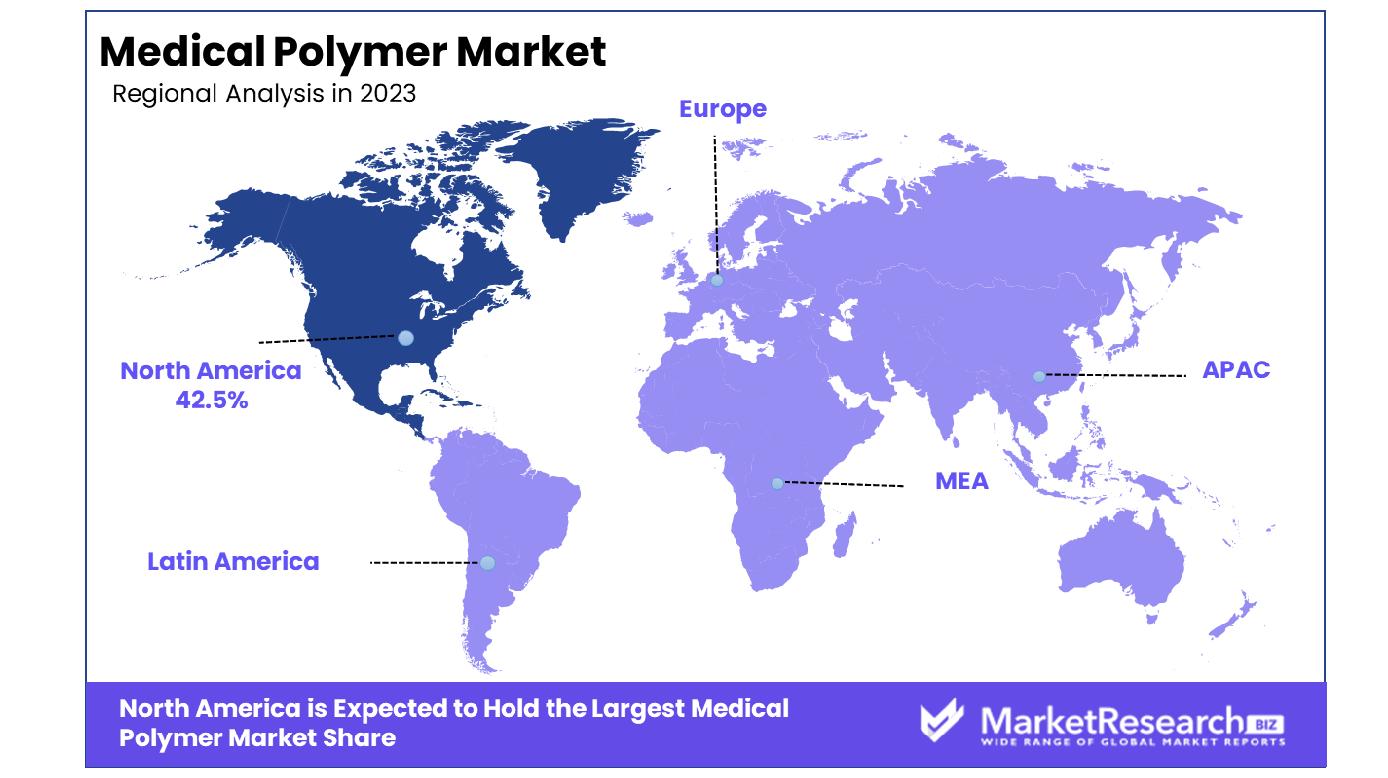

- Regional Dominance: In North America, the medical polymer market commands a significant 42.5% share.

- Growth Opportunity: The 2023 growth outlook for the global medical polymer market is optimistic, driven by demand for high-performance polymers in implants and increased focus on infection control measures in healthcare settings.

Driving factors

Favorable Government Initiatives and Policies

The growth of the medical polymer market is significantly bolstered by favorable government initiatives and policies. Governments across the globe are implementing supportive regulations and offering incentives to encourage the development and adoption of advanced medical materials. For instance, the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have streamlined approval processes for medical devices and materials, expediting the introduction of innovative medical polymers.

Furthermore, initiatives such as the Medical Device User Fee Amendments (MDUFA) and similar programs in other regions reduce the financial burden on manufacturers, encouraging investment in research and development. These policies not only facilitate faster market entry but also ensure higher standards of safety and efficacy, thereby enhancing consumer trust and driving demand for medical polymers.

Increasing Healthcare Expenditure and Insurance Coverage

Rising healthcare expenditure and broader insurance coverage are pivotal in driving the medical polymer market. Global healthcare spending is projected to increase at an annual rate of 5.4% from 2021 to 2025, reaching approximately $10 trillion by 2025. This surge is accompanied by expanded insurance coverage, particularly in emerging economies, improving access to advanced medical treatments. Increased funding allows healthcare providers to invest in high-quality, polymer-based medical devices and equipment.

As insurance coverage widens, patients are more likely to receive and afford advanced treatments, boosting the demand for innovative medical polymers used in devices such as catheters, prosthetics, and diagnostic equipment. This trend is expected to sustain long-term growth in the market.

Shift Towards Minimally Invasive and Implantable Devices

The shift towards minimally invasive procedures and implantable devices is a major driver of the medical polymer market. Minimally invasive surgeries (MIS) are gaining popularity due to their benefits, including reduced recovery times, lower risk of infection, and shorter hospital stays. According to recent data, the global market for minimally invasive surgical instruments is expected to grow at a compound annual growth rate (CAGR) of 9.2% from 2021 to 2028.

Medical polymers play a crucial role in the manufacturing of devices used in MIS, such as endoscopes and catheters, due to their biocompatibility, flexibility, and durability. Additionally, the rising demand for implantable devices, such as artificial joints and cardiovascular stents, further propels the market. These devices rely heavily on advanced polymers to ensure longevity and compatibility with human tissues, thereby driving market expansion.

Restraining Factors

High Initial Investment Re quired for Development

The high initial investment required for the development of medical polymers is a significant restraining factor impacting market growth. The development and production of advanced medical polymers demand substantial financial resources, encompassing research and development (R&D), state-of-the-art manufacturing facilities, and stringent testing protocols. These costs can be prohibitive, particularly for small and medium-sized enterprises (SMEs), limiting their ability to enter or expand within the market.

The high capital expenditure is often associated with the need for specialized equipment and the adherence to rigorous quality control standards. For instance, developing biocompatible polymers necessitates extensive testing to ensure they meet safety and efficacy criteria, further driving up costs. This financial barrier can deter innovation and slow the introduction of new products, thereby constraining overall market growth.

Regulatory Constraints and Standards Compliance Challenge

Regulatory constraints and the challenge of standards compliance present another major restraint on the growth of the medical polymer market. Medical polymers must meet stringent regulatory requirements set by authorities such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other global regulatory bodies. These regulations are designed to ensure the safety and efficacy of medical devices, but they also impose significant hurdles for manufacturers.

The process of obtaining regulatory approval is often lengthy, complex, and costly. Companies must navigate a labyrinth of clinical trials, documentation, and inspections, which can delay product launches and increase development costs. Additionally, maintaining compliance with evolving standards requires continuous investment in regulatory affairs and quality assurance.

These challenges can limit the ability of manufacturers to bring new products to market quickly and efficiently, thereby hindering market growth. The stringent regulatory landscape, while essential for ensuring patient safety, poses a substantial barrier to entry and can stifle innovation within the medical polymer industry.

By Product Analysis

In the Fibers & Resins market, dominance at 54.3% signifies robust growth and market leadership.

In 2023, Fibers & Resins held a dominant market position in the By Product segment of the Medical Polymer Market, capturing more than a 54.3% share. This segment encompasses a diverse range of materials vital to the medical industry's production of various devices, equipment, and packaging materials. Within Fibers & Resins, Polyvinyl Chloride (PVC), Polypropylene (PP), Polyethylene (PE), Polystyrene (PS), and other engineering thermoplastics such as nylon, PET, PLA, PHA, PA, PC, and ABS play pivotal roles in meeting the demanding requirements of medical applications.

PVC, known for its versatility and cost-effectiveness, remains a cornerstone material in medical products, ranging from tubing to blood bags. PP and PE, valued for their durability and chemical resistance, find extensive use in medical packaging and disposable products. Similarly, PS serves in medical packaging applications due to its clarity and barrier properties.

Moreover, Medical Elastomers, including Styrene Block Copolymers and Rubber Latex, contribute significantly to the market, offering flexibility, elasticity, and biocompatibility essential for medical devices such as catheters and surgical gloves. Emerging materials like Thermoplastic Polyurethane (TPU), Thermoplastic Olefin (TPO), and Thermoplastic Vulcanizate (TPV) are gaining traction, owing to their superior mechanical properties and processing advantages.

In line with the industry's growing emphasis on sustainability, Biodegradable Polymers, particularly Polyhydroxyalkanoates (PHA), are witnessing increased adoption. PHA, with its biodegradability and biocompatibility, holds promise for eco-friendly medical applications, aligning with evolving regulatory and consumer preferences for sustainable healthcare solutions. As the medical polymer market continues to evolve, innovation across these diverse segments will play a crucial role in addressing emerging challenges and meeting the dynamic needs of the healthcare sector.

By Application Analysis

Medical Components application's dominance at 42.3% underscores its pivotal role in the industry.

In 2023, Medical Components held a dominant market position in the By Application segment of the Medical Polymer Market, capturing more than a 42.3% share. This segment encompasses a wide array of applications crucial to the healthcare industry, spanning from medical device packaging to specialized implants and orthopedic soft goods. Medical device packaging stands out as a significant component, ensuring the integrity and sterility of medical products throughout their lifecycle. Additionally, Medical Components encompass a broad spectrum of products ranging from catheters, syringes, and IV sets to respiratory masks and surgical instruments, catering to diverse healthcare needs.

Orthopedic soft goods, including braces, splints, and supports, constitute another vital segment within Medical Components, addressing musculoskeletal conditions and injuries. Similarly, wound care products, essential for managing acute and chronic wounds, drive demand for advanced materials with properties like moisture management and biocompatibility. Cleanroom supplies play a critical role in maintaining sterile environments for medical manufacturing and research activities, demanding materials with exceptional purity and cleanliness characteristics.

Moreover, BioPharm devices, mobility aids, and sterilization & infection prevention products contribute significantly to the market, serving various healthcare settings and patient needs. Tooth implants and denture-based materials cater to the dental segment, offering solutions for tooth replacement and oral rehabilitation. Other implants encompass a wide range of medical devices, including cardiovascular stents, intraocular lenses, and tissue scaffolds, highlighting the versatility of medical polymers across diverse therapeutic areas.

As healthcare demands evolve and technology advances, the Medical Components segment will continue to witness innovation and growth, driven by the pursuit of improved patient outcomes, infection control measures, and enhanced healthcare delivery.

By Processing Method Analysis

Injection Stretch Blow Molding's dominance at 33.2% highlights its efficiency and widespread adoption.

In 2023, Injection Stretch Blow Molding (ISBM) held a dominant market position in the By Processing Method segment of the Medical Polymer Market, capturing more than a 33.2% share. This method stands out as a preferred manufacturing technique due to its versatility, efficiency, and ability to produce intricate and precise medical components and packaging solutions.

ISBM involves the injection of polymer material into a preform, followed by stretching and blowing to achieve the desired shape and dimensions. This process is widely utilized in the production of bottles, vials, containers, and other packaging materials for pharmaceuticals, medical devices, and diagnostics. The method offers several advantages, including high production speed, consistent product quality, and excellent dimensional stability, making it well-suited for meeting the stringent requirements of the medical industry.

In addition to ISBM, other processing methods such as Blow Fill Seal (BFS), Extrusion Blow Molding, and alternative techniques play significant roles in the medical polymer market. BFS, known for its aseptic packaging capabilities, is particularly favored for single-dose containers and ampoules used in pharmaceuticals and sterile medical products. Extrusion Blow Molding, on the other hand, is commonly employed in the manufacturing of larger containers, reservoirs, and components for medical devices and equipment.

Furthermore, innovative processing methods continue to emerge, offering unique advantages in terms of efficiency, cost-effectiveness, and product customization. These include technologies such as 3D printing, compression molding, and thermoforming, which cater to specific applications within the medical sector, ranging from personalized implants to custom-designed medical devices.

As the demand for advanced medical solutions grows, manufacturers are expected to leverage a combination of processing methods to meet diverse market needs, driving innovation and growth in the medical polymer segment.

Key Market Segments

By Product

- Fibers & Resins

- PVC

- PP

- PE

- PS

- Others (engineering thermoplastics such as nylon, PET, PLA, PHA, PA, PC, ABS)

- Medical Elastomers

- Styrene Block Copolymer

- Rubber latex (NR + Butyl Rubber+Silicone rubber)

- Others (TPU, TPO, TPV)

- Biodegradable Polymers

- Polyhydroxyalkanoate (PHA)

- Others

By Application

- Medical Device Packaging

- Medical Components

- Orthopedic Soft Goods

- Wound Care

- Cleanroom Supplies

- BioPharm Devices

- Mobility Aids

- Sterilization & Infection Prevention

- Tooth Implants

- Denture-based Materials

- Other Implants

- Others

By Processing Method

- Blow Fill Seal

- Extrusion Blow Molding

- Injection Stretch Blow Molding

- Others

Growth Opportunity

Demand for High-performance Polymers in Medical Implants

The growth trajectory of the global medical polymer market in 2023 is poised for significant expansion, primarily fueled by the escalating demand for high-performance polymers in medical implants. With technological advancements and innovation in material science, the medical industry is witnessing a paradigm shift towards the utilization of polymers exhibiting superior biocompatibility, mechanical properties, and long-term stability.

High-performance polymers such as polyetheretherketone (PEEK) and polyethylene (PE) are gaining prominence for their exceptional strength, corrosion resistance, and biostability, making them ideal candidates for orthopedic and cardiovascular implants.

Furthermore, the surge in chronic diseases and the aging population worldwide amplifies the need for durable and biocompatible materials, thereby propelling the adoption of medical polymers in implantable medical devices. This trend is anticipated to stimulate substantial market growth opportunities, with key players focusing on research and development initiatives to enhance polymer properties and cater to evolving healthcare demands.

Focus on Infection Control Measures in Healthcare Settings

Another pivotal driver shaping the growth landscape of the global medical polymer market in 2023 is the heightened emphasis on infection control measures in healthcare settings. The outbreak of infectious diseases and the prevalence of healthcare-associated infections have underscored the critical importance of antimicrobial and sterilizable medical devices and equipment.

Polymer materials embedded with antimicrobial agents or possessing inherent antimicrobial properties are gaining traction for their ability to inhibit microbial growth and prevent nosocomial infections. Additionally, advancements in polymer manufacturing techniques, such as additive manufacturing and surface modification technologies, enable the development of medical devices with enhanced antimicrobial properties and easy-to-clean surfaces.

Consequently, healthcare facilities worldwide are increasingly adopting antimicrobial polymers to mitigate infection risks and uphold patient safety standards, thereby driving the demand for medical polymers and fostering market growth opportunities in 2023.

Latest Trends

Integration of Antimicrobial Polymers in Healthcare Settings

In 2023, the global medical polymer market is witnessing a notable trend towards the integration of antimicrobial polymers in healthcare settings. With the rising concerns over healthcare-associated infections and the emergence of antimicrobial resistance, healthcare facilities are increasingly adopting medical devices and equipment fabricated from polymers embedded with antimicrobial agents. These antimicrobial polymers exhibit the ability to inhibit the growth of pathogens on surfaces, thereby reducing the risk of nosocomial infections and enhancing patient safety.

The demand for antimicrobial polymers is driven by their efficacy in maintaining hygienic environments in hospitals, clinics, and other medical facilities. As a result, manufacturers are investing in research and development to enhance the antimicrobial properties of medical polymers, thereby catering to the evolving needs of the healthcare industry.

Development of Biodegradable Polymers for Sustainable Medical Solutions

Another significant trend shaping the global medical polymer market in 2023 is the development of biodegradable polymers for sustainable medical solutions. With growing environmental concerns and increasing regulatory pressure to reduce plastic waste, there is a growing demand for biodegradable polymers in medical applications. These polymers are designed to degrade naturally over time, minimizing their environmental impact and offering sustainable alternatives to conventional petroleum-based plastics.

The development of biodegradable polymers for medical use is driven by their potential to reduce the accumulation of plastic waste in landfills and oceans, as well as their compatibility with emerging trends towards eco-friendly healthcare practices. Manufacturers are focusing on the research and commercialization of biodegradable polymers with suitable mechanical properties and biocompatibility, thereby unlocking new opportunities for sustainable medical solutions in 2023.

Regional Analysis

In North America, the medical polymer market commands a substantial share of 42.5%.

In the realm of medical polymers, distinct regional dynamics shape the market landscape across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America emerges as a prominent hub for medical polymers, accounting for a substantial market share of 42.5%. This dominance is underpinned by robust healthcare infrastructure, high adoption rates of advanced medical technologies, and significant investments in research and development endeavors. Moreover, stringent regulatory frameworks emphasizing the use of high-quality materials in medical applications further bolster the demand for polymers in the region.

In Europe, the medical polymer market exhibits steady growth propelled by a burgeoning healthcare sector, particularly in countries like Germany, France, and the United Kingdom. Stringent regulatory standards, such as those outlined by the European Pharmacopoeia, drive the adoption of medical-grade polymers, ensuring product safety and efficacy. Additionally, increasing investments in medical research and development initiatives contribute to the expansion of the market across the region.

Asia Pacific emerges as a burgeoning market for medical polymers, propelled by rapid urbanization, burgeoning population, and increasing healthcare expenditure. Countries like China, Japan, and India are at the forefront of market growth, driven by the expansion of healthcare infrastructure and the rising prevalence of chronic diseases. Moreover, favorable government initiatives aimed at enhancing healthcare accessibility and affordability further fuel market expansion in the region.

In the Middle East & Africa and Latin America regions, the medical polymer market showcases promising growth prospects, albeit at a relatively slower pace compared to other regions. Factors such as improving healthcare infrastructure, rising disposable incomes, and growing awareness regarding advanced medical treatments contribute to market growth. However, challenges such as limited access to healthcare services and regulatory complexities may impede the market's full potential in these regions.

In summary, the medical polymer market exhibits a diverse regional landscape, with North America leading the pack with a dominant market share of 42.5%. However, opportunities for growth and expansion abound across Europe, Asia Pacific, Middle East & Africa, and Latin America, driven by evolving healthcare needs, technological advancements, and regulatory developments.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global medical polymer market witnessed significant activity and competition among key players striving to carve their niche in this burgeoning sector. Among these, several notable companies stood out for their contributions and strategies.

BASF SE, a stalwart in the chemical industry, continued to assert its presence in the medical polymer market through its diversified portfolio and commitment to innovation. Leveraging its extensive research and development capabilities, BASF SE aimed to address emerging healthcare challenges with tailored polymer solutions, emphasizing safety, efficacy, and sustainability.

NatureWorks LLC emerged as a frontrunner, particularly in the realm of biodegradable polymers, catering to the increasing demand for eco-friendly medical materials. With a focus on bio-based solutions, NatureWorks LLC capitalized on growing environmental awareness and regulatory incentives to expand its market footprint and foster sustainable healthcare practices.

Covestro AG positioned itself as a key player in the medical polymer landscape, leveraging its expertise in high-performance materials to address critical industry needs. Through strategic partnerships and investments, Covestro AG continued to innovate and develop advanced polymer solutions, enhancing patient care outcomes and driving market growth.

Celanese Corporation remained at the forefront of innovation, offering a diverse range of medical-grade polymers tailored to meet the stringent requirements of the healthcare industry. With a global presence and a strong focus on customer collaboration, Celanese Corporation maintained its competitive edge by delivering high-quality, reliable polymer solutions.

Overall, in 2023, key players in the global medical polymer market such as BASF SE, NatureWorks LLC, Covestro AG, and Celanese Corporation demonstrated resilience, innovation, and strategic vision, positioning themselves for sustained growth and success in the dynamic healthcare landscape.

Market Key Players

- BASF SE

- NatureWorks LLC

- Covestro AG

- Celanese Corporation

- Eastman Chemical Corporation

- Evonik Industries AG

- Dow Inc.

- Exxon Mobil Corporation

- Arkema

- Koninklijke DSM NV

- Formosa Plastics Corporation

- Foryou Medical

- KRATON CORPORATION

- SABIC

- Trinseo S.A.

Recent Development

- In April 2024, Valmet introduces Polymer Concentration Measurement system, enhancing precision in polymer processing. TotalEnergies pioneers circular polymers from plastic waste, fostering sustainability. Athina Anastasaki explores innovative polymer recycling techniques. Panasonic launches Electrolytic Polymer Hybrid capacitors for EVs.

- In January 2024, The SPE/MPD MiniTec Conference highlights advances in medical plastics. Topics include biodegradable TPUs by DSM Biomedical, PFAS impact discussed by Exponent, and sustainable designs by DuPont Delrin.

- In December 2023, EQT Private Equity acquired Zeus, a leader in medical polymer components, enhancing innovation and global expansion. John Groetelaars was appointed as Executive Chairman to drive growth and strengthen partnerships.

Report Scope

Report Features Description Market Value (2023) USD 21.3 Billion Forecast Revenue (2033) USD 46.3 Billion CAGR (2024-2032) 8.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Fibers & Resins(PVC, PP, PE, PS, Others (engineering thermoplastics such as nylon, PET, PLA, PHA, PA, PC, ABS)), Medical Elastomers(Styrene Block Copolymer, Rubber latex (NR + Butyl Rubber+Silicone rubber), Others (TPU, TPO, TPV)), Biodegradable Polymers, Polyhydroxyalkanoate (PHA), Others), By Application(Medical Device Packaging, Medical Components, Orthopedic Soft Goods, Wound Care, Cleanroom Supplies, BioPharm Devices, Mobility Aids, Sterilization & Infection Prevention, Tooth Implants, Denture-based Materials, Other Implants, Others), By Processing Method(Blow Fill Seal, Extrusion Blow Molding, Injection Stretch Blow Molding, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape BASF SE, NatureWorks LLC, Covestro AG, Celanese Corporation, Eastman Chemical Corporation, Evonik Industries AG, Dow Inc., Exxon Mobil Corporation, Arkema, Koninklijke DSM NV, Formosa Plastics Corporation, Foryou Medical, KRATON CORPORATION, SABIC, Trinseo S.A. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- BASF SE

- NatureWorks LLC

- Covestro AG

- Celanese Corporation

- Eastman Chemical Corporation

- Evonik Industries AG

- Dow Inc.

- Exxon Mobil Corporation

- Arkema

- Koninklijke DSM NV

- Formosa Plastics Corporation

- Foryou Medical

- KRATON CORPORATION

- SABIC

- Trinseo S.A.

Our Clients

View Our Licence Options