FMCG Market By Product Type (Food & Beverage, Health Care, Personal Care, Home Care), , By Distribution Channel (Grocery Stores, Supermarkets & Hypermarkets, E-commerce, Specialty Stores), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

9921

-

June 2024

-

181

-

-

This report was compiled by Research Team Research team of over 50 passionate professionals leverages advanced research methodologies and analytical expertise to deliver insightful, data-driven market intelligence that empowers businesses across diverse industries to make strategic, well-informed Correspondence Research Team Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

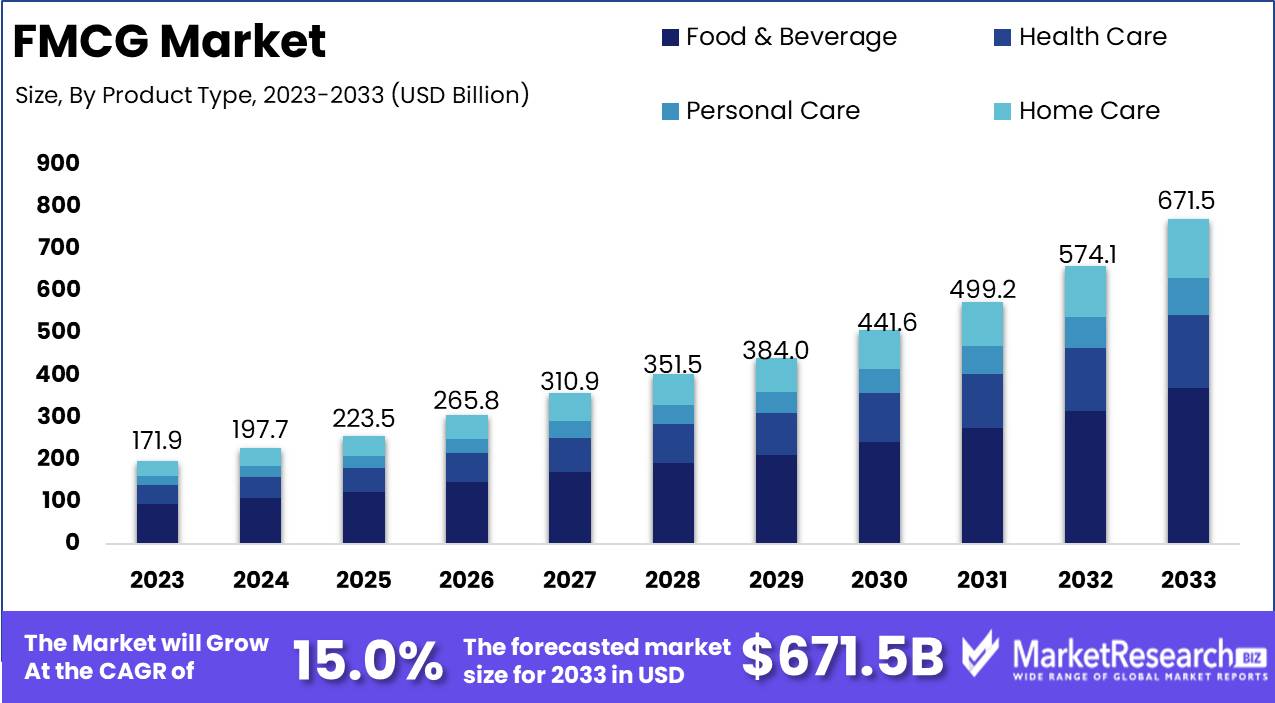

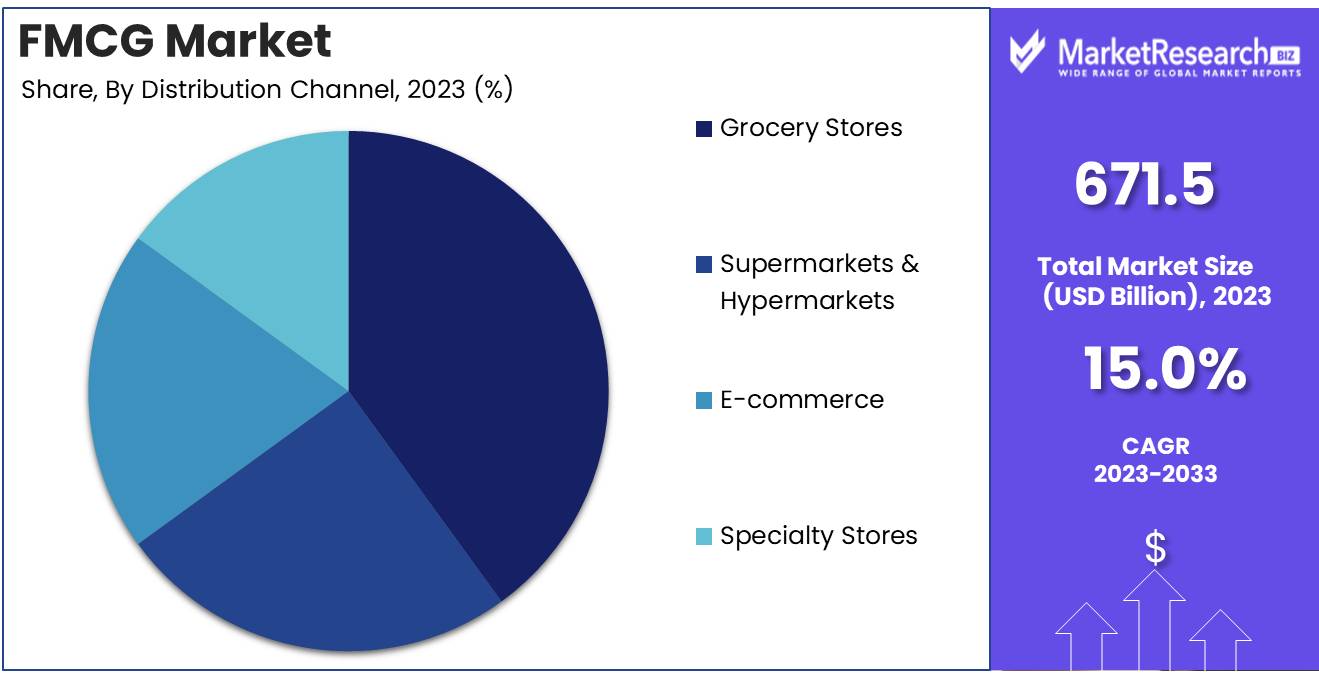

The Global FMCG Market was valued at USD 171.9 Bn in 2023. It is expected to reach USD 671.5 Bn by 2033, with a CAGR of 15% during the forecast period from 2024 to 2033.

The FMCG market encompasses products that are sold quickly and at relatively low cost, such as packaged foods, beverages, toiletries, over-the-counter drugs, and other consumables. This sector is characterized by high consumer demand and rapid inventory turnover. Companies operating in this market focus on efficient supply chain management, strong distribution networks, and effective marketing strategies to maintain competitive advantage. The FMCG market is pivotal to the global economy, driving significant revenue streams and influencing trends across various industries.

The FMCG market remains a dynamic and competitive sector, driven by rapid inventory turnover and high consumer demand. Recent trends indicate a significant shift towards premiumization, as evidenced by Parle Products' strategic reclassification of 15%-18% of its portfolio as premium and ITC's achievement in doubling the contribution of its premium personal care portfolio over the past four years. This shift underscores the growing consumer preference for high-quality, value-added products, highlighting the need for FMCG companies to innovate and differentiate to capture market share.

The FMCG market remains a dynamic and competitive sector, driven by rapid inventory turnover and high consumer demand. Recent trends indicate a significant shift towards premiumization, as evidenced by Parle Products' strategic reclassification of 15%-18% of its portfolio as premium and ITC's achievement in doubling the contribution of its premium personal care portfolio over the past four years. This shift underscores the growing consumer preference for high-quality, value-added products, highlighting the need for FMCG companies to innovate and differentiate to capture market share.In an increasingly saturated market, companies must leverage advanced analytics and consumer insights to tailor their offerings. Investment in sustainable practices and digital transformation is crucial, not only to meet regulatory requirements but also to resonate with environmentally conscious consumers. The integration of e-commerce platforms and omnichannel strategies further enhances consumer reach and engagement, allowing for a seamless shopping experience.

Supply chain resilience has become paramount, as disruptions from global events have exposed vulnerabilities. Companies must focus on building robust and agile supply chains to mitigate risks and ensure uninterrupted product availability. This involves diversifying supplier bases, investing in technology for real-time tracking, and fostering closer collaboration with key stakeholders.

Key Takeaways

- Market Value: The Global FMCG Market was valued at USD 171.9 Bn in 2023. It is expected to reach USD 671.5 Bn by 2033, with a CAGR of 15% during the forecast period from 2024 to 2033.

- By Product Type: Food & Beverage segment holds the largest share, accounting for approximately 55% of the FMCG market.

- By Distribution Channel: Grocery Stores dominating the distribution channels, grocery stores account for about 40% of FMCG sales.

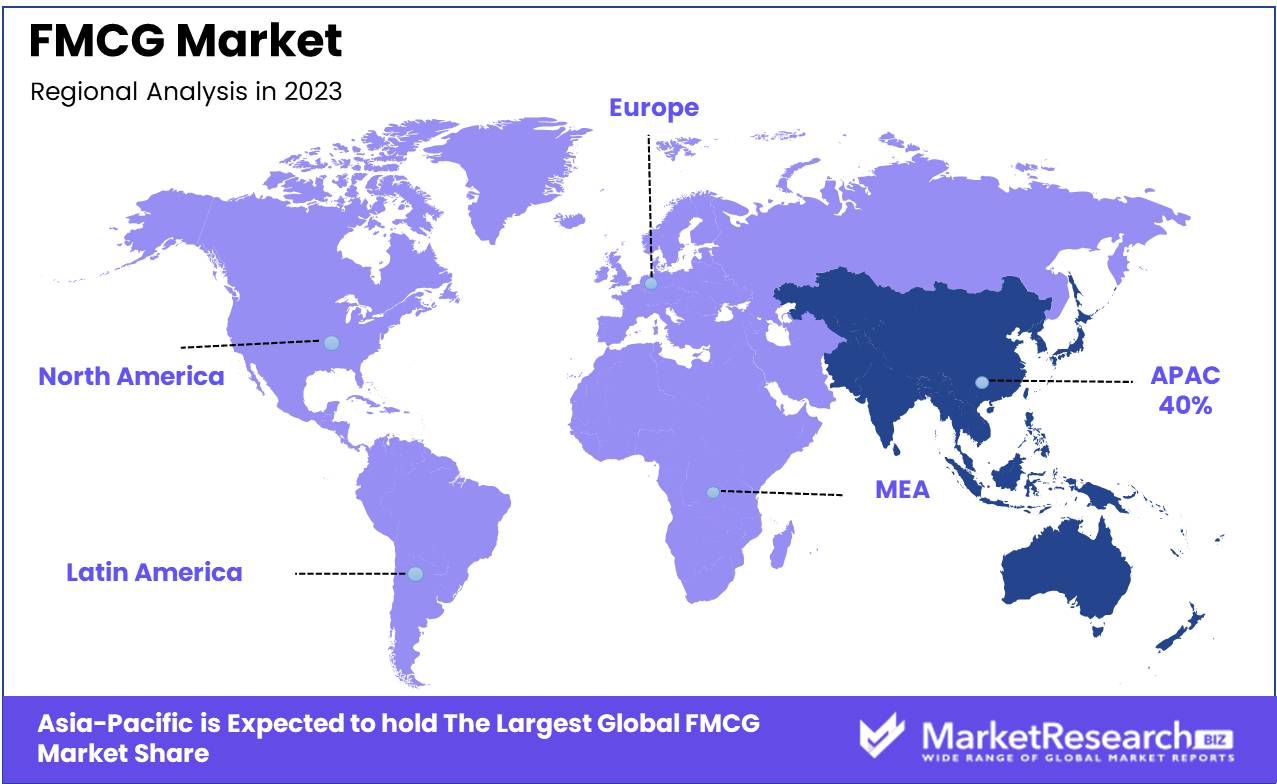

- Regional Dominance: The Asia-Pacific region dominates the FMCG market, accounting for approximately 40% of the market share.

- Growth Opportunity: Expanding e-commerce platforms and digital marketing strategies present significant growth opportunities in the FMCG market.

Driving factors

Rising Disposable Incomes

The rise in disposable incomes across various demographic segments is a significant driver of the FMCG market growth. As consumers experience higher purchasing power, their expenditure on consumer goods increases, leading to a direct surge in market demand. Higher disposable incomes enable consumers to not only purchase more products but also opt for premium and branded goods, which often offer better quality and perceived value.

This trend towards premiumization is evident in categories such as personal care, food and beverages, and household products, where consumers are willing to pay a premium for organic, sustainable, or luxury variants. The increased spending capacity also fuels the growth of emerging product categories and innovation within the FMCG sector, as companies strive to cater to the evolving preferences of a more affluent consumer base.

Rural Market Growth

The growth of rural markets represents a vast and relatively untapped opportunity for the FMCG sector. With increasing rural incomes and improved infrastructure, including better roads, telecommunications, and supply chain logistics, FMCG companies can now reach these previously inaccessible areas more efficiently. The rural population's growing awareness and aspiration towards modern lifestyles drive demand for a wide range of consumer goods. Moreover, government initiatives aimed at rural development and financial inclusion have enhanced the purchasing power and consumption patterns in these regions.

FMCG companies are tailoring their product offerings and marketing strategies to cater specifically to rural consumers, focusing on affordability, smaller packaging sizes, and localized marketing campaigns. The rural market growth not only contributes to overall market expansion but also provides a buffer against urban market saturation.

Increasing Working Women

The rise in the number of working women is reshaping consumption patterns and driving innovation in the FMCG market. As more women enter the workforce, their time constraints and disposable incomes influence their purchasing decisions, leading to a higher demand for convenient, time-saving, and health-oriented products. This trend is particularly pronounced in categories such as ready-to-eat meals, snacks, personal care products, and household cleaning items. Working women prioritize efficiency and convenience, pushing FMCG companies to innovate and develop products that cater to their specific needs, such as quick-preparation foods, multi-functional personal care items, and effective household cleaners.

The increased financial independence of working women contributes to a shift in household decision-making dynamics, often resulting in more diversified and higher-value purchases. Companies that understand and address the unique preferences and challenges of this demographic are well-positioned to capture a significant share of the FMCG market growth.

Restraining Factors

High Launch Costs

High launch costs represent a significant challenge for FMCG companies, particularly when introducing new products to the market. These costs encompass a wide range of expenses, including research and development, production, marketing, distribution, and promotional activities. The necessity of substantial investment in these areas can be a formidable barrier to entry, especially for smaller firms and startups, limiting their ability to compete with established players.

High launch costs can also impact larger companies by requiring careful allocation of resources and strategic planning to ensure a return on investment. This often leads to a cautious approach in product innovation and market expansion, potentially slowing down the overall pace of new product introductions in the FMCG sector. Companies must therefore balance the need for innovation and market differentiation with the financial risks associated with high launch costs.

Logistics Challenges

Logistics challenges are a critical factor influencing the growth and efficiency of the FMCG market. The distribution of fast-moving consumer goods involves complex supply chain networks that must ensure timely delivery and availability of products across diverse geographies. Key logistics challenges include transportation infrastructure limitations, warehousing inefficiencies, supply chain disruptions, and last-mile delivery hurdles.

Transportation infrastructure, particularly in emerging markets, can significantly affect the ability to distribute goods efficiently. Poor road conditions, traffic congestion, and inadequate transport facilities can lead to delays, increased costs, and compromised product quality. Warehousing inefficiencies, such as inadequate storage facilities and inventory management issues, further exacerbate these problems, leading to stockouts or excess inventory.

By Product Type Analysis

Food & Beverage dominated the By Product Type segment of the FMCG Market, 55% of the market share.

In 2023, Food & Beverage held a dominant market position in the By Product Type segment of the FMCG Market, capturing more than a 55% share. This significant market share underscores the critical role of the Food & Beverage sector within the FMCG industry, driven by increasing consumer demand for convenience foods, beverages, and ready-to-eat products. The segment's growth can be attributed to rising urbanization, changing dietary habits, and a growing preference for healthier and organic food options.

The Health Care segment has also shown substantial growth, reflecting an increasing consumer focus on health and wellness. This segment encompasses a wide range of products, including over-the-counter medications, vitamins, supplements, and other health-related items. The growing awareness of preventive healthcare and the rising incidence of lifestyle-related diseases have driven demand in this segment.

Personal Care products have maintained a strong presence in the FMCG market. This segment includes a variety of products such as skincare, haircare, cosmetics, and hygiene products. The rising emphasis on personal grooming and the influence of social media on beauty standards have significantly contributed to the growth of this segment.

The Home Care segment, encompassing cleaning agents, detergents, and other household products, has also experienced steady growth. Increasing awareness about hygiene and cleanliness, along with innovations in eco-friendly and sustainable products, has propelled the demand in this segment.

By Distribution Channel Analysis

Grocery stores, leading with over 40% market share, remain the primary distribution channel for FMCG products.

In 2023, Grocery Stores held a dominant market position in the By Distribution Channel segment of the FMCG Market, capturing more than a 40% share. This significant market share highlights the crucial role of grocery stores in the FMCG sector, driven by consumer preferences for convenience and accessibility. The growth of grocery stores is attributed to their widespread presence, local reach, and the ability to offer a variety of everyday essential products.

Supermarkets & hypermarkets also hold a substantial share in the FMCG market. These large retail formats provide a one-stop shopping experience, offering an extensive selection of products under one roof. The competitive pricing, promotional offers, and wide product assortments attract a diverse customer base, making this channel a key player in the FMCG market.

The E-commerce segment has shown remarkable growth, reflecting the increasing consumer shift towards online shopping. The convenience of home delivery, availability of a wide range of products, and attractive discounts have driven the popularity of e-commerce platforms. The ongoing digital transformation and the rise in smartphone usage have further accelerated the growth of this distribution channel.

Specialty stores, focusing on specific product categories such as health foods, organic products, and niche personal care items, have also carved out a significant niche in the FMCG market. These stores cater to the growing consumer demand for specialized and premium products, offering a curated selection that appeals to discerning customers seeking quality and unique items.

Key Market Segments

By Product Type

- Food & Beverage

- Health Care

- Personal Care

- Home Care

By Distribution Channel

- Grocery Stores

- Supermarkets & Hypermarkets

- E-commerce

- Specialty Stores

Growth Opportunity

E-commerce Expansion

The rapid expansion of e-commerce presents a significant growth opportunity for the global FMCG market in 2024. With the continued rise of online shopping, FMCG companies can reach a broader audience, including tech-savvy millennials and Gen Z consumers who prefer the convenience of digital platforms. E-commerce not only provides a cost-effective distribution channel but also enables personalized marketing and direct consumer engagement, fostering brand loyalty.

The integration of advanced technologies like AI and big data analytics enhances the consumer shopping experience through personalized recommendations and seamless transaction processes. As more consumers shift to online purchasing, FMCG companies that invest in robust e-commerce strategies will likely experience substantial market growth.

Processed Food Market Growth

The growth of the processed food market is another key driver of FMCG market expansion in 2024. Increasing urbanization, hectic lifestyles, and a growing preference for convenient meal options have led to a surge in demand for processed and ready-to-eat foods. This trend is particularly pronounced among working professionals and dual-income households seeking quick and easy meal solutions without compromising on quality and nutrition.

Innovations in food processing technology and a focus on health-oriented products, such as organic and low-calorie options, further boost market appeal. FMCG companies that capitalize on this trend by offering a diverse range of processed food products can tap into a lucrative market segment, driving significant revenue growth.

Latest Trends

Natural and Organic Products

In 2024, the demand for natural and organic products is expected to significantly influence the global FMCG market. Consumers are increasingly prioritizing health and wellness, driving a shift towards products free from synthetic additives, pesticides, and GMOs. This trend is particularly strong among millennials and Gen Z, who are willing to pay a premium for products perceived as healthier and more sustainable. FMCG companies that invest in organic certification, transparent sourcing, and eco-friendly packaging are likely to attract a loyal customer base.

The rise of plant-based diets and clean-label products underscores the need for innovation in this segment. Companies that can successfully develop and market natural and organic offerings will be well-positioned to capture a growing market share.

Tech in Logistics

The integration of advanced technologies in logistics is set to transform the FMCG market in 2024. Innovations such as AI, IoT, and blockchain are enhancing supply chain efficiency, reducing costs, and improving transparency. AI and predictive analytics enable better demand forecasting, inventory management, and route optimization, minimizing waste and ensuring timely delivery. IoT devices provide real-time tracking of goods, ensuring quality control and reducing losses.

Blockchain technology offers traceability and authenticity, addressing consumer concerns about product origins and ethical sourcing. By adopting these technologies, FMCG companies can streamline their operations, reduce their carbon footprint, and enhance customer satisfaction through improved service delivery.

Regional Analysis

Asia-Pacific leads the FMCG market with a 40% share.

The global FMCG market demonstrates significant regional variations, influenced by economic conditions, consumer behavior, and local market dynamics. Asia-Pacific leads the market, commanding a dominant 40% share. This leadership is underpinned by robust economic growth, a burgeoning middle class, and rapid urbanization in countries like China and India. The region’s substantial population base and increasing disposable incomes drive demand for diverse FMCG products, from food and beverages to personal care items.

North America represents a mature FMCG market, characterized by high per capita consumption and advanced retail infrastructure. The U.S. and Canada show strong preferences for health-conscious and convenience-oriented products, reflected in the popularity of organic foods and ready-to-eat meals.

In Europe, the FMCG market is marked by significant diversity, driven by varying consumer preferences across countries. Western Europe, with nations like Germany, France, and the U.K., emphasizes sustainability and premium products, while Eastern Europe sees growth in basic consumption due to rising economic stability.

The Middle East & Africa region is experiencing steady growth in the FMCG sector, propelled by urbanization and an increasing young population. While market penetration varies significantly across the region, countries like the UAE and South Africa show higher consumption rates of FMCG products.

Latin America, with key markets such as Brazil and Mexico, is recovering from economic volatility and is seeing renewed growth in the FMCG sector. The region’s market is driven by a mix of traditional consumption patterns and a gradual shift towards healthier and more convenient product options.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2024, the global Fast-Moving Consumer Goods (FMCG) market continues to be shaped by a combination of innovation, sustainability, and shifting consumer preferences. Key players in this dynamic landscape include The Coca-Cola Company, PepsiCo, Inc., and Nestlé, which remain at the forefront due to their extensive product portfolios and robust distribution networks. These companies are leveraging advanced technologies and data analytics to enhance consumer engagement and streamline supply chains.

The Coca-Cola Company and PepsiCo, Inc. are expected to further their investments in healthier beverage options, responding to the increasing consumer demand for low-sugar and functional drinks. Simultaneously, Nestlé's focus on nutrition, health, and wellness aligns with global trends towards more conscious consumption.

Procter & Gamble and Unilever Group continue to lead in the personal care and home care segments, with their commitment to sustainability and innovation driving growth. Their strategic initiatives in reducing plastic waste and enhancing product efficacy are likely to resonate strongly with environmentally conscious consumers.

Johnson & Johnson and Kimberly-Clark Corporation, key players in the healthcare and hygiene sectors, are poised to benefit from ongoing health awareness post-pandemic. Their continuous product innovations and adherence to high safety standards bolster their market positions.

Patanjali Ayurved Ltd. distinguishes itself with its focus on natural and ayurvedic products, catering to the growing preference for organic and traditional wellness solutions. This differentiator not only strengthens its domestic presence but also enhances its global appeal.

Revlon, Inc., though facing competitive pressures, remains a significant player in the beauty and cosmetics sector, driven by its brand legacy and efforts in digital transformation.

Market Key Players

- The Coca-Cola Company

- Pepper Snapple Group, Inc.

- Johnson & Johnson

- Kimberly-Clark Corporation

- Nestle

- Patanjali Ayurved Ltd.

- PepsiCo, Inc.

- Procter and Gamble

- Revlon, Inc.

- Unilever Group

Recent Development

- In May 2024, Unilever implemented AI-driven inventory management to optimize supply chain efficiency and reduce waste, enhancing overall operational effectiveness.

- In April 2024, Procter & Gamble launched eco-friendly packaging solutions across various product categories, focusing on sustainability and reducing environmental impact.

Report Scope

Report Features Description Market Value (2023) USD 171.9 Bn Forecast Revenue (2033) USD 671.5 Bn CAGR (2024-2033) 15% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Food & Beverage, Health Care, Personal Care, Home Care), , By Distribution Channel (Grocery Stores, Supermarkets & Hypermarkets, E-commerce, Specialty Stores) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape The Coca-Cola Company, Pepper Snapple Group, Inc., Johnson & Johnson, Kimberly-Clark Corporation, Nestle, Patanjali Ayurved Ltd., PepsiCo, Inc., Procter and Gamble, Revlon, Inc., Unilever Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- The Coca-Cola Company

- Pepper Snapple Group, Inc.

- Johnson & Johnson

- Kimberly-Clark Corporation

- Nestle

- Patanjali Ayurved Ltd.

- PepsiCo, Inc.

- Procter and Gamble

- Revlon, Inc.

- Unilever Group

Our Clients

View Our Licence Options