Generative AI in Media and Entertainment Market Report By Component (Software, Services [Professional Services, Managed Services]), By Technology (Natural Language Processing (NLP), Machine Learning, Deep Learning, Computer Vision, Others), By Application (Content Creation, Personalized Recommendation, Virtual Assistants, Data Analytics, Interactive Storytelling, Others), By End-User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

38069

-

August 2024

-

324

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

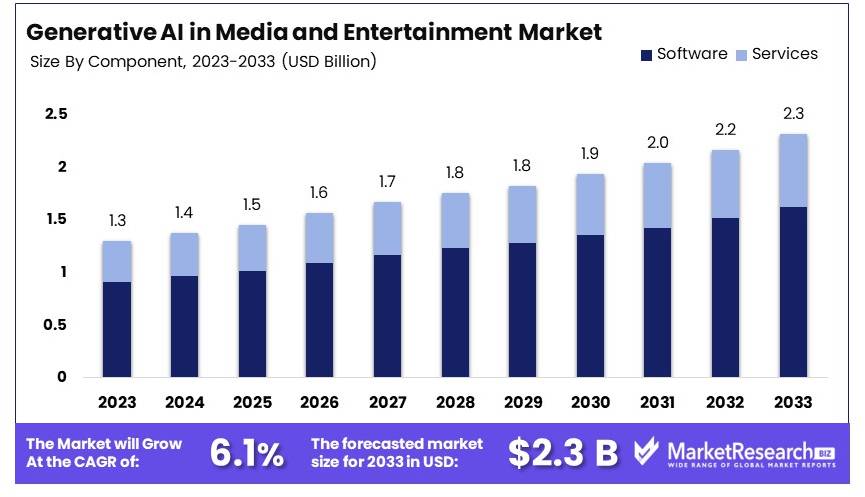

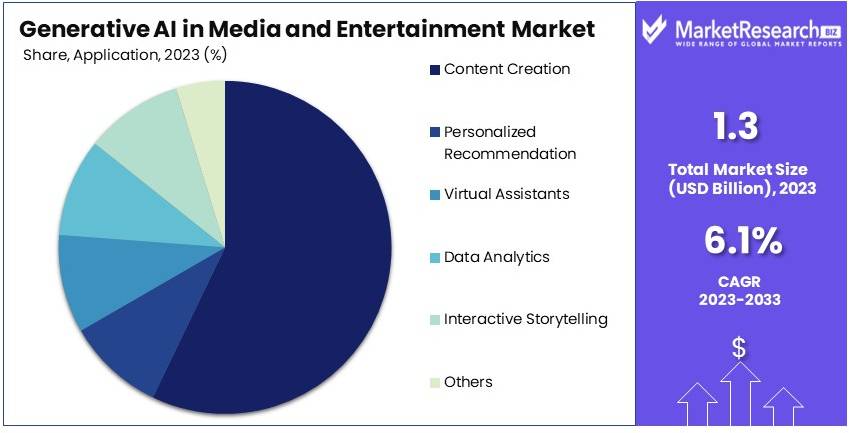

The Global Generative AI in Media and Entertainment Market size is expected to be worth around USD 2.3 Billion by 2033, from USD 1.3 Billion in 2023, growing at a CAGR of 6.1% during the forecast period from 2024 to 2033.

The generative AI in media and entertainment market focuses on the use of artificial intelligence to create content, enhance production processes, and personalize user experiences. This market is driven by advancements in AI technology and the increasing demand for innovative content solutions.

Key players include AI developers, media companies, and entertainment platforms. The market is characterized by rapid technological advancements and high investment in research and development. Major trends include the use of AI for content creation, virtual reality, and audience engagement. The market is competitive, with significant opportunities for growth and innovation.

The generative AI (GenAI) market in media and entertainment is experiencing rapid growth. This is driven by advancements in AI technology and increasing adoption of AI tools for content creation. GenAI can quickly generate scripts, stories, and realistic images from simple text prompts. Tools like ChatGPT and DALL-E are at the forefront of this revolution, boasting over 100 million users. These platforms are being used to create a wide range of content, from written narratives to complex visual designs.

This technology is transforming the way content is produced, enabling faster and more efficient creative processes. Media companies can now generate high-quality content with reduced human intervention, leading to cost savings and faster turnaround times. This is particularly beneficial for industries such as film, television, advertising, and gaming, where content demand is high and production timelines are tight.

Additionally, GenAI enhances personalization in media and entertainment. AI-driven content can be tailored to individual preferences, creating a more engaging and immersive experience for audiences. This capability is becoming increasingly important as consumers seek more personalized and interactive content.

The growing investment in AI research and development further propels the market. Major tech companies are investing heavily in AI capabilities, driving innovation and expanding the applications of GenAI in media and entertainment.

The generative AI market in media and entertainment is set for continued growth. The technology’s ability to streamline content creation and enhance personalization is driving its adoption. With ongoing advancements and increasing user engagement, GenAI is poised to play a crucial role in the future of media and entertainment.

Key Takeaways

- Market Value: The Generative AI in Media and Entertainment Market was valued at USD 1.3 billion in 2023 and is expected to reach USD 2.3 billion by 2033, with a CAGR of 6.1%.

- Component Analysis: Software holds a significant 70%; its critical role in enabling AI functionalities underpins this dominance.

- Technology Analysis: Natural Language Processing (NLP) leads with 55%; its importance in creating interactive and engaging content is paramount.

- Application Analysis: Content Creation accounts for 60%; the demand for automated and personalized content drives growth in this area.

- End-User Analysis: The Film Industry has a 40% share; AI's ability to enhance storytelling and production processes is key.

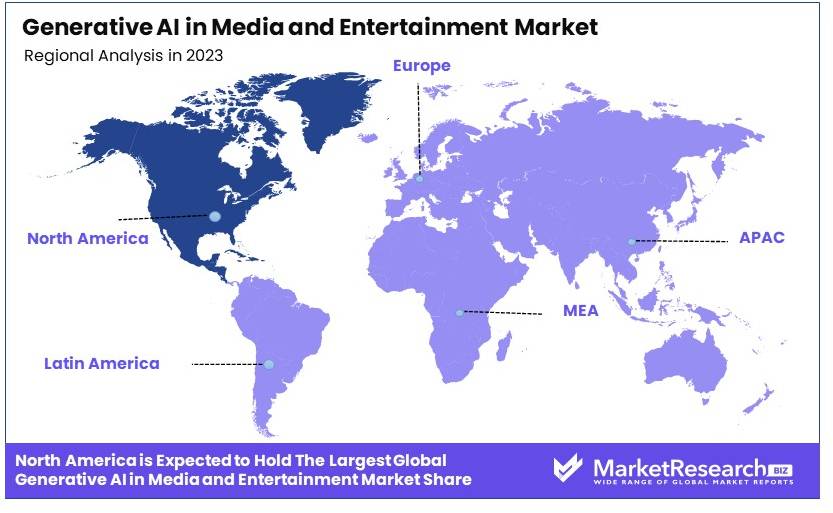

- Dominant Region: North America at 38.2%; technological advancements and strong media presence boost regional growth.

Driving Factors

Content Creation Efficiency Drives Market Growth

Generative AI is revolutionizing content creation in the media and entertainment industry by significantly reducing production time and costs. This technology can generate scripts, storyboards, and even visual elements, allowing creators to produce more content in less time.

For example, Netflix has been experimenting with AI-generated artwork for show thumbnails, optimizing viewer engagement. This efficiency boost enables media companies to meet the growing demand for content across various platforms, driving market growth as more organizations adopt these tools to stay competitive.

Personalization and User Experience Enhancement Drive Market Growth

Generative AI enables unprecedented levels of content personalization, tailoring media experiences to individual user preferences. This technology analyzes user data to create customized content recommendations, generate personalized narratives, or even adapt visual and audio elements in real-time.

Spotify's AI DJ feature, which creates personalized playlists and provides commentary in a voice modeled after a real DJ, exemplifies this trend. As consumers increasingly expect personalized experiences, the demand for generative AI solutions in media and entertainment will continue to grow. The synergy between AI-driven personalization and consumer expectations is a key growth driver.

Cost Reduction in Production and Post-Production Drives Market Growth

Generative AI is significantly reducing costs associated with various stages of media production. In film and television, AI can generate realistic visual effects, background scenery, and even entire characters, reducing the need for expensive on-location shoots or complex CGI work.

For instance, The Mandalorian utilized AI-powered technology to create virtual backgrounds, significantly cutting production costs. This cost-efficiency is particularly attractive to smaller production companies and independent creators, broadening the market for generative AI tools. The economic benefits of AI in production make it an essential tool for industry players, facilitating market growth.

Restraining Factors

Ethical and Copyright Concerns Restrain Market Growth

The use of generative AI in media and entertainment raises significant ethical and copyright issues, restraining market growth. Concerns about AI models being trained on copyrighted material without proper attribution or compensation can lead to legal challenges.

For example, the lawsuit against Stability AI and Midjourney for allegedly using copyrighted images to train their AI models highlights these issues. These ethical and legal uncertainties make companies hesitant to fully adopt generative AI technologies until clearer guidelines and regulations are in place.

Quality and Consistency Challenges Restrain Market Growth

While generative AI has advanced significantly, challenges remain in consistently producing high-quality content that meets professional standards in media and entertainment. AI-generated content can sometimes be unpredictable, contain errors, or lack the nuanced understanding of context and cultural sensitivities that human creators provide.

For instance, Microsoft's AI chatbot Tay quickly learned to produce offensive content, demonstrating the potential pitfalls of AI-generated content. These quality concerns may limit the adoption of generative AI in high-stakes or premium content areas, restricting market growth.

Component Analysis

Software dominates the Generative AI component market with 70% due to its foundational role in enabling AI functionalities across media and entertainment platforms.

Generative AI in the media and entertainment sector is segmented into software and services, which include professional and managed services. Software holds a significant lead as the dominant sub-segment, primarily because it is the core enabler of AI capabilities. This includes everything from content creation tools and personalized recommendation engines to data analytics and virtual assistant applications. The robust demand for AI software is driven by its ability to dramatically enhance creativity, personalize content delivery, and streamline production processes in media and entertainment.

Services are also vital, particularly professional services, which support the implementation, customization, and maintenance of AI solutions. Managed services are growing as companies seek to outsource the operational aspects of their AI systems to focus on creative and strategic activities.

The software's dominance is reinforced by continuous advancements in AI technology, which broaden its application range and deepen its impact across various media formats, driving overall market growth within this segment.

Technology Analysis

Natural Language Processing (NLP) leads the Generative AI technology segment with 55% due to its critical role in transforming interaction and content customization.

In the realm of Generative AI for media and entertainment, technology can be classified into natural language processing (NLP), machine learning, deep learning, computer vision, and others. NLP stands out as the predominant technology due to its ability to understand, interpret, and generate human language in a way that is meaningful to users. This capability is especially valuable in applications such as generative ai in content creation, personalized recommendations, and interactive storytelling.

Machine learning and deep learning are integral for analyzing large datasets and improving over time, thereby enhancing the AI's effectiveness and accuracy. Computer vision technology is vital in areas such as video generation and augmented reality, providing machines with the ability to understand and interpret visual data.

The growth in other AI technologies also contributes significantly to the expansion of generative AI applications, supporting a wide range of creative and analytical functions in the media and entertainment industry.

Application Analysis

Content Creation is the largest application area for Generative AI in media and entertainment, occupying 60%

Generative AI applications in media and entertainment are diversified across content creation, personalized recommendation, virtual assistants, data analytics, and interactive storytelling. Content creation, however, is the dominant sub-segment. This includes text generation, image generation, video generation, and music composition. AI's ability to quickly produce diverse and creative content supports not only scale but also customization, meeting the fast-paced demand of the media landscape.

Personalized recommendation systems are essential for platforms like streaming services, where they enhance viewer engagement by suggesting content aligned with individual preferences. Virtual assistants and data analytics are increasingly used to improve customer service and decision-making processes, while interactive storytelling is transforming how stories are told and experienced.

The non-dominant applications are also vital, supporting the overall growth and innovation in the sector by meeting specific needs that enhance user engagement and business efficiency.

End-User Analysis

The Film Industry is the top end-user of Generative AI in the media sector, accounting for 40% of the market, driven by its need for high-quality, innovative content production.

Generative AI's end-user market in media and entertainment includes the film industry, music industry, gaming, publishing, advertising, broadcasting, and others. The film industry leads this segment, leveraging AI in various stages of production from scripting and animation to post-production effects. This not only enhances the creative process but also reduces costs and production times.

The gaming industry is also a significant consumer, using AI to create realistic and interactive environments. In publishing, AI assists in content generation and layout design, while in advertising, it is used to create targeted and personalized campaigns. Broadcasting benefits from AI in scheduling, content management, and audience analytics.

Each of these industries contributes to the growth of generative AI in media and entertainment by harnessing these technologies to meet specific needs, ultimately enhancing product offerings and consumer experiences.

Key Market Segments

By Component

- Software

- Services

- Professional Services

- Managed Services

By Technology

- Natural Language Processing (NLP)

- Machine Learning

- Deep Learning

- Computer Vision

- Others

By Application

- Content Creation

- Text Generation

- Image Generation

- Video Generation

- Music Composition

- Personalized Recommendation

- Virtual Assistants

- Data Analytics

- Interactive Storytelling

- Others

By End-User

- Film Industry

- Music Industry

- Gaming

- Publishing

- Advertising

- Broadcasting

- Others

Growth Opportunities

Interactive and Immersive Experiences Offer Growth Opportunity

Generative AI presents a significant opportunity for creating more interactive and immersive media experiences. By dynamically generating content based on user interactions, AI can enable personalized storytelling in video games, interactive movies, and virtual reality experiences.

For example, AI Dungeon uses GPT-3 to create unique, player-driven narrative experiences. As demand for immersive content grows, particularly with the advancement of VR and AR technologies, generative AI will play a crucial role in creating scalable, personalized experiences. This trend towards interactive content offers substantial growth potential as consumers increasingly seek engaging and customizable entertainment options.

AI-Assisted Localization and Globalization Offer Growth Opportunity

Generative AI offers tremendous potential in automating and improving content localization for global audiences. This technology can assist in translating and adapting content for different cultures, including generating culturally appropriate visuals and modifying storylines to resonate with local audiences.

Netflix's use of AI for dubbing shows into multiple languages demonstrates this opportunity. As media companies seek to expand their global reach, AI-powered localization tools will become increasingly valuable. These tools enhance efficiency and accuracy in localization efforts, allowing for a broader and more effective reach in diverse markets.

Trending Factors

AI-Human Collaboration in Creative Processes Are Trending Factors

A growing trend in the industry is the collaborative use of AI alongside human creators. Rather than replacing human creativity, AI is increasingly being used as a tool to augment and enhance the creative process.

This trend is evident in music production, where artists use generative ai in music to generate melodies or chord progressions as starting points for composition. For example, AIVA (Artificial Intelligence Virtual Artist) has been used by composers to create original music for films and advertisements, showcasing how AI can be a powerful collaborative tool in the creative industry. This synergy between AI and human creativity is driving innovation and expanding possibilities in media and entertainment.

Synthetic Media and Deep Fakes for Entertainment Are Trending Factors

The use of synthetic media, including deep fakes, is a controversial but rapidly growing trend in entertainment. While there are concerns about misuse, the technology also offers creative possibilities for film and television production.

For instance, the ability to digitally recreate deceased actors or age/de-age living actors, as seen in films like "Star Wars: Rogue One" with the digital recreation of Peter Cushing, is becoming more sophisticated and widespread. This trend is likely to continue, raising both exciting possibilities and ethical questions for the industry. The advancements in synthetic media are opening new frontiers in storytelling and production, driving interest and investment in this technology.

Regional Analysis

North America Dominates with 38.2% Market Share in Generative AI in Media and Entertainment

North America's significant 38.2% market share in Generative AI for media and entertainment is primarily driven by its advanced technological infrastructure and heavy investment in AI research and development. The presence of major technology giants and startups focused on AI innovations contributes greatly to this dominance. Furthermore, the region's strong intellectual property laws protect and encourage the development of new AI technologies.

The regional dynamics are characterized by high adoption rates of AI technologies among media and entertainment industries, which are seeking to enhance content personalization and audience engagement. North America also benefits from a skilled workforce specializing in AI and machine learning, fostering rapid advancements and deployment in practical applications. The openness to adopting new technologies among consumers and businesses alike boosts the market growth.

The influence of North America in the generative AI sector of media and entertainment is expected to grow, driven by ongoing technological advancements and increasing investments. The market's expansion will likely be supported by further integration of AI in emerging entertainment platforms and content creation tools, maintaining North America's leading position.

Regional Market Shares:

- Europe: Europe holds approximately 24% of the market. The growth is supported by robust data protection regulations that ensure AI is developed and applied in a secure and ethical manner.

- Asia Pacific: This region accounts for about 28% of the market share. Rapid technological adoption and significant investments in AI from both private and public sectors in countries like China, Japan, and South Korea drive this substantial market presence.

- Middle East & Africa: With a smaller market share of around 5%, growth in this region is slowly increasing as more countries begin to recognize the potential of AI in transforming media and entertainment industries.

- Latin America: Capturing about 5% of the market, Latin America is on a growth trajectory, facilitated by improving technological infrastructure and increasing local startups focusing on AI.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The generative AI in media and entertainment market features key players with significant influence and strategic positioning. Google LLC (DeepMind) and OpenAI lead with their cutting-edge AI research and innovative applications. IBM Corporation and Adobe Inc. leverage their technological expertise to enhance content creation and media production.

Microsoft Corporation and NVIDIA Corporation utilize their advanced computing capabilities to develop powerful AI tools for the industry. Amazon Web Services, Inc. and Meta Platforms, Inc. provide scalable AI solutions and cloud services to support media enterprises.

Sony Corporation and Baidu, Inc. focus on integrating AI into entertainment platforms and consumer products. Tencent Holdings Ltd. and Alibaba Group leverage their vast digital ecosystems to drive AI adoption in media and entertainment.

SAP SE and Salesforce, Inc. emphasize AI-driven analytics and personalization to enhance user experiences. Oracle Corporation utilizes its cloud infrastructure to support AI innovations in media.

These companies collectively drive the market through continuous innovation, strategic partnerships, and advanced AI applications, transforming the media and entertainment landscape.

Market Key Players

- Google LLC (DeepMind)

- Autodesk, Inc.

- OpenAI

- IBM Corporation

- Adobe Inc.

- Microsoft Corporation

- NVIDIA Corporation

- Amazon Web Services, Inc.

- Meta Platforms, Inc.

- Sony Corporation

- Baidu, Inc.

- Tencent Holdings Ltd.

- Alibaba Group

- SAP SE

- Salesforce, Inc.

- Oracle Corporation

Recent Developments

- July 2024: Adobe has launched a new suite of generative AI tools aimed at content creators, further solidifying its position in the market. The company's focus on AI-driven innovation has contributed to a substantial increase in revenue, with projections indicating continued growth as adoption of these tools expands globally.

- July 2024: Unity Software has reported significant revenue growth following the integration of generative AI in its game development platform. This move has enhanced the company's ability to provide developers with advanced tools for creating immersive gaming experiences, driving its market valuation upward.

Report Scope

Report Features Description Market Value (2023) USD 1.3 Billion Forecast Revenue (2033) USD 2.3 Billion CAGR (2024-2033) 6.1% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Software, Services [Professional Services, Managed Services]), By Technology (Natural Language Processing (NLP), Machine Learning, Deep Learning, Computer Vision, Others), By Application (Content Creation [Text Generation, Image Generation, Video Generation, Music Composition], Personalized Recommendation, Virtual Assistants, Data Analytics, Interactive Storytelling, Others), By End-User (Film Industry, Music Industry, Gaming, Publishing, Advertising, Broadcasting, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Google LLC (DeepMind), OpenAI, IBM Corporation, Adobe Inc., Microsoft Corporation, NVIDIA Corporation, Amazon Web Services, Inc., Meta Platforms, Inc., Sony Corporation, Baidu, Inc., Tencent Holdings Ltd., Alibaba Group, SAP SE, Salesforce, Inc., Oracle Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Google LLC (DeepMind)

- Autodesk, Inc.

- OpenAI

- IBM Corporation

- Adobe Inc.

- Microsoft Corporation

- NVIDIA Corporation

- Amazon Web Services, Inc.

- Meta Platforms, Inc.

- Sony Corporation

- Baidu, Inc.

- Tencent Holdings Ltd.

- Alibaba Group

- SAP SE

- Salesforce, Inc.

- Oracle Corporation

Our Clients

View Our Licence Options