Laboratory Equipment Services Market By Equipment Type (Analytical Equipment, General Equipment, Specialty Equipment, Support Equipment), By Type (Repair & Maintenance, Calibration, Validation, Others), By Contract Type (Standard Service Contracts, Customized Service Contracts), By Service Provider (OEM (Original Equipment Manufacturer), Third-Party Service), By End-User (Research Institutions, Clinical Laboratories, Pharmaceutical Companies, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends

-

48548

-

July 2024

-

214

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

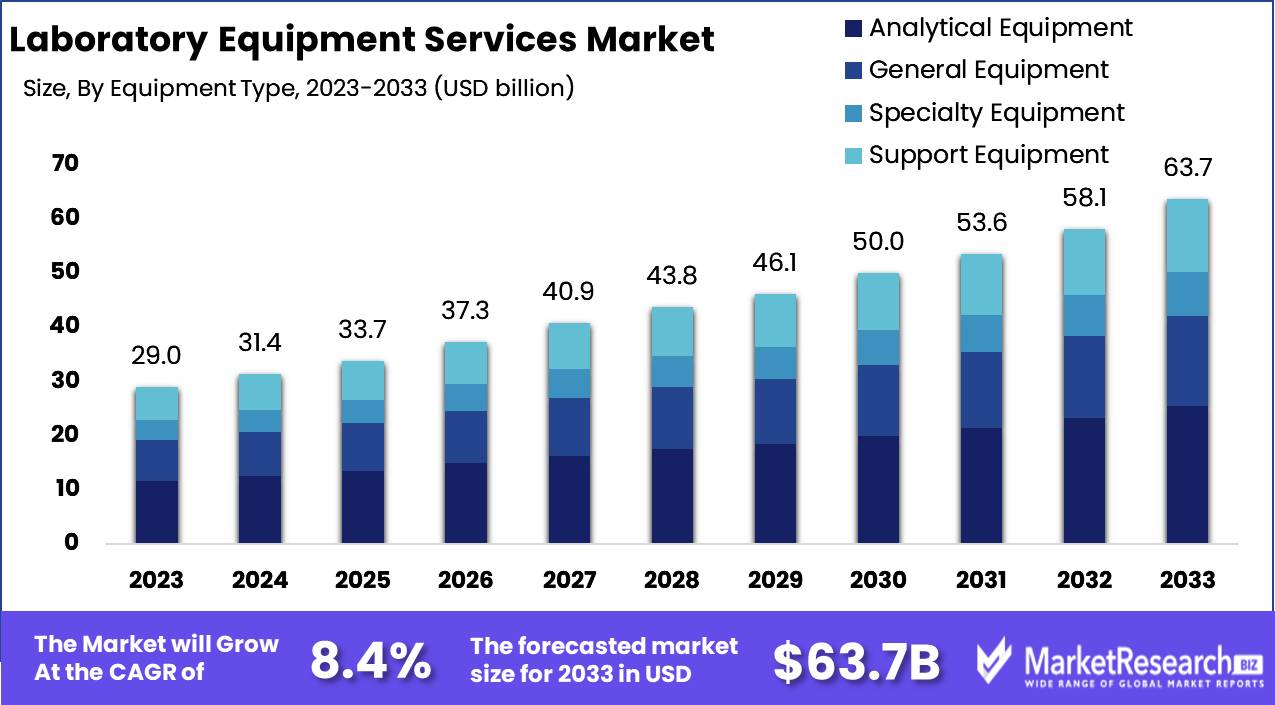

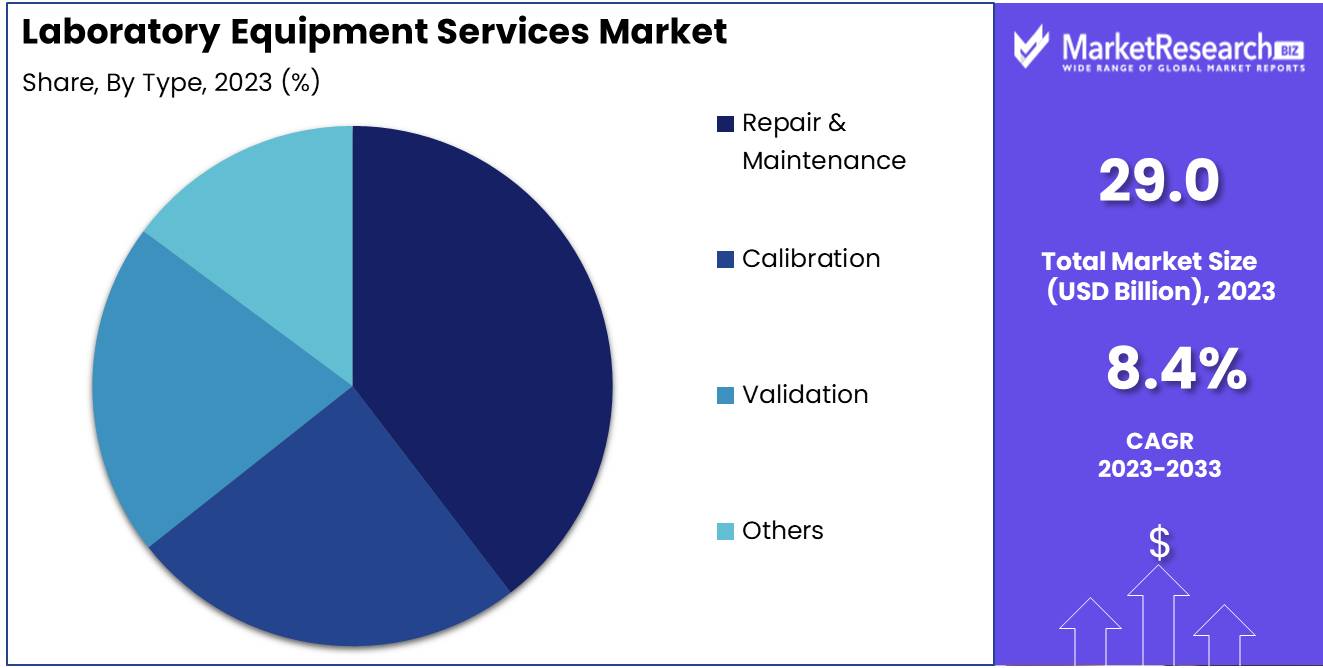

The Global Laboratory Equipment Services Market was valued at USD 29.0 Bn in 2023. It is expected to reach USD 63.7 Bn by 2033, with a CAGR of 8.4% during the forecast period from 2024 to 2033.

The Laboratory Equipment Services Market encompasses a range of services aimed at ensuring the optimal performance and longevity of laboratory instruments and devices. This market includes maintenance, calibration, validation, repair, and installation services provided by manufacturers, third-party service providers, and independent laboratories. These services are crucial for maintaining the accuracy, reliability, and compliance of laboratory equipment used across various industries, including healthcare, pharmaceuticals, biotechnology, and academic research. As technological advancements in laboratory equipment continue, the demand for specialized services to support these sophisticated instruments is growing, driving market expansion and innovation in service offerings.

The Laboratory Equipment Services Market is undergoing substantial growth, driven by the increasing complexity and criticality of laboratory instruments across various sectors, including healthcare, pharmaceuticals, biotechnology, and academic research. As laboratories strive to maintain high standards of accuracy, reliability, and regulatory compliance, the demand for comprehensive service solutions is escalating. Services such as maintenance, calibration, validation, repair, and installation are essential to ensure the optimal performance and longevity of sophisticated laboratory equipment.

The Laboratory Equipment Services Market is undergoing substantial growth, driven by the increasing complexity and criticality of laboratory instruments across various sectors, including healthcare, pharmaceuticals, biotechnology, and academic research. As laboratories strive to maintain high standards of accuracy, reliability, and regulatory compliance, the demand for comprehensive service solutions is escalating. Services such as maintenance, calibration, validation, repair, and installation are essential to ensure the optimal performance and longevity of sophisticated laboratory equipment.Key market players are enhancing their service offerings to meet this demand. For instance, Laboratory Equipment Service & Supplies, LLC provides on-site services within 24-48 hours to hospitals, schools, universities, and research labs across the U.S., ensuring minimal disruption to critical operations. Additionally, Medical Equipment Source (MES) highlights the effectiveness of their preventative maintenance contracts and repair services, which can reduce equipment downtime by up to 60%. These timely and efficient service solutions underscore the importance of reliable and responsive support in maintaining laboratory productivity and operational efficiency.

As technological advancements continue to elevate the capabilities of laboratory equipment, the need for specialized services to support these innovations grows correspondingly. The integration of advanced diagnostics and predictive maintenance technologies further propels the market, enabling proactive identification and resolution of potential issues before they impact performance.

Key Takeaways

- Market Value: The Global Laboratory Equipment Services Market was valued at USD 29.0 Bn in 2023. It is expected to reach USD 63.7 Bn by 2033, with a CAGR of 8.4% during the forecast period from 2024 to 2033.

- By Equipment Type: Analytical equipment is the dominant segment, accounting for 40% of the market, due to its widespread use in various laboratory applications.

- By Type: Repair & Maintenance services lead with a 40% share, reflecting the necessity for ongoing maintenance of laboratory equipment.

- By Contract Type: Standard Service Contracts are the most prevalent, representing 55% of the market, as they offer a reliable and predictable service framework.

- By Service Provider: OEMs (Original Equipment Manufacturers) dominate the market with a 60% share, given their expertise and availability of original parts.

- By End-User: Clinical laboratories are the leading end-users, comprising 35% of the market, due to their extensive need for laboratory equipment services.

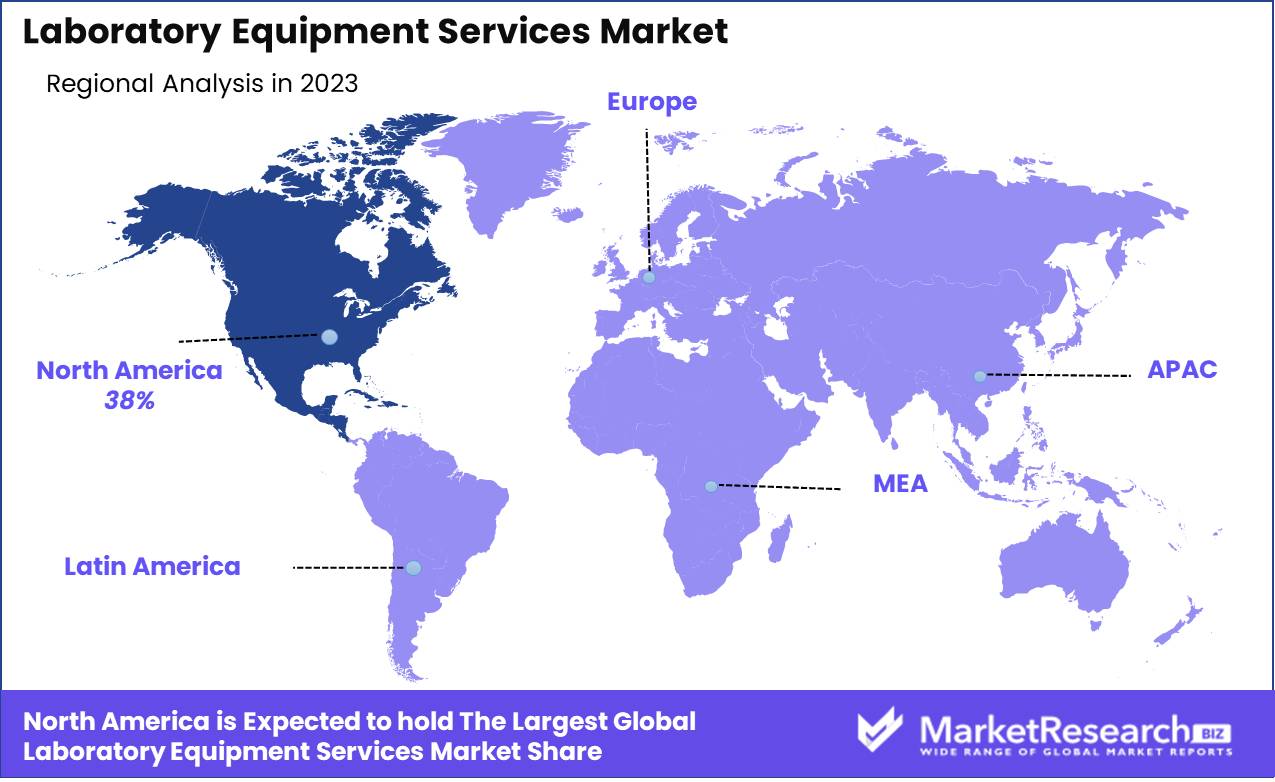

- Regional Dominance: North America dominates the Laboratory Equipment Services Market with a 38% share, driven by a robust laboratory infrastructure and high demand for advanced laboratory services.

- Growth Opportunity: The rising demand for advanced analytical techniques, regulatory compliance, and preventive maintenance create growth opportunities in the laboratory equipment services market.

Driving factors

Increasing Demand for Diagnostic Tests Fueling Market Expansion

The escalating demand for diagnostic tests is a primary driver of growth in the Laboratory Equipment Services Market. The rising prevalence of chronic diseases, the need for early disease detection, and the growing awareness of personalized medicine have significantly increased the volume of diagnostic testing globally. This surge in diagnostic tests requires well-maintained, accurate, and reliable laboratory equipment to ensure high-quality results. Consequently, the demand for services such as equipment calibration, maintenance, and repair has intensified.

The need to minimize downtime and maintain continuous operation of diagnostic laboratories further boosts the market for laboratory equipment services. This trend is expected to continue as healthcare systems globally prioritize early diagnosis and disease prevention, driving sustained demand for laboratory equipment services.

Rising Investment in Research and Development Driving Innovation

The rising investment in research and development (R&D) is another crucial factor propelling the Laboratory Equipment Services Market. Governments, academic institutions, and private companies are increasingly allocating funds towards scientific research, leading to the establishment of new laboratories and the upgrading of existing ones. This investment fosters innovation in fields such as biotechnology, pharmaceuticals, and clinical diagnostics, which in turn requires advanced and sophisticated laboratory equipment.

To ensure optimal performance and compliance with stringent regulatory standards, these high-tech instruments necessitate regular servicing and maintenance. The growing R&D activities not only enhance the demand for new laboratory equipment but also amplify the need for comprehensive equipment services, including installation, validation, and preventive maintenance.

Synergistic Impact of Diagnostic Demand and R&D Investment

The combined impact of increasing demand for diagnostic tests and rising investment in R&D creates a synergistic effect that significantly boosts the Laboratory Equipment Services Market. As diagnostic testing becomes more prevalent and R&D activities expand, the volume and complexity of laboratory equipment in use grow correspondingly. This expansion necessitates robust service support to maintain equipment efficiency, accuracy, and longevity.

The interdependence of these factors ensures a continuous and escalating demand for laboratory equipment services. Service providers are thus presented with substantial growth opportunities, particularly in offering advanced, tailored solutions that cater to the evolving needs of both diagnostic and research laboratories.

Restraining Factors

High Cost of Service Contracts as a Market Constraint

The high cost of service contracts is a significant barrier to the growth of the Laboratory Equipment Services Market. Comprehensive service contracts, which cover calibration, maintenance, repair, and sometimes upgrades, often come with substantial price tags. These costs can be prohibitive for small and medium-sized laboratories that operate on tight budgets.

High service costs can deter laboratories from entering into long-term contracts, leading them to opt for ad-hoc services that may be less effective in maintaining equipment performance and longevity. This financial barrier not only limits the accessibility of essential services but also affects the overall efficiency and reliability of laboratory operations, thereby hindering market growth.

Lack of Skilled Professionals Hindering Market Development

The lack of skilled professionals is another critical challenge facing the Laboratory Equipment Services Market. The complexity and sophistication of modern laboratory equipment require highly trained technicians to perform maintenance, calibration, and repairs accurately. However, there is a notable shortage of such skilled professionals, particularly in emerging markets and rural areas. This skill gap can lead to prolonged equipment downtime, reduced productivity, and potential inaccuracies in diagnostic and research results.

The shortage of qualified technicians also places additional strain on existing service providers, who must manage increased demand with limited resources. This challenge is compounded by the continuous advancement of laboratory technologies, which necessitate ongoing training and education to keep technicians up-to-date with the latest developments.

By Equipment Type Analysis

Analytical equipment accounted for 40% of the Laboratory Equipment Services Market by equipment type.

In 2023, Analytical Equipment held a dominant market position in the By Equipment Type segment of the Laboratory Equipment Services Market, capturing more than a 40% share. This significant share highlights the crucial role of analytical equipment in research and development, quality control, and diagnostics across various industries. Analytical Equipment includes instruments such as spectrometers, chromatographs, and electron microscopes, which are essential for precise and accurate analysis of chemical compositions, biological samples, and material properties.

General Equipment, encompassing basic laboratory instruments like centrifuges, balances, and pH meters, holds a smaller but significant market share. These instruments are fundamental to routine laboratory operations and are widely used across various types of laboratories.

Specialty Equipment includes highly specialized instruments tailored for specific applications, such as cell counters, DNA testing sequencers, and automated liquid handling systems. Although this segment represents a smaller share of the market, the need for specialized service providers with expertise in maintaining and repairing such advanced equipment is critical.

Support Equipment refers to auxiliary devices that support laboratory functions, such as fume hoods, incubators, and autoclaves. These are vital for creating controlled environments and ensuring the safety and efficiency of laboratory work.

By Type Analysis

Repair and maintenance services held 40% of the Laboratory Equipment Services Market by type.

In 2023, Repair & Maintenance held a dominant market position in the By Type segment of the Laboratory Equipment Services Market, capturing more than a 40% share. This significant market share highlights the critical importance of ensuring the continuous, reliable operation of laboratory equipment through regular repair and maintenance services. Repair & Maintenance services are vital for extending the lifespan of laboratory equipment, preventing downtime, and ensuring accurate and reliable performance. These services include routine maintenance checks, troubleshooting, parts replacement, and emergency repairs.

Calibration services, which involve adjusting and verifying the accuracy of laboratory instruments, represent another crucial segment. Calibration is essential for ensuring that equipment performs correctly and provides precise measurements, which is vital for research accuracy, compliance with industry standards, and quality control.

Validation services involve ensuring that laboratory equipment and processes meet predefined standards and regulatory requirements. This includes performance qualification, installation qualification, and operational qualification of equipment.

Others category encompasses additional services such as training, consultancy, and software support. These services are important for enhancing the overall efficiency and effectiveness of laboratory operations.

By Contract Type Analysis

Standard service contracts dominated the Laboratory Equipment Services Market by contract type with a 55% share.

In 2023, Standard Service Contracts held a dominant market position in the By Contract Type segment of the Laboratory Equipment Services Market, capturing more than a 55% share. This substantial market share underscores the widespread preference for standardized agreements that offer predictable and comprehensive service solutions for laboratory equipment maintenance and support. Standard Service Contracts are favored for their simplicity, reliability, and cost-effectiveness. These contracts typically cover routine maintenance, repairs, calibration, and occasional emergency services, providing laboratories with a consistent and structured approach to equipment management.

Customized Service Contracts, while holding a smaller market share, are essential for laboratories with unique needs and specialized equipment. These contracts are tailored to the specific requirements of the laboratory, offering flexibility in the scope of services, frequency of maintenance, and levels of support. Customized contracts are particularly valuable for facilities with advanced or uncommon equipment that requires specialized expertise and attention.

By Service Provider Analysis

OEM service providers captured 60% of the Laboratory Equipment Services Market by service provider.

In 2023, OEM (Original Equipment Manufacturer) held a dominant market position in the By Service Provider segment of the Laboratory Equipment Services Market, capturing more than a 60% share. This significant market share reflects the preference for manufacturer-provided service solutions that ensure the highest compatibility and quality standards for laboratory equipment maintenance and support.

OEM (Original Equipment Manufacturer) service providers are highly valued for their deep expertise and intimate knowledge of the equipment they produce. These service contracts often include comprehensive maintenance programs, timely repairs, and access to original parts and updates, ensuring that laboratory instruments operate at peak performance. The assurance of quality and reliability, backed by the manufacturer’s brand reputation, drives the dominance of OEM services in the market.

Third-Party Service providers, while holding a smaller market share, play a crucial role in the laboratory equipment services market by offering flexible and cost-effective solutions. These independent service providers often deliver competitive pricing, customizable service packages, and quicker response times, appealing to laboratories with budget constraints or those seeking alternative service options.

By End-User Analysis

Clinical laboratories captured 35% of the Laboratory Equipment Services Market by end-user.

In 2023, Clinical Laboratories held a dominant market position in the By End-User segment of the Laboratory Equipment Services Market, capturing more than a 35% share. This significant market share underscores the critical role of clinical laboratories in healthcare diagnostics and patient care, driving the demand for reliable and efficient laboratory equipment services. Clinical Laboratories rely heavily on precise and dependable laboratory equipment to conduct a wide range of diagnostic tests, from routine blood work to complex molecular diagnostics.

Research Institutions represent another vital segment within the laboratory equipment services market. These institutions, which include academic and government research facilities, depend on sophisticated laboratory equipment to conduct cutting-edge research across various scientific disciplines.

Pharmaceutical Companies also constitute a significant end-user segment, utilizing advanced laboratory equipment for drug development, testing, and quality control. The pharmaceutical industry’s stringent regulatory requirements and the critical nature of their work drive the demand for reliable equipment services to ensure compliance and maintain the integrity of their research and development processes.

Others category includes various end-users such as biotechnology firms, environmental testing labs, and food and beverage testing laboratories. Although this segment captures a smaller portion of the market, it represents a diverse range of industries that require specialized laboratory equipment services to support their unique testing and quality assurance needs.

Key Market Segments

By Equipment Type

- Analytical Equipment

- General Equipment

- Specialty Equipment

- Support Equipment

By Type

- Repair & Maintenance

- Calibration

- Validation

- Others

By Contract Type

- Standard Service Contracts

- Customized Service Contracts

By Service Provider

- OEM (Original Equipment Manufacturer)

- Third-Party Service

By End-User

- Research Institutions

- Clinical Laboratories

- Pharmaceutical Companies

- Others

Growth Opportunity

Expansion in Emerging Markets Fueling Growth

The expansion of the Laboratory Equipment Services Market into emerging markets presents a significant growth opportunity for 2024. Countries in regions such as Asia-Pacific, Latin America, and Africa are experiencing rapid economic growth and improvements in healthcare infrastructure. This development leads to an increase in the establishment of new laboratories and the upgrade of existing ones. As these markets expand, the demand for laboratory equipment services, including installation, maintenance, and repair, is expected to rise significantly.

International and local companies are investing heavily in these regions, recognizing the untapped potential. By offering cost-effective and tailored service packages, providers can capture substantial market share in these burgeoning markets, driving overall industry growth.

Development of Personalized Medicine Driving Service Demand

The growing emphasis on personalized medicine is another critical opportunity for the Laboratory Equipment Services Market in 2024. Personalized medicine, which involves tailoring medical treatment to the individual characteristics of each patient, relies heavily on advanced laboratory equipment for genetic testing, biomarker analysis, and other diagnostic procedures. This trend necessitates the use of highly sophisticated and precise equipment, which in turn requires regular and expert servicing to maintain optimal performance.

As personalized medicine continues to gain traction, the demand for specialized laboratory equipment services is expected to increase. Service providers that can offer advanced, reliable, and responsive support for these high-tech instruments will be well-positioned to capitalize on this trend.

Latest Trends

Adoption of Automation and Robotics Transforming Laboratory Operations

The adoption of automation and robotics is set to be a major trend in the Laboratory Equipment Services Market in 2024. Laboratories are increasingly integrating automated systems and robotic technologies to enhance efficiency, accuracy, and throughput. Automated equipment reduces human error, speeds up repetitive tasks, and allows for more precise handling of samples and reagents. As these technologies become more prevalent, the demand for specialized maintenance and calibration services for automated and robotic equipment rises.

Service providers need to develop expertise in these advanced systems to ensure they can offer the necessary support and keep laboratory operations running smoothly. This trend is expected to drive significant growth in the market as laboratories seek to maximize the benefits of automation and robotics.

IoT in Lab Equipment Enhancing Connectivity and Predictive Maintenance

The incorporation of the Internet of Things (IoT) into laboratory equipment is another transformative trend expected to shape the market in 2024. IoT-enabled lab equipment can communicate real-time data on usage, performance, and maintenance needs, allowing for proactive and predictive maintenance strategies. This connectivity reduces downtime and extends the lifespan of expensive laboratory instruments.

Service providers can leverage IoT data to offer more efficient and effective services, such as remote diagnostics and automated service scheduling. The ability to monitor equipment health and predict failures before they occur not only improves operational efficiency but also reduces costs associated with unexpected downtime and repairs.

Regional Analysis

North America's dominance at 38% underscores the region's advanced healthcare infrastructure, significant research and development investments, and a strong presence of leading biotechnology.The Laboratory Equipment Services market exhibits diverse growth patterns across different regions, driven by varying levels of technological advancement, healthcare infrastructure, and research activity. North America leads the global market with a commanding 38% share, underpinned by a robust healthcare system, extensive research and development activities, and substantial investments in biotechnology and pharmaceuticals. The United States, with its advanced medical research facilities and high concentration of academic and research institutions, significantly contributes to the region's dominance, while Canada also plays a notable role with its growing focus on healthcare innovation.

In Europe, the market is supported by a strong emphasis on scientific research and stringent regulatory standards. Countries such as Germany, the UK, and France are key contributors, with well-established healthcare infrastructure and significant public and private sector investments in laboratory technologies.

The Asia Pacific region is experiencing rapid expansion, propelled by increasing healthcare expenditure, burgeoning research activities, and a growing number of clinical laboratories. China, Japan, and India are the primary markets, driven by government initiatives to enhance healthcare services, rising investments in life sciences, and a growing focus on early disease detection and prevention.

The Middle East & Africa market is gradually expanding, with countries like Saudi Arabia, the UAE, and South Africa making significant progress. The region's growth is supported by improving healthcare infrastructure, increasing investments in medical research, and the adoption of advanced laboratory technologies.

Latin America shows steady growth, with Brazil and Mexico being the main markets. The region benefits from improving healthcare services, rising research activities, and increasing government and private sector investments in laboratory infrastructure.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global Laboratory Equipment Services market is set to expand significantly, driven by technological advancements, the increasing complexity of laboratory instruments, and heightened demand for maintenance and calibration services. Key players such as Thermo Fisher Scientific Inc. and Waters Corporation lead the market with their comprehensive service portfolios that include installation, maintenance, and training, alongside their cutting-edge equipment offerings. Thermo Fisher's extensive global reach and robust service infrastructure make it a pivotal player in ensuring seamless laboratory operations worldwide.

Abbott and Agilent Technologies, Inc. are notable for their focus on providing specialized services tailored to the needs of the biomedical and analytical sectors, respectively. Abbott’s strong presence in the clinical diagnostics market complements its service offerings, ensuring high uptime and precision of critical laboratory instruments. Agilent's expertise in chemical analysis and life sciences bolsters its service capabilities, meeting the stringent requirements of these research-intensive industries.

Kheiron Medical Technologies Limited and Therapixel are innovative entrants, leveraging artificial intelligence to enhance laboratory equipment efficiency and predictive maintenance. Their cutting-edge solutions are poised to revolutionize service paradigms, offering predictive analytics that preempt equipment failures and optimize performance.

Microsoft, while primarily known for its software solutions, is increasingly integrating its cloud and AI technologies into laboratory equipment management, enhancing data analytics and operational efficiency. Danaher Corporation and PerkinElmer, Inc. maintain strong market positions through their diverse service offerings and global presence, supporting laboratories in achieving high performance and compliance standards.

Pace Analytical Services, LLC, and Bio-Rad Laboratories, Inc. emphasize robust quality control and regulatory compliance services, crucial for laboratories navigating complex regulatory landscapes. Becton, Dickinson and Company, Siemens Healthineers, and Eppendorf AG continue to provide comprehensive service solutions that ensure the reliability and longevity of laboratory instruments.

Market Key Players

- Thermo Fisher Scientific Inc.

- Waters Corporation

- Abbott

- Kheiron Medical Technologies Limited

- Therapixel

- Microsoft

- Hettich Instruments, LP

- Agilent Technologies, Inc.

- Danaher Corporation

- PerkinElmer, Inc.

- Pace Analytical Services, LLC

- Bio-Rad Laboratories, Inc.

- Becton, Dickinson and Company

- Siemens Healthineers

- Eppendorf AG

Recent Development

- In June 2024, Agilent Technologies expanded their service portfolio to include remote diagnostics and predictive maintenance capabilities for laboratory equipment, improving uptime and efficiency.

- In May 2024, Thermo Fisher Scientific launched a new global support service offering specialized calibration and validation services for advanced laboratory instruments.

Report Scope

Report Features Description Market Value (2023) USD 29.0 Bn Forecast Revenue (2033) USD 63.7 Bn CAGR (2024-2033) 8.4% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Equipment Type (Analytical Equipment, General Equipment, Specialty Equipment, Support Equipment), By Type (Repair & Maintenance, Calibration, Validation, Others), By Contract Type (Standard Service Contracts, Customized Service Contracts), By Service Provider (OEM (Original Equipment Manufacturer), Third-Party Service), By End-User (Research Institutions, Clinical Laboratories, Pharmaceutical Companies, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Thermo Fisher Scientific Inc., Waters Corporation, Abbott, Kheiron Medical Technologies Limited, Therapixel, Microsoft, Hettich Instruments, LP, Agilent Technologies, Inc., Danaher Corporation, PerkinElmer, Inc., Pace Analytical Services, LLC, Bio-Rad Laboratories, Inc., Becton, Dickinson and Company, Siemens Healthineers, Eppendorf AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Thermo Fisher Scientific Inc.

- Waters Corporation

- Abbott

- Kheiron Medical Technologies Limited

- Therapixel

- Microsoft

- Hettich Instruments, LP

- Agilent Technologies, Inc.

- Danaher Corporation

- PerkinElmer, Inc.

- Pace Analytical Services, LLC

- Bio-Rad Laboratories, Inc.

- Becton, Dickinson and Company

- Siemens Healthineers

- Eppendorf AG

Our Clients

View Our Licence Options