Independent Software Vendors (ISVs) Market By Type Outlook (Cloud-based and On-premises), By Application Outlook( E-Commerce,, Logistics, Retail, Healthcare, Financial, Educational, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

22282

-

May 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

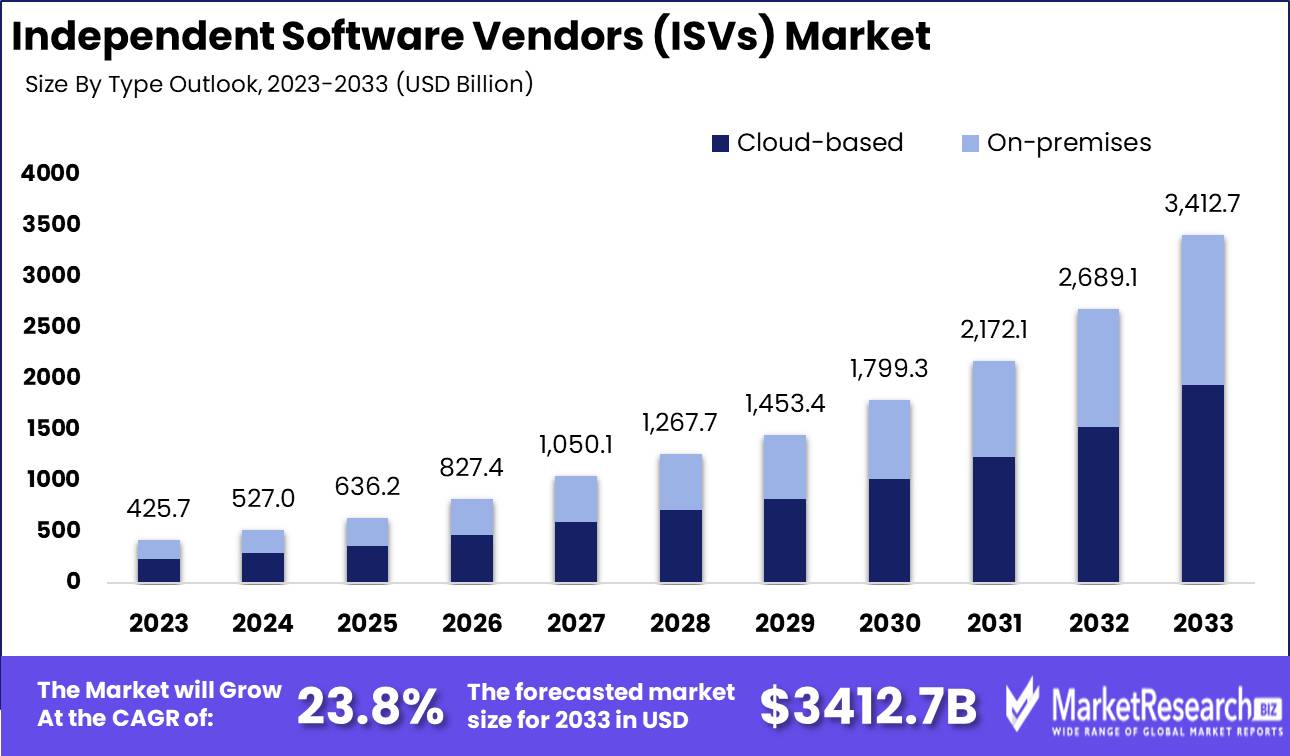

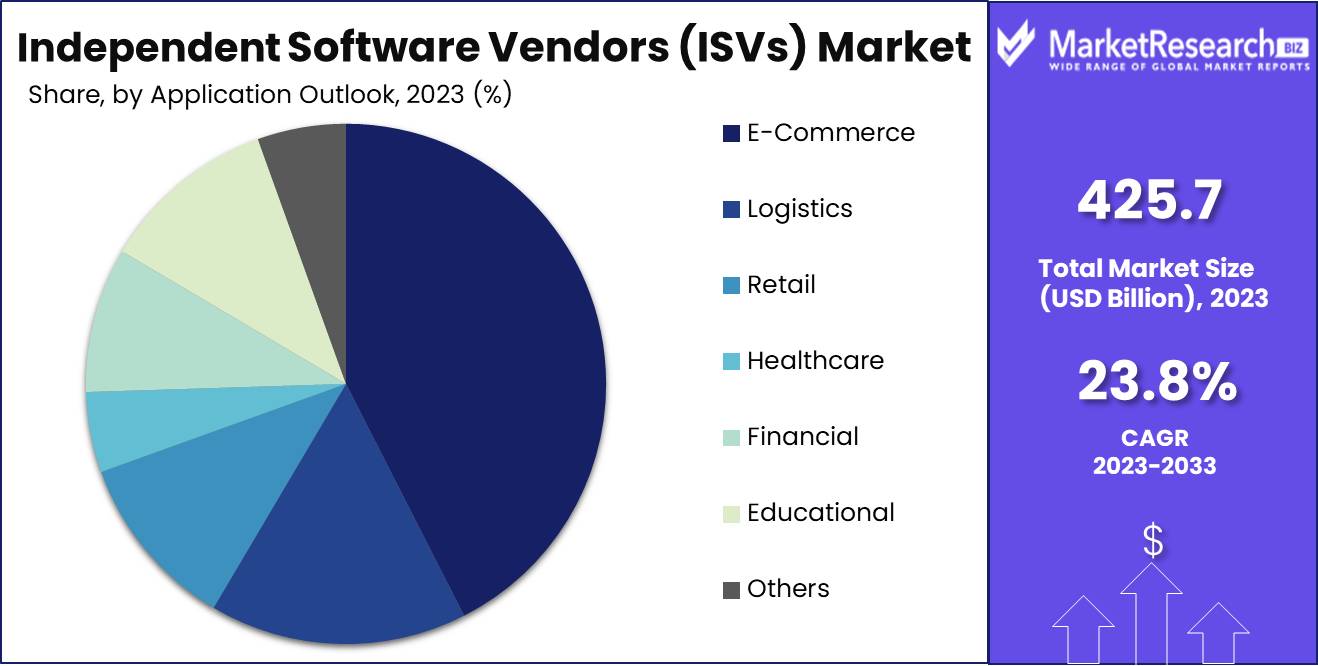

The Independent Software Vendor (ISVs) Market was valued at USD 425.7 billion in 2023. It is expected to reach USD 3412.7 billion by 2033, with a CAGR of 23.8% during the forecast period from 2024 to 2033.

The surge in demand for original equipment manufacturers and high value-added services by the end-use customers are some of the main driving factors for the independent software vendors market. An Independent software vendor commonly known as ISV is an individual or firm that creates, markets, and sells all software solutions that run on one computer hardware supplier. It comprises Macintosh, OS like IOS, or cloud platforms like Amazon web services. These vendors have transformed into one of the main requirements in the IT industry by promoting the latest technologies and services. ISV develops software products that can run on all backend channels like Windows and Linux.

Many independent software vendors are personalized in creating software applications for specific sector verticals. This is unique from the in-house software or personalized software that is developed for in-house purposes or changed for a specific or particular third party. ISVs are thinking of offering software that can run on virtual appliances and tools and moving for cloud delivery as cloud computing becomes more prevalent. For example, any firm that provides its software solution in a market sector like Hubspot Connect or Salesforce AppExchange is called an independent software vendor.

Independent software vendors should have ISV certifications as such vendors can provide the best and most relevant services in the market area. For example, Salesforce’s AppExchange permits ISV providers to offer their client services. Salesforce provides a program named Salesforce Certified that integrates technical, security, and market examinations to verify quality. Only the independent software vendors that have successfully completed such type of program can provide their services on AppExchange, by making sure the clients are opting for the finest and best options.

Independent software vendors with ISV certifications can enhance visibility and help in brand recognition. It also helps in gaining access to new customers. Many collaborator channels provide built-in promotions like sponsored listing in their market area and in blog posts, PRs, webinars, and seminar resources. This helps to gain more product visibility. Such type of ISV-certified programs help boost the brands that will help to increase revenue. The demand for ISVs will increase due to their high-end requirement in the IT industries which will help in market expansion during the forecasted period.

Key Takeaways

- Market Growth: The Independent Software Vendor (ISVs) Market was valued at USD 425.7 billion in 2023. It is expected to reach USD 3412.7 billion by 2033, with a CAGR of 23.8% during the forecast period from 2024 to 2033.

- By Type Outlook: In 2023, cloud-based solutions dominated ISVs, driven by scalability and flexibility.

- By Application Outlook: In 2023, E-Commerce led ISV market growth across multiple sectors.

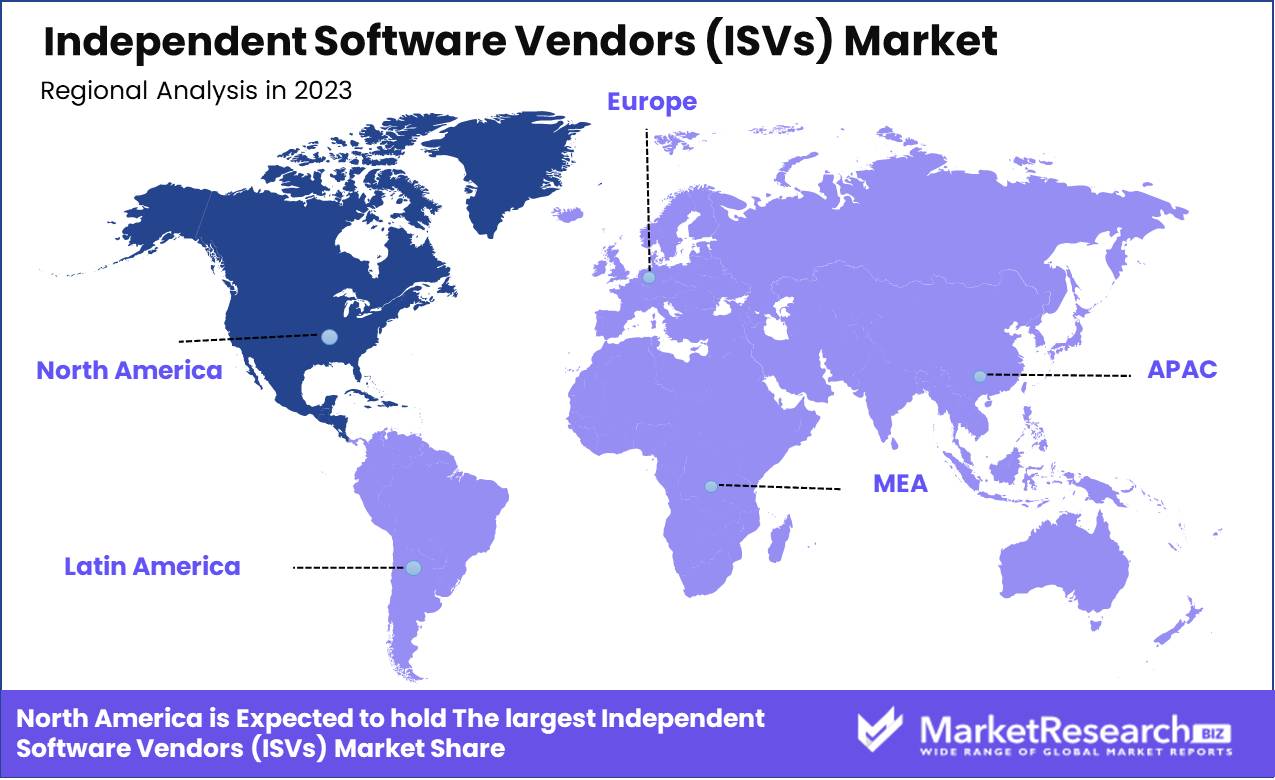

- Regional Dominance: North America leads the ISVs market with a 40% share, driving global growth.

- Growth Opportunity: ISVs can achieve growth by focusing on cloud-native, AI-enhanced solutions and strategic technology partnerships.

Driving factors

Rising Demand for Multi-cloud & Hybrid Cloud Systems

The increasing preference for multi-cloud and hybrid cloud systems is a significant driver of growth in the Independent Software Vendors (ISVs) market. Multi-cloud strategies allow organizations to leverage multiple cloud based services from different providers, optimizing performance, reducing latency, and enhancing reliability. Hybrid cloud systems, combining private and public cloud resources, offer greater flexibility and scalability.

This demand is driven by the need for improved data management, enhanced security, and regulatory compliance. A survey by Flexera indicates that 92% of enterprises have a multi-cloud strategy, with 80% adopting a hybrid cloud approach. These trends necessitate robust, interoperable software solutions, creating substantial opportunities for ISVs to develop and integrate cloud-compatible applications and services, thereby expanding their market presence and enhancing customer satisfaction.

Growing Adoption of Software as a Service (SaaS)

The surge in Software as a Service (SaaS) adoption is a pivotal factor contributing to the expansion of the ISVs market. SaaS offers a cost-effective, scalable, and easily deployable solution for businesses, eliminating the need for extensive on-premise infrastructure.

ISVs are increasingly capitalizing on this trend by developing SaaS-based solutions, enabling businesses to access sophisticated software tools via subscription models. This shift not only reduces upfront costs but also ensures continuous updates and support, enhancing user experience and operational efficiency. The scalability and flexibility of SaaS platforms align with the dynamic needs of businesses, driving demand for innovative ISV solutions and fostering market growth.

Increased Demand for Value-Added Services

The growing demand for value-added services is significantly propelling the ISV market forward. Value-added services, including customization, consulting, integration, and technical support, enhance the core functionalities of software products, offering tailored solutions to meet specific business needs.

ISVs that provide these additional services differentiate themselves from competitors by delivering comprehensive solutions that address the unique challenges of their clients. This differentiation enhances customer satisfaction and loyalty, leading to increased market share and revenue opportunities. Moreover, value-added services enable ISVs to build long-term relationships with clients, fostering continuous innovation and adaptation to evolving market demands, thereby reinforcing their market position and growth trajectory.

Restraining Factors

Data Security Concerns: A Critical Barrier to ISV Market Expansion

Data security concerns are a significant impediment to the growth of the Independent Software Vendors (ISVs) market. As businesses increasingly adopt digital solutions, the safeguarding of sensitive information has become paramount. ISVs are often seen as potential weak links in cybersecurity, given that their applications integrate with broader IT ecosystems. This perception can lead to hesitance among potential clients, particularly in sectors where data sensitivity is paramount, such as finance and healthcare.

Recent statistics highlight that 74% of businesses prioritize data security when choosing software solutions, underscoring the impact of security concerns on ISV adoption rates. Moreover, regulatory frameworks like GDPR in Europe and CCPA in California impose stringent data protection requirements, adding compliance burdens on ISVs. This regulatory pressure necessitates substantial investment in security measures, which can be particularly challenging for smaller ISVs with limited resources.

Integration Challenges: A Barrier to Seamless ISV Adoption

Integration challenges pose a substantial barrier to the growth of the ISV market. As businesses seek to enhance operational efficiency, the ability to seamlessly integrate new software solutions with existing IT infrastructure is crucial. ISVs often face difficulties in achieving compatibility with diverse legacy systems, which can lead to increased deployment times and costs.

Statistics indicate that 67% of companies identify integration complexity as a primary obstacle to adopting new software solutions. This complexity is compounded by the heterogeneous nature of IT environments across industries, necessitating bespoke integration efforts for each client. Additionally, the rapid pace of technological advancement means that ISVs must continuously update their solutions to maintain compatibility, further straining their development resources.

By Type Outlook Analysis

In 2023, cloud-based solutions dominated ISVs, driven by scalability and flexibility.

In 2023, Cloud-based solutions held a dominant market position in the By Type Outlook segment of the Independent Software Vendors (ISVs) Market. The cloud-based software approach has been increasingly favored due to its scalability, cost-efficiency, and flexibility, which cater to the dynamic needs of businesses aiming to innovate rapidly without the burden of extensive IT infrastructure investments. This model facilitates seamless updates, enhances collaboration, and supports remote work environments, thereby appealing to a broad spectrum of ISVs seeking to leverage cloud technology for competitive advantage and operational efficiency.

Conversely, On-premises solutions, while still significant, have seen a relatively subdued growth trajectory. This traditional model offers enhanced control over data security and customization, making it a preferred choice for organizations with stringent regulatory requirements and those seeking to maintain legacy systems. Despite the growing inclination towards cloud-based solutions, on-premises systems retain their relevance, particularly in sectors where data sovereignty and compliance are critical, ensuring their continued presence in the ISV market landscape.

By Application Outlook Analysis

In 2023, E-Commerce led ISV market growth across multiple sectors.

In 2023, E-Commerce held a dominant market position in the By Application Outlook segment of the Independent Software Vendors (ISVs) Market. The rise in online retail has driven demand for robust e-commerce solutions, propelling ISVs to innovate and offer specialized software to enhance user experiences, streamline operations, and integrate advanced analytics. Logistics, closely tied to e-commerce growth, has also seen substantial investments in software solutions for tracking, inventory management, and supply chain optimization.

In Retail, ISVs have focused on developing point-of-sale systems, customer relationship management, and personalized shopping experiences. The Healthcare sector's digitization has spurred the adoption of electronic health records, telemedicine platforms, and patient management systems, positioning it as a critical ISV market. Financial services have increasingly relied on ISVs for fintech solutions, cybersecurity, and compliance management tools. Educational institutions' shift towards digital learning has boosted demand for e-learning platforms, student information systems, and virtual classrooms. The 'Others' category encompasses diverse applications, including manufacturing, entertainment, and energy, where ISVs provide tailored solutions to meet specific industry needs, further underscoring the sector's expansive growth potential.

Key Market Segments

By Type Outlook

- Cloud-based

- On-premises

By Application Outlook

- E-Commerce

- Logistics

- Retail

- Healthcare

- Financial

- Educational

- Others

Growth Opportunity

Increasing Adoption of Cloud-Based Solutions

In 2024, the global ISV market is poised for significant growth, driven predominantly by the increasing adoption of cloud-based solutions. As enterprises continue to shift from traditional on-premises software to cloud-based platforms, ISVs have a unique opportunity to innovate and expand their offerings. This trend is underpinned by the need for scalable, cost-effective, and flexible solutions that can adapt to dynamic business environments.

Cloud platforms provide ISVs with the infrastructure to deploy and manage their software with greater efficiency, reducing time-to-market and enabling rapid iteration and deployment of updates. Furthermore, cloud solutions enhance collaboration and accessibility, allowing ISVs to cater to a global customer base with diverse needs. As businesses seek to optimize their IT expenditures and enhance operational agility, ISVs that leverage cloud capabilities will likely see substantial demand growth.

Leveraging Artificial Intelligence and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are set to be game-changers for ISVs in 2024, offering transformative opportunities to enhance product offerings and drive competitive differentiation. By integrating AI and ML, ISVs can provide advanced analytics, predictive insights, and automation capabilities, which are increasingly sought after by businesses aiming to harness data-driven decision-making. These technologies enable ISVs to offer more personalized and intelligent solutions, enhancing user experience and operational efficiency.

For instance, AI-powered features such as natural language processing, image recognition, and predictive maintenance can significantly enhance the value proposition of software products across various industries. As organizations continue to prioritize digital transformation, ISVs that embed AI and ML into their solutions will be well-positioned to capitalize on this trend, driving innovation and growth in the competitive software landscape.

Latest Trends

Emphasis on Cybersecurity Amidst 5G Integration

As the global Independent Software Vendors (ISVs) market progresses into 2024, the convergence of cybersecurity and 5G technology stands out as a pivotal trend. The rapid deployment of 5G networks is significantly enhancing data transmission speeds and connectivity, offering ISVs a robust platform to develop more sophisticated and scalable software solutions.

However, this increased connectivity also presents heightened security challenges. ISVs are thus prioritizing the integration of advanced cybersecurity measures to protect sensitive data and maintain robust defense mechanisms against evolving cyber threats. This dual focus on leveraging 5G's capabilities while ensuring stringent cybersecurity protocols is expected to drive substantial innovation and differentiation in the ISV sector.

Rise of Low-code Software Development Accelerates Digital Transformation

In 2024, low-code software development platforms are emerging as a critical catalyst for digital transformation within the ISV market. These platforms enable businesses to accelerate application development processes by minimizing the need for extensive coding expertise. This trend is particularly significant as it democratizes software development, empowering a broader range of organizations to create custom applications swiftly and efficiently.

ISVs are capitalizing on this trend by offering comprehensive low-code solutions that streamline workflows, enhance operational agility, and reduce time-to-market. As businesses seek to enhance their digital capabilities, the adoption of low-code platforms is poised to become a cornerstone of modern software development strategies, fostering innovation and competitiveness across various industries.

Regional Analysis

North America leads the ISVs market with a 40% share, driving global growth.

The Independent Software Vendors (ISVs) market demonstrates significant regional diversity, with North America leading at approximately 40% market share, driven by technological innovation hubs such as Silicon Valley and a high adoption rate of advanced IT solutions. In Europe, the ISV market is robust, particularly in Germany, the UK, and France, supported by a strong emphasis on digital transformation and a mature enterprise software landscape.

The Asia Pacific region is experiencing rapid growth, with a notable surge in countries like China and India, reflecting a CAGR of over 12% due to increasing digitalization and the proliferation of SMEs leveraging cloud-based solutions. The Middle East & Africa region, while smaller in market share, is seeing steady growth driven by IT investments in Gulf countries and increasing demand for customized software solutions across sectors like banking and retail. Latin America presents a burgeoning market, with Brazil and Mexico at the forefront, spurred by rising IT infrastructure development and growing enterprise software needs. North America remains the dominant region, underpinned by substantial R&D investments, a dynamic startup ecosystem, and strong demand for enterprise and SaaS applications.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global Independent Software Vendors (ISVs) market continues to be shaped by industry leaders such as IBM, Microsoft, SAP SE, Salesforce, Oracle, Google, Inc., Apple Inc., Dell, Inc., HPE, Compuware(BMC), ServiceNow, Symantec Corporation (Broadcom), Cisco Systems, Inc., Carbonite, Inc. (OpenText), and Mocana. These key players represent a diverse array of expertise and solutions, each contributing significantly to the advancement and evolution of the ISV landscape.

IBM, Microsoft, and SAP SE maintain their stronghold with robust offerings across various sectors, leveraging their extensive experience and technological prowess. Salesforce, Oracle, and Google, Inc. continue to innovate, particularly in cloud-based solutions and data analytics, catering to the growing demand for scalable and efficient software services.

Meanwhile, emerging players like Apple Inc., Dell, Inc., and HPE are making notable strides, capitalizing on their unique strengths and market niches. ServiceNow and Compuware(BMC) are increasingly recognized for their contributions to IT service management and application development, respectively.

Market Key Players

- IBM

- Microsoft

- SAP SE

- Salesforce

- Oracle

- Google, Inc.

- Apple Inc.

- Dell, Inc

- HOPE

- Compuware(BMC)

- ServiceNow

- Symantec Corporation (Broadcom)

- Cisco Systems, Inc.

- Carbonite, Inc. (OpenText)

- Mocana

Recent Development

- In May 2024, Crayon Software Experts India expands to East India, opening a dedicated ISV Incubation Center in Kolkata, aimed at fostering local startups and ISVs in crafting cloud-based solutions for public sector challenges.

- In April 2024, Coherent Market Insights, – The Global Independent Software Vendors (ISVs) Market report from 2024 to 2031 offers a comprehensive analysis of market dynamics, competitive strategies, and growth prospects across various regions and industries.

- In January 2024, Payroc unveiled its cloud-based payment solution, PayByCloud, simplifying omnichannel payment integrations for independent software vendors (ISVs), reducing complexity, and streamlining transactions with a 'low code' semi-integrated approach.

Report Scope

Report Features Description Market Value (2023) USD 425.7 Billion Forecast Revenue (2033) USD 3412.7 Billion CAGR (2024-2032) 23.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type Outlook (Cloud-based and On-premises), By Application Outlook( E-Commerce,, Logistics, Retail, Healthcare, Financial, Educational, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape IBM, Microsoft, SAP SE, Salesforce, Oracle, Google, Inc., Apple Inc., Dell, Inc, HPE, Compuware(BMC), ServiceNow, Symantec Corporation (Broadcom), Cisco Systems,Inc., Carbonite, Inc. (OPENTEXT), Mocana Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- IBM

- Microsoft

- SAP SE

- Salesforce

- Oracle

- Google, Inc.

- Apple Inc.

- Dell, Inc

- HPE

- Compuware(BMC)

- ServiceNow

- Symantec Corporation (Broadcom)

- Cisco Systems, Inc.

- Carbonite, Inc. (OPENTEXT)

- Mocana

Our Clients

View Our Licence Options