Hypoglycemic Drugs Market By Drug Class (Sulphonylareas, Biguanides, Alpha-glucosidase inhibitors, Thiazolidinediones, Dipetidylpeptidase-4(DPP-4), Glucagoan), By Route of Administration (Oral, Injectable, Nasal), By Distribution Channel (Hospital Pharmacies, Retail Pharamcies, Online Pharamcies), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

46887

-

June 2024

-

136

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

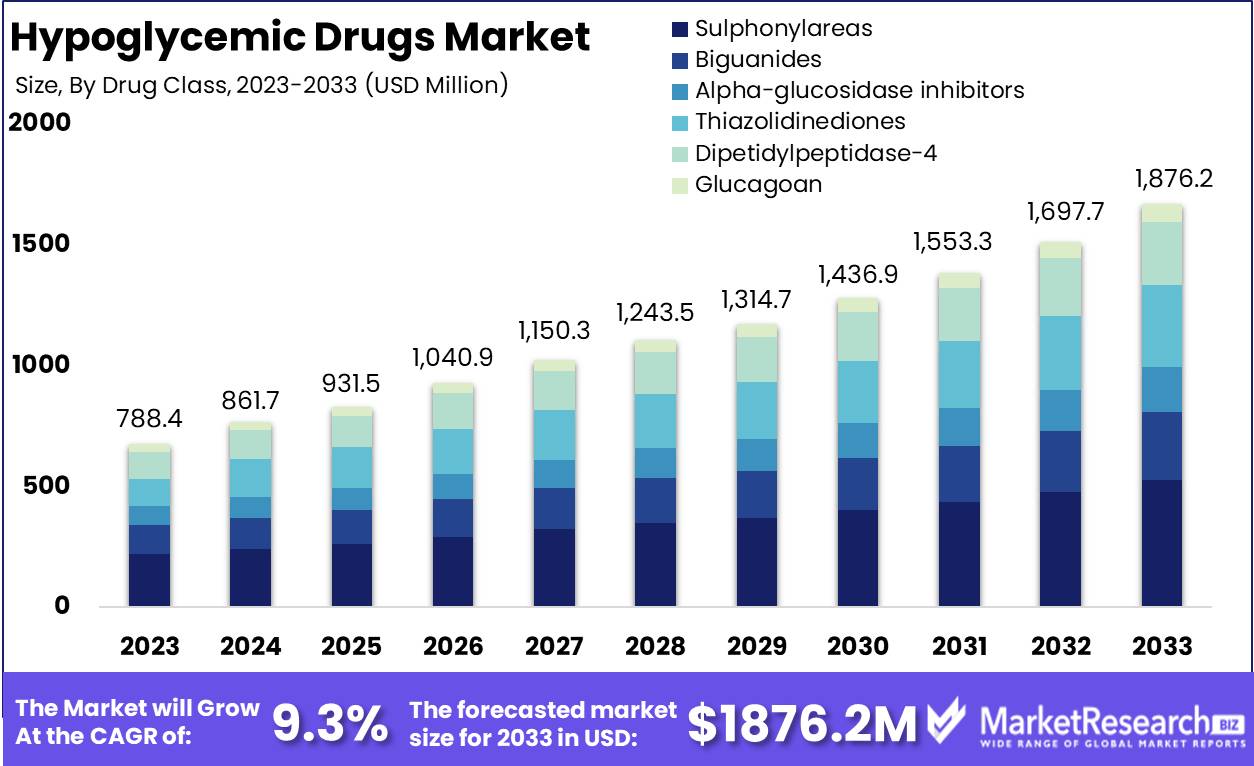

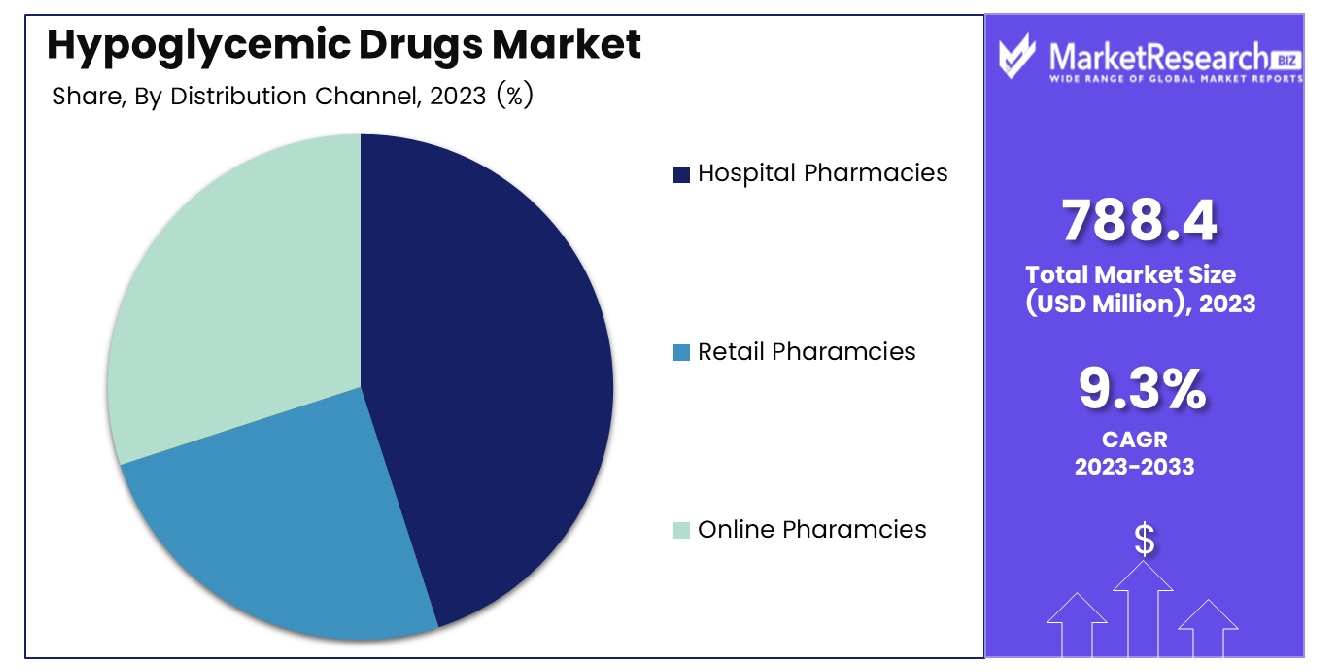

The Global Hypoglycemic Drugs Market was valued at USD 788.4 Mn in 2023. It is expected to reach USD 1876.2 Mn by 2033, with a CAGR of 9.3% during the forecast period from 2024 to 2033.

The Hypoglycemic Drugs Market encompasses pharmaceuticals designed to manage blood glucose levels in individuals suffering from diabetes. These medications, including insulin and oral hypoglycemic agents, play a pivotal role in controlling hyperglycemia, thereby reducing the risk of diabetic complications. With the rising global prevalence of diabetes, this market experiences continual evolution in drug development, delivery mechanisms, and patient-centric solutions. Market dynamics are influenced by factors such as technological advancements, regulatory landscapes, and shifting healthcare paradigms.

The Hypoglycemic Drugs Market continues to exhibit robust growth and dynamic evolution, driven by a myriad of factors shaping the landscape of diabetes management globally. With approximately 200 million individuals worldwide afflicted by Type 2 diabetes, the demand for effective therapeutic interventions remains pressing, especially among the burgeoning elderly population in developed nations. Dipeptidyl peptidase-4 (DPP-4) inhibitors, hailed as a novel class of oral antidiabetic agents, have emerged as a pivotal treatment option for individuals unresponsive to conventional medications like metformin and sulphonylureas. Their effectiveness and tolerability profile underscore their prominence in clinical practice, contributing significantly to market expansion.

The advent of GLP-1 receptor agonists such as exenatide and liraglutide heralds a paradigm shift in diabetes management strategies. These agents, mimicking the actions of the incretin hormone GLP-1, exhibit dual benefits of enhancing insulin secretion while suppressing glucagon release, thereby fostering glycemic control. Their efficacy in improving not only glycemic parameters but also cardiovascular outcomes underscores their growing adoption in clinical settings.

Against the backdrop of an aging population and the escalating prevalence of diabetes, stakeholders in the Hypoglycemic Drugs Market are poised to navigate a dynamic landscape characterized by evolving treatment modalities, stringent regulatory frameworks, and shifting patient preferences. Strategic initiatives centered on innovation, patient-centricity, and market expansion will be imperative to capitalize on emerging opportunities and drive sustainable growth in this vital therapeutic domain.

Key Takeaways

- Market Value: The Global Hypoglycemic Drugs Market was valued at USD 788.4 Mn in 2023. It is expected to reach USD 1876.2 Mn by 2033, with a CAGR of 9.3% during the forecast period from 2024 to 2033.

- By Drug Class: Sulphonylureas dominate the hypoglycemic drugs market, holding approximately 42% of the market share, driven by their long-standing efficacy and widespread use in the management of type 2 diabetes.

- By Route of Administration: Oral administration leads the route of administration segment in the hypoglycemic drugs market with 39% of the market share, primarily due to patient preference for non-invasive treatment options and the convenience of oral medications.

- By Distribution Channel: Hospital pharmacies dominate the distribution channel segment of the hypoglycemic drugs market with a substantial 45% market share, reflecting their critical role in providing specialized diabetes care and ensuring the availability of essential medications.

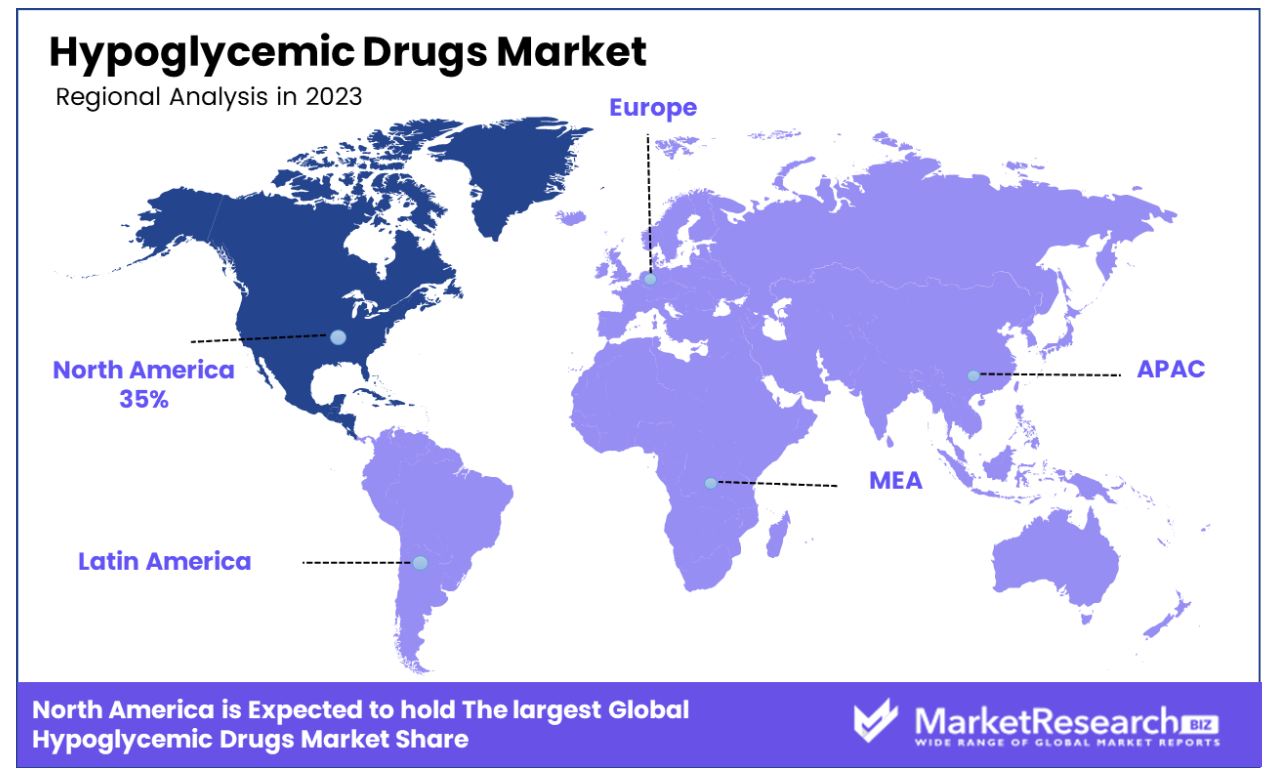

- Regional Dominance: North America dominates the hypoglycemic drugs market with 35% share, driven by high diabetes prevalence and advanced healthcare infrastructure.

- Growth Opportunity: The hypoglycemic drugs market presents a promising growth opportunity fueled by rising diabetes prevalence globally, technological advancements in drug delivery systems, and increasing healthcare expenditure.

Driving factors

Increasing Diabetes Prevalence

The escalating prevalence of diabetes globally is a significant driver for the growth of the hypoglycemic drugs market. Diabetes, particularly type 2 diabetes, is becoming more common due to various factors such as aging populations, sedentary lifestyles, and rising obesity rates. According to the International Diabetes Federation (IDF), approximately 537 million adults (20-79 years) were living with diabetes in 2021, and this number is expected to rise to 643 million by 2030 and 783 million by 2045.

This surge in diabetes cases creates a substantial demand for effective hypoglycemic medications, as managing blood glucose levels becomes a critical aspect of diabetes care. The chronic nature of diabetes ensures a continuous and growing need for these drugs, thus significantly contributing to the expansion of the market.

Growing Awareness and Education

Increased awareness and education about diabetes management are also pivotal in driving the hypoglycemic drugs market. Educational initiatives by healthcare organizations, governments, and pharmaceutical companies have been instrumental in informing the public about the importance of managing blood glucose levels to prevent complications. Awareness campaigns have successfully highlighted the availability of advanced hypoglycemic drugs and the benefits of early intervention and consistent treatment.

The role of healthcare professionals in educating patients about diabetes management cannot be overstated. Improved patient knowledge leads to better adherence to prescribed medications, ultimately enhancing treatment outcomes. According to a study published by the American Diabetes Association, patient education and self-management support have been shown to improve glycemic control, which translates into increased demand for hypoglycemic drugs.

Restraining Factors

Side Effects and Safety Concerns

While the increasing prevalence of diabetes and heightened awareness are driving forces behind the hypoglycemic drugs market, side effects and safety concerns can act as significant restraints. Hypoglycemic drugs, like all medications, come with potential side effects ranging from mild to severe. Common side effects include gastrointestinal issues, weight gain, and hypoglycemia (dangerously low blood sugar levels). For instance, drugs such as sulfonylureas and insulin can cause hypoglycemia, which is a critical concern for many patients.

Safety issues can deter patients and healthcare providers from opting for specific hypoglycemic drugs, potentially slowing market growth. Patients may discontinue use due to adverse effects, and physicians might be cautious in prescribing medications with known risks, thus affecting overall market demand. Consequently, pharmaceutical companies are investing heavily in the development of safer and more effective medications, aiming to minimize these concerns and restore patient and provider confidence.

Competition from Other Therapies

The hypoglycemic drugs market faces significant competition from alternative therapies, which can limit its growth. These competing therapies include non-pharmacological interventions, emerging treatment modalities, and innovative technologies.

Lifestyle modifications such as diet and exercise are crucial in diabetes management. For some patients, especially those with prediabetes or early-stage type 2 diabetes, these interventions can be effective enough to delay or even avoid the need for hypoglycemic drugs. Programs promoting weight loss and physical activity are gaining traction, supported by evidence showing their efficacy in improving glycemic control.

Novel therapeutic approaches, including GLP-1 receptor agonists and SGLT-2 inhibitors, are providing effective alternatives to traditional hypoglycemic drugs. These newer drugs often have additional benefits, such as weight loss and cardiovascular protection, making them attractive options.

Advances in diabetes management technologies, such as continuous glucose monitors (CGMs) and insulin pumps, offer alternative ways to manage blood sugar levels. These technologies are becoming increasingly sophisticated and user-friendly, providing real-time data and greater control over blood glucose levels.

By Drug Class Analysis

Sulphonylureas dominate the hypoglycemic drugs market with 42% market share

In 2023, Sulphonylureas held a dominant market position in the Sulphonylureas segment of the Hypoglycemic Drugs Market, capturing more than a 42% share. The Sulphonylureas segment represents a significant portion of the hypoglycemic drugs market, which is dedicated to managing diabetes mellitus by lowering blood sugar levels in patients.

Sulphonylureas, a class of oral hypoglycemic agents, have been widely prescribed for the management of type 2 diabetes mellitus due to their effectiveness in stimulating insulin secretion from pancreatic beta cells. This mechanism of action helps to regulate blood glucose levels and improve glycemic control in diabetic patients.

The dominance of Sulphonylureas in the segment can be attributed to their long-standing presence in the market, proven efficacy, and affordability compared to newer classes of hypoglycemic drugs. Despite the introduction of newer classes of antidiabetic medications, Sulphonylureas continue to be prescribed as first-line or adjunctive therapy for type 2 diabetes management, particularly in resource-constrained settings.

Sulphonylureas are available in various formulations and dosages, offering flexibility in treatment regimens and catering to the individual needs of patients. This versatility, coupled with their oral administration route, contributes to their widespread acceptance and usage among healthcare professionals and diabetic patients.

By Route of Administration Analysis

Oral administration leads with 39% market share in the hypoglycemic drugs market

In 2023, Oral administration held a dominant market position in the Oral segment of the Route of Administration segment of the Hypoglycemic Drugs Market, capturing more than a 39% share. The Route of Administration segment plays a crucial role in the hypoglycemic drugs market as it determines how medications are delivered to patients for managing diabetes mellitus and controlling blood sugar levels effectively.

Oral administration, being the most preferred route of drug delivery, encompasses a wide range of hypoglycemic medications that are taken orally, typically in the form of tablets, capsules, or liquids. This route offers convenience, ease of administration, and improved patient compliance compared to other routes such as injectable or nasal administration.

The dominance of Oral administration in this segment can be attributed to the widespread acceptance and familiarity of oral medications among healthcare providers and diabetic patients. Oral hypoglycemic drugs offer a non-invasive and patient-friendly approach to diabetes management, allowing individuals to self-administer their medication without the need for healthcare professionals or specialized equipment.

The availability of various classes of oral hypoglycemic drugs, including sulphonylureas, biguanides, alpha-glucosidase inhibitors, and thiazolidinediones, among others, provides healthcare providers with multiple treatment options to tailor therapy according to individual patient needs and preferences.

By Distribution Channel Analysis

Hospital pharmacies command a significant 45% market share, crucial for specialized diabetes care.

In 2023, Hospital Pharmacies held a dominant market position in the Hospital Pharmacies segment of the Distribution Channel segment of the Hypoglycemic Drugs Market, capturing more than a 45% share. The Distribution Channel segment is a crucial component of the hypoglycemic drugs market, as it determines the pathways through which medications are supplied to patients for managing diabetes mellitus and regulating blood sugar levels effectively.

Hospital Pharmacies, as integral parts of healthcare institutions, play a pivotal role in dispensing medications to patients receiving treatment for various medical conditions, including diabetes mellitus. These pharmacies are equipped to handle a wide range of medications, including hypoglycemic drugs, and are staffed by pharmacists who are trained to provide specialized pharmaceutical care to patients.

The dominance of Hospital Pharmacies in this segment can be attributed to several factors, including the high volume of diabetic patients treated in hospital settings, the availability of specialized medical professionals who oversee medication management, and the seamless integration of pharmacy services within the broader healthcare infrastructure.

Hospital pharmacies offer patients the convenience of accessing medications and ancillary services under one roof, streamlining the medication dispensing process and ensuring continuity of care. Patients receiving inpatient treatment for diabetes-related complications or undergoing surgical procedures often rely on hospital pharmacies to fulfill their medication needs and monitor their therapeutic regimens closely.

Key Market Segments

By Drug Class

- Sulphonylareas

- Biguanides

- Alpha-glucosidase inhibitors

- Thiazolidinediones

- Dipetidylpeptidase-4(DPP-4)

- Glucagoan

By Route of Administration

- Oral

- Injectable

- Nasal

By Distribution Channel

- Hospital Pharmacies

- Retail Pharamcies

- Online Pharamcies

Growth Opportunity

Increasing Use of Combination Therapies

The trend towards combination therapies presents a significant opportunity for the hypoglycemic drugs market in 2024. Combination therapies, which use multiple medications to manage blood glucose levels more effectively, are becoming increasingly popular among healthcare providers.

These therapies can enhance efficacy, reduce the risk of side effects, and improve patient adherence. For instance, combining metformin with SGLT-2 inhibitors or GLP-1 receptor agonists has shown superior outcomes in glycemic control and weight management. The rising adoption of these combination treatments is expected to drive substantial market growth.

Digital Health and Telemedicine

Digital health and telemedicine are transforming diabetes care, offering new growth avenues for the hypoglycemic drugs market. With the proliferation of telehealth services, patients can now receive continuous monitoring and personalized treatment plans from the comfort of their homes. This accessibility improves medication adherence and enables timely adjustments to treatment regimens.

The integration of digital health tools, such as mobile apps for blood glucose monitoring and virtual consultations, supports patient engagement and education, further boosting the demand for hypoglycemic drugs. The convenience and efficiency of these digital solutions are likely to attract a broader patient base, driving market expansion.

Growing Demand for Insulin Sensitizers

Insulin sensitizers, such as thiazolidinediones and metformin, are gaining traction due to their ability to improve insulin sensitivity and manage blood sugar levels effectively. The growing prevalence of insulin resistance, particularly in type 2 diabetes patients, underscores the increasing demand for these medications.

Insulin sensitizers not only help in controlling blood glucose but also offer cardiovascular benefits, making them a preferred choice for many healthcare providers. As the incidence of type 2 diabetes rises, the demand for insulin sensitizers is expected to surge, presenting a lucrative opportunity for market growth in 2024.

Latest Trends

Personalized Medicine and Precision Medicine

Personalized medicine and precision medicine are set to revolutionize the hypoglycemic drugs market in 2024. These approaches involve customizing medical treatment to the individual characteristics of each patient, such as their genetic makeup, lifestyle, and environment. In diabetes management, personalized medicine can lead to more effective and targeted therapies, reducing the risk of adverse effects and improving overall treatment outcomes.

Genetic profiling can help determine the most effective hypoglycemic drugs for specific patient subgroups, enhancing efficacy and minimizing side effects. The shift towards precision medicine is expected to drive innovation in drug development and foster the adoption of more sophisticated and effective diabetes treatments.

Increasing Use of Biosimilars

The rising use of biosimilars represents a significant trend in the hypoglycemic drugs market. Biosimilars are biologic medical products that are highly similar to already approved biologics, offering comparable safety and efficacy at a lower cost. As patents for several key biologic drugs expire, the market is witnessing an influx of biosimilar products.

These cost-effective alternatives are particularly appealing in managing diabetes, where long-term medication use is common. Biosimilars provide patients and healthcare systems with more affordable treatment options without compromising quality. The increasing acceptance and utilization of biosimilars are expected to drive market growth by making hypoglycemic drugs more accessible to a broader patient population.

Regional Analysis

North America emerges as the dominating region in the global hypoglycemic drugs market, holding a substantial share of 35%.

The hypoglycemic drugs market in North America is witnessing robust growth attributed to the high prevalence of diabetes and the presence of advanced healthcare infrastructure. According to recent statistics, North America holds a dominant share of 35% in the global hypoglycemic drugs market, indicating its significant contribution to the overall market. The region is characterized by a well-established pharmaceutical industry, favorable reimbursement policies, and a growing adoption of innovative diabetes management solutions.

Europe represents another significant market for hypoglycemic drugs, driven by the rising diabetic population and increasing awareness regarding the importance of glycemic control. The presence of key market players and ongoing clinical trials for the development of advanced treatment options contribute to the market expansion in this region.

The hypoglycemic drugs market in Asia Pacific is poised for substantial growth due to factors such as the rapid urbanization, changing lifestyle patterns, and increasing prevalence of diabetes. Asia Pacific presents lucrative opportunities for market players. The growing awareness regarding diabetes management and the introduction of cost-effective treatment options drive market growth in this region.

The hypoglycemic drugs market in the Middle East & Africa region is witnessing steady growth, fueled by the rising prevalence of diabetes and improving healthcare infrastructure. It is expected to contribute significantly to market growth due to increasing investments in healthcare and growing adoption of advanced treatment modalities.

Latin America represents a promising market for hypoglycemic drugs, supported by factors such as the increasing diabetic population, improving access to healthcare services, and rising awareness about diabetes management.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the dynamic landscape of the global Hypoglycemic Drugs Market in 2024, key players such as Eli Lilly & Company, Boehringer Ingelheim GmbH, Vistin Pharma AS, Johnson & Johnson, AstraZeneca plc, Merck & Co., Inc., Novartis AG, Novo Nordisk A/S, Teva Pharmaceutical Pvt Ltd., and Sun Pharmaceutical Industries Ltd. are shaping the industry through their innovative products and strategic initiatives.

Eli Lilly & Company, a pharmaceutical giant with a strong focus on diabetes care, is likely to maintain its position through continuous research and development efforts, aiming to introduce novel therapies and expand its product portfolio. Similarly, Boehringer Ingelheim GmbH, known for its collaborative approach and patient-centric innovations, might focus on developing effective treatments with improved safety profiles.

Vistin Pharma AS, a key player in the diabetes market, could leverage its expertise in specialized drug manufacturing to introduce cost-effective and high-quality medications, catering to a wide patient base. Johnson & Johnson, a diversified healthcare company, may emphasize integrated healthcare solutions and patient support programs to enhance treatment outcomes and patient adherence.

AstraZeneca plc, Merck & Co., Inc., Novartis AG, and Novo Nordisk A/S are likely to compete through a combination of innovative drug formulations, strategic alliances, and market expansion strategies. Meanwhile, Teva Pharmaceutical Pvt Ltd. and Sun Pharmaceutical Industries Ltd. may focus on generic versions of hypoglycemic drugs, offering affordable treatment options to a larger population.

Market Key Players

- Eli Lilly & Company

- Boehringer Ingelheim GmbH

- Vistin Pharma AS

- Jhonson & Johnson

- AstraZeneca plc

- Merck & Co., Inc.

- Novartis AG

- Novo Norsidk A/S

- Teva Pharmaceutical Pvt Ltd.

- Sun Pharamaceutical Industries Ltd

Recent Development

- In January 2024, AstraZeneca invests $26.5 million in China for a new production line of diabetes drug Xigduo XR, aiming to address the country's rising diabetes prevalence and strengthen its position in the market.

- In January 2024, Kumaravel Kaliaperumal et al. study the antidiabetic effects of Tribulus terrestris and Curcuma amada extracts on diabetic rats, showcasing potential for natural antidiabetic agents in Ayurvedic medicine.

Report Scope

Report Features Description Market Value (2023) USD 788.4 Mn Forecast Revenue (2033) USD 1876.2 Mn CAGR (2024-2033) 9.3% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Drug Class (Sulphonylareas, Biguanides, Alpha-glucosidase inhibitors, Thiazolidinediones, Dipetidylpeptidase-4(DPP-4), Glucagoan), By Route of Administration (Oral, Injectable, Nasal), By Distribution Channel (Hospital Pharmacies, Retail Pharamcies, Online Pharamcies) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Eli Lilly & Company, Boehringer Ingelheim GmbH, Vistin Pharma AS, Jhonson & Johnson, AstraZeneca plc, Merck & Co., Inc., Novartis AG, Novo Norsidk A/S, Teva Pharmaceutical Pvt Ltd., Sun Pharamaceutical Industries Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Eli Lilly & Company

- Boehringer Ingelheim GmbH

- Vistin Pharma AS

- Jhonson & Johnson

- AstraZeneca plc

- Merck & Co., Inc.

- Novartis AG

- Novo Norsidk A/S

- Teva Pharmaceutical Pvt Ltd.

- Sun Pharamaceutical Industries Ltd

Our Clients

View Our Licence Options