Industrial Fasteners Market By Material (Metal, Plastic), By Product Type (Externally Threaded, Internally Threaded, Non-Threaded), By Application (Automotive, Aerospace, Industrial Machinery, Home appliances, Furniture, Other), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

4550

-

May 2023

-

154

-

-

This report was compiled by Kalyani Khudsange Kalyani Khudsange is a Research Analyst at Prudour Pvt. Ltd. with 2.5 years of experience in market research and a strong technical background in Chemical Engineering and manufacturing. Correspondence Sr. Research Analyst Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

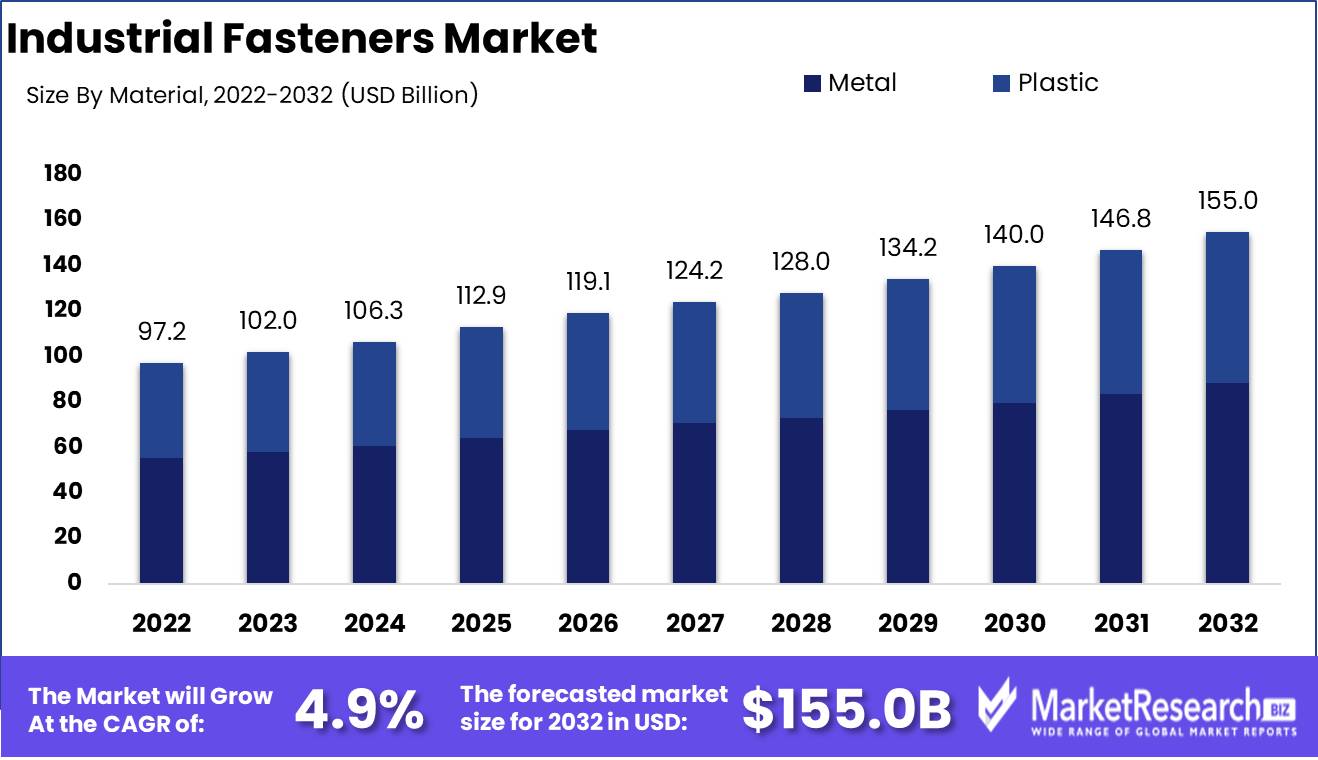

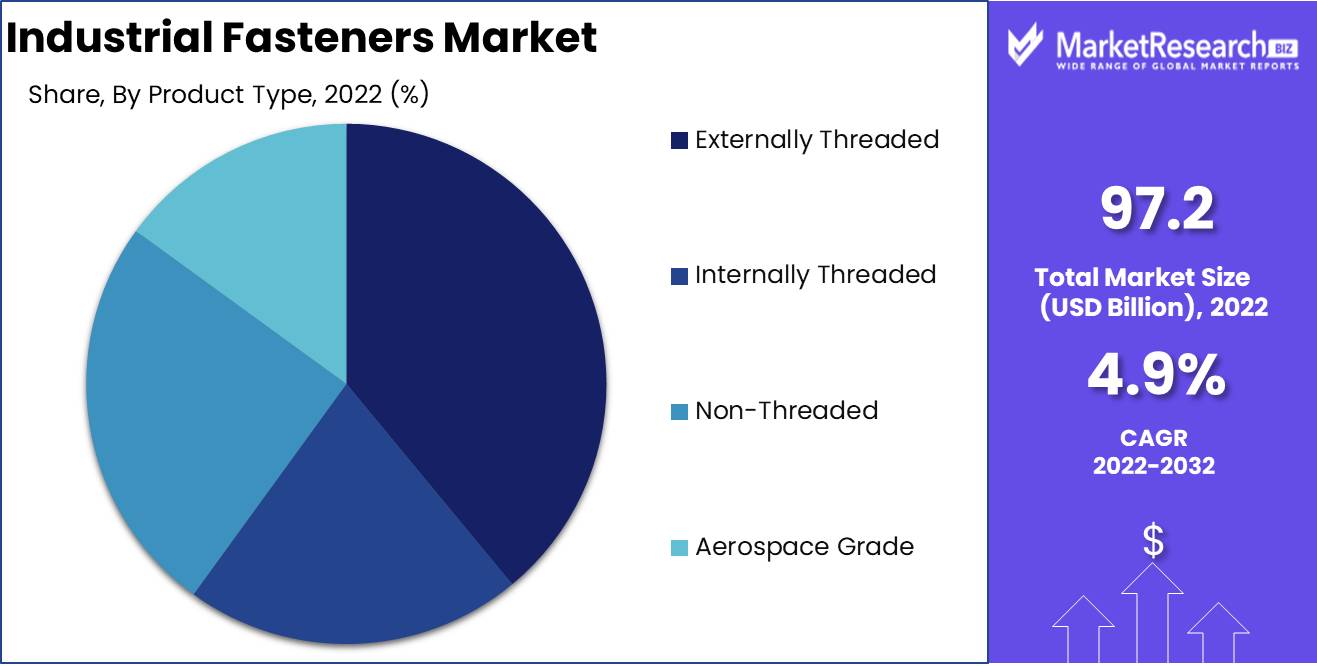

Industrial Fasteners Market size is expected to be worth around USD 155.0 Bn by 2032 from USD 97.2 Bn in 2022, growing at a CAGR of 4.9% during the forecast period from 2023 to 2032.

Industrial Fasteners Market comprises the production, distribution, and utilization of various fastening devices utilized in industrial contexts. These fasteners are devised and manufactured in a variety of shapes, sizes, and materials to satisfy the needs of various industries. The primary objective of the industrial fasteners market is to provide dependable and efficient solutions for joining and securing various components, materials, and structures.

There is no denying the significance of industrial fasteners, as they offer numerous benefits in terms of mechanical stability, durability, and simplicity of assembly. The term industrial refers to the process of converting raw materials into finished goods. Whether apparatus is being assembled, buildings are being constructed, or pipelines are being installed, fasteners ensure that the components remain securely affixed, enduring vibrations, dynamic loads, and environmental factors.

Due to advancements in materials, design techniques, and manufacturing processes, the industrial fasteners market has witnessed significant innovation. The development of high-strength alloys and composites, for instance, has led to the production of fasteners with enhanced tensile strength, corrosion resistance, and fatigue properties. In addition, the advent of technologies such as 3D printing has revolutionized the production of fasteners, allowing for complex geometries and customized designs.

These innovative fasteners have attracted significant investment and have been incorporated into a wide range of products and services across industries. Aerospace companies, for instance, rely significantly on high-performance fasteners to ensure the structural integrity and safety of aircraft. Advanced fastening systems are utilized by automakers to enhance vehicle performance, reduce vehicle weight, and improve fuel economy. The construction industry relies on specialized fasteners for securing building facades and merging structural components.

Increasing demand from industries including automotive, aerospace, construction, energy, and electronics is driving the growth of the industrial fasteners market. As these industries continue to grow and innovate, the need for dependable and effective fastening solutions becomes increasingly crucial. Moreover, the emergence of new applications, such as renewable energy systems and lightweight materials, augments the market's growth potential.

Driving factors

Growing industrial and building activity

The need for industrial fasteners is driven by construction and industry. Economic growth necessitates large-scale infrastructure, industries, and industrial units. These industries depend on fasteners to secure components. The structural integrity of buildings, bridges, and other structures is supported by the use of fasteners, which may be found in many different places. Thus, global urbanization and industrialization are driving the industrial fasteners market.

Automotive and aerospace growth

Fasteners are essential to assuring the performance, dependability, and safety of their products in the automotive and aerospace sectors, which are recognized for their relentless pursuit of innovation. High-quality, lightweight fasteners are needed as these sectors grow. Technologically enhanced fastening systems are needed by car manufacturers for fuel efficiency and safety and aerospace firms for lighter aircraft. Automotive and aerospace growth fuels industrial fasteners market development.

Growing need for robust fastening solutions

Extreme-pressure, vibration, and environmental fastening solutions are needed in many sectors. Industrial fasteners, which secure connections, prevent loosening, and improve efficiency, are essential to product safety and dependability. As enterprises in automotive, construction, and manufacturing seek trustworthy and lasting fastening solutions, the industrial fasteners market has grown.

Fastener and coating innovations

Fastener makers are always exploring new materials and coatings to improve performance and longevity. High-strength alloys, stainless steel, and corrosion-resistant coatings have made fasteners more resistant to wear, temperature changes, and chemical exposure. The market for industrial fasteners is strengthened by its ability to deliver long-lasting performance in demanding applications.

Globalizing commerce and manufacturing

Globalization has transformed commerce and production, expanding supply chains and cross-border cooperation. Manufacturers need trustworthy fastening solutions to satisfy production demands, which has increased demand for industrial fasteners. Fasteners secure parts and provide high-quality products during assembly. Thus, global commerce and production have boosted the industrial fasteners market.

Restraining Factors

Variations in Raw Material Prices

Prices of raw materials play a crucial function in the industrial fasteners market. Fluctuations in the prices of basic materials, such as steel, aluminum pigment, and plastics, can have a substantial effect on the profitability of manufacturers and alter the market's dynamics. These price fluctuations may be caused by a number of variables, such as global supply and demand, currency fluctuations, geopolitical events, and trade policies. As a participant in the industry, it is crucial to closely monitor these price fluctuations, make informed procurement decisions, and investigate alternative sourcing options in order to mitigate potential risks and maintain cost competitiveness.

Rivalry from Alternative Joining Techniques

Alternative methods of joining components, such as adhesives, welding, and riveting, pose potential competition in the market for industrial fasteners, which have been a tried-and-true method for decades. These alternative methods offer benefits in terms of lightweight designs, increased efficiency, and decreased assembly time. To remain ahead of the competition, manufacturers in the market for industrial fasteners must continuously innovate, improve their product offerings, and educate consumers about the distinct advantages of fasteners over alternative joining methods. Maintaining market dominance can be accomplished by highlighting the durability, dependability, and cost-effectiveness of fasteners in particular applications.

Obstacles to Compliance with Standards

The industrial fasteners market must adhere to stringent quality and regulatory standards to ensure safe and dependable operations. Due to the enormous variety of fastener types and applications, as well as the numerous international regulations and certifications, meeting these standards can be difficult. Manufactures must invest in stringent quality management systems, conduct routine audits, and engage in continuous improvement activities. Businesses can increase customer confidence, foster trust, and obtain a market advantage by assuring compliance with industry standards and certifications.

Cost and Supply Chain factors to consider

The market for industrial fasteners is cost-sensitive and requires efficient supply chain management. Frequently, the costs of basic materials, manufacturing processes, labor, and transportation increase for manufacturers. To remain competitive, it is essential to optimize the supply chain, streamline operations, and investigate opportunities for cost savings. By collaborating closely with suppliers, instituting lean manufacturing practices, and employing advanced technologies such as automation and predictive analytics, a business can increase operational efficiency, decrease expenses, and increase customer value.

Economic Recession Effects on End-User

The market for industrial fasteners is highly dependent on the performance of end-user industries such as the automotive, aerospace, construction, and machinery sectors. During economic downturns, these industries may experience a decline in demand, which may have repercussions for the demand for industrial fasteners. There may be obstacles such as decreased orders, inventory administration, and delayed payments. To navigate such difficult times, businesses should diversify their consumer base across numerous industries, invest in research and development, and cultivate strong customer relationships to form long-term partnerships.

Material Analysis

The industrial fasteners market is dominated by the metal segment, which accounts for a significant share of the overall market. Metal fasteners are widely used in various industries due to their durability, strength, and resistance to corrosion. They play a crucial role in providing structural integrity and reliability to the products they are used in.

Consumer trends and behavior towards the metal segment of industrial fasteners have also contributed to its dominance in the market. Consumers are increasingly focused on the quality and performance of the products they purchase. Metal fasteners are perceived as premium products that offer superior strength and reliability, which aligns with the consumer demand for durable and long-lasting products.

Product Type Analysis

Among the different types of industrial fasteners, the externally threaded segment holds the dominant position in the market. Externally threaded fasteners, such as bolts and screws, are extensively used in a wide range of applications, including construction, machinery, and automotive, among others. Their versatility, ease of installation, and ability to withstand heavy loads make them indispensable in various industries.

Consumer trends and behavior towards externally threaded fasteners have also contributed to their dominance in the market. Consumers value practicality and convenience, and externally threaded fasteners offer simplicity and ease of use. Their straightforward installation process and wide availability have made them a popular choice among consumers in various industries.

Application Analysis

The automotive segment dominates the industrial fasteners market, accounting for a significant share of the overall market. Fasteners play a critical role in the automotive industry, where they are used in various applications, including chassis, engine, body, and interior components. The automotive industry demands fasteners that can withstand high loads, vibrations, and extreme temperatures while maintaining structural integrity.

Consumer trends and behavior towards automotive fasteners have also contributed to the dominance of this segment in the market. Consumers are increasingly concerned about the safety, performance, and aesthetic appeal of their vehicles. Automotive fasteners play a crucial role in ensuring the overall quality and reliability of vehicles, thereby influencing consumer purchasing decisions.

Key Market Segments

By Material

- Metal

- Plastic

By Product Type

- Externally Threaded

- Internally Threaded

- Non-Threaded

- Aerospace Grade

By Application

- Automotive

- Aerospace

- Building & Construction

- Industrial Machinery

- Home appliances

- Furniture

- Other Applications

Growth Opportunity

Customized and Specialized Fasteners

The development of specialized and customized fasteners is one of the most significant growth opportunities in the industrial fasteners market. There is a growing demand for fasteners that meet specific requirements as a result of technological advances and changing consumer needs. This includes fasteners that are resistant to corrosion, capable of withstanding extreme temperatures, or designed for particular applications. Companies that can provide customized solutions to their customers have a competitive advantage and greater market growth potential.

Infrastructure Development

Infrastructure development in emergent markets represents a second opportunity for expansion. As several developing nations work to improve their infrastructure, the demand for industrial fasteners to support construction initiatives is growing. This creates a favorable environment for fastener manufacturers to enter these markets and satisfy the rising demand. Companies can capitalize on latent opportunities and position themselves for long-term growth by strategically targeting emerging economies with robust infrastructure development plans.

Manufacturers and Construction Firms

Collaboration with original equipment manufacturers (OEMs) and construction firms is an additional growth opportunity for the industrial fasteners market. OEMs play a crucial role in a variety of industries, and their partnerships with fastener manufacturers can fuel market expansion and development. By working closely with original equipment manufacturers, fastener manufacturers can ensure that their products are seamlessly incorporated into the overall manufacturing process. Similarly, establishing solid relationships with construction firms enables fastener manufacturers to become preferred suppliers for large-scale projects, thereby enhancing their growth potential.

Lightweight and Strong Fastener Components

Adoption of lightweight and high-strength fastening materials also presents a substantial growth opportunity for the industrial fasteners market. Lightweight materials such as titanium and aluminum are acquiring popularity as industries strive to improve efficiency, reduce costs, and boost performance. These materials have high strength-to-weight ratios, making them ideal for applications in which weight reduction is crucial. Companies that invest in R&D to create innovative fasteners with these materials can increase their market share and stimulate growth.

Latest Trends

Automotive/Aerospace Fastener Growth

Automotive and aerospace industries have grown rapidly, increasing demand for specialty fasteners that fulfill their strict criteria. Advanced fastening systems are needed to meet automobile industry demands for lightweighting, safety, and performance. These fasteners protect crucial components from excessive stress and vibration. In the aircraft engines business, fasteners must resist severe temperatures, pressures, and stresses for safety and dependability. Manufacturers are investing in R&D to improve automotive and aerospace fasteners' performance and efficiency.

Corrosion-Resistant and High-Performance Fastener

Corrosion threatens infrastructure, maritime equipment, and industrial gear. Corrosion-resistant fasteners that can tolerate hostile environments are in demand to address this issue. Industries choose corrosion-resistant materials like stainless steel and specialized alloys. In harsh working circumstances like oil and gas, high-performance fasteners that can endure high temperatures, pressures, and mechanical strains are in demand.

Self-Locking and Tamper-Resistant Fasteners

Industries must ensure component safety and security. Self-locking and tamper-resistant fasteners meet this demand. Nylon patches or pellets prevent self-locking fasteners from loosening. These fasteners are used in safety-critical industries including aviation and automotive. Tamper-resistant fasteners also prevent unwanted entry. Electronics, healthcare, and public infrastructure benefit from this.

Lightweight and Composite Fasteners Rise

Composites are becoming more popular as sectors prioritize weight reduction and fuel economy. Traditional fasteners may not bind these materials well. Manufacturers are developing lightweight and composite fasteners. These fasteners use new designs, coatings, and materials to increase bonding strength without losing composite weight savings. Lightweight sectors including automotive, aerospace, and renewable energy require such fasteners.

Automated Fastening Systems

Automation and Industry 4.0 are replacing manual fastening procedures. Automated fastening systems are faster, more accurate, and less error-prone. These systems use robots, AI, and machine vision to fasten accurately. In industries like automotive, electronics, and aerospace, where large-scale manufacturing and quality control are essential, automated fastening systems have grown. Manufacturers will continue to automate fastening operations.

Regional Analysis

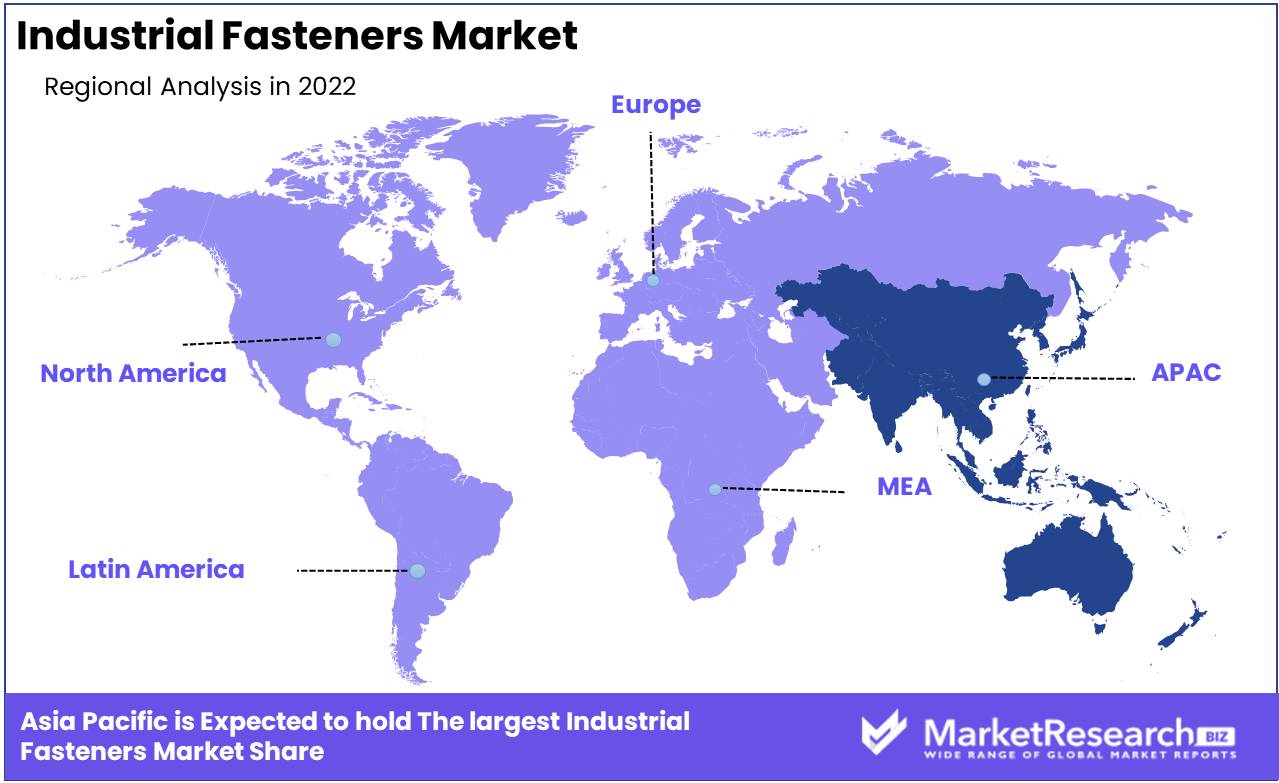

The Industrial Fasteners market is dominated by the Asia-Pacific region. In recent years, the market for industrial fasteners has expanded significantly, primarily due to the rising demand for efficient and dependable fastening solutions in a variety of industries. A significant portion of the market has been captured by the Asia-Pacific (APAC) region, which has evolved as a dominant force among global regions. APAC continues to drive the growth of the industrial fasteners market with its flourishing manufacturing sector, robust infrastructure development, and rapid industrialization.

As businesses strive to increase productivity, enhance efficiencies, and ensure the safety and longevity of their products, the demand for high-quality fastening solutions grows. Industrial fasteners are essential for joining different components, ensuring structural integrity, and facilitating effortless disassembly when necessary. Among others, they have extensive applications in the automotive, aerospace, construction, electronics, and machinery industries.

The Asia-Pacific region, which includes China, India, Japan, South Korea, and ASEAN countries, has a substantial manufacturing sector. Strong demand for industrial fasteners has been primarily driven by the proliferation of manufacturing facilities in these nations. For example, the automotive industry relies extensively on fasteners for vehicle assembly. As APAC continues to be a global manufacturing center, the demand for automotive fasteners has skyrocketed, contributing to the region's market dominance.

Manufacturers, suppliers, and industry stakeholders must strategically position themselves to capitalize on the region's development potential as Asia-Pacific continues to dominate the global industrial fasteners market. Companies can gain a competitive advantage in this ever-changing environment by remaining attuned to shifting market trends, leveraging technology and innovation, and providing high-quality, customized fastening solutions.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

Switzerland-based ABB Limited leads power and automation technology. ABB offers several productivity, efficiency, and safety solutions in the industrial fasteners market. ABB fasteners are reliable, durable, and high-performing. Robotics, electrical systems, and automation help the firm create new fastening solutions for automotive, aerospace, and industrial industries.

Siemens AG, a German multinational, dominates the industrial fasteners market. Siemens provides fastening solutions for industrial industries such as power generation, transportation, and infrastructure. Siemens fasteners are precision-made and tested to assure longevity and performance. Sustainability and innovation have made the firm a market leader.

US-based Honeywell International Inc. is known for its wide range of industrial products and solutions. Precision, dependability, and efficiency characterize the company's fastening solutions. Honeywell's diversified fasteners perform in difficult applications, enabling safe and secure operations in aerospace, military, and oil & gas. Honeywell introduces new fastening technologies to fulfill client needs via research and development.

Industrial automation leader Rockwell Automation also knows industrial fasteners. Customers get comprehensive production solutions from the company's fasteners, which interface easily with its automation and control systems. Rockwell Automation's fastening products are high-quality, reliable, and compatible, enabling uninterrupted operations in automotive, food & beverage, and pharmaceutical sectors.

Baumer Ltd., based in Switzerland, makes top-notch industrial sensors and equipment. The company's fasteners complement its sensors, providing accurate and dependable mounting options in numerous applications. Baumer's durable, accurate, and easy-to-install fastening products are trusted globally. Baumer improves manufacturing, medical, and agricultural efficiency by integrating sensors and fasteners.

US-based Encoder Products Company Inc. makes high-performance encoders and sensors. The company's encoder solutions and fasteners interact flawlessly to improve position and motion detection accuracy. Robotics, industrial automation, and renewable energy use Encoder devices Company's strong, precise, and compatible fastening devices. The firm guarantees that their fasteners match global client demands with a strong focus to customer satisfaction.

Top Key Players in Industrial Fasteners Market

- ABB Limited (Switzerland)

- Siemens AG (Germany)

- Honeywell International Inc. (U.S.)

- Rockwell Automation (U.S.)

- Baumer Ltd (Switzerland)

- Encoder Products Company Inc (U.S.)

- Fuji Electric Co. Ltd. (Japan)

- Delta Electronics Inc (Taiwan)

- Emerson Electric (U.S.)

- Omron Corporation (Japan)

- Panasonic Corporation (Japan)

- Baumuller Holding GmbH & Co. KG (Germany)

- Balluff GmbH (Germany)

- Sensata Technologies Inc (U.S.)

- Festo Corporation (Germany)

- Parker-Hannifin Corporation (U.S.)

- SMC Corporation (Japan)

- DESTACO (U.S.)

- SWISS Automation Inc (U.S.)

- Mitsubishi Electric Corporation (Japan)

Recent Development

- Fastenal Corporation to Open New Distribution Center in China (2023): This strategic move is aimed at meeting the growing demand for industrial fasteners and enhancing the company's supply chain capabilities in the region.

- Stanley Black & Decker's Acquisition of Black Hills Industrial Group (2022): This move is expected to bolster Stanley Black & Decker's product portfolio, particularly in the industrial fasteners sector.

- Würth Group to Establish New Manufacturing Plant in Mexico (2021): This expansion reflects Würth Group's commitment to meeting the growing demand for industrial fasteners in the region while ensuring proximity to key markets.

- Acument Global Technologies' Acquisition of Apex Tool Group (2020): This strategic move aims to broaden Acument's product range by adding Apex Tool Group's extensive portfolio of high-quality tools and fastening solutions.

Report Scope:

Report Features Description Market Value (2022) USD 97.2 Bn Forecast Revenue (2032) USD 155.0 Bn CAGR (2023-2032) 4.9% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material (Metal, Plastic )

By Product Type (Externally Threaded, Internally Threaded, Non-Threaded, Aerospace Grade)

By Application (Automotive, Aerospace, Building & Construction, Industrial Machinery, Home appliances, Furniture, Other ApplicationsRegional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape ABB Limited (Switzerland), Siemens AG (Germany), Honeywell International Inc. (U.S.), Rockwell Automation (U.S.), Baumer Ltd (Switzerland), Encoder Products Company Inc (U.S.), Fuji Electric Co. Ltd. (Japan), Delta Electronics Inc (Taiwan), Emerson Electric (U.S.), Omron Corporation (Japan), Panasonic Corporation (Japan), Baumuller Holding GmbH & Co. KG (Germany), Balluff GmbH (Germany), Sensata Technologies Inc (U.S.), Festo Corporation (Germany), Parker-Hannifin Corporation (U.S.), SMC Corporation (Japan), DESTACO (U.S.), SWISS Automation Inc (U.S.), Mitsubishi Electric Corporation (Japan) Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- ABB Limited (Switzerland)

- Siemens AG (Germany)

- Honeywell International Inc. (U.S.)

- Rockwell Automation (U.S.)

- Baumer Ltd (Switzerland)

- Encoder Products Company Inc (U.S.)

- Fuji Electric Co. Ltd. (Japan)

- Delta Electronics Inc (Taiwan)

- Emerson Electric (U.S.)

- Omron Corporation (Japan)

- Panasonic Corporation (Japan)

- Baumuller Holding GmbH & Co. KG (Germany)

- Balluff GmbH (Germany)

- Sensata Technologies Inc (U.S.)

- Festo Corporation (Germany)

- Parker-Hannifin Corporation (U.S.)

- SMC Corporation (Japan)

- DESTACO (U.S.)

- SWISS Automation Inc (U.S.)

- Mitsubishi Electric Corporation (Japan)

Our Clients

View Our Licence Options