Medical Device Cybersecurity Market By Component (Solutions, Services), By Device Type (Hospital Medical Devices, Home-Use Medical Devices, Wearable Medical Devices), By End-User (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

50517

-

Aug 2024

-

304

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

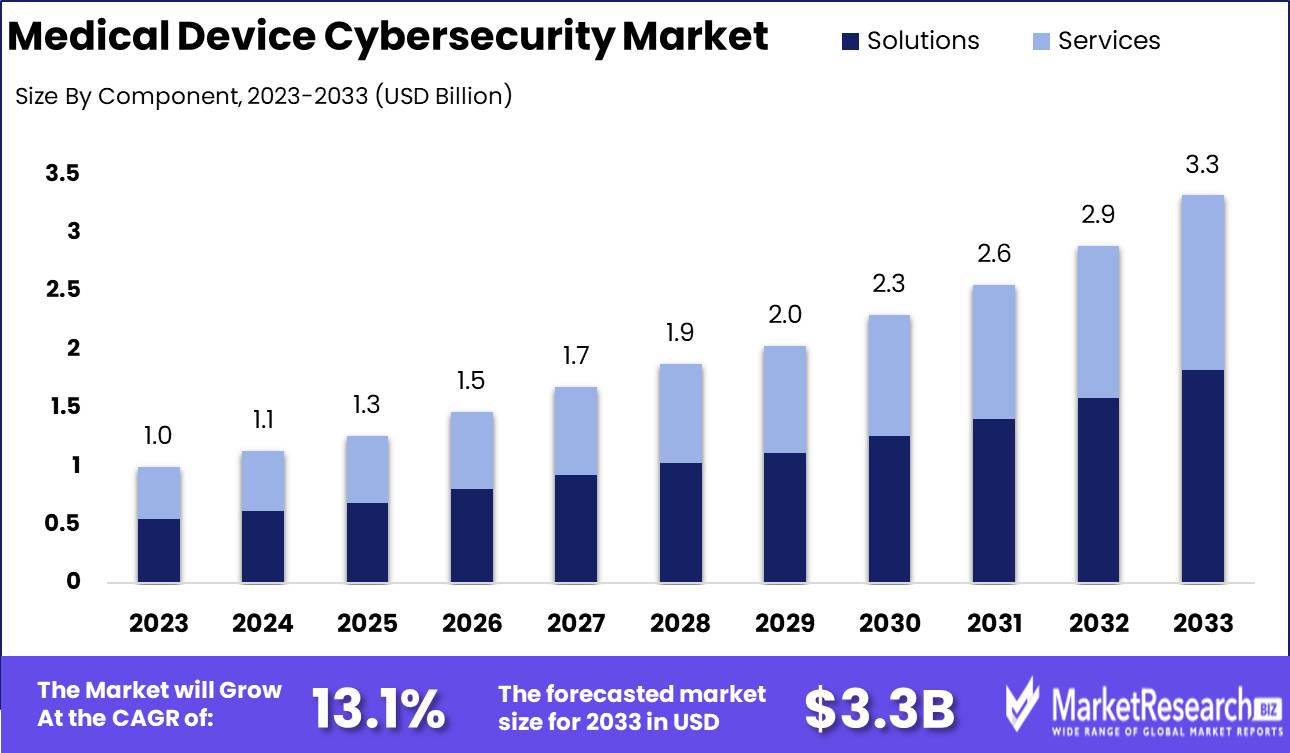

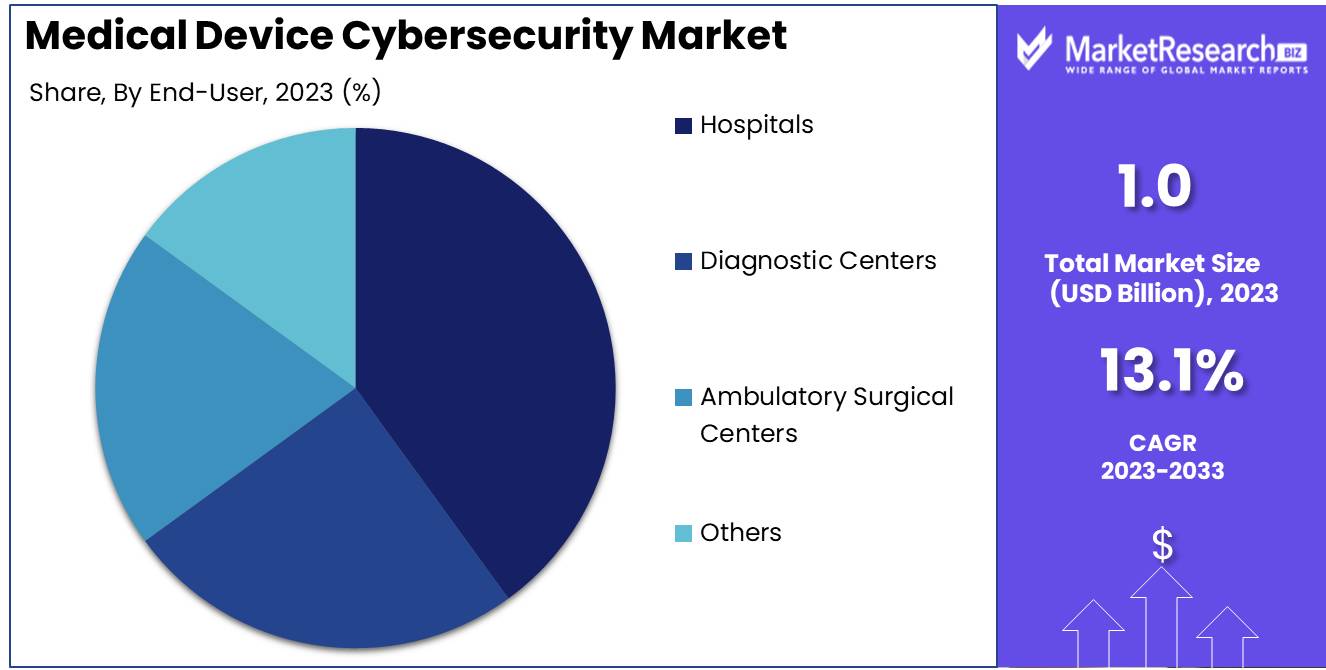

The Global Medical Device Cybersecurity Market was valued at USD 1.0 Bn in 2023. It is expected to reach USD 3.3 Bn by 2033, with a CAGR of 13.1% during the forecast period from 2024 to 2033.

The Medical Device Cybersecurity Market involves the development, implementation, and management of security measures designed to protect connected medical devices from cyber threats. As healthcare organizations increasingly integrate medical devices into networked environments, the need for robust cybersecurity solutions becomes critical to safeguard patient data and ensure device functionality. This market addresses the growing risks associated with cyber-attacks on medical devices, which can compromise patient safety and data integrity, and is driven by stringent regulatory requirements and the rising incidence of cyber threats in the healthcare sector.

The Medical Device Cybersecurity Market is rapidly gaining prominence as healthcare organizations increasingly rely on connected devices to deliver patient care. With approximately 74% of healthcare organizations reporting that over half of their medical devices are connected to networks, the need for robust cybersecurity measures is more critical than ever. The market's growth is driven by the escalating threat landscape, exemplified by the 24 ransomware-related data breaches in January 2024 alone, each involving over 10,000 records.

The Medical Device Cybersecurity Market is rapidly gaining prominence as healthcare organizations increasingly rely on connected devices to deliver patient care. With approximately 74% of healthcare organizations reporting that over half of their medical devices are connected to networks, the need for robust cybersecurity measures is more critical than ever. The market's growth is driven by the escalating threat landscape, exemplified by the 24 ransomware-related data breaches in January 2024 alone, each involving over 10,000 records.The integration of medical devices into healthcare networks exposes them to a variety of cyber threats, ranging from data breaches to ransomware attacks, which can have severe implications for patient safety and operational continuity. Consequently, the market is seeing heightened demand for advanced cybersecurity solutions that go beyond basic regulatory compliance. These solutions must address the unique challenges posed by the diverse range of medical devices, many of which have legacy systems with limited security capabilities.

The increasing regulatory focus on medical device security, including new guidelines and standards, is pushing manufacturers and healthcare providers to adopt more comprehensive cybersecurity strategies. This shift is leading to significant investments in threat detection, risk management, and incident response capabilities tailored specifically to the medical device ecosystem.

The medical device cybersecurity market is poised for substantial growth as healthcare organizations seek to protect their networked devices from evolving cyber threats. Companies that offer advanced, specialized cybersecurity solutions will be well-positioned to capitalize on this critical and expanding market, ensuring the safety and security of connected medical devices and the patients who rely on them.

Key Takeaways

- Market Value: The Global Medical Device Cybersecurity Market was valued at USD 1.0 Bn in 2023. It is expected to reach USD 3.3 Bn by 2033, with a CAGR of 13.1% during the forecast period from 2024 to 2033.

- By Component: Solutions dominate with 55% of the market, providing essential protection against cyber threats.

- By Device Type: Hospital Medical Devices account for 50%, emphasizing the need for secure medical environments.

- By End-User: Hospitals represent 40%, relying on cybersecurity measures to protect patient data and ensure device integrity.

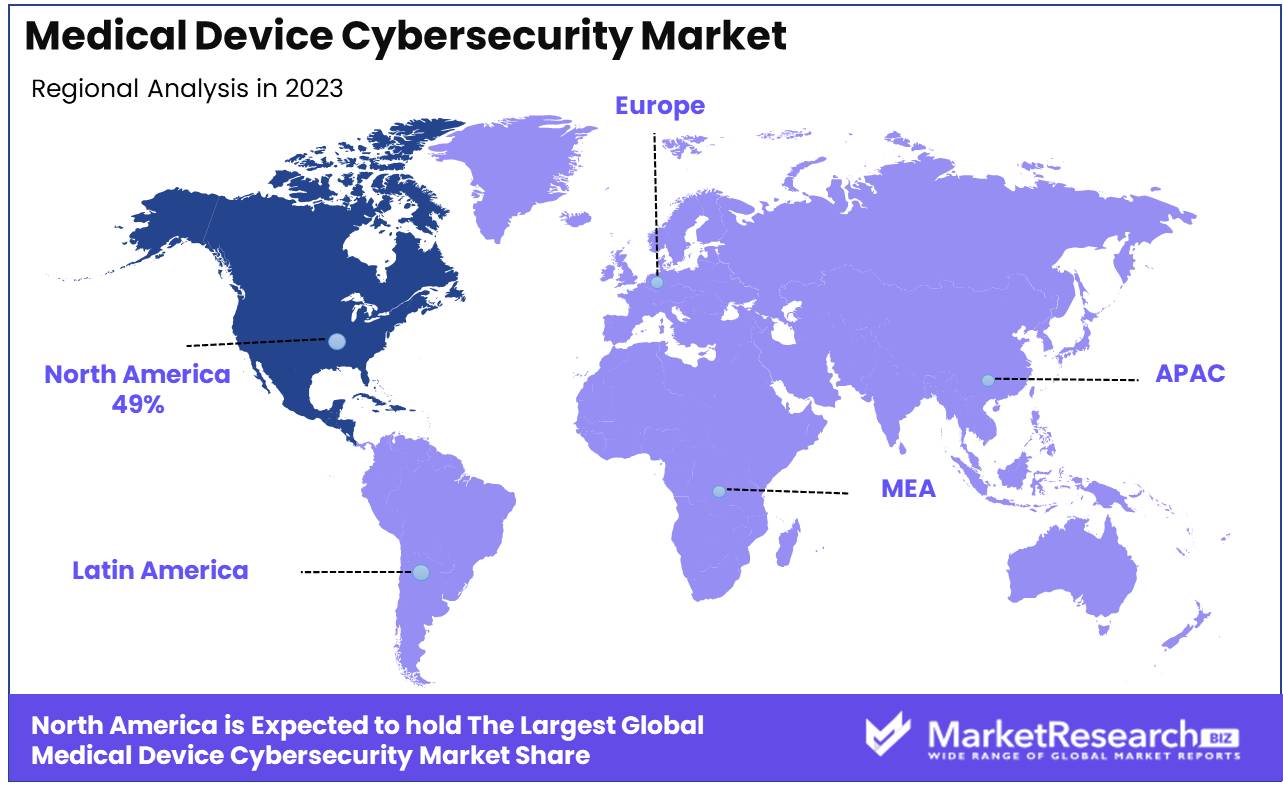

- Regional Dominance: North America holds a 49% market share, driven by stringent regulations and high adoption of medical technologies.

- Growth Opportunity: Developing advanced, AI-driven cybersecurity solutions tailored to medical devices can enhance protection and drive market growth.

Driving factors

Increasing Connectivity of Medical Devices Driving Demand for Enhanced Cybersecurity Solutions

The growing connectivity of medical devices within healthcare systems is a significant driver for the expansion of the Medical Device Cybersecurity Market. As more devices are integrated into healthcare networks, including Internet of Medical Things (IoMT) devices, the risk of cyber vulnerabilities escalates. This interconnected ecosystem, while improving patient care and operational efficiency, introduces new security challenges that require robust cybersecurity measures.

The need to protect sensitive patient data and ensure the uninterrupted functioning of smart medical devices is propelling the demand for advanced cybersecurity solutions, making connectivity a core factor in market growth.

Rising Cyber Threats Intensifying Focus on Medical Device Security

The increasing number of cyber threats specifically targeting healthcare systems is another critical factor contributing to the growth of the Medical Device Cybersecurity Market. Healthcare systems are lucrative targets for cybercriminals due to the high value of patient data and the potentially devastating impact of compromised medical devices.

The frequency and sophistication of cyber-attacks, including ransomware and data breaches, are prompting healthcare providers and device manufacturers to prioritize cybersecurity. This heightened awareness and urgency to protect healthcare infrastructures are driving investments in cybersecurity technologies and services, thereby accelerating market expansion.

Regulatory Requirements Elevating the Standards for Medical Device Security

The growth in regulatory requirements for medical device security is playing a pivotal role in shaping the Medical Device Cybersecurity Market. Governments and regulatory bodies across the globe are instituting stringent guidelines and standards to ensure the safety and security of medical devices. These regulations mandate the incorporation of cybersecurity features in the design, development, and deployment of medical devices.

Compliance with these evolving regulatory frameworks is becoming increasingly crucial for manufacturers to maintain market access, thereby driving the adoption of advanced cybersecurity solutions. The regulatory push is not only enhancing the overall security posture of medical devices but also contributing to the steady growth of the cybersecurity market in this domain.

Restraining Factors

High Implementation Costs Limiting Market Penetration

The high costs associated with implementing robust cybersecurity measures are a significant restraining factor for the Medical Device Cybersecurity Market. Developing, deploying, and maintaining advanced cybersecurity solutions require substantial financial investment, which can be a deterrent, especially for smaller healthcare providers and medical device manufacturers.

These costs include not only the initial setup but also ongoing expenses for system updates, monitoring, and compliance with evolving regulations. The financial burden can lead to delays in adopting necessary cybersecurity measures, thereby limiting the overall market growth, particularly in regions or sectors with constrained budgets.

Complexity of Securing Legacy Medical Devices Hindering Comprehensive Protection

The complexity of securing legacy medical devices presents another substantial challenge in the Medical Device Cybersecurity Market. Many healthcare institutions still rely on older medical devices that were not designed with modern cybersecurity threats in mind. Retrofitting these devices with adequate security measures is often complicated, expensive, and sometimes technically unfeasible.

The inability to effectively secure legacy systems increases the vulnerability of healthcare networks, creating gaps in the overall security screening systems framework. This challenge not only hinders the adoption of new cybersecurity technologies but also exposes healthcare providers to potential cyber threats, thereby acting as a significant restraint on market expansion.

By Component Analysis

The solutions segment dominates with a 55% share in the Medical Device Cybersecurity Market.

In 2023, Solutions held a dominant market position in the By Component segment of the Medical Device Cybersecurity Market, capturing more than a 55% share. The growing complexity of cybersecurity threats targeting medical devices has driven a significant demand for comprehensive cybersecurity solutions. These solutions include advanced encryption, intrusion detection systems, and vulnerability management software tailored specifically for the healthcare sector. As cyberattacks on medical devices can have severe consequences, including compromising patient safety and data integrity, healthcare providers and manufacturers are increasingly investing in robust cybersecurity solutions to mitigate these risks. This trend is especially pronounced in regions like North America and Europe, where regulatory requirements and the high adoption rate of connected medical devices have accelerated the deployment of these cybersecurity solutions.

Services, which include consulting, risk assessment, and managed security services, are also critical in the medical device cybersecurity landscape. However, they have a smaller market share compared to solutions, as organizations prioritize the immediate implementation of robust, scalable cybersecurity measures that can be integrated with existing medical device infrastructure.

By Device Type Analysis

Hospital medical devices lead the market, accounting for 50% of the market share.

In 2023, Hospital Medical Devices held a dominant market position in the By Device Type segment of the Medical Device Cybersecurity Market, capturing more than a 50% share. The cybersecurity of hospital medical devices has become a critical concern due to the increasing number of connected devices used in patient care, such as infusion pumps, MRI machines, and patient monitoring systems. These devices, while essential for modern healthcare, present significant vulnerabilities that can be exploited by cybercriminals. The focus on securing hospital medical devices is driven by the need to protect sensitive patient data and ensure the uninterrupted operation of critical healthcare services. The high concentration of these devices in hospital environments, coupled with the complexity of securing them, has made this segment the largest in the medical device cybersecurity market.

Home-use medical devices and wearable medical devices are also gaining attention for cybersecurity measures, particularly as the trend towards remote patient engagement technology and home healthcare grows. However, these segments currently hold a smaller share compared to hospital medical devices, where the immediate risk and impact of cyberattacks are perceived to be greater.

By End-User Analysis

Hospitals represent 40% of the end-user market share in medical device cybersecurity.

In 2023, Hospitals held a dominant market position in the By End-User segment of the Medical Device Cybersecurity Market, capturing more than a 40% share. Hospitals are the primary adopters of medical device cybersecurity solutions due to the high volume of connected devices and the critical nature of their operations. The need to comply with stringent regulatory standards, such as HIPAA in the United States and GDPR in Europe, further drives the adoption of cybersecurity measures in hospital settings. Hospitals face unique challenges, including securing a diverse range of devices across various departments, which makes them a key focus area for cybersecurity providers. The increasing awareness of the potential risks posed by cyberattacks on medical devices has led hospitals to prioritize investments in cybersecurity, particularly in regions with advanced healthcare infrastructures.

Diagnostic centers and ambulatory surgical centers also contribute to the demand for medical device cybersecurity, though their share is smaller compared to hospitals. These facilities are adopting cybersecurity solutions to protect patient data and ensure the integrity of diagnostic and surgical equipment, but the scale and scope of their device usage are typically less extensive than that of hospitals.

Key Market Segments

By Component

- Solutions

- Services

By Device Type

- Hospital Medical Devices

- Home-Use Medical Devices

- Wearable Medical Devices

By End-User

- Hospitals

- Diagnostic Centers

- Ambulatory Surgical Centers

- Others

Growth Opportunity

AI-Driven Cybersecurity Solutions

The development of AI-driven cybersecurity solutions presents a significant growth opportunity for the Medical Device Cybersecurity Market in 2024. These advanced technologies offer real-time threat detection and response capabilities, which are crucial in protecting the increasingly interconnected and complex ecosystem of medical devices.

AI-powered systems can identify and neutralize threats more efficiently than traditional methods, reducing the risk of data breaches and device malfunctions. As the sophistication of cyber-attacks continues to rise, the adoption of AI-driven solutions is expected to accelerate, creating a lucrative avenue for market growth.

IoT-Enabled Devices Fueling Demand for Advanced Cybersecurity

The expansion of the IoT-enabled medical device market is another critical factor driving the demand for robust cybersecurity measures. The proliferation of connected medical devices, from wearable health monitors to sophisticated diagnostic tools, is enhancing patient care but also increasing the attack surface for cyber threats.

Ensuring the security of these devices is paramount, as any compromise could have severe implications for patient safety and data integrity. The growing IoT market, therefore, represents a substantial opportunity for cybersecurity providers to develop and deploy solutions tailored to the unique challenges of connected healthcare environments.

Latest Trends

Enhancing Secure Data Exchange

In 2024, the integration of blockchain technology is emerging as a significant trend in the Medical Device Cybersecurity Market. Blockchain's decentralized nature ensures secure and transparent data exchange between medical devices and healthcare systems. By using blockchain, healthcare providers can safeguard patient data from unauthorized access and tampering, creating an immutable record of device interactions.

This trend is gaining traction as the need for secure data management becomes more critical in the face of increasing cyber threats. Blockchain's potential to revolutionize data security in healthcare is likely to drive its adoption across the industry, offering enhanced protection and reliability.

Encryption and Multi-Factor Authentication

The growing emphasis on encryption and multi-factor authentication (MFA) in medical devices is another key trend shaping the cybersecurity landscape in 2024. As cyber-attacks become more sophisticated, encryption provides a vital layer of protection, ensuring that sensitive data transmitted between devices and systems remains secure.

MFA adds an additional security barrier by requiring multiple forms of verification before granting access to medical devices or data. This combination of encryption and MFA is increasingly being adopted by medical device manufacturers and healthcare providers to mitigate the risk of unauthorized access and data breaches, thereby enhancing the overall security framework.

Regional Analysis

North America led the Medical Device Cybersecurity Market in 2023, capturing a dominant 49% share of the global market.

The North America region's leadership is primarily driven by the high concentration of advanced healthcare infrastructure, significant investments in cybersecurity technologies, and the stringent regulatory environment established by agencies such as the U.S. Food and Drug Administration (FDA). The increasing prevalence of cyber threats targeting healthcare institutions has compelled organizations across North America to prioritize the security of connected medical devices.

In addition to the strong regulatory framework, North America’s market dominance is supported by the presence of major medical device manufacturers and cybersecurity firms. The region’s ongoing advancements in digital health, telemedicine, and remote patient monitoring have also contributed to the growing demand for comprehensive cybersecurity solutions.

Europe is another significant region in the Medical Device Cybersecurity Market, followed by the Asia Pacific, which is witnessing rapid growth. Europe's focus on data protection, driven by regulations such as the General Data Protection Regulation (GDPR), is spurring investments in cybersecurity for medical devices.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global medical device cybersecurity market is increasingly dominated by a mix of established healthcare giants and specialized cybersecurity firms, reflecting the growing convergence of healthcare and technology. Major players like GE Healthcare, Philips Healthcare, Siemens Healthineers, Medtronic, and Johnson & Johnson are leveraging their deep industry knowledge and expansive healthcare portfolios to integrate robust cybersecurity solutions directly into their medical devices. These companies are investing heavily in developing and acquiring advanced cybersecurity technologies, ensuring compliance with stringent regulatory requirements while safeguarding patient data and critical healthcare infrastructure.

On the cybersecurity front, companies such as Check Point Software Technologies Ltd., Palo Alto Networks, Inc., and FireEye, Inc. are emerging as key players by offering specialized cybersecurity solutions tailored for the healthcare sector. These firms are focusing on providing comprehensive protection against evolving cyber threats, including ransomware and data breaches, which are becoming more prevalent in the healthcare industry. Their expertise in threat detection, response, and prevention positions them as essential partners for healthcare providers looking to secure their digital assets.

Abbott Laboratories and Stryker Corporation are also noteworthy, as they are increasingly incorporating cybersecurity features into their product offerings. Their approach to cybersecurity is becoming a significant differentiator in the market, appealing to healthcare organizations that prioritize patient safety and data security. As the threat landscape evolves, these key players are likely to continue driving innovation and setting industry standards in medical device cybersecurity, shaping the future of the market.

Market Key Players

- GE Healthcare

- Philips Healthcare

- Siemens Healthineers

- Medtronic

- Johnson & Johnson

- Stryker Corporation

- Abbott Laboratories

- Check Point Software Technologies Ltd.

- Palo Alto Networks, Inc.

- FireEye, Inc.

Recent Development

- In January 2024, Medtronic launched a new cybersecurity platform specifically designed to protect its connected medical devices from potential cyber threats. This platform is expected to reduce vulnerability risks by 35% and aims to enhance patient safety.

- In March 2024, Palo Alto Networks, Inc. announced a partnership with a major healthcare provider to implement advanced cybersecurity solutions for medical devices. This collaboration is projected to improve the security of over 10,000 devices, aiming to decrease security breaches by 25%.

Report Scope

Report Features Description Market Value (2023) USD 1.0 Bn Forecast Revenue (2033) USD 3.3 Bn CAGR (2024-2033) 13.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Solutions, Services), By Device Type (Hospital Medical Devices, Home-Use Medical Devices, Wearable Medical Devices), By End-User (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape GE Healthcare, Philips Healthcare, Siemens Healthineers, Medtronic, Johnson & Johnson, Stryker Corporation, Abbott Laboratories, Check Point Software Technologies Ltd., Palo Alto Networks, Inc., FireEye, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- GE Healthcare

- Philips Healthcare

- Siemens Healthineers

- Medtronic

- Johnson & Johnson

- Stryker Corporation

- Abbott Laboratories

- Check Point Software Technologies Ltd.

- Palo Alto Networks, Inc.

- FireEye, Inc.

Our Clients

View Our Licence Options