Irritable Bowel Syndrome Treatment Market By Type (IBS with Diarrhea (IBS-D), IBS with Constipation (IBS-C), Mixed-presentation IBS (IBS-M)), By Product (Rifaximin, Eluxadoline, Lubiprostone, Linaclotide, Others), By End User (Hospitals Pharmacies, Drug Stores & Retail Pharmacies, Online Pharmacies), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

2676

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

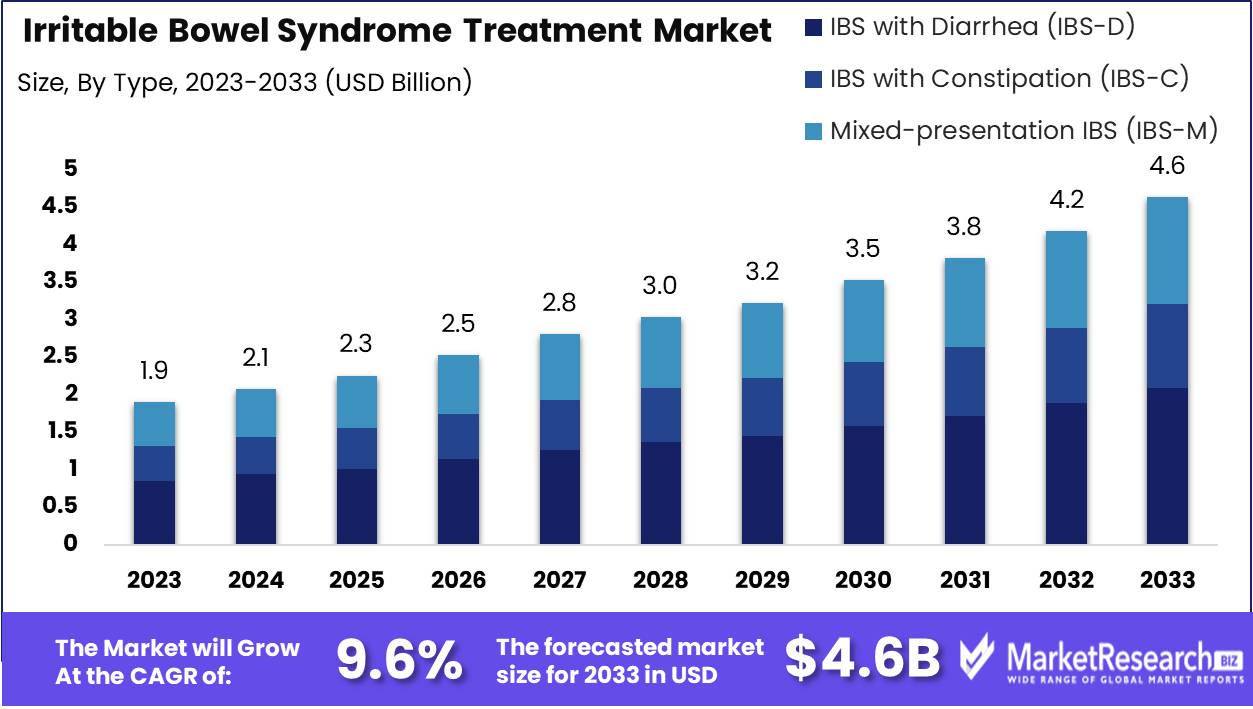

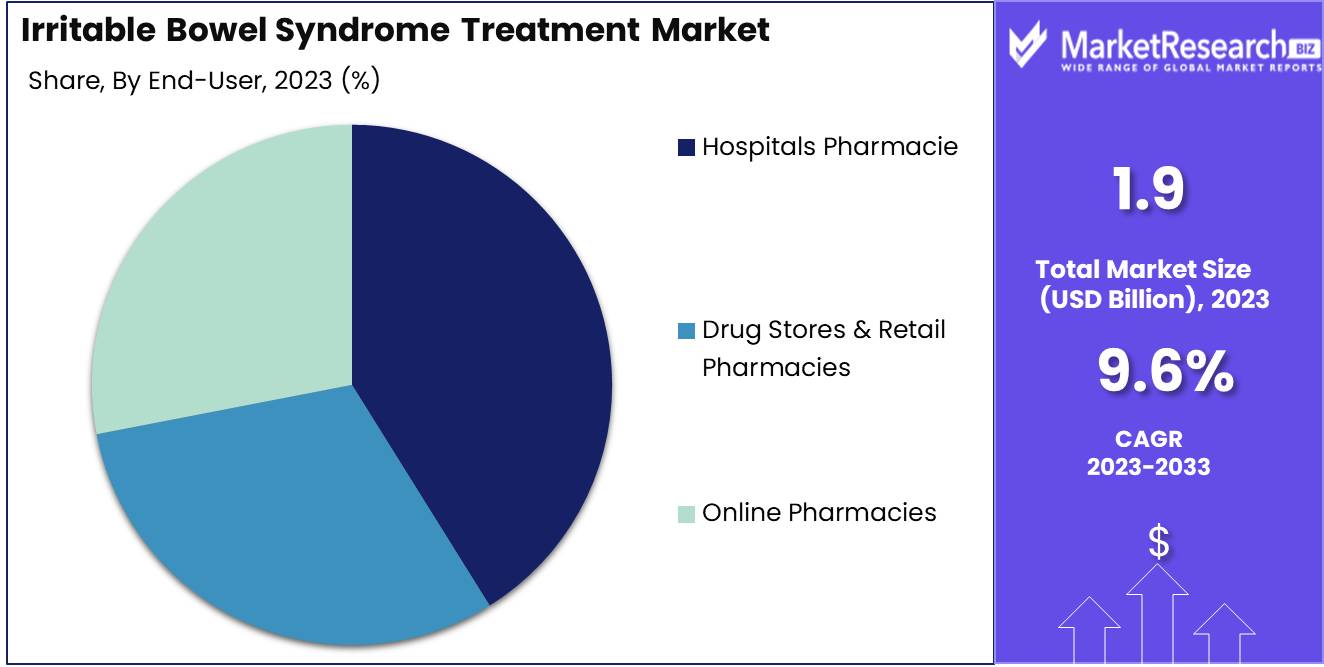

The Irritable Bowel Syndrome Treatment Market was valued at USD 1.9 billion in 2023. It is expected to reach USD 4.6 billion by 2033, with a CAGR of 9.6% during the forecast period from 2024 to 2033.

The Irritable Bowel Syndrome (IBS) Treatment Market encompasses an array of products and therapies aimed at alleviating the symptoms of IBS, a chronic gastrointestinal disorder characterized by abdominal pain, bloating, and altered bowel habits. This market includes pharmaceuticals such as antispasmodics, laxatives, and antidepressants, alongside probiotics, dietary modifications, and behavioral therapies. The growing prevalence of IBS, advancements in medical research, and an increasing focus on personalized medicine drive market expansion. Strategic developments by key players and a heightened awareness of gut health further propel the market, fostering innovation and improved patient outcomes.

The global Irritable Bowel Syndrome (IBS) Treatment Market is witnessing significant growth, driven primarily by the increasing incidence of IBS worldwide, affecting approximately 10-15% of the global population. This substantial prevalence has heightened the demand for effective treatment solutions, positioning the market for robust expansion. Ongoing research and development efforts are pivotal in this context, as they lead to the introduction of innovative and more efficacious treatment options, further fueling market growth. For instance, advancements in biotechnology and personalized medicine are expected to provide tailored therapies, thereby enhancing treatment outcomes and patient satisfaction. These innovations not only address the unmet needs of patients but also stimulate competitive dynamics within the market.

However, the market faces challenges, notably the high cost of IBS medications and therapies, which can impede access to treatment, especially in developing regions. This economic barrier underscores the necessity for more cost-effective therapeutic solutions to ensure broader accessibility. Despite these challenges, the overall outlook for the IBS treatment market remains positive, buoyed by technological advancements and a strong pipeline of new treatments.

As the market evolves, stakeholders are likely to witness a surge in strategic collaborations and investments aimed at overcoming existing barriers and leveraging emerging opportunities. Thus, the IBS treatment market is poised for substantial growth, underpinned by both clinical advancements and strategic industry initiatives.

Key Takeaways

- Market Growth: The Irritable Bowel Syndrome Treatment Market was valued at USD 1.9 billion in 2023. It is expected to reach USD 4.6 billion by 2033, with a CAGR of 9.6% during the forecast period from 2024 to 2033.

- By Type: IBS-D dominated the IBS treatment market by type.

- By Product: Rifaximin dominated the IBS Treatment Market By Product segment.

- By End-User: Hospital pharmacies dominated the IBS Treatment Market by end-user.

- Regional Dominance: North America dominates the IBS treatment market with a 35% largest share.

- Growth Opportunity: The global IBS treatment market is growing significantly due to drug advancements and the expansion of diversified product portfolios.

Driving factors

Rise in Geriatric Population: A Significant Driver of IBS Treatment Market Growth

The rise in the geriatric population is a crucial factor driving the growth of the Irritable Bowel Syndrome (IBS) treatment market. As the global population ages, there is a corresponding increase in the incidence of age-related gastrointestinal disorders, including IBS. Older adults are more susceptible to chronic illnesses, including gastrointestinal conditions, due to physiological changes in the digestive system and increased prevalence of co-morbidities. The global population aged 65 and above is projected to reach nearly 1.5 billion by 2050, significantly increasing the demand for IBS treatments. This demographic shift results in a larger patient pool requiring medical intervention, thereby boosting the market for IBS therapies.

Increase in Prevalence of Gastrointestinal Diseases and Disorders: Expanding the Market Scope

The increasing prevalence of gastrointestinal diseases and disorders is another primary driver of the IBS treatment market. The rise in cases of conditions such as Crohn's disease, ulcerative colitis, and other inflammatory bowel diseases directly contributes to the higher incidence of IBS. The World Gastroenterology Organisation estimates that more than 10% of the global population suffers from IBS, highlighting a significant need for effective treatment options.

Additionally, advancements in diagnostic techniques have led to better identification and understanding of IBS, further contributing to market growth. The continuous rise in gastrointestinal disorders underscores the necessity for innovative and effective treatment modalities, thereby expanding the market scope for IBS therapies.

Surge in Level of Stress and Adoption of Unhealthy Diets: Accelerating IBS Cases and Treatment Demand

The surge in stress levels and the adoption of unhealthy diets are interrelated factors that significantly impact the prevalence of IBS, thereby driving the market for its treatment. Modern lifestyles, characterized by high stress and poor dietary habits, are known to exacerbate IBS symptoms. The reports that stress levels have been rising steadily over the past decade, which correlates with an increase in functional gastrointestinal disorders like IBS.

Concurrently, the widespread consumption of processed foods, high in fats and sugars and low in fiber, contributes to gastrointestinal distress and IBS. This combination of psychological stress and unhealthy diets leads to a higher incidence of IBS, necessitating effective management and treatment solutions. Consequently, the market for IBS treatments is expected to grow as more individuals seek relief from stress-induced gastrointestinal symptoms.

Restraining Factors

Lack of Definitive Diagnostic Tools: A Barrier to Market Expansion

The absence of definitive diagnostic tools for Irritable Bowel Syndrome (IBS) remains a significant barrier to the growth of the IBS treatment market. Without precise and reliable diagnostic methods, patients often undergo a lengthy and uncertain diagnostic journey, which can delay treatment and reduce patient confidence in available therapies. This uncertainty can result in lower demand for treatments, as patients may be skeptical of the efficacy of prescribed medications or therapeutic interventions.

Additionally, the lack of standardized diagnostics hinders the ability of healthcare providers to accurately identify and segment patient populations, which is crucial for the development of targeted therapies and personalized medicine. The reliance on symptom-based diagnosis also complicates clinical trials and regulatory approvals, potentially slowing down the introduction of new treatments into the market.

The Intricate Nature of Diagnosing IBS: Compounding Diagnostic Challenges

The complex and multifaceted nature of diagnosing IBS exacerbates the challenges posed by the lack of definitive diagnostic tools. IBS presents with a broad spectrum of symptoms that often overlap with other gastrointestinal disorders, making it difficult for healthcare providers to differentiate between IBS and other conditions. This diagnostic complexity can lead to misdiagnoses or delayed diagnoses, further hindering effective treatment. Patients may experience frustration and decreased quality of life due to the protracted diagnostic process, reducing their willingness to seek or adhere to treatment regimens. The variability in symptom presentation also complicates the establishment of clear diagnostic criteria, which is essential for developing effective treatments and obtaining regulatory approval. As a result, pharmaceutical companies may be hesitant to invest in the IBS treatment market, given the high risk and uncertainty associated with bringing new therapies to market.

By Type Analysis

In 2023, IBS-D dominated the IBS treatment market by type.

In 2023, IBS with Diarrhea (IBS-D) held a dominant market position in the "By Type" segment of the Irritable Bowel Syndrome (IBS) Treatment Market. The IBS-D segment captured a significant share due to the rising prevalence of gastrointestinal disorders and increased awareness about IBS-D among patients and healthcare providers. The availability of targeted therapies and medications specifically designed for IBS-D contributed to this dominance.

IBS with Constipation (IBS-C), the second segment, experienced steady growth driven by advancements in treatment options and increasing patient adoption of over-the-counter and prescription medications. The segment benefitted from an expanding elderly population, which is more prone to constipation-related IBS symptoms, thus bolstering the market demand.

Mixed-presentation IBS (IBS-M) represented the third significant segment, characterized by fluctuating symptoms of both diarrhea and constipation. The complexity of managing IBS-M symptoms necessitated a multifaceted treatment approach, thereby promoting the use of combination therapies. Innovations in diagnostic techniques and personalized treatment regimens further supported the growth of the IBS-M segment. Together, these subtypes highlight the diverse therapeutic needs and market dynamics within the IBS treatment landscape.

By Product Analysis

In 2023, Rifaximin dominated the IBS Treatment Market By Product segment.

In 2023, Rifaximin held a dominant market position in the by-product segment of the Irritable Bowel Syndrome (IBS) Treatment Market. Rifaximin's efficacy in reducing IBS symptoms, particularly in patients with diarrhea-predominant IBS (IBS-D), has been well-documented, leading to its widespread adoption. The targeted antibiotic mechanism of Rifaximin, which modulates the gut microbiota without significant systemic absorption, has made it a preferred choice among healthcare providers.

Eluxadoline, another significant player in the IBS treatment landscape, caters primarily to IBS-D patients by acting as a mixed mu-opioid receptor agonist and delta-opioid receptor antagonist. Its unique action provides both pain relief and improved bowel function. Lubiprostone indicated for IBS with constipation (IBS-C), works by enhancing intestinal fluid secretion, facilitating easier stool passage, and alleviating symptoms.

Linaclotide, a guanylate cyclase-C agonist, also addresses IBS-C by increasing intestinal fluid secretion and accelerating transit time, which helps in reducing abdominal pain and discomfort. Other treatment options within this segment include a variety of lesser-used pharmaceuticals and over-the-counter remedies that offer alternative therapeutic approaches.

Overall, the IBS treatment market demonstrates a diverse range of products catering to the varying needs of IBS patients, with Rifaximin leading the way due to its effective symptom management and favorable safety profile. The competitive landscape is characterized by continuous advancements and a robust pipeline of novel therapies aimed at enhancing patient outcomes.

By End-User Analysis

In 2023, Hospital pharmacies dominated the IBS Treatment Market by end-user.

In 2023, Hospital pharmacies held a dominant market position in the end-user segment of the Irritable Bowel Syndrome Treatment Market. This dominance can be attributed to the extensive infrastructure and comprehensive patient management systems inherent in hospital settings, which facilitate efficient diagnosis and treatment of IBS. The capability to provide a wide range of medications and integrated care ensures high patient trust and adherence to prescribed therapies.

Drug Stores & Retail Pharmacies followed, capturing a significant share due to their accessibility and convenience. These pharmacies serve as critical points for over-the-counter and prescription medication distribution, making IBS treatments readily available to a broader population. The personalized service offered by retail pharmacists enhances patient education and compliance, contributing to the segment's substantial market presence.

Online Pharmacies, although currently the smallest segment, are experiencing rapid growth driven by increasing internet penetration and consumer preference for digital solutions. The ability to offer competitive pricing, home delivery, and discreet purchasing options appeals to patients seeking privacy and convenience. This segment is poised for significant expansion as digital health trends continue to evolve and regulatory frameworks become more supportive.

Key Market Segments

By Type

- IBS with Diarrhea (IBS-D)

- IBS with Constipation (IBS-C)

- Mixed-presentation IBS (IBS-M)

By Product

- Rifaximin

- Eluxadoline

- Lubiprostone

- Linaclotide

- Others

By End-User

- Hospitals Pharmacie

- Drug Stores & Retail Pharmacies

- Online Pharmacies

Growth Opportunity

Advancements in Drug Development

The global market for Irritable Bowel Syndrome (IBS) treatment is poised for significant growth, driven by substantial advancements in drug development. The introduction of novel therapeutics and the improvement of existing medications are enhancing treatment efficacy and patient outcomes. Innovations such as microbiome-targeted therapies and biologics are revolutionizing the IBS treatment landscape, offering new avenues for symptom management and disease modification. These advancements are expected to propel market growth as they address previously unmet medical needs and offer more personalized treatment options.

Expansion of Product Portfolios

The expansion of product portfolios by leading pharmaceutical companies is another critical driver of market growth. Companies are increasingly focusing on diversifying their offerings to include a broader range of treatment options, such as probiotics, prebiotics, and dietary supplements, alongside traditional pharmaceuticals. This strategic expansion is aimed at providing comprehensive care solutions that cater to the diverse needs of IBS patients. Additionally, the development of over-the-counter (OTC) products is expected to increase accessibility and convenience for patients, further driving market expansion.

Latest Trends

Personalized Medicine and Precision Therapies

The irritable bowel syndrome (IBS) treatment market is poised to experience significant advancements, driven by the growing adoption of personalized medicine and precision therapies. Personalized medicine tailors treatment to the individual characteristics of each patient, enhancing efficacy and reducing adverse effects. With advancements in genomic research and biotechnology, healthcare providers can now identify specific genetic markers associated with IBS. This allows for the development of targeted therapies that address the underlying causes of the disorder, rather than merely managing symptoms. Precision therapies, leveraging data from genomic, proteomic, and metabolomic analyses, enable a more accurate diagnosis and treatment plan for IBS patients, thereby improving outcomes and patient satisfaction.

Collaborations Accelerating Discovery of Novel Therapeutic Targets

Collaborative efforts between pharmaceutical companies, research institutions, and biotechnology firms are expected to accelerate the discovery of novel therapeutic targets for IBS treatment in 2024. These partnerships facilitate the sharing of knowledge, resources, and technologies, thereby expediting the research and development process. For instance, collaborations focusing are uncovering new insights into the gut-brain axis, which plays a crucial role in IBS pathophysiology. By pooling expertise and resources, these collaborations aim to develop innovative therapies that can more effectively modulate the gut microbiome, offering new hope for patients with IBS. Furthermore, joint ventures in artificial intelligence and machine learning are enhancing drug discovery processes, enabling the identification of potential therapeutic candidates at an unprecedented pace.

Regional Analysis

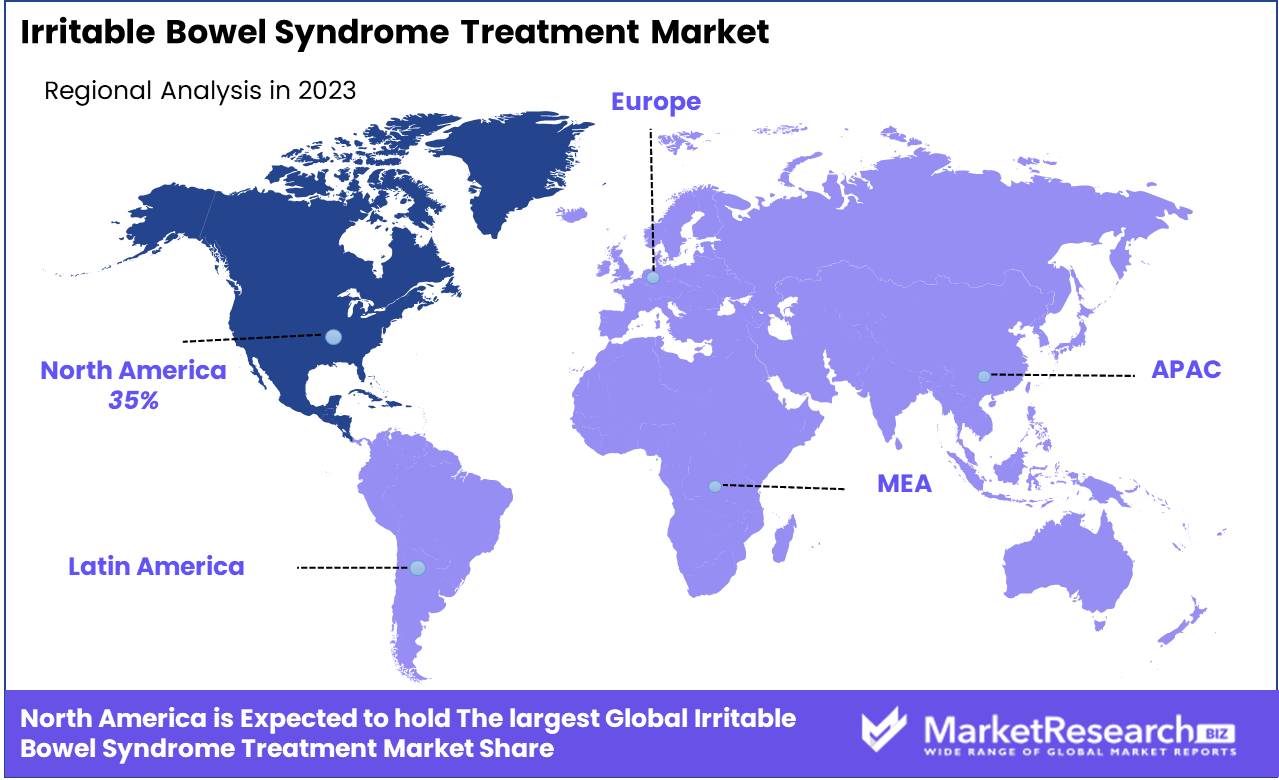

North America dominates the IBS treatment market with a 35% largest share.

The Irritable Bowel Syndrome (IBS) Treatment Market exhibits significant regional variations driven by healthcare infrastructure, awareness levels, and economic conditions. North America holds the dominant position, accounting for approximately 35% of the global market share, primarily due to the high prevalence of IBS, advanced healthcare facilities, and substantial investment in research and development. The region's market is bolstered by the increasing adoption of novel therapies and a well-established pharmaceutical sector.

In Europe, the market is propelled by rising awareness about IBS and the availability of advanced diagnostic and therapeutic options. Countries such as Germany, France, and the UK are at the forefront, contributing significantly to the regional market share. The Asia Pacific region is expected to witness the fastest growth, driven by a large patient pool, increasing healthcare expenditure, and improving healthcare infrastructure. China and India are notable markets due to their vast populations and growing prevalence of IBS.

The Middle East & Africa region, though smaller in market size, is gradually expanding due to improving healthcare systems and rising awareness. Latin America shows moderate growth, with Brazil and Mexico being key contributors, supported by improved healthcare services and increased patient awareness. Overall, the North American region dominates the global IBS treatment market, leveraging its robust healthcare infrastructure and innovation-driven pharmaceutical industry.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Irritable Bowel Syndrome (IBS) Treatment Market in 2024 is significantly influenced by several key players, each contributing to market dynamics through innovation, product development, and strategic alliances.

Valeant Pharmaceuticals International, now Bausch Health Companies, continues to leverage its robust gastrointestinal product portfolio, enhancing treatment options for IBS. Allergan Inc. maintains a strong market presence with its flagship product, Linzess (linaclotide), which remains a preferred choice for many patients with IBS-C (constipation).

Astellas Pharma and Lexicon Pharmaceuticals are notable for their research and development initiatives, with the latter’s innovative approach with telotristat ethyl showing promise in clinical studies. Nestle Health Science's focus on nutritional therapies offers complementary treatment avenues, aligning with the growing preference for holistic health solutions.

Synergy Pharmaceuticals Inc., despite financial hurdles, has significantly impacted the market with Trulance, providing an effective alternative for chronic idiopathic constipation and IBS-C. Ironwood Pharmaceuticals, Inc, in collaboration with Allergan, continues to expand the use of Linzess, solidifying its market leadership.

Ardelyx Inc.'s tenapanor presents a novel mechanism of action, addressing unmet needs in IBS-C management. Mallinckrodt, Abbott, AstraZeneca plc, and Novartis AG contribute through their diversified portfolios and strategic market entries, enhancing treatment accessibility and efficacy.

Takeda Pharmaceutical Company Limited, with its extensive experience in gastrointestinal therapies, remains a formidable player, particularly through its development of new therapeutic agents. Sebela Pharmaceuticals Inc., GlaxoSmithKline Plc, and Johnson & Johnson are recognized for their ongoing commitment to addressing IBS through advanced pharmaceutical innovations and comprehensive patient care strategies.

Overall, the competitive landscape is characterized by a blend of established treatments and innovative therapeutic advancements, driving the market towards enhanced patient outcomes and sustained growth.

Market Key Players

- Valeant Pharmaceuticals International

- Allergan Inc

- Astellas Pharma

- Lexicon Pharmaceuticals

- Nestle Health Science

- Synergy Pharmaceuticals Inc

- Ironwood Pharmaceuticals

- Ardelyx Inc.

- Mallinckrodt

- Abbott

- AstraZeneca plc

- Novartis AG

- Takeda Pharmaceutical Company Limited

- Sebela Pharmaceuticals Inc.

- GlaxoSmithKline Plc

- Johnson & Johnson

Recent Development

- In October 2023, Allergan announced positive results from a Phase 3 clinical trial for its investigational drug candidate aimed at treating IBS. The trial showed statistically significant improvements in abdominal pain and stool consistency among patients, indicating the potential of this new therapy to meet unmet medical needs in IBS treatment.

- In September 2023, Ironwood announced the approval and commercial launch of a new formulation of its flagship IBS treatment in selected markets. This new formulation offers enhanced convenience and dosing flexibility, reflecting Ironwood's dedication to improving patient outcomes and experiences in IBS management.

- In March 2023, Takeda initiated a Phase 2 clinical trial for a novel treatment candidate for diarrhea-predominant IBS (IBS-D). This clinical trial is a crucial step towards developing new therapeutic options for individuals suffering from this subtype of IBS, demonstrating Takeda's commitment to advancing IBS research and innovation.

Report Scope

Report Features Description Market Value (2023) USD 1.9 Billion Forecast Revenue (2033) USD 4.6 Billion CAGR (2024-2032) 9.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (IBS with Diarrhea (IBS-D), IBS with Constipation (IBS-C), Mixed-presentation IBS (IBS-M)), By Product (Rifaximin, Eluxadoline, Lubiprostone, Linaclotide, Others), By End User (Hospitals Pharmacies, Drug Stores & Retail Pharmacies, Online Pharmacies) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Valeant Pharmaceuticals International, Allergan Inc, Astellas Pharma, Lexicon Pharmaceuticals, Nestle Health Science, Synergy Pharmaceuticals Inc, Ironwood Pharmaceuticals, Inc, Ardelyx Inc., Mallinckrodt, Abbott, AstraZeneca plc, Novartis AG, Takeda Pharmaceutical Company Limited, Sebela Pharmaceuticals Inc., GlaxoSmithKline Plc, Johnson & Johnson Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Valeant Pharmaceuticals International

- Allergan Inc

- Astellas Pharma

- Lexicon Pharmaceuticals

- Nestle Health Science

- Synergy Pharmaceuticals Inc

- Ironwood Pharmaceuticals

- Ardelyx Inc.

- Mallinckrodt

- Abbott

- AstraZeneca plc

- Novartis AG

- Takeda Pharmaceutical Company Limited

- Sebela Pharmaceuticals Inc.

- GlaxoSmithKline Plc

- Johnson & Johnson

Our Clients

View Our Licence Options