Gemstones Market By Product Type (Diamond, Emerald, Ruby, Sapphire, Alexandrite, Topaz, Others), By Product Format (Natural, Synthetic), By End User (Jewellery & Ornaments, Bangles, Necklaces, Pendants, Earrings, Rings, Anklets, Brooches, Luxury Art), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

39778

-

July 2024

-

176

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

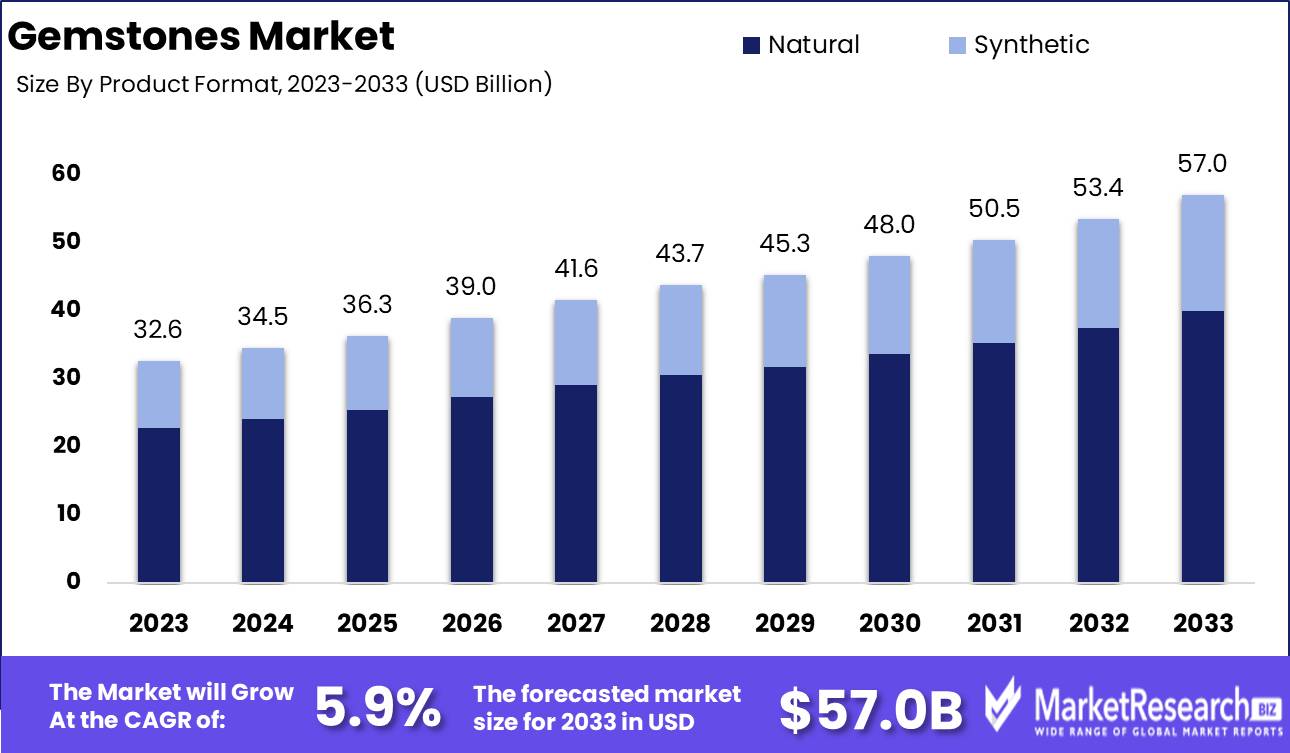

The Global Gemstones Market was valued at USD 32.6 Bn in 2023. It is expected to reach USD 57.0 Bn by 2033, with a CAGR of 5.9% during the forecast period from 2024 to 2033.

The Gemstones Market encompasses the trade and distribution of precious and semi-precious stones, including diamonds, sapphires, emeralds, rubies, and a variety of other colored stones. These gemstones are used in luxury jewelry, ornamental objects, and industrial applications. The market is characterized by factors such as the quality, cut, and rarity of the stones, as well as the demand from consumers and industries. Innovations in cutting techniques and the increasing use of technology in grading and certification have further influenced market dynamics, making the gemstones market a vital segment of the global luxury goods and industrial materials industries.

The Gemstones Market is a dynamic and multifaceted sector, driven by the demand for both aesthetic appeal in jewelry and practical applications in various industries. The market is segmented by the type of gemstone, quality, and cut, with cabochon cuts typically used for softer, opaque stones, and faceted cuts, developed in the 14th century, preferred for harder gemstones to enhance their brilliance and light reflection.

A critical factor in the valuation and utility of gemstones is their durability, which is assessed using the Mohs Scale of Hardness, introduced in 1822. This scale rates stones from 1 (softest - Talc) to 10 (hardest - Diamond), providing a standard measure for resistance to scratching and abrasion. Diamonds, rated at 10, continue to dominate the market not only for their unparalleled hardness but also for their desirability in both jewelry and industrial applications.

Technological advancements in gemstone cutting and grading have significantly influenced market trends. Enhanced precision in cutting techniques has improved the visual appeal and value of gemstones, while sophisticated grading technologies have increased transparency and trust among consumers and investors.

The market is also shaped by consumer preferences for ethically sourced and sustainably mined gemstones. This trend has led to increased scrutiny and certification processes to ensure the provenance and ethical standards of gemstone production.

Key Takeaways

- Market Value: The Global Gemstones Market was valued at USD 32.6 Bn in 2023. It is expected to reach USD 57.0 Bn by 2033, with a CAGR of 5.9% during the forecast period from 2024 to 2033.

- By Product Type: Diamond leads the market at 50%, highly valued for its aesthetic and investment qualities.

- By Product Format: Natural stones dominate with 70%, sought after for their authenticity and rarity.

- By End User: Jewellery & Ornaments are the primary consumers, accounting for 80%, driving demand in fashion and luxury sectors.

- Regional Dominance: Asia Pacific controls 50% of the market, fueled by economic growth and a strong cultural affinity for gemstones.

- Growth Opportunity: Leveraging ethical sourcing and transparency in the supply chain can enhance brand reputation and consumer trust, opening new market segments.

Driving factors

Increasing Demand for Luxury and Personalized Jewelry

The demand for luxury and personalized jewelry is a significant driver of the gemstones market. As consumers seek unique and high-quality pieces, the appeal of customized jewelry featuring precious and semi-precious gemstones has grown. The desire for exclusivity and personal expression is leading to a surge in bespoke jewelry requests, where customers choose specific gemstones to create one-of-a-kind pieces.

This trend is particularly prevalent among affluent consumers who view gemstones not only as decorative items but also as status symbols. The luxury segment's continuous expansion, supported by rising disposable incomes and a growing middle class in emerging markets, is bolstering the demand for gemstones, driving market growth.

Growing Consumer Interest in Alternative Investments

Gemstones are increasingly being recognized as a viable alternative investment, contributing to market growth. In an environment of financial uncertainty and volatile stock markets, investors are looking for tangible assets that can retain or appreciate in value over time. Gemstones, with their intrinsic value and historical appreciation, offer a compelling investment option.

The rarity and enduring appeal of gemstones such as diamonds, rubies, sapphires, and emeralds make them attractive to investors seeking to diversify their portfolios. This growing interest in gemstones as investment assets is further supported by the establishment of gemstone investment funds and the development of transparent valuation and certification processes, enhancing investor confidence and driving demand.

Rising Popularity of Gemstones in Fashion and Design

The rising popularity of gemstones in fashion and design is another key factor propelling the market. Gemstones are increasingly being used in various forms of jewelry and accessories, from high-end fashion lines to everyday wear. Influential designers and fashion houses are incorporating gemstones into their collections, setting trends and influencing consumer preferences.

The versatility of gemstones allows for their use in a wide range of styles, from traditional to contemporary, making them a staple in both classic and modern fashion. Additionally, the trend of mixing and matching different gemstones and incorporating them into various design elements has broadened their appeal, driving market growth.

Restraining Factors

High Cost and Limited Availability of Certain Gemstones

The high cost and limited availability of certain gemstones are significant restraining factors for the growth of the gemstones market. Rare gemstones such as high-quality diamonds, rubies, emeralds, and sapphires command premium prices due to their scarcity and desirability. The limited supply of these stones, exacerbated by mining challenges and geopolitical issues in key producing regions, restricts their availability in the market.

This scarcity drives up prices, making these gemstones accessible only to a wealthy segment of consumers and limiting their broader market appeal. Additionally, the high cost of these gemstones can deter potential buyers who might otherwise be interested in investing or purchasing luxury jewelry, thereby constraining market growth.

Concerns Over Ethical Sourcing

Ethical sourcing concerns are another major restraint impacting the gemstones market. The extraction of gemstones often involves significant environmental degradation and can be associated with labor practices that violate human rights, such as child labor and unsafe working conditions. These issues have raised awareness and concern among consumers, who are increasingly demanding transparency and ethical practices in the sourcing of gemstones. The rise of the "ethical consumer" has pressured the industry to adopt more sustainable and responsible practices.

Implementing and maintaining ethical sourcing standards can be challenging and costly for businesses, particularly those operating in regions with weak regulatory frameworks. The complexity and cost of ensuring ethical sourcing can slow down the supply chain, limit the availability of ethically sourced gemstones, and potentially drive up costs, further restraining market growth.

By Product Type Analysis

Diamond held a dominant market position in the By Product Type segment of the Gemstones Market, capturing more than a 50% share.

In 2023, Diamond held a dominant market position in the By Product Type segment of the Gemstones Market, capturing more than a 50% share. This dominance is driven by the enduring popularity of diamonds as the gemstone of choice for engagement rings, luxury jewelry, and investment pieces. Diamonds' unmatched hardness, brilliance, and cultural significance contribute to their high demand across various regions. The market benefits from consistent marketing efforts by major diamond producers and retailers, emphasizing the value and emotional significance of diamonds.

Emeralds hold a significant share due to their vibrant color and historical prestige, particularly in luxury and high-end jewelry markets. Despite their appeal, their market share is smaller compared to diamonds due to higher prices and specific sourcing challenges.

Rubies and Sapphires are also popular for their rich colors and durability, often used in fine jewelry. Their market shares are notable but less dominant than diamonds due to their niche appeal and varying consumer preferences.

Alexandrite and Topaz cater to specific tastes with their unique color-changing properties and affordability, respectively. While important, their market shares remain modest compared to more mainstream gemstones like diamonds.

Others include a wide range of semi-precious stones that are popular in fashion jewelry and niche markets. Their collective market share is significant but not dominant due to the diverse nature and varying appeal of these gemstones.

By Product Format Analysis

Natural held a dominant market position in the By Product Format segment of the Gemstones Market, capturing more than a 70% share.

In 2023, Natural gemstones held a dominant market position in the By Product Format segment of the Gemstones Market, capturing more than a 70% share. This dominance is driven by the high value placed on the authenticity, rarity, and natural beauty of gemstones. Consumers and collectors highly prize natural gemstones for their unique characteristics and intrinsic value. The market benefits from the perception of natural stones as more prestigious and desirable, particularly in high-end jewelry and luxury markets.

Synthetic gemstones are gaining popularity due to their affordability and ethical appeal, as they offer a conflict-free and environmentally friendly alternative to natural stones. Despite these advantages, their market share is smaller compared to natural gemstones, primarily due to lingering perceptions about their lesser value and prestige.

By End User Analysis

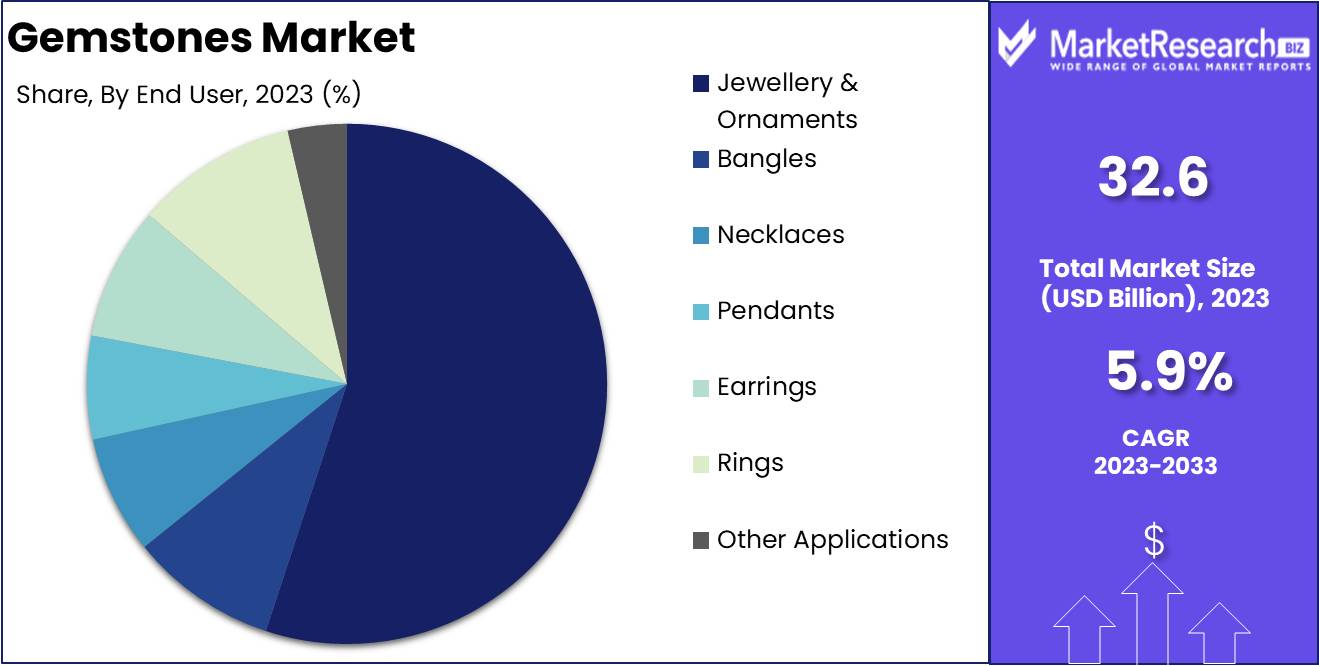

Jewellery & Ornaments held a dominant market position in the By End User segment of the Gemstones Market, capturing more than an 80% share.

In 2023, Jewellery & Ornaments held a dominant market position in the By End User segment of the Gemstones Market, capturing more than an 80% share. This significant market share is driven by the extensive use of gemstones in a wide variety of jewelry pieces, including rings, necklaces, earrings, and bracelets. The cultural and emotional significance of gemstone jewelry, particularly for special occasions such as weddings and anniversaries, supports sustained high demand. The market benefits from continuous innovations in jewelry design, appealing to diverse consumer preferences and trends.

Bangles, Necklaces, Pendants, Earrings, and Rings are integral to this segment, with each type catering to specific fashion and cultural preferences. Rings, especially engagement and wedding rings, hold a substantial share within this category due to their symbolic importance and high consumer demand.

Anklets and Brooches serve niche markets but contribute to the overall diversity and appeal of gemstone jewelry.

Luxury Art and decorative pieces that incorporate gemstones are also significant, appealing to high-net-worth individuals and collectors. Although important, their market share is relatively modest compared to mainstream jewelry pieces due to their specialized and high-value nature.

Key Market Segments

By Product Type

- Diamond

- Emerald

- Ruby

- Sapphire

- Alexandrite

- Topaz

- Others

By Product Format

- Natural

- Synthetic

By End User

- Jewellery & Ornaments

- Bangles

- Necklaces

- Pendants

- Earrings

- Rings

- Anklets

- Brooches

- Luxury Art

Growth Opportunity

Development of Lab-Grown Gemstones

The development of lab-grown gemstones presents a transformative opportunity for the global gemstones market in 2024. Lab-grown gemstones, which are chemically, physically, and optically identical to their natural counterparts, offer a sustainable and cost-effective alternative. As consumer awareness of ethical sourcing and environmental sustainability grows, lab-grown gemstones are gaining popularity.

They address key concerns such as the high cost and limited availability of certain gemstones, making high-quality stones more accessible to a broader audience. Additionally, the reduced environmental impact and ethical production processes associated with lab-grown gemstones appeal to socially conscious consumers. This shift towards lab-grown options is expected to drive significant market expansion, as they offer a reliable and scalable solution to meet growing demand.

Expansion in Online Sales and Marketing

The expansion of online sales and marketing is another pivotal growth opportunity for the gemstones market in 2024. The digital transformation of the retail sector, accelerated by the global pandemic, has reshaped consumer purchasing behaviors. E-commerce platforms provide a convenient and accessible way for consumers to explore and purchase gemstones from the comfort of their homes.

Enhanced digital marketing strategies, including social media campaigns, virtual try-ons, and influencer partnerships, are effectively reaching a wider audience and driving engagement. Online platforms also enable consumers to access a broader selection of gemstones, compare prices, and verify authenticity through digital certifications. This digital shift not only broadens the market reach but also enhances customer experience and trust, driving sales growth.

Latest Trends

Use of Colored Gemstones in Engagement Rings

The use of colored gemstones in engagement rings is a notable trend set to shape the global gemstones market in 2024. Traditionally dominated by diamonds, the engagement ring market is witnessing a shift as consumers seek unique and personalized options. Colored gemstones such as sapphires, emeralds, rubies, and even lesser-known stones like morganite and aquamarine are becoming increasingly popular choices.

This trend is driven by a desire for individuality and distinctive styles, as well as the influence of celebrity engagements showcasing colored gemstone rings. The growing acceptance and demand for colored gemstones in such significant jewelry pieces are expected to boost market growth and diversify product offerings.

Rising Demand for Ethically Sourced and Certified Gemstones

The rising demand for ethically sourced and certified gemstones is another critical trend influencing the market in 2024. Consumers are becoming more conscientious about the origins of the products they purchase, prioritizing ethical sourcing and sustainability. This shift is prompting greater transparency and accountability within the gemstones supply chain. Certifications and guarantees of ethical practices are becoming essential for gaining consumer trust and ensuring compliance with international standards.

Retailers and manufacturers are increasingly adopting sustainable practices, from responsible mining to transparent labor conditions. This trend not only aligns with consumer values but also mitigates risks associated with unethical sourcing, driving demand for certified gemstones and fostering a more responsible market environment.

Regional Analysis

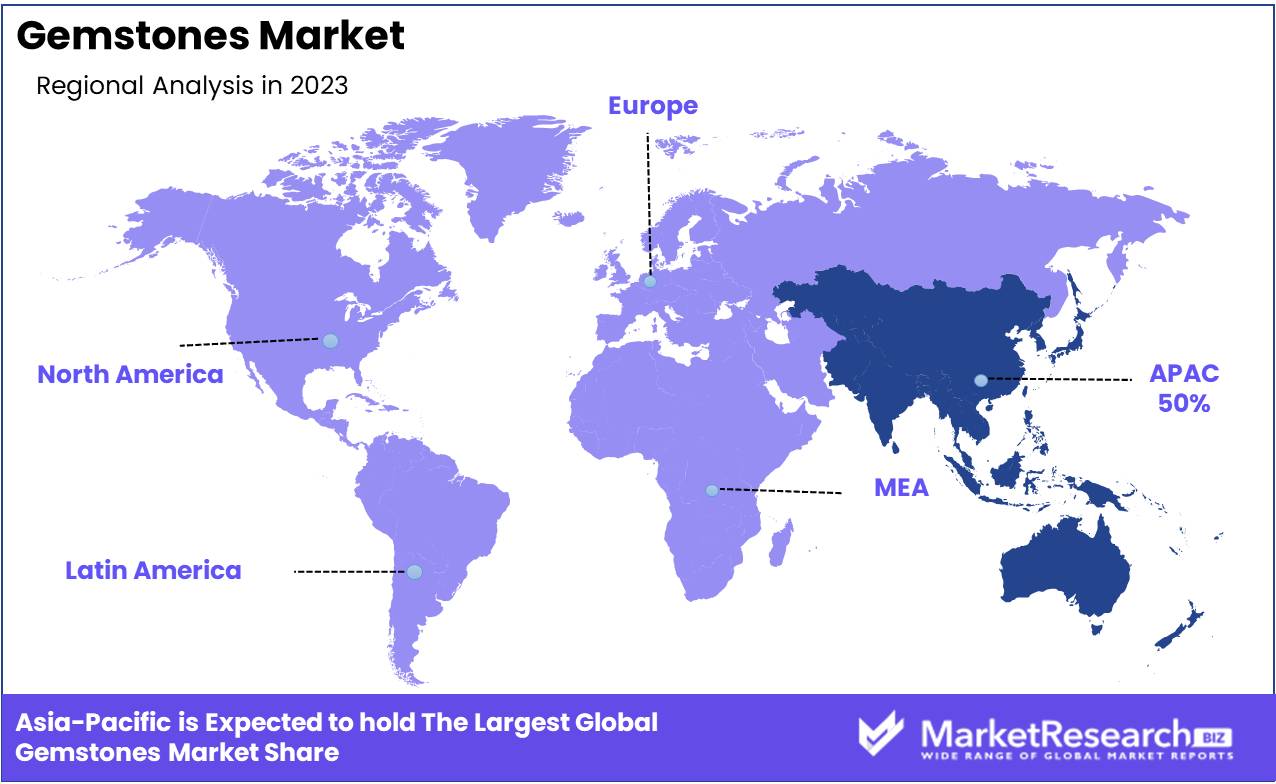

In 2023, Asia Pacific dominated the Gemstones Market, capturing a significant market share.

In 2023, Asia Pacific dominated the Gemstones Market, capturing a significant market share of around 50%. This dominance is driven by the region's rich cultural heritage and long-standing traditions of gemstone use in countries such as China, India, and Thailand. The growing middle class and increasing disposable incomes in these countries have led to higher demand for both precious and semi-precious gemstones for use in jewelry and as investment assets.

North America holds a substantial share in the gemstones market, driven by high consumer spending and strong demand for luxury goods, particularly in the US and Canada. The market favors high-quality, certified gemstones, with a focus on ethical sourcing and sustainability.

Europe's significant share in the gemstones market is supported by a rich history of gemstone use and high demand for luxury jewelry in Switzerland, the UK, France, and Italy. The market values craftsmanship and ethical sourcing, with renowned brands enhancing its appeal.

Middle East & Africa show potential in the gemstones market, with the UAE and Saudi Arabia leading due to high valuation of gemstones for adornment and investment. Africa is a key source of gemstones, driven by tourist demand for unique products.

Latin America's gemstones market is growing, led by Brazil and Colombia, due to rich gemstone resources and rising middle-class affluence. The market features local artisans and international brands, though economic variability limits overall market share.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The global Gemstones Market in 2024 is poised for dynamic growth, driven by the strategic initiatives of key players such as Gem Diamonds, SWAROVSKI, Bric Jewels Co. Ltd., JINDAL GEMS JAIPUR, Anglo American plc, Gemfields Group Limited, Petra Diamonds Limited, PJSC ALROSA, Rio Tinto, Debswana, Lucara Diamond, Botswana Diamonds PLC, Fura Gems INC., Pala International, KGK Group, Trans Hex Group, Arctic Star Exploration Corp., Blue Nile Inc., Tiffany & Co., STORNOWAY DIAMOND, and MOUNTAIN DIAMONDS.

Gem Diamonds and PJSC ALROSA lead the market with their substantial mining operations and focus on producing high-quality diamonds. Their investments in cutting-edge extraction technologies and sustainable practices position them as industry leaders committed to ethical sourcing.

SWAROVSKI, known for its luxury brand and innovative design, continues to dominate the synthetic gemstones segment. Their ability to blend artistry with precision manufacturing ensures their strong market presence and consumer appeal.

Anglo American plc, Rio Tinto, and Debswana leverage their extensive mining networks and robust supply chains to maintain a steady flow of gemstones to the market. Their focus on operational efficiency and sustainability enhances their market competitiveness.

Gemfields Group Limited and Petra Diamonds Limited emphasize transparency and responsible mining practices. Their commitment to ethical sourcing resonates with consumers and investors alike, boosting their market reputation and demand for their gemstones.

JINDAL GEMS JAIPUR and Bric Jewels Co. Ltd. cater to the growing demand for colored gemstones, leveraging their expertise in crafting unique and high-value jewelry pieces. Their focus on quality and customization appeals to discerning consumers.

Blue Nile Inc. and Tiffany & Co. are key players in the retail segment, known for their premium offerings and exceptional customer service. Their strong brand equity and strategic marketing initiatives drive consumer engagement and sales.

Market Key Players

- Gem Diamonds

- SWAROVSKI

- Bric Jewels Co. Ltd.

- JINDAL GEMS JAIPUR

- Anglo American plc

- Gemfields Group Limited

- Petra Diamonds Limited

- PJSC ALROSA

- Rio Tinto

- Debswana

- Lucara Diamond

- Botswana Diamonds PLC

- Fura Gems INC.

- Pala International

- KGK Group

- Trans Hex Group

- Arctic Star Exploration Corp.

- Blue Nile Inc.

- Tiffany & Co.

- STORNOWAY DIAMOND and MOUNTAIN DIAMONDS

Recent Development

- In June 2024, Tiffany & Co. invested $15 million in a new marketing campaign to promote their sustainable gemstone collection. This investment aims to attract environmentally conscious consumers and strengthen their brand image.

- In April 2024, PJSC ALROSA acquired a smaller diamond mining company to expand its production capacity. This acquisition is expected to increase their output by 20%, enhancing their competitive edge in the market.

Report Scope

Report Features Description Market Value (2023) USD 32.6 Bn Forecast Revenue (2033) USD 57.0 Bn CAGR (2024-2033) 5.9% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Diamond, Emerald, Ruby, Sapphire, Alexandrite, Topaz, Others), By Product Format (Natural, Synthetic), By End User (Jewellery & Ornaments, Bangles, Necklaces, Pendants, Earrings, Rings, Anklets, Brooches, Luxury Art) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Gem Diamonds, SWAROVSKI, Bric Jewels Co. Ltd., JINDAL GEMS JAIPUR, Anglo American plc, Gemfields Group Limited, Petra Diamonds Limited, PJSC ALROSA, Rio Tinto, Debswana, Lucara Diamond, Botswana Diamonds PLC, Fura Gems INC., Pala International, KGK Group, Trans Hex Group, Arctic Star Exploration Corp., Blue Nile Inc., Tiffany & Co., STORNOWAY DIAMOND and MOUNTAIN DIAMONDS Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Gem Diamonds

- SWAROVSKI

- Bric Jewels Co. Ltd.

- JINDAL GEMS JAIPUR

- Anglo American plc

- Gemfields Group Limited

- Petra Diamonds Limited

- PJSC ALROSA

- Rio Tinto

- Debswana

- Lucara Diamond

- Botswana Diamonds PLC

- Fura Gems INC.

- Pala International

- KGK Group

- Trans Hex Group

- Arctic Star Exploration Corp.

- Blue Nile Inc.

- Tiffany & Co.

- STORNOWAY DIAMOND and MOUNTAIN DIAMONDS

Our Clients

View Our Licence Options