Fumigation Products Market By Type (Phosphine, Chloropicrin, Telone, Metam Sodium, DimethylDisulfide, 1,3-Dichloropropene, Others), By Form (Solid, Liquid, Gas), By End User (Residential, Agricultural, Warehouses/ Storage, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48481

-

July 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

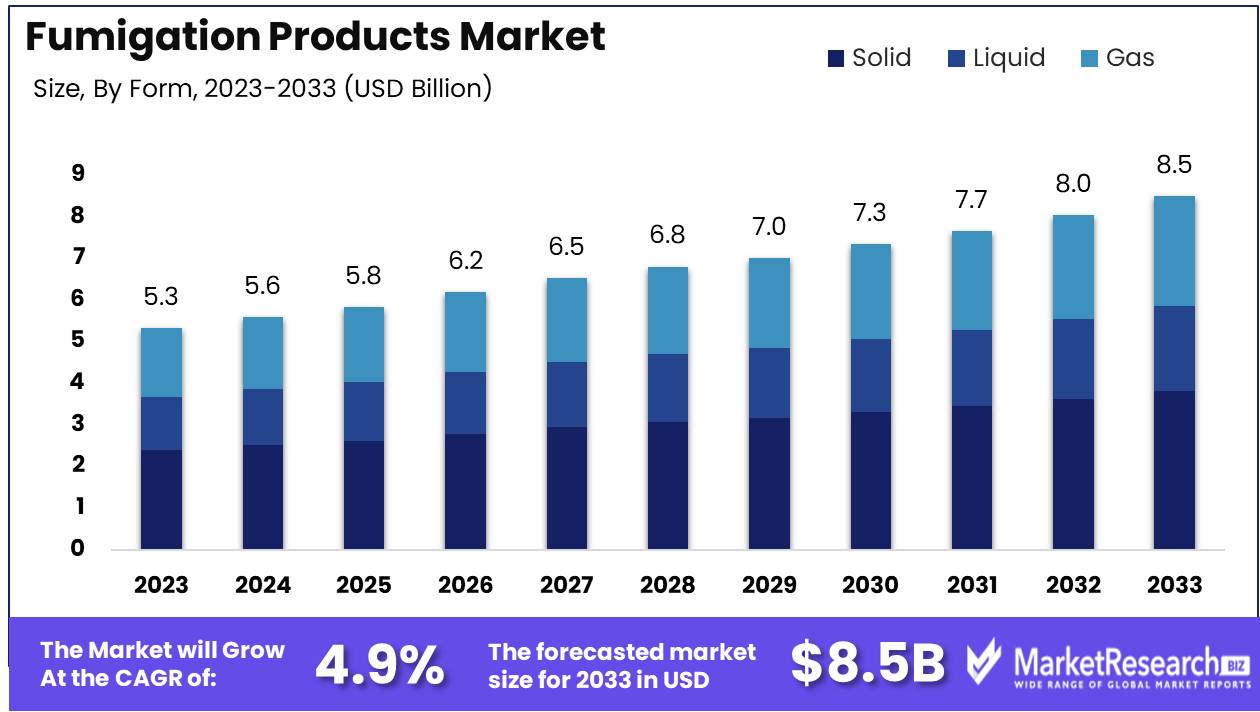

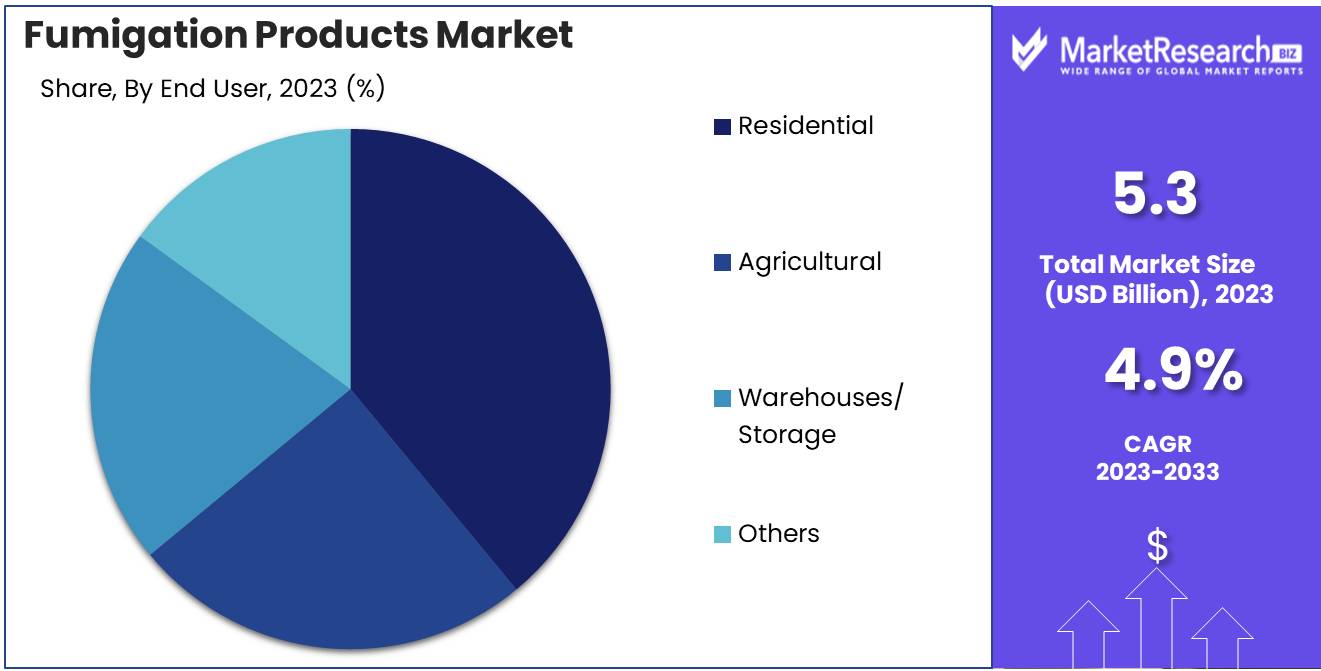

The Fumigation Products Market was valued at USD 5.3 billion in 2023. It is expected to reach USD 8.5 billion by 2033, with a CAGR of 4.9% during the forecast period from 2024 to 2033.

The fumigation products market encompasses a range of chemical and biological agents used to eliminate pests and pathogens from agricultural produce, storage facilities, and residential areas. This market includes products like fumigants, insecticides, and disinfectants, essential for ensuring food safety, preserving crop yields, and maintaining hygiene. Driven by increasing global food production, stringent regulatory frameworks, and rising awareness of pest control benefits, the market is experiencing significant growth.

The Fumigation Products Market is poised for significant growth, driven by several key factors. The increasing agricultural activities globally are a primary driver, as the need for effective pest control in crop production continues to escalate. This demand is particularly pronounced in regions with intensive farming practices, where pest infestations can severely impact crop yields and quality. Concurrently, the trend of urbanization is contributing to higher demand for pest control services in urban and suburban areas. As cities expand, the interaction between human habitats and pest populations increases, necessitating efficient fumigation solutions.

However, the market faces challenges from stringent regulatory restrictions on certain fumigants, such as methyl bromide, which have been identified for their adverse environmental and health impacts. These regulations are prompting manufacturers to innovate and develop safer, more environmentally friendly alternatives. Additionally, health and safety concerns associated with fumigation chemicals are influencing market dynamics. There is a growing emphasis on adopting integrated pest management (IPM) practices that minimize chemical use and focus on sustainable solutions. This shift is expected to drive the development of advanced fumigation products that balance efficacy with safety, aligning with regulatory standards and consumer preferences.

In summary, while the Fumigation Products Market is set to grow, it must navigate regulatory and safety challenges. The sector's ability to innovate and adapt to these constraints will be crucial in capturing the expanding demand from agricultural and urban sectors. The industry's trajectory will be shaped by its responsiveness to regulatory frameworks and its commitment to developing safer, effective pest control solutions.

Key Takeaways

- Market Growth: The Fumigation Products Market was valued at USD 5.3 billion in 2023. It is expected to reach USD 8.5 billion by 2033, with a CAGR of 4.9% during the forecast period from 2024 to 2033.

- By Type: Phosphine dominated the Fumigation Products Market by type.

- By Form: Solid Fumigants dominated the Fumigation Products Market.

- By End User: The Residential segment dominated the Fumigation Products Market.

- Regional Dominance: Asia Pacific dominates the fumigation products market with a 32% largest share.

- Growth Opportunity: The global fumigation products market is poised for significant growth, driven by eco-friendly demand and innovative formulations.

Driving factors

Rising Pest Infestations in Warehouses and Crop Storage Facilities

The increase in pest infestations within warehouses and crop storage facilities is a significant driver of the fumigation products market. As pests pose substantial threats to stored goods, leading to financial losses and reduced product quality, the demand for effective fumigation solutions has surged. This rise in infestations is attributed to inadequate pest control measures, changing climatic conditions that favor pest proliferation, and the global increase in food production and storage activities. The necessity to protect stored products from pest damage propels market growth, as businesses seek to mitigate losses and ensure the integrity of their inventory.

Growing Awareness of Crop Protection Agents and Urbanization in Developing Nations

The heightened awareness of crop protection agents, combined with rapid urbanization in developing nations, significantly contributes to the expansion of the fumigation products market. As urbanization accelerates, agricultural practices become more intensive and concentrated, increasing the likelihood of pest infestations. This urban growth also fosters improved access to information and resources, enabling farmers and storage facility operators to adopt advanced fumigation techniques. The increased focus on protecting crops from pests is reflected in the rising adoption of fumigation products, driven by educational initiatives, government support, and the need for sustainable agricultural practices. Consequently, the market experiences growth as awareness and urbanization trends continue to evolve.

Expansion of the Agricultural Sector and Need to Reduce Post-Harvest Losses Caused by Pests

The agricultural sector's expansion, coupled with the imperative to reduce post-harvest losses caused by pests, plays a crucial role in driving the fumigation products market. As global agricultural activities intensify to meet the food demands of a growing population, the vulnerability to pest infestations during storage and transportation increases. Post-harvest losses represent a significant economic burden, with estimates indicating that pests account for 20-30% of such losses globally. The urgent need to protect agricultural produce and enhance food security fuels the demand for effective fumigation solutions. Innovations in fumigation technology, alongside increased investment in agricultural infrastructure, bolster market growth by addressing the challenges of pest management and post-harvest preservation.

Restraining Factors

Intermittency and Reliability: Challenges in Consistent Efficacy

The fumigation products market faces significant challenges due to intermittency and reliability issues, impacting the consistent efficacy of these products. Intermittency refers to the irregular or sporadic effectiveness of fumigation treatments, which can be influenced by various factors such as weather conditions, pest resistance, and the quality of the fumigation product itself. This inconsistency can lead to repeated applications, thereby increasing operational costs and reducing overall market attractiveness.

Additionally, reliability issues stem from the varying effectiveness of fumigation treatments across different environments and pest species. This unpredictability can erode user confidence, prompting a preference for alternative pest control methods perceived as more reliable. Consequently, these factors collectively restrain market growth by diminishing consumer trust and increasing costs.

Concerns about Residual Effects: Health and Environmental Implications

Concerns regarding the residual effects of fumigation products significantly restrain market growth due to heightened awareness and regulatory scrutiny. Residual effects refer to the potentially harmful chemical residues left behind after fumigation, which can pose health risks to humans and animals, as well as environmental hazards. Increasing evidence of these adverse effects has led to stricter regulations and compliance requirements for fumigation product manufacturers.

Additionally, consumers and businesses are increasingly opting for safer, environmentally friendly alternatives, further curbing the demand for traditional fumigation products. This shift is driven by growing health consciousness and environmental awareness, compelling manufacturers to innovate and develop products with minimal residual impact. However, the transition to safer formulations can be costly and time-consuming, posing additional challenges to market growth.

By Type Analysis

In 2023, Phosphine dominated the Fumigation Products Market by type.

In 2023, Phosphine held a dominant market position in the By Type segment of the Fumigation Products Market. The primary reason for this dominance is Phosphine's efficacy as a fumigant, widely utilized in the agriculture sector for pest control in stored grain and other commodities. Its ability to penetrate deeply and eliminate a broad spectrum of pests has made it a preferred choice. Additionally, Phosphine is favored due to its relatively lower cost and reduced environmental impact compared to some alternatives.

Chloropicrin, known for its strong odor and effectiveness against a wide range of pests, occupies a significant share of the market. Telone, primarily used for soil fumigation, is valued for its ability to control nematodes, which are critical agricultural pests. Metam Sodium, another major fumigant, is appreciated for its versatility and effectiveness against soil-borne diseases, weeds, and nematodes.

Dimethyl Disulfide (DMDS) is gaining traction due to its environmental benefits and effectiveness as a nematicide. 1,3-Dichloropropene is also notable for its application in pre-plant soil fumigation, helping control various soil pests. Other fumigants, including a range of specialized products, contribute to the market by addressing specific pest control needs. These alternatives, while not as dominant as Phosphine, play crucial roles in integrated pest management strategies, ensuring comprehensive protection against pests in various agricultural and storage settings.

By Form Analysis

In 2023, Solid Fumigants dominated the Fumigation Products Market.

In 2023, The Solid form held a dominant market position in the Fumigation Products Market, attributed to its ease of application and longer residual effect compared to other forms. Solid fumigants, often utilized in granules or powder form, are highly effective in controlling pests in stored grains and other agricultural produce. Their stability and slower release of active ingredients ensure prolonged protection, making them a preferred choice among agricultural and industrial users.

Liquid fumigants, while less dominant, are crucial in scenarios requiring rapid action. These are particularly effective in soil fumigation and structural fumigation due to their ability to penetrate deeply and act quickly against pests. Their application, however, requires specialized equipment and safety measures, which slightly limits their market share compared to solid fumigants.

Gas fumigants, known for their ability to diffuse and penetrate hard-to-reach areas, play a vital role in treating large-scale storage facilities and quarantine treatments. Despite their efficiency, the need for stringent safety regulations and controlled environments during application has kept their market share below that of solid and liquid forms. Each form of fumigant serves distinct purposes, catering to various needs across agriculture, industrial storage, and pest control sectors, contributing to the overall growth of the Fumigation Products Market.

By End User Analysis

In 2023, The Residential segment dominated the Fumigation Products Market.

In 2023, The Residential Segment held a dominant market position in the end-user segment of the Fumigation Products Market. This dominance can be attributed to the rising demand for pest control solutions in urban and suburban areas, where homeowners prioritize the safety and comfort of their living environments. The increasing awareness of health risks associated with pest infestations and the growing trend of preventive pest management further bolstered this segment's growth.

The Agricultural sector also demonstrated significant growth, driven by the need to protect crops from pests and diseases, ensuring higher yield and quality. This segment's expansion is supported by advancements in fumigation technologies and the adoption of integrated pest management practices.

Warehouses/Storage facilities represented a crucial market segment, as the necessity to safeguard stored goods from pest damage and contamination remained paramount. The stringent regulatory requirements for maintaining hygiene standards in storage environments further fueled the demand for fumigation products in this sector.

Lastly, the Others category, encompassing industrial and commercial establishments, also contributed to the market growth. The increasing focus on maintaining pest-free environments in manufacturing units, food processing plants, and other commercial spaces highlighted the importance of fumigation products across various applications.

Key Market Segments

By Type

- Phosphine

- Chloropicrin

- Telone

- Metam Sodium

- DimethylDisulfide

- 1,3-Dichloropropene

- Others

By Form

- Solid

- Liquid

- Gas

By End User

- Residential

- Agricultural

- Warehouses/ Storage

- Others

Growth Opportunity

Increasing Demand for Eco-Friendly and Organic Fumigants

A notable trend influencing the fumigation products market is the escalating demand for eco-friendly and organic fumigants. With rising environmental concerns and stringent regulatory frameworks, consumers and businesses are increasingly favoring sustainable products. The shift towards organic fumigants, which are perceived as safer for both health and the environment, is expected to propel market growth. This trend is particularly prominent in the agricultural sector, where there is a heightened awareness of the adverse effects of chemical fumigants on soil health and biodiversity.

Developing Innovative Formulations

Innovation in fumigation product formulations is another critical growth driver. Companies are investing heavily in research and development to create more effective and safer fumigants. These innovative formulations are designed to enhance efficacy, reduce application time, and minimize harmful residues. The introduction of advanced fumigation technologies, such as controlled-release formulations and microencapsulation, is expected to significantly boost market adoption. Such innovations not only improve the efficiency of fumigation processes but also align with the growing preference for environmentally sustainable practices.

Latest Trends

Increasing Adoption of Eco-Friendly and Organic Fumigants

The market for fumigation products is witnessing a significant shift towards eco-friendly and organic alternatives. This trend is driven by heightened awareness of environmental sustainability and the adverse effects of chemical fumigants on health and ecosystems. In response to regulatory pressures and consumer preferences, manufacturers are innovating and investing in the development of organic fumigants derived from natural sources. These products offer the advantage of being less toxic and biodegradable, thereby reducing environmental impact. As countries enforce stricter regulations on chemical use, the adoption of these eco-friendly solutions is expected to gain momentum, fostering a safer and more sustainable approach to pest control.

Growing Demand for Technology-Enabled Fumigation Solutions

The integration of technology in fumigation practices is revolutionizing the market. Advanced technology-enabled solutions, such as automated fumigation systems and remote monitoring tools, are becoming increasingly popular. These innovations offer enhanced precision, efficiency, and safety in fumigation processes. Automated systems can control fumigant release with high accuracy, minimizing wastage and ensuring optimal dosage. Additionally, remote monitoring tools provide real-time data and analytics, allowing for better decision-making and proactive management of fumigation activities. The adoption of such technology-driven solutions is expected to improve operational efficiencies and reduce costs, making them highly attractive to commercial users.

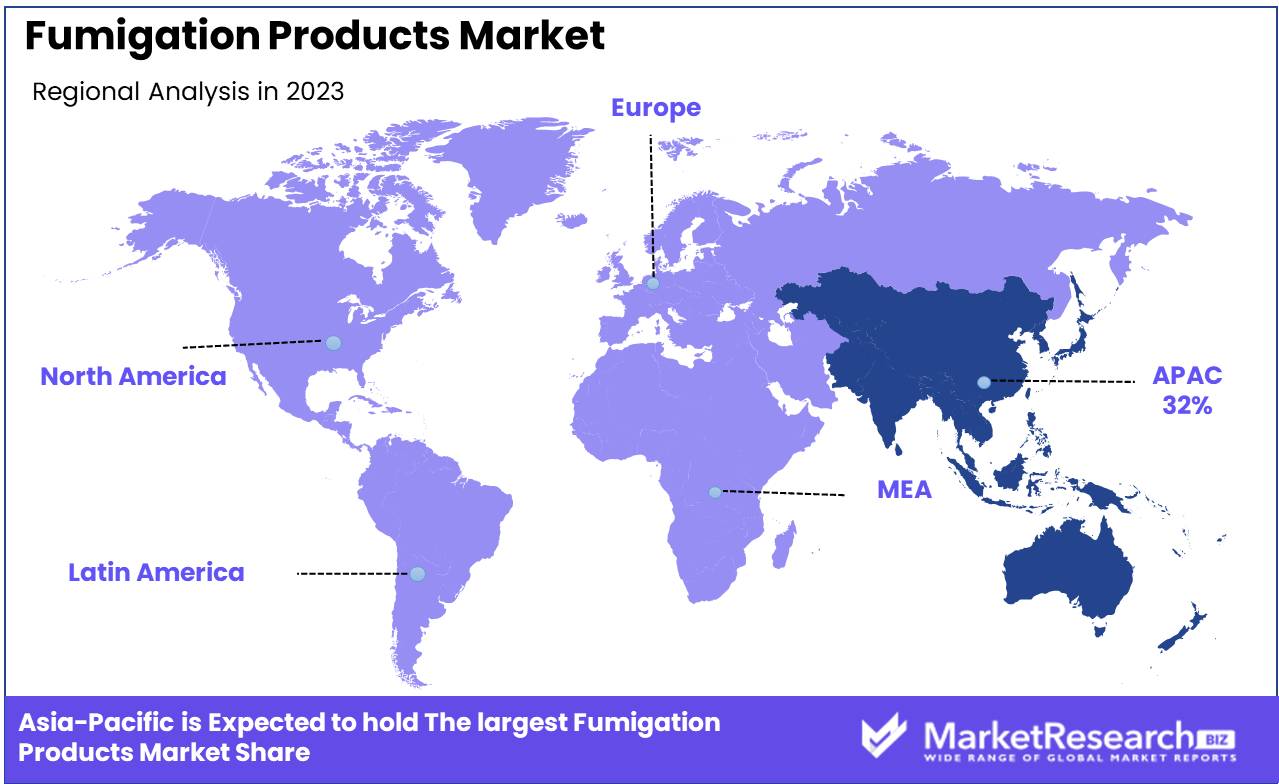

Regional Analysis

Asia Pacific dominates the fumigation products market with a 32% largest share.

The global fumigation products market exhibits diverse growth patterns across various regions, driven by differing regulatory frameworks, agricultural practices, and pest control needs. In North America, the market is bolstered by stringent agricultural regulations and a high demand for effective pest management solutions. The region accounted for approximately 25% of the global market share in 2023, supported by advancements in fumigation technology and the presence of major market players. Europe follows closely, with a market share of around 22%, driven by robust agricultural sectors in countries like Germany and France and increasing awareness about food safety standards.

Asia Pacific emerges as the dominant region, holding the largest market share of 32% in 2023, attributed to rapid industrialization, growing agricultural activities, and the adoption of advanced fumigation practices in countries such as China and India. The region's market growth is further accelerated by increasing investments in agriculture and rising incidences of pest infestations.

The Middle East & Africa region captures a smaller yet significant market share of 10%, driven by the growing need for pest control in stored grains and expanding agricultural activities in countries like Egypt and South Africa. Latin America holds an 11% market share, supported by the extensive cultivation of crops and the implementation of integrated pest management practices in countries such as Brazil and Argentina.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global fumigation products market in 2024 is poised for significant growth, driven by the increasing need for pest control in agricultural and urban settings. Key players such as BASF SE and Bayer AG are at the forefront, leveraging their extensive research and development capabilities to innovate and introduce advanced fumigation solutions. BASF SE’s focus on sustainability and Bayer AG’s integrated pest management strategies are expected to solidify their market positions.

The Dow Chemical Company and FMC Corporation are also crucial contributors, with their robust product portfolios and global reach. Their strategic investments in technology and expansion into emerging markets are anticipated to enhance their market shares. Syngenta AG’s strong agronomic expertise and Rentokil Initial plc’s comprehensive pest control services further contribute to market dynamics, offering end-to-end solutions.

Ecolab Inc. and Terminix International Company LP continue to dominate the commercial fumigation sector, providing specialized services and maintaining high standards of safety and efficacy. Companies like Eurofins Scientific and Rollins Inc. bring valuable expertise in compliance and quality assurance, ensuring regulatory adherence and customer satisfaction.

New entrants like Industrial Fumigant Company LLC and Royal Agro Organic Pvt. Ltd. are expected to drive competition, focusing on niche markets and organic fumigation products. Established players such as Solvay S.A., Detia Degesch GmbH, and AMVAC Chemical Corporation maintain their foothold through continuous innovation and strategic partnerships.

Overall, the fumigation products market in 2024 will witness dynamic growth and diversification, with major companies investing in sustainable and efficient solutions to meet the evolving demands of global pest control.

Market Key Players

- BASF SE

- Bayer AG

- Dow Chemical Company

- FMC Corporation

- Syngenta AG

- Rentokil Initial plc

- Ecolab Inc.

- Terminix International Company LP

- Eurofins Scientific

- Rollins Inc.

- Solvay S.A.

- Detia Degesch GmbH

- Industrial Fumigant Company LLC

- Royal Agro Organic Pvt. Ltd.

- UPI-USA

- National Fumigants

- Corteva Agriscience

- JAFFER Group of Companies

- AMVAC Chemical Corporation

Recent Development

- In June 2024, Western Fumigation Company partnered with Hot Logistics, USDA, and Draslovka Services to utilize Draslovka's fumigant product eFume. This collaboration aims to enhance the fumigation processes in containers, silos, and other storage structures, reflecting an increase in demand for fumigants in commercial and industrial sectors.

- In March 2024, Solvay S.A. introduced a new eco-friendly fumigant formulation designed to reduce environmental impact while maintaining high efficacy in pest control. This development is part of their broader strategy to align with growing environmental regulations and market demand for sustainable pest control solutions.

- In April 2024, Corteva Agriscience announced the expansion of its fumigation product line, specifically focusing on the Asia Pacific region. This expansion aims to meet the increasing demand for effective pest control in agricultural sectors, driven by the region's significant agricultural production growth.

Report Scope

Report Features Description Market Value (2023) USD 5.3 Billion Forecast Revenue (2033) USD 8.5 Billion CAGR (2024-2032) 4.9% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Phosphine, Chloropicrin, Telone, Metam Sodium, DimethylDisulfide, 1,3-Dichloropropene, Others), By Form (Solid, Liquid, Gas), By End User (Residential, Agricultural, Warehouses/ Storage, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape BASF SE, Bayer AG, Dow Chemical Company, FMC Corporation, Syngenta AG, Rentokil Initial plc, Ecolab Inc., Terminix International Company LP, Eurofins Scientific, Rollins Inc., Solvay S.A., Detia Degesch GmbH, Industrial Fumigant Company LLC, Royal Agro Organic Pvt. Ltd., UPI-USA, National Fumigants, Corteva Agriscience, JAFFER Group of Companies, AMVAC Chemical Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- BASF SE

- Bayer AG

- Dow Chemical Company

- FMC Corporation

- Syngenta AG

- Rentokil Initial plc

- Ecolab Inc.

- Terminix International Company LP

- Eurofins Scientific

- Rollins Inc.

- Solvay S.A.

- Detia Degesch GmbH

- Industrial Fumigant Company LLC

- Royal Agro Organic Pvt. Ltd.

- UPI-USA

- National Fumigants

- Corteva Agriscience

- JAFFER Group of Companies

- AMVAC Chemical Corporation

Our Clients

View Our Licence Options