Liquid Fertilizers Market By Source (Organic, Synthetic), By Nutrient Type (Nitrogen, Potassium, Phosphate, Micronutrients, Complex, Straight), By Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, Others), By Application (Fertigation, Foliar, Soil, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

5578

-

July 2024

-

176

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

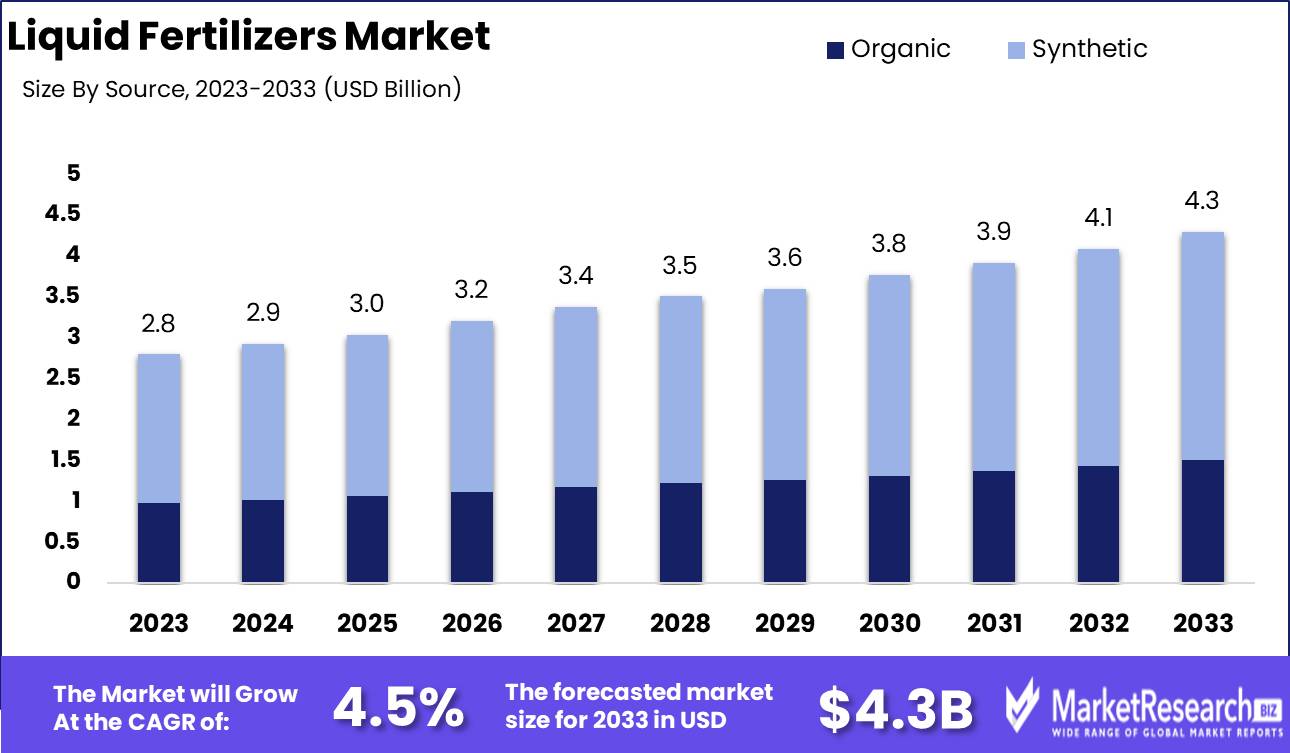

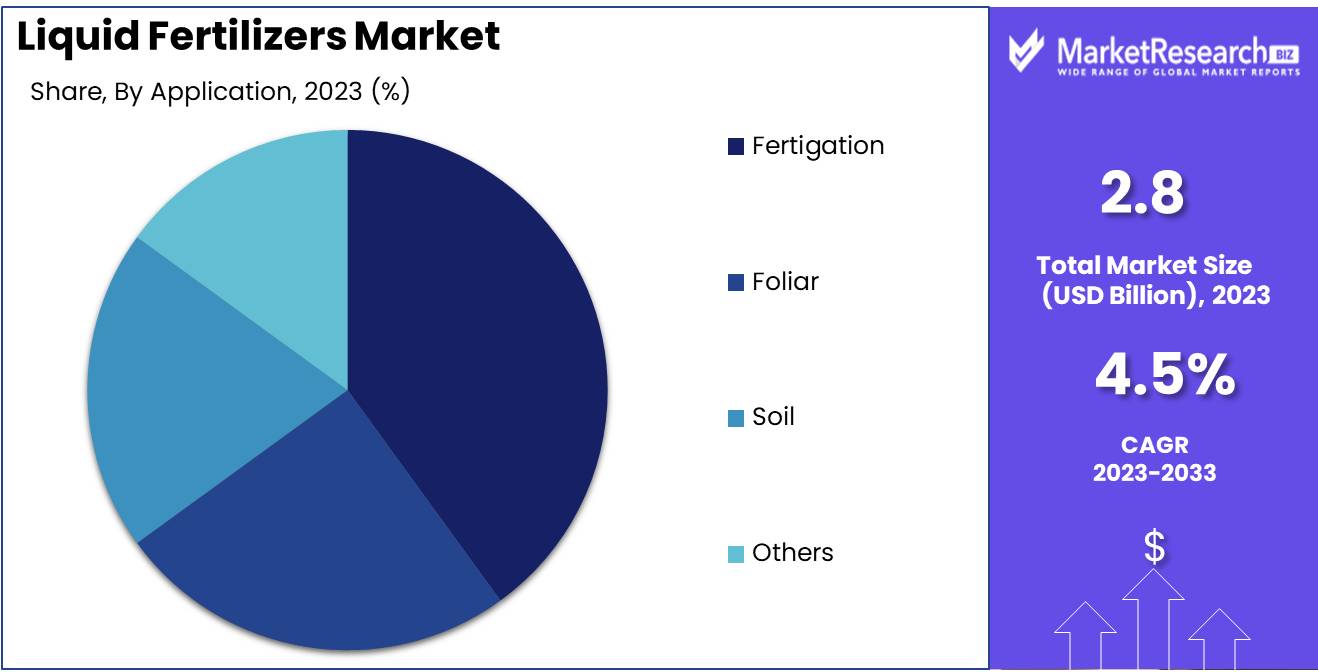

The Global Liquid Fertilizers Market was valued at USD 2.8 Bn in 2023. It is expected to reach USD 4.3 Bn by 2033, with a CAGR of 4.5% during the forecast period from 2024 to 2033.

The Liquid Fertilizers Market involves the production and distribution of nutrient-rich liquid solutions designed to enhance soil fertility and crop yield. These fertilizers, which include nitrogen, phosphorus, potassium, and micronutrient blends, offer advantages such as uniform nutrient distribution, easy application, and quick absorption by plants. Market growth is driven by the increasing demand for high-efficiency agricultural inputs, the need for sustainable farming practices, and advancements in precision agriculture technologies.

Key players are focusing on innovative formulations and delivery systems to improve efficacy and meet the evolving needs of modern agriculture, ensuring optimal crop productivity and sustainability. The Liquid Fertilizers Market is experiencing robust growth, driven by the increasing demand for efficient and sustainable agricultural practices. Liquid fertilizers, comprising nitrogen, phosphorus, potassium, and micronutrient blends, offer significant advantages such as uniform nutrient distribution, ease of application, and rapid plant absorption.

The market's expansion is further fueled by advancements in precision agriculture technologies, which enhance the effective application of these fertilizers, ensuring optimal crop productivity and sustainability. Price points for liquid fertilizers vary, with 1 gallon typically costing between $30 to $80, and most products priced around $40-$50. This variance reflects differences in nutrient composition and brand reputation, indicating a market sensitive to quality and performance metrics.

High nitrogen content, ranging from 20% to 32%, is a notable characteristic of many liquid fertilizers, underscoring their efficacy in boosting crop yields. As global food demand rises and agricultural land becomes increasingly limited, the need for high-efficiency inputs like liquid fertilizers becomes paramount. Key players in this market are focusing on innovative formulations and advanced delivery systems to improve nutrient uptake and reduce environmental impact.

Strategically, companies are investing in research and development to create next-generation liquid fertilizers that cater to the specific needs of various crops and soil types. Strategic partnerships and collaborations are enhancing market reach and product offerings. As regulatory frameworks emphasize sustainable farming practices, the adoption of liquid fertilizers is expected to rise, presenting substantial growth opportunities for market leaders.

Key Takeaways

- Market Value: The Global Liquid Fertilizers Market was valued at USD 2.8 Bn in 2023. It is expected to reach USD 4.3 Bn by 2033, with a CAGR of 4.5% during the forecast period from 2024 to 2033.

- By Source: Synthetic fertilizers dominate the market, holding a significant 65% share, preferred for their consistency in nutrient composition and immediate impact on crop growth.

- By Nutrient Type: Nitrogen is the primary nutrient utilized, comprising 30% of the market, essential for plant growth and commonly used in high-yield farming.

- By Crop Type: Cereals & Grains are the largest crop category benefiting from liquid fertilizers, accounting for 35%, underscoring their importance in staple food production.

- By Application: Fertigation leads the application methods with 40%, reflecting its efficiency in nutrient delivery and water usage, especially in large-scale agriculture.

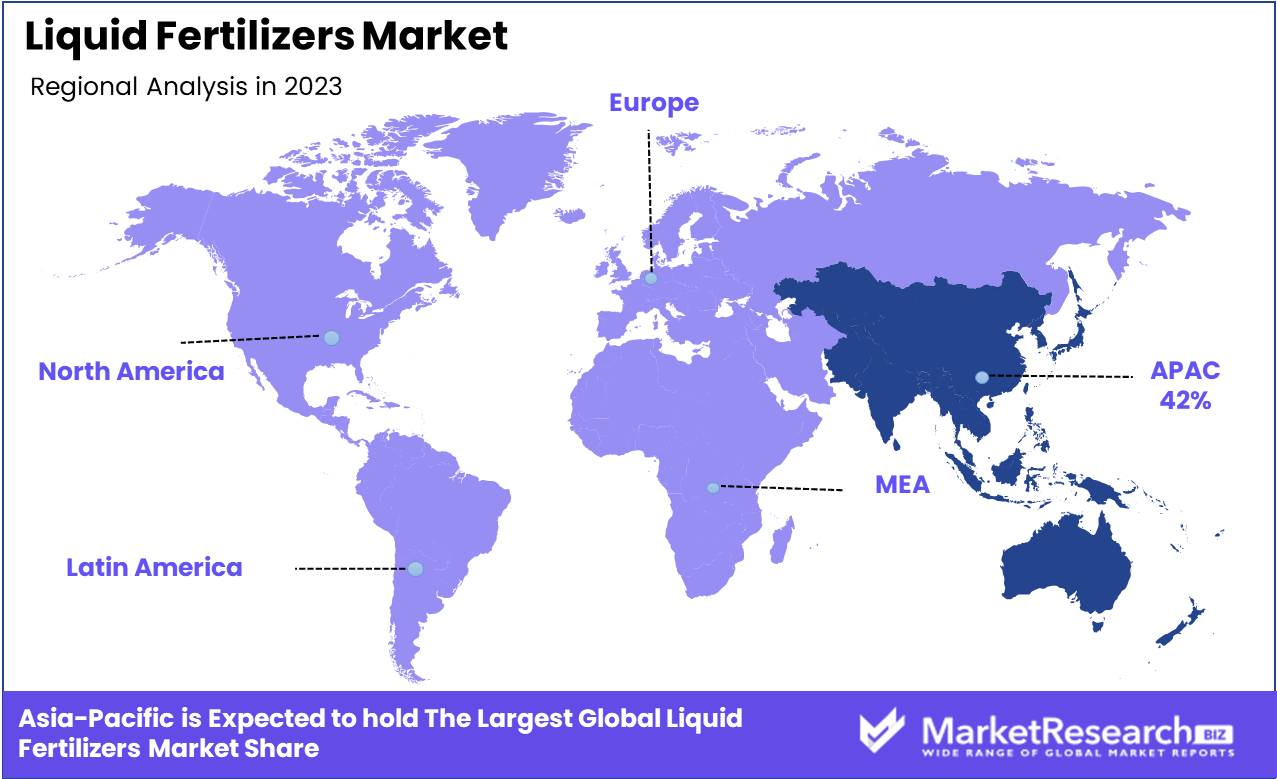

- Regional Dominance: Asia Pacific holds a dominant 42% share of the market, driven by intensive agricultural practices and the need to maximize crop yields in the region.

Driving factors

Increasing Demand for High-Efficiency Fertilizers

The demand for high-efficiency fertilizers is a major driver of the liquid fertilizers market. Traditional granular fertilizers often suffer from issues such as nutrient leaching and uneven application, leading to suboptimal crop yields. Liquid fertilizers, in contrast, offer more efficient nutrient delivery systems. They are easily absorbed by plants and can be applied directly to the root zone or through foliar feeding, ensuring that nutrients are readily available.

This efficiency reduces waste and increases crop productivity, which is particularly important in regions facing agricultural land scarcity and environmental challenges. The rising preference for high-efficiency fertilizers is therefore significantly boosting the demand for liquid fertilizers globally.

Growth in Precision Agriculture Practices

The adoption of precision agriculture practices is another critical factor contributing to the growth of the liquid fertilizers market. Precision agriculture involves the use of advanced technologies such as GPS, remote sensing, and data analytics to optimize field-level management of crops. Liquid fertilizers are well-suited to these practices as they can be precisely applied in controlled amounts, tailored to the specific needs of different crops and soil conditions.

This targeted application enhances nutrient use efficiency and reduces environmental impact. As farmers increasingly adopt precision agriculture to improve yield and sustainability, the demand for compatible inputs like liquid fertilizers is expected to rise.

Rising Global Food Demand

Rising global food demand is a fundamental driver of the liquid fertilizers market. The global population is expected to reach 9.7 billion by 2050, significantly increasing the demand for food. To meet this demand, agricultural productivity must be enhanced, which necessitates the use of efficient fertilizers. Liquid fertilizers, with their ability to quickly provide essential phytonutrients, play a crucial role in increasing crop yields.

The growing preference for high-value crops, such as fruits and vegetables, which often require intensive nutrient management, further boosts the demand for liquid fertilizers. As global fresh food demand continues to rise, so too will the need for effective fertilization solutions, driving market growth.

Restraining Factors

High Production and Storage Costs

High production and storage costs present significant challenges to the growth of the liquid fertilizers market. The manufacturing of liquid fertilizers involves complex processes that require advanced technology and high-quality raw materials, leading to higher production costs compared to traditional granular fertilizers. Additionally, the storage and transportation of liquid fertilizers necessitate specialized equipment and infrastructure to prevent leakage and ensure stability, further increasing costs.

These financial burdens can limit the affordability and accessibility of liquid fertilizers, particularly for small-scale farmers and in regions with limited agricultural budgets. To mitigate these challenges, companies need to focus on improving production efficiency, scaling operations, and exploring cost-effective storage solutions. Reducing these costs is essential for making liquid fertilizers more competitive and widely adopted.

Environmental Concerns and Regulations

Environmental concerns and stringent regulations also pose significant hurdles for the liquid fertilizers market. The use of fertilizers, including liquid variants, is increasingly scrutinized due to their potential impact on soil health, water quality, and greenhouse gas emissions. Regulatory bodies across the globe are implementing stricter guidelines to mitigate these environmental impacts, which can increase the compliance costs for manufacturers. For example, regulations may require the use of more environmentally friendly formulations or mandate specific application practices to reduce runoff and pollution.

Compliance with these regulations can be resource-intensive and may slow down the introduction of new products to the market. However, these challenges also present opportunities for innovation. Companies that develop eco-friendly liquid fertilizers and sustainable application methods can gain a competitive edge and meet the growing demand for environmentally responsible agricultural inputs.

By Source Analysis

Synthetic dominated the By Source segment of the Liquid Fertilizers Market in 2023, capturing more than a 65% share.

In 2023, Synthetic held a dominant market position in the By Source segment of the Liquid Fertilizers Market, capturing more than a 65% share. The dominance of synthetic liquid fertilizers is driven by their consistent nutrient composition, high nutrient concentration, and immediate availability for plant uptake, which ensures rapid and predictable results. These fertilizers are extensively used in large-scale commercial farming operations due to their ease of application and ability to support high-yield crop production.

Organic liquid fertilizers, derived from natural sources such as compost, manure, and plant extracts, offer benefits in terms of improving soil health and promoting sustainable agriculture. They are increasingly favored by organic farmers and those seeking to reduce chemical inputs. However, organic liquid fertilizers often have lower nutrient concentrations and slower nutrient release rates compared to synthetic alternatives, which can limit their immediate effectiveness.

By Nutrient Type Analysis

Nitrogen dominated the By Nutrient Type segment of the Liquid Fertilizers Market in 2023, capturing more than a 30% share.

In 2023, Nitrogen held a dominant market position in the By Nutrient Type segment of the Liquid Fertilizers Market, capturing more than a 30% share. This leadership is driven by nitrogen's crucial role in promoting plant growth and increasing crop yields. Nitrogen is an essential component of chlorophyll, amino acids, and proteins, making it vital for photosynthesis and overall plant health. The widespread use of nitrogen-based liquid fertilizers in various crops, including cereals, grains, and vegetables, underscores their importance in modern agriculture. Additionally, the ability of liquid nitrogen fertilizers to be rapidly absorbed by plants ensures immediate nutrient availability, which supports their prominent market position.

Potassium is another vital nutrient that significantly contributes to the market, aiding in water regulation, enzyme activation, and disease resistance in plants. Liquid potassium fertilizers are particularly important for improving fruit quality and increasing the overall resilience of crops. Despite their critical role, potassium fertilizers hold a smaller market share compared to nitrogen due to their more specialized application.

Phosphate fertilizers are essential for root development and energy transfer within plants. Liquid phosphate fertilizers enhance the early growth stages of crops and are crucial for flowering and fruiting processes. While their importance is undeniable, their market share is less than that of nitrogen fertilizers, partly because phosphorus is often required in smaller quantities.

Micronutrients such as iron, zinc chemical, and manganese are necessary for various physiological functions in plants, albeit in smaller amounts. Liquid formulations of micronutrients are gaining popularity due to their ease of application and quick absorption. However, their market share remains smaller due to the lower overall demand compared to macronutrients like nitrogen.

Complex fertilizers, which combine multiple nutrients in a single formulation, offer a balanced approach to plant nutrition. These fertilizers are valued for their convenience and ability to address multiple nutrient deficiencies simultaneously. Despite their benefits, the market share of complex fertilizers is limited compared to straight fertilizers due to their higher cost and specific application needs.

Straight fertilizers contain a single nutrient and are widely used to correct specific nutrient deficiencies in crops. The simplicity and targeted application of straight fertilizers make them popular among farmers. However, their market share is divided among various nutrient types, with nitrogen leading due to its fundamental role in plant growth.

By Crop Type Analysis

Cereals & Grains dominated the By Crop Type segment of the Liquid Fertilizers Market in 2023, capturing more than a 35% share.

In 2023, Cereals & Grains held a dominant market position in the By Crop Type segment of the Liquid Fertilizers Market, capturing more than a 35% share. This leading position is driven by the extensive cultivation of staple crops such as wheat, rice, maize, and barley, which are fundamental to global food security. Liquid fertilizers are extensively used in cereal and grain farming due to their ability to provide rapid and efficient nutrient uptake, essential for achieving high yields and meeting the demands of a growing population. The widespread application of liquid fertilizers in these crops supports their strong market position, as they enhance growth rates, improve resilience, and increase productivity.

Fruits & Vegetables represent a significant segment within the liquid fertilizers market. The high-value nature of these crops necessitates precise and balanced nutrient application to maximize quality and yield. Liquid fertilizers offer the advantage of targeted nutrient delivery, which is crucial for the intensive cultivation methods used in fruit and vegetable farming. Although the market share of this segment is substantial, it remains smaller compared to cereals and grains due to the relatively lower global acreage dedicated to fruit and vegetable production.

Oilseeds & Pulses, including crops such as soybeans, sunflower, canola, and lentils, also play a vital role in the liquid fertilizers market. These crops are important sources of oils and proteins, and their cultivation benefits from the efficient nutrient delivery provided by liquid fertilizers. While the demand for oilseeds and pulses continues to grow, their market share is less than that of cereals and grains due to the differences in scale and intensity of cultivation.

Others, encompassing a variety of specialty crops such as herbs, spices, and ornamental plants, utilize liquid fertilizers to enhance growth and quality. These crops, while important in niche markets, contribute a smaller overall share to the liquid fertilizers market compared to the major crop types. However, the high-value nature of these crops ensures that liquid fertilizers remain a critical input for optimizing their production.

By Application Analysis

Fertigation dominated the By Application segment of the Liquid Fertilizers Market in 2023, capturing more than a 40% share.

In 2023, Fertigation held a dominant market position in the By Application segment of the Liquid Fertilizers Market, capturing more than a 40% share. This leading position is driven by the efficiency and precision that fertigation systems offer, allowing farmers to deliver nutrients directly to the plant roots through irrigation systems. The integration of liquid fertilizers with irrigation helps optimize nutrient uptake, reduce wastage, and improve crop yields. Fertigation is particularly effective in managing the nutrient needs of high-value crops and large-scale agricultural operations, supporting its widespread adoption and dominant market share.

Foliar application, where liquid fertilizers are sprayed directly onto plant leaves, provides a rapid method of nutrient delivery that can quickly address deficiencies and boost plant health. This method is especially beneficial for micronutrient applications and in situations where soil conditions limit nutrient availability. Despite its effectiveness, the market share of foliar application is smaller compared to fertigation due to its more labor-intensive nature and the need for frequent applications.

Soil application involves applying liquid fertilizers directly to the soil, either through surface spraying or soil injection. This method ensures that nutrients are readily available in the root zone, promoting healthy plant growth. Soil application is widely used in both conventional and organic farming practices, but its market share is limited by the lower efficiency compared to fertigation and the potential for nutrient leaching and runoff.

Others include various innovative and niche application methods such as hydroponics and aeroponics, where liquid fertilizers play a critical role in providing essential nutrients in controlled environments. While these methods offer significant advantages in specific contexts, their overall market share remains smaller due to their specialized nature and higher initial setup costs.

Key Market Segments

By Source

- Organic

- Synthetic

By Nutrient Type

- Nitrogen

- Potassium

- Phosphate

- Micronutrients

- Complex

- Straight

By Crop Type

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Others

By Application

- Fertigation

- Foliar

- Soil

- Others

Growth Opportunity

Expansion in Emerging Markets

The liquid fertilizers market in 2024 presents substantial opportunities for expansion in emerging markets. Regions such as Asia-Pacific, Latin America, and parts of Africa are experiencing rapid agricultural development and increased demand for efficient agricultural inputs. These regions have large agricultural sectors with a growing emphasis on improving crop yields and sustainability. By entering these markets, companies can tap into a vast and underserved customer base.

Strategic initiatives such as forming partnerships with local distributors, offering competitive pricing, and investing in education and training programs for farmers can facilitate market entry and growth. The potential for market expansion in these regions is immense, providing significant revenue opportunities for liquid fertilizer manufacturers.

Development of Sustainable and Eco-Friendly Formulations

The development of sustainable and eco-friendly formulations represents another critical opportunity for market growth in 2024. With increasing environmental regulations and consumer awareness about the impact of fertilizers on the environment, there is a growing demand for products that are both effective and environmentally friendly. Innovations in bio-based and organic liquid fertilizers, which minimize negative environmental impacts while enhancing soil health and crop productivity, are gaining traction.

Companies that focus on developing these sustainable formulations can meet the rising demand for eco-friendly agricultural inputs, differentiate themselves in the market, and potentially command premium pricing. This trend aligns with global sustainability goals and presents a lucrative growth avenue for forward-thinking manufacturers.

Latest Trends

Adoption of Foliar Feeding Techniques

A significant trend in the liquid fertilizers market for 2024 is the increasing adoption of foliar feeding techniques. Foliar feeding involves applying liquid fertilizers directly to the leaves of plants, allowing nutrients to be absorbed more quickly and efficiently than through soil application. This method is particularly beneficial for correcting nutrient deficiencies and boosting plant health during critical growth stages.

The adoption of foliar feeding is driven by its proven efficacy in enhancing crop yields and improving plant resilience against diseases and environmental stresses. As farmers seek more efficient and targeted fertilization methods, the demand for liquid fertilizers compatible with foliar application is expected to rise, driving market growth.

Integration of Liquid Fertilizers with Irrigation Systems

Another notable trend is the integration of liquid fertilizers with advanced irrigation systems, such as drip and sprinkler irrigation. This practice, known as fertigation, allows for the precise and uniform application of nutrients directly to the root zone of plants. By combining irrigation and fertilization, farmers can optimize water and nutrient use efficiency, leading to better crop performance and reduced environmental impact.

The growing adoption of smart irrigation technologies and precision agriculture practices is fueling this trend, as it offers significant advantages in terms of resource conservation and crop management. The integration of liquid fertilizers with irrigation systems is poised to enhance market demand and drive innovation in the sector.

Regional Analysis

The Liquid Fertilizers Market is dominated by the Asia Pacific region, which holds a significant 42% share of the global market.

The Liquid Fertilizers Market exhibits diverse regional trends and growth drivers. In the Asia Pacific region, which leads the market with a commanding 42% share, the growth is fueled by the extensive agricultural activities, increasing demand for high-yield crops, and the rising adoption of modern farming techniques. Major contributors to this market include China, India, and Japan, where significant agricultural output and government initiatives promoting sustainable farming practices drive the demand for liquid fertilizers.

In North America, the market is driven by advanced agricultural practices, high awareness of the benefits of liquid fertilizers, and the presence of key market players. The United States and Canada are leading contributors, with a strong focus on enhancing crop yields and soil fertility through the use of innovative fertilizer solutions. The adoption of precision farming techniques further supports market growth in this region.

Europe presents a steady demand for liquid fertilizers, supported by stringent regulations on sustainable agriculture and a growing preference for organic farming. Countries such as Germany, France, and the UK are at the forefront, with increasing investments in agricultural research and development and a strong emphasis on environmental sustainability.

The Middle East & Africa region is experiencing moderate growth in the liquid fertilizers market, driven by efforts to improve agricultural productivity and combat soil degradation. Key markets in this region include Saudi Arabia, South Africa, and Egypt, where government initiatives and investments in agricultural infrastructure are prominent.

Latin America also shows significant potential in the liquid fertilizers market, driven by extensive agricultural activities and increasing awareness about the benefits of liquid fertilizers. Brazil and Argentina are notable contributors, with large-scale farming operations and a rising trend towards sustainable agriculture practices.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global liquid fertilizers market is poised for robust growth in 2024, driven by the increasing demand for efficient and high-yield agricultural inputs. Key players in this market are leveraging their extensive product portfolios, global distribution networks, and innovative solutions to capture market share and drive growth.

Nutrien Ltd. and Yara International ASA are leading the market with their comprehensive range of liquid fertilizers designed to enhance crop productivity and soil health. Nutrien’s extensive global distribution network and Yara’s commitment to sustainable agricultural practices position them as market leaders.

ICL and K+S Aktiengesellschaft focus on specialty fertilizers that cater to specific crop needs. Their advanced formulations and focus on innovation ensure they meet the evolving demands of modern agriculture, promoting sustainable farming practices.

The Mosaic Company and EuroChem Group bring significant expertise in producing high-quality liquid fertilizers that support large-scale agricultural operations. Their emphasis on research and development allows them to introduce products that improve nutrient uptake efficiency and crop yields.

SQM SA and PhosAgro Group of Companies leverage their strong presence in the global market, particularly in regions with high agricultural activity. Their diverse product offerings cater to a wide range of crops, enhancing their market penetration.

Agrium Inc. and JSC Belaruskali emphasize the importance of balanced nutrient solutions, providing farmers with tailored products that meet specific agricultural needs. Their customer-centric approach and strong service networks enhance their competitive edge.

HELM AG and Borealis AG are noted for their innovative approaches and technological advancements in liquid fertilizer formulations. Their products are designed to meet the needs of precision agriculture, supporting sustainable and efficient farming practices.

Sinofert Holding Limited and Haifa Negev Technologies LTD focus on delivering high-quality fertilizers that promote sustainable agriculture. Their strong market presence in Asia and innovative product lines ensure they remain key players in the industry.

DFPCL and ARTAL Smart Agriculture and Plant Food Company Inc. contribute significantly with their specialized liquid fertilizers that address specific crop requirements. Their emphasis on research and product development ensures they meet the dynamic needs of the agricultural sector.

Market Key Players

- Nutrien Ltd.

- Yara

- ICL

- K+S Aktiengesellschaft

- SQM SA

- The Mosaic Company

- EuroChem Group

- Yara International ASA

- Agrium Inc

- Ptashcrop Corportation Of Sackatchewan Inc

- EuroChem Group

- (MOS)

- JSC Belaruskali

- HELM AG

- ICL-group ltd

- Borealis AG

- Sinofert holding limited

- K+S Aktiengesellschaft

- PhosAgro Group of Companies

- Haifa Negev technologies LTD

- DFPCL

- HELM AG AgroLiquid

- ARTAL SMART AGRICULTURE

- Seksaria Foundries Limited

- Nexus Cast.and Sneh Precast Products

Recent Development

- In April 2024, AgroTech Innovations released a new line of eco-friendly liquid fertilizers enhancing nutrient uptake and reducing environmental impact.

- In March 2024, GreenGrow Solutions introduced a bio-based liquid fertilizer targeting organic farming to boost crop yields sustainably.

Report Scope

Report Features Description Market Value (2023) USD 2.8 Bn Forecast Revenue (2033) USD 4.3 Bn CAGR (2024-2033) 4.5% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Organic, Synthetic), By Nutrient Type (Nitrogen, Potassium, Phosphate, Micronutrients, Complex, Straight), By Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, Others), By Application (Fertigation, Foliar, Soil, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Nutrien Ltd., Yara, ICL, K+S Aktiengesellschaft, SQM SA, The Mosaic Company, EuroChem Group, Yara International ASA, Agrium Inc, Ptashcrop Corportation Of Sackatchewan Inc, EuroChem Group, (MOS), JSC Belaruskali, HELM AG, ICL-group ltd, Borealis AG, Sinofert holding limited, K+S Aktiengesellschaft, PhosAgro Group of Companies, Haifa Negev technologies LTD, DFPCL, HELM AG AgroLiquid, ARTAL SMART AGRICULTURE and Plant Food Company Inc., Seksaria Foundries Limited, Nexus Cast.and Sneh Precast Products Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Nutrien Ltd.

- Yara

- ICL

- K+S Aktiengesellschaft

- SQM SA

- The Mosaic Company

- EuroChem Group

- Yara International ASA

- Agrium Inc

- Ptashcrop Corportation Of Sackatchewan Inc

- EuroChem Group

- (MOS)

- JSC Belaruskali

- HELM AG

- ICL-group ltd

- Borealis AG

- Sinofert holding limited

- K+S Aktiengesellschaft

- PhosAgro Group of Companies

- Haifa Negev technologies LTD

- DFPCL

- HELM AG AgroLiquid

- ARTAL SMART AGRICULTURE

- Seksaria Foundries Limited

- Nexus Cast.and Sneh Precast Products

Our Clients

View Our Licence Options