Geotextile Market By Material (Natural, Jute, Others, Synthetic, Polypropylene, Polyester, Polyethylene), By Product (Woven, Non-Woven, Knitted), By Application (Agriculture, Erosion Control, Reinforcement, Lining System, Asphalt Overlays, Silt Fences, Drainage, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

47802

-

June 2024

-

136

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

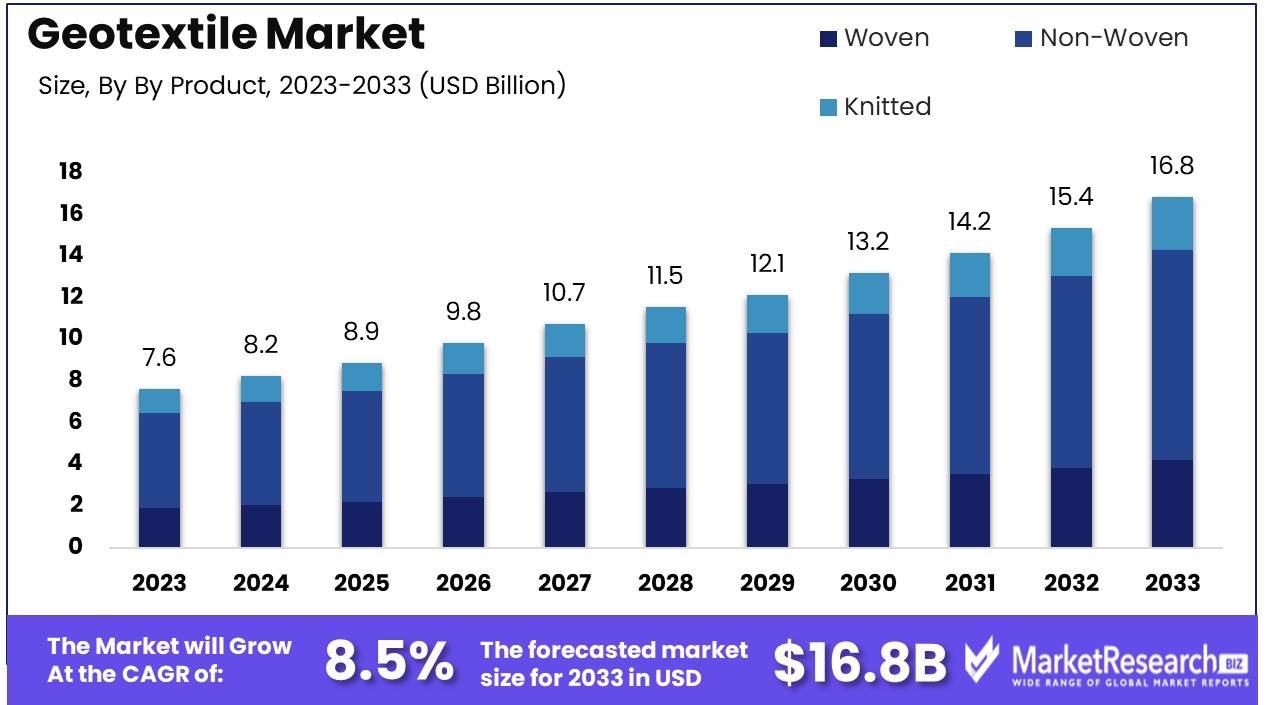

The Global Geotextile Market was valued at USD 7.6 Bn in 2023. It is expected to reach USD 16.8 Bn by 2033, with a CAGR of 8.5% during the forecast period from 2024 to 2033.

The Geotextile Market encompasses the global industry involved in the production, distribution, and application of geotextiles. Geotextiles are permeable fabrics used in construction and environmental engineering projects to enhance soil stability, provide erosion control, and improve drainage. These materials are essential in infrastructure development, including roads, railways, and embankments, as well as in landfills and agricultural applications. The market is driven by increasing infrastructure investments, growing environmental concerns, and advancements in geotextile technology.

The Geotextile Market is poised for significant growth, driven by its critical role in modern infrastructure and environmental projects. Geotextiles, including woven, non-woven, and knitted types, are indispensable in applications such as soil stabilization, erosion control, and drainage enhancement. Their use in large-scale construction projects, including Caselon playing fields and AstroTurf, highlights their versatility and essential contribution to supporting synthetic grass surfaces with durable polypropylene materials and latex backing, achieving pile heights of 2.0 to 2.5 cm.

Advancements in material science, particularly the integration of nanotechnology, are expected to further elevate the performance of geotextiles. Nano-sized fibers with specific surface areas up to 1000 m²/g offer superior strength, durability, and functionality, positioning geotextiles as high-performance solutions in demanding environments. The adoption of such innovative technologies is anticipated to drive market expansion, offering enhanced benefits such as increased longevity and efficiency in geotechnical applications.

The market's growth trajectory is underpinned by several factors. Increasing infrastructure investments across emerging economies, heightened environmental awareness, and the push for sustainable construction practices are key drivers. Regulatory frameworks promoting the use of eco-friendly materials in construction projects provide a conducive environment for market growth.

Key Takeaways

- Market Value: The Global Geotextile Market was valued at USD 7.6 Bn in 2023. It is expected to reach USD 16.8 Bn by 2033, with a CAGR of 8.5% during the forecast period from 2024 to 2033.

- By Material: Synthetic materials dominate the Geotextile Market with a 75% share, primarily driven by the widespread use of polypropylene, polyester, and polyethylene in various applications.

- By Product: Non-Woven geotextiles lead the market with a 60% share, valued for their high strength, filtration capabilities, and ease of installation compared to woven and knitted types.

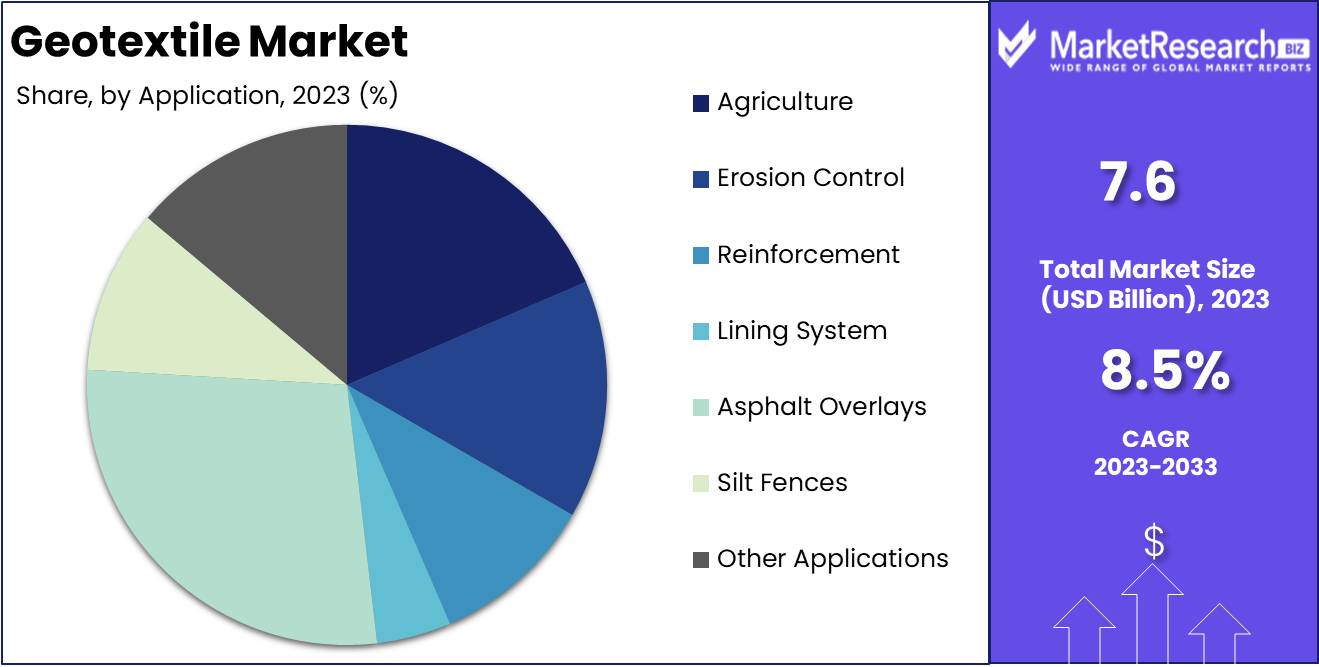

- By Application: Asphalt Overlays is the dominating application segment with a 30% share, highlighting the critical role of geotextiles in stabilizing soil and preventing erosion in construction and environmental projects.

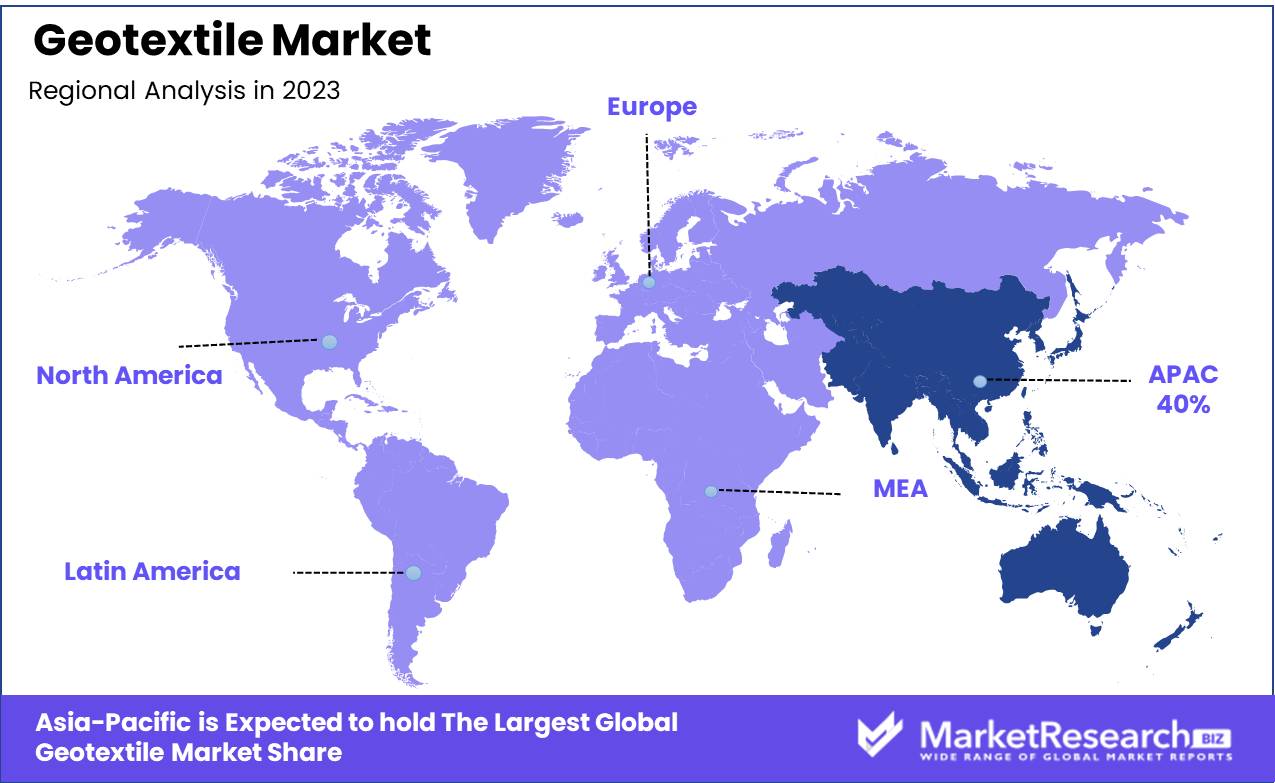

- Regional Dominance: The Asia-Pacific region leads the Geotextile market with a significant share of 40%.

- Growth Opportunity: The geotextile market is set for expansion with growing infrastructure development and environmental awareness driving the adoption of sustainable construction materials.

Driving factors

Increasing Usage in Construction

The geotextile market is significantly driven by the increasing usage in construction activities. As urbanization continues to expand globally, the demand for sustainable and durable construction materials rises in tandem. Geotextiles, known for their reinforcement, filtration, and separation properties, have become integral in civil engineering projects such as roads, highways, and railways.

They enhance the longevity and stability of these structures by providing effective soil stabilization and erosion control. In the construction sector is expected to account for a substantial share of the geotextile market, with a projected growth rate of 8.5% annually over the next decade. This growth is fueled by large-scale infrastructure projects in emerging economies and the ongoing development of smart cities worldwide.

Framework for Environmental Protection

The implementation of stringent environmental protection frameworks is a pivotal factor propelling the geotextile market. Governments and environmental bodies are increasingly advocating for sustainable construction practices to mitigate the impact of urbanization on natural ecosystems. Geotextiles play a crucial role in environmental protection by preventing soil erosion, managing water drainage, and promoting vegetation growth.

Their application in landfills, water reservoirs, and coastal engineering projects aids in preserving natural habitats and reducing ecological footprints. The market is witnessing a surge in demand as industries comply with environmental regulations aimed at promoting green infrastructure.

Growing Demand in Mining Activities

The geotextile market is also experiencing growth due to the rising demand in mining activities. Geotextiles are employed in mining operations for tasks such as heap leach pads, tailings containment, and access roads, where they offer superior filtration, separation, and reinforcement capabilities.

The mining industry’s focus on operational efficiency and environmental management has led to a greater reliance on geotextiles to ensure the stability of mining structures and to mitigate environmental impacts. The increasing exploration activities and expansion of mining projects in regions like Asia-Pacific and Latin America further bolster this demand.

Restraining Factors

Fluctuating Raw Material Prices

The geotextile market is vulnerable to fluctuations in raw material prices, particularly those of synthetic fibers such as polypropylene and polyester. These materials constitute a significant portion of the production cost, and their price volatility can substantially affect the overall cost structure of geotextile products. An increase in the price of crude oil, a key raw material for synthetic fibers, can lead to higher production costs, which in turn may result in increased market prices for geotextiles.

Conversely, a decrease in raw material prices can make geotextiles more affordable, potentially boosting demand. Manufacturers must develop effective pricing strategies and explore alternative materials to mitigate the impact of raw material price fluctuations on their profit margins.

Supply Chain Disruptions

Supply chain disruptions pose a significant challenge to the geotextile market, impacting the availability and timely delivery of products. Factors such as geopolitical tensions, natural disasters, and the ongoing effects of the COVID-19 pandemic have led to disruptions in the global supply chain. These disruptions can cause delays in raw material procurement, production bottlenecks, and increased logistics costs.

The pandemic-induced lockdowns and restrictions on transportation have resulted in shortages of critical raw materials and delayed shipments, affecting production schedules and delivery timelines. The market is estimated to have experienced a supply chain disruption impact of up to 20% in terms of delayed projects and increased operational costs during peak disruption periods.'

By Material Analysis

Synthetic materials dominated the Geotextile Market, capturing over 75% share.

In 2023, Synthetic materials held a dominant market position in the By Material segment of the Geotextile Market, capturing more than a 75% share. This segment's dominance underscores the widespread adoption of synthetic geotextiles due to their superior durability, versatility, and performance characteristics across various civil engineering and environmental applications.

Polypropylene emerged as a leading material within the synthetic category, offering excellent resistance to chemicals, UV degradation, and biological factors. These properties make polypropylene geotextiles ideal for applications such as erosion control, soil stabilization, and drainage systems in infrastructure projects.

Polyester, another prominent synthetic material in the geotextile market, is valued for its high tensile strength, dimensional stability, and resistance to creep under load. These attributes make polyester geotextiles suitable for demanding applications such as road construction, railway stabilization, and coastal protection.

Polyethylene-based geotextiles, known for their flexibility, puncture resistance, and ability to withstand harsh environmental conditions, also contributed significantly to the synthetic materials segment. These geotextiles find applications in landfill engineering, geomembrane protection, and hydraulic engineering projects.

In contrast, Natural materials, primarily represented by Jute, accounted for a smaller share of the geotextile market in 2023. Jute geotextiles are appreciated for their biodegradability and eco-friendly properties, making them suitable for temporary erosion control and landscaping applications. However, their usage is limited compared to synthetic alternatives due to lower durability and performance in challenging environmental conditions.

By Product Analysis

Non-Woven geotextiles led the Geotextile Market with over 60% share.

In 2023, Non-Woven geotextiles held a dominant market position in the By Product segment of the Geotextile Market, capturing more than a 60% share. This segment's leadership underscores the widespread preference for non-woven geotextiles due to their versatility, durability, and performance across a wide range of civil engineering and environmental applications.

Following Non-Woven geotextiles, Woven geotextiles represented a significant portion of the market. Woven geotextiles are produced by weaving together individual yarns of synthetic materials like polypropylene or polyester. They are known for their high strength and modulus, making them suitable for applications requiring soil reinforcement, load distribution, and separation.

Knitted geotextiles, while holding a smaller share of the market compared to non-woven and woven types, offer unique characteristics such as high elongation and conformability. Knitted geotextiles are used in applications where flexibility and conformability to irregular surfaces are crucial, such as in landscaping, slope stabilization, and soft soil reinforcement projects.

By Application Analysis

Asphalt Overlays led in market share of 30% due to their critical role in road maintenance and longevity, applications.

In 2023, Asphalt Overlays held a dominant market position in the By Application segment of the Geotextile Market, capturing more than a 30% share. This segment's prominence underscores the critical role of geotextiles in enhancing the performance and longevity of asphalt pavements through reinforcement and separation functions.

Following Asphalt Overlays, Reinforcement applications represented a significant portion of the market. Geotextiles used for reinforcement purposes enhance the strength and stability of soil structures in various civil engineering projects.

Erosion Control also held a substantial share in the Geotextile Market in 2023. Geotextiles used for erosion control prevent soil erosion and sediment runoff in environmentally sensitive areas, such as riverbanks, coastlines, and construction sites.

Drainage applications, facilitated by geotextiles with excellent filtration and drainage properties, were another significant segment in the market. Geotextile drainage systems enhance water management in roadways, sports fields, and agricultural lands, improving soil permeability, reducing waterlogging, and enhancing crop yields.

Silt Fences, employed primarily in construction and land development projects, use geotextiles to control sediment runoff and protect water quality in adjacent water bodies. These barriers prevent sediment-laden runoff from polluting streams, rivers, and lakes, thereby complying with environmental regulations and minimizing ecological impact.

Key Market Segments

By Material

- Natural

-

- Jute

- Others

- Synthetic

- Polypropylene

- Polyester

- Polyethylene

By Product

- Woven

- Non-Woven

- Knitted

By Application

- Agriculture

- Erosion Control

- Reinforcement

- Lining System

- Asphalt Overlays

- Silt Fences

- Drainage

- Others

Growth Opportunity

Expanding Road Construction Projects

The increasing investment in road construction projects worldwide presents a substantial opportunity for the geotextile market. Geotextiles are essential in enhancing the durability and stability of roadways by providing effective soil stabilization and drainage solutions. With numerous governments prioritizing infrastructure development, the demand for geotextiles in road construction is expected to rise.

In 2024, road construction projects are anticipated to contribute significantly to market growth, with a projected increase in demand. This surge is driven by ongoing urbanization and the need for robust transportation networks.

Erosion Control Initiatives

Erosion control remains a critical application area for geotextiles, particularly in regions prone to soil erosion and landslides. The implementation of erosion control measures is vital for protecting natural landscapes and infrastructure. Geotextiles are extensively used in slope stabilization, riverbank protection, and coastal engineering projects. Market data indicates that erosion control applications are expected to grow in 2024, driven by heightened awareness of environmental conservation and the adoption of sustainable land management practices.

Water Conservation Projects

Water conservation is another key area where geotextiles play a crucial role. Geotextiles are used in the construction of water reservoirs, dams, and irrigation systems to enhance water retention and prevent soil erosion. With increasing concerns about water scarcity and the need for efficient water management, the demand for geotextiles in water conservation projects is set to rise.

Latest Trends

Adoption of Sustainable Materials

Sustainability is at the forefront of the geotextile market trends in 2024. Increasing environmental awareness and stringent regulations are pushing manufacturers to explore and adopt sustainable materials. Geotextiles made from recycled fibers and biodegradable materials are gaining traction as they align with global sustainability goals.

The shift towards eco-friendly products is driven by the need to reduce the environmental footprint of construction projects and enhance the lifecycle performance of geotextiles. This trend is supported by governmental incentives and the rising preference for green construction practices among industry stakeholders.

Development of High-Performance Materials

The quest for advanced functionality is spurring the development of high-performance geotextiles. Innovations in material science are leading to the creation of geotextiles with enhanced properties such as higher tensile strength, improved durability, and better chemical resistance.

These high-performance materials are particularly suited for challenging applications in harsh environments, including heavy-duty road construction, mining, and coastal protection projects. The market for high-performance geotextiles is expected to grow in 2024, driven by the increasing complexity of engineering projects and the demand for materials that offer superior performance and longevity.

Regional Analysis

Asia-Pacific leads the global geotextile market with a dominant share of 40%

Asia-Pacific dominates the geotextile market with a significant share of 40%. This region is experiencing rapid infrastructure development, particularly in emerging economies like China, India, and Southeast Asian countries. The demand for geotextiles in Asia-Pacific is driven by large-scale construction projects, including highways, railways, and environmental protection initiatives.

North America represents another substantial market segment for geotextiles, supported by stringent environmental regulations and a strong focus on sustainable construction practices. The region's adoption of geotextiles is driven by infrastructure renewal projects, erosion control measures, and soil stabilization applications.

Europe is also a significant player in the global geotextile market, characterized by a mature construction sector and growing emphasis on environmental sustainability. Countries like Germany, France, and the UK are leading adopters of geotextile solutions for applications ranging from drainage systems to landfill liners.

Middle East & Africa and Latin America are emerging markets in the geotextile industry, driven by urbanization, infrastructure development, and environmental conservation efforts. In these regions, geotextiles are increasingly utilized in road construction, mining operations, and water management projects to improve soil stability and reduce environmental impact.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global geotextile market is marked by dynamic growth and technological advancements, with key players, TYPAR Geosynthetics, known for its innovative approach and diverse product range, continues to lead with solutions that enhance soil stabilization, erosion control, and drainage management. GSE Environmental specializes in advanced geosynthetic solutions for environmental containment and infrastructure applications, leveraging its global footprint and extensive research capabilities.

SKAPS Industries stands out for its comprehensive geosynthetic offerings, catering to diverse sectors including construction, transportation, and agriculture. Fibertex Nonwovens A/S focuses on high-performance nonwoven geotextiles, meeting stringent quality standards and sustainability criteria.

Maccaferri remains a key player with its integrated solutions in geotechnical engineering, offering geotextiles that reinforce soil structures and provide erosion protection. Global Synthetics and TenCate Geosynthetics Asia Sdn Bhd. contribute significantly with their advanced materials and engineering expertise, supporting infrastructure projects worldwide.

Belton Industries and NAUE GMBH & CO. KG are recognized for their innovations in geosynthetic products, addressing the challenges of modern construction and environmental management. HUESKER Synthetic GmbH and Gayatri Polymers & Geo-Synthetics provide tailored solutions for soil reinforcement and hydraulic engineering, emphasizing sustainability and durability.

Market Key Players

- TYPAR Geosynthetics

- GSE Environmental

- SKAPS Industries

- Fibertex Nonwovens A/S

- Maccaferri

- Global Synthetics

- TenCate Geosynthetics Asia Sdn Bhd.

- Belton Industries

- NAUE GMBH & CO. KG

- HUESKER Synthetic GmbH

- Gayatri Polymers & Geo – Synthetics

- Suntech Geotextile Pvt. Ltd.

- Thrace Group

- Terram Geosynthetics Pvt. Ltd.

- TENAX

- AGRU AMERICA, INC

Recent Development

- In April 2024, Freudenberg Performance Materials expands Enka Solutions with new geosynthetics line in Changzhou, China, enhancing production for APAC markets.

- In March 2024, Van Oord and Van Aalsburg collaborate on circular fascine mattresses using jute cloth, eliminating microplastics.

Report Scope

Report Features Description Market Value (2023) USD 7.6 Bn Forecast Revenue (2033) USD 16.8 Bn CAGR (2024-2033) 8.5% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Natural, Jute, Others, Synthetic, Polypropylene, Polyester, Polyethylene), By Product (Woven, Non-Woven, Knitted), By Application (Agriculture, Erosion Control, Reinforcement, Lining System, Asphalt Overlays, Silt Fences, Drainage, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape TYPAR Geosynthetics, GSE Environmental, SKAPS Industries, Fibertex Nonwovens A/S, Maccaferri, Global Synthetics, TenCate Geosynthetics Asia Sdn Bhd., Belton Industries, NAUE GMBH & CO. KG, HUESKER Synthetic GmbH, Gayatri Polymers & Geo – Synthetics, Suntech Geotextile Pvt. Ltd., Thrace Group, Terram Geosynthetics Pvt. Ltd., TENAX, AGRU AMERICA, INC, Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- TYPAR Geosynthetics

- GSE Environmental

- SKAPS Industries

- Fibertex Nonwovens A/S

- Maccaferri

- Global Synthetics

- TenCate Geosynthetics Asia Sdn Bhd.

- Belton Industries

- NAUE GMBH & CO. KG

- HUESKER Synthetic GmbH

- Gayatri Polymers & Geo – Synthetics

- Suntech Geotextile Pvt. Ltd.

- Thrace Group

- Terram Geosynthetics Pvt. Ltd.

- TENAX

- AGRU AMERICA, INC

Our Clients

View Our Licence Options