Global Fire Protection System Market By Product(Fire Detection, Fire Suppression, Fire Response, Fire Analysis, Fire Sprinkler System), By Service(Managed Service, Installation and Design Service, Maintenance Service, Others), By Application(Commercial, Industrial, Residential), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48954

-

July 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

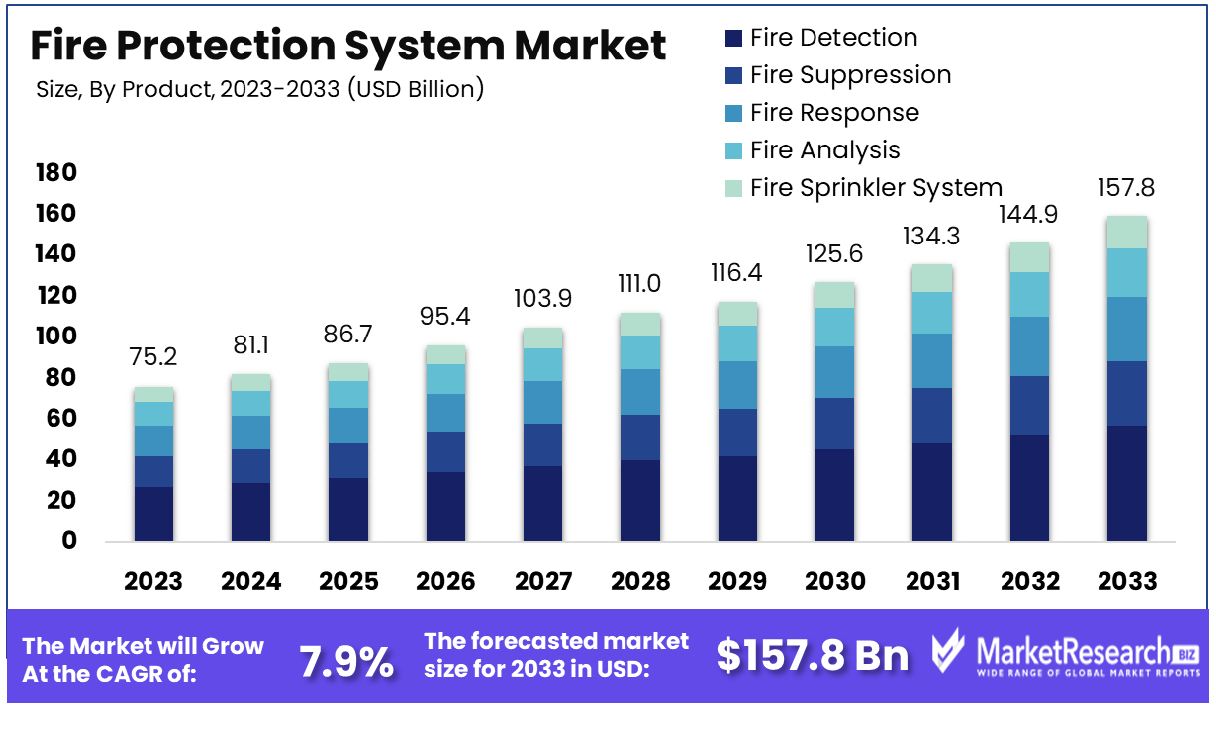

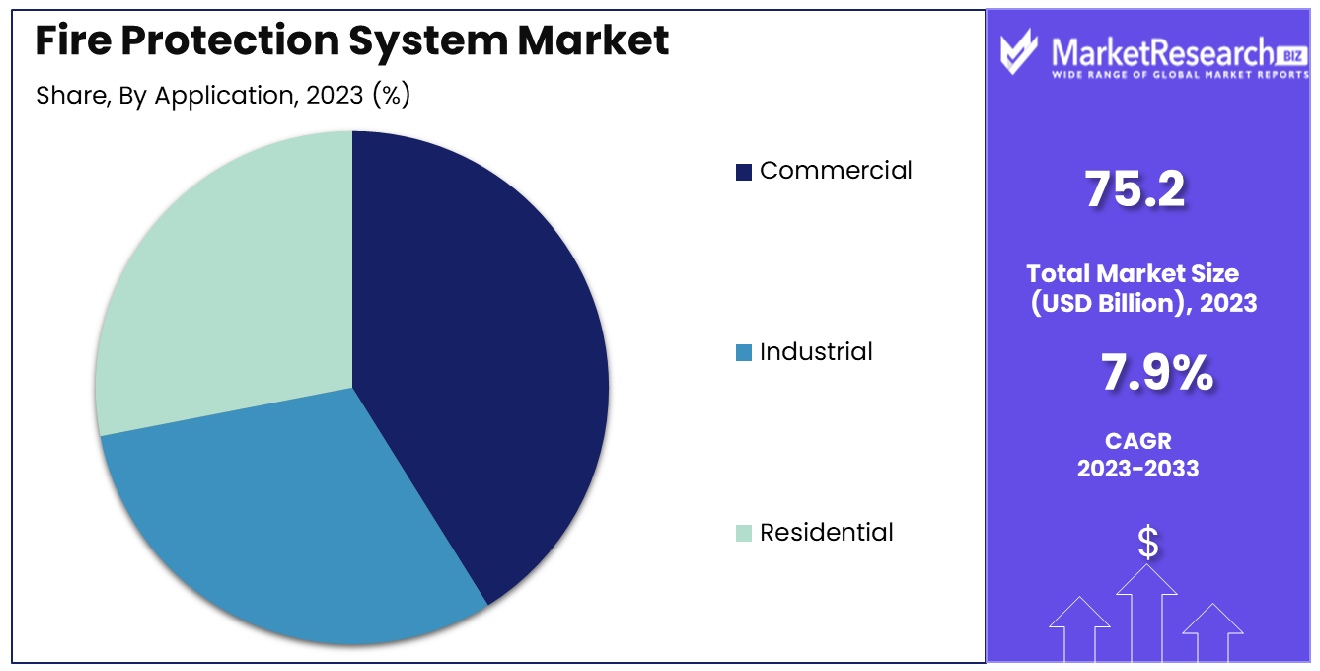

The Global Fire Protection System Market was valued at USD 75.2 billion in 2023. It is expected to reach USD 157.8 billion by 2033, with a CAGR of 7.9% during the forecast period from 2024 to 2033.

The Fire Protection System Market encompasses a comprehensive range of technologies, products, and services dedicated to safeguarding infrastructure and lives from fire hazards. This market includes fire detection devices, such as smoke detectors and flame sensors, fire suppression systems like sprinklers and extinguishers, and integrated fire control and management solutions.

With a focus on innovation and regulatory compliance, the sector caters to various industries, including residential, commercial, and industrial sectors. Strategic advancements and heightened safety standards globally are driving demand, positioning this market as critical for risk management in business continuity planning for executives and decision-makers across verticals.

The Fire Protection System Market is positioned for robust growth, propelled by advancing technology and stringent regulatory mandates worldwide. Despite a 4.8% decline in incidents attended by fire and rescue services as reported by recent government data for the year ending September 2023, the market is buoyed by rising concerns over asset safety and human life protection. This decline in incidents paradoxically underscores the effectiveness of existing fire protection systems, supporting market growth as businesses and government entities continue to invest in these critical systems.

Conversely, the same dataset highlights a 3.1% increase in false alarms compared to the previous year, pointing towards a significant area of improvement within the market. This increase in false alarms not only indicates potential over-sensitivities in current systems but also represents an opportunity for innovation in fire detection technologies, driving demand for more sophisticated and accurate systems. Such advancements could lead to higher adoption rates and greater market penetration, especially in sectors where precision is paramount.

Key Takeaways

- Market Growth: The Global Fire Protection System Market was valued at USD 75.2 billion in 2023. It is expected to reach USD 157.8 billion by 2033, with a CAGR of 7.9% during the forecast period from 2024 to 2033.

- By Product: Fire Detection dominated with a commanding 40% market share.

- By Service: Managed Service led the market with a 35% share.

- By Application: Commercial applications dominated, capturing a significant 50% share.

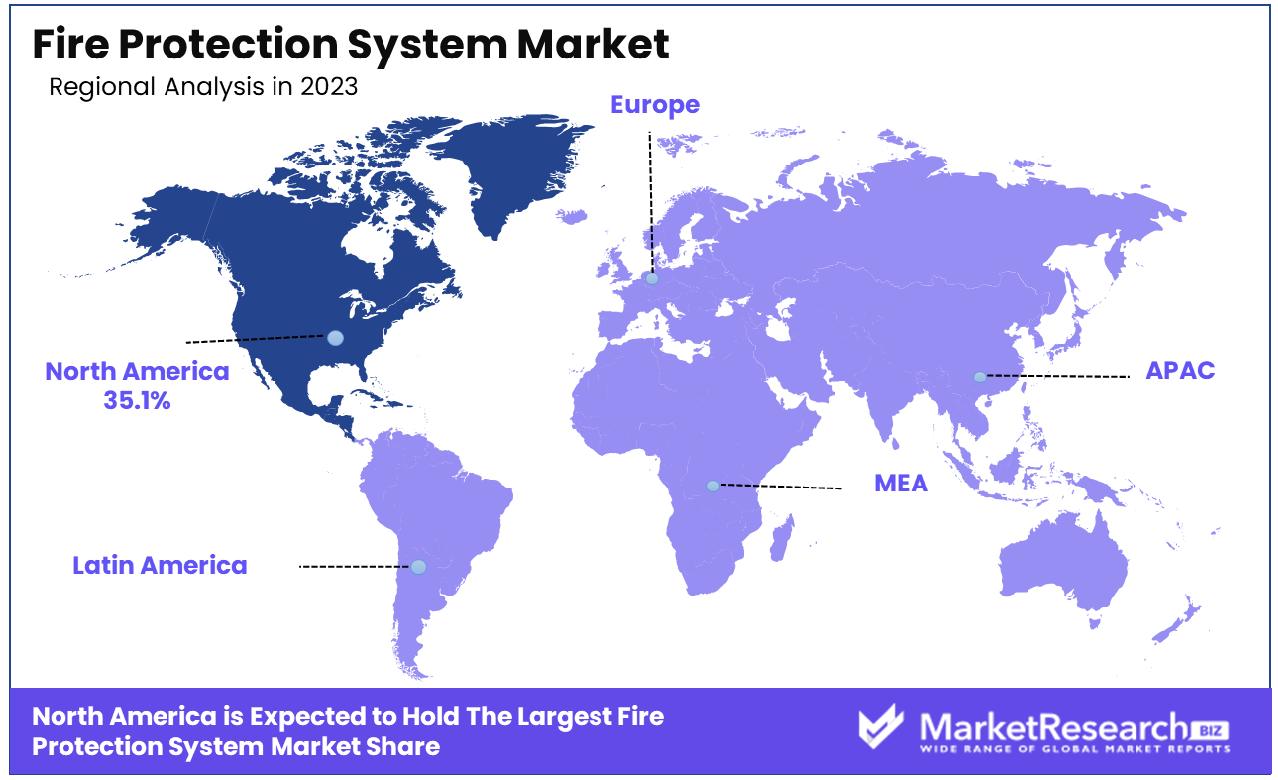

- Regional Dominance: North America holds a significant share of 35.1% in the Fire Protection System Market as of the latest analysis.

Driving factors

Enhanced Regulatory Focus and Stringent Safety Standards

The increasing global emphasis on safety regulations is a pivotal driver for the Fire Protection System Market. Governments worldwide are enforcing stricter safety standards and building codes that mandate the installation and maintenance of advanced fire protection systems.

This regulatory push ensures that fire protection is not just an option but a compulsory element of architectural design, particularly in public spaces and industries such as healthcare, hospitality, and education. These regulations also extend to residential areas, significantly broadening the market scope and necessitating regular updates and technological upgrades in existing systems.

Urbanization and Infrastructure Expansion

Rising urbanization is closely linked to the expansion of infrastructure, both of which significantly contribute to the growth of the Fire Protection System Market. As urban areas expand, the density of population and property increases the potential risk and consequences of fire incidents.

This necessitates comprehensive fire safety solutions that are integrated into the development of new commercial, industrial, and residential buildings. Infrastructure projects, especially in emerging economies, are incorporating advanced fire safety systems early in the construction phase, fostering market expansion and technological integration.

Technological Innovations in Fire Safety Systems

Advancements in technology are dramatically transforming the Fire Protection System Market. Innovations in fire detection and suppression technologies are making systems more efficient, reliable, and capable of addressing the unique challenges of modern infrastructures. Smart fire safety systems, which leverage IoT, artificial intelligence, and data analytics, are becoming more prevalent.

These systems offer predictive insights, real-time monitoring, and automated responses, enhancing safety measures and operational efficiencies. The integration of these technologies not only improves system performance but also drives down the long-term costs associated with fire safety management and insurance, investing in these technologies increasingly attractive to businesses and property managers.

Restraining Factors

Economic Constraints: High Installation and Maintenance Costs

The economic burden associated with the installation and ongoing maintenance of advanced fire protection systems significantly restrains market growth. These systems often involve sophisticated technologies that require not only a higher initial capital investment but also ongoing expenses related to maintenance, testing, and compliance with evolving standards.

For many businesses, particularly small to medium enterprises and those in developing regions, these costs can be prohibitively high, limiting the adoption of the latest innovations in fire safety technology. This economic hurdle is a major factor slowing down the rate at which new fire protection technologies are embraced across the market.

Technical Challenges: Integrating Legacy Systems with Modern Technologies

Another major restraining factor is the complexity involved in integrating legacy fire safety systems with modern technologies. Many existing buildings and facilities are equipped with older fire protection systems that are not readily compatible with the newest innovations, such as IoT-enabled devices and smart control systems.

Upgrading these systems often requires substantial retrofitting or complete overhauls, which can be both costly and disruptive to operations. The challenge of integration not only adds to the financial burden but also complicates the technical execution, posing a significant barrier to the widespread adoption of advanced fire protection technologies.

By Product Analysis

Fire Detection dominated with a commanding 40% share due to its critical safety role.

In 2023, Fire Detection held a dominant market position in the By Product segment of the Fire Protection System Market, capturing more than a 40% share. This segment benefits from continuous technological advancements and the increasing integration of IoT, which enhances the effectiveness and connectivity of fire detection systems. These systems are crucial for the early identification of fire-related incidents, thereby allowing for timely intervention and minimizing potential damage and loss of life.

Following closely, the Fire Suppression segment also plays a significant role in the market. This segment includes a range of products such as fire extinguishers and specialized suppression systems that are used to control and extinguish fires once detected. The adoption of environmentally friendly fire suppression agents is a key trend within this segment, reflecting growing regulatory and consumer demand for sustainable practices.

The Fire Response segment, which includes emergency service notifications and evacuation management systems, integrates closely with fire detection and suppression technologies to enhance the overall effectiveness of fire safety measures. The synergy between these segments ensures a comprehensive approach to fire safety, from detection to suppression and response.

Additionally, the Fire Analysis segment is gaining traction due to its role in utilizing data collected from fire incidents to improve future fire safety measures and technologies. This segment's growth is fueled by advancements in data analytics and AI, which are used to predict fire risks and optimize fire protection strategies.

Lastly, the Fire Sprinkler System segment continues to be essential in both residential and commercial buildings. The widespread adoption of these systems is driven by their proven efficacy in controlling fires, supported by stringent building codes and safety regulations that mandate their installation in new constructions and renovations.

By Service Analysis

Managed Service led with 35%, reflecting the shift towards outsourced fire safety management.

In 2023, Managed Service held a dominant market position in the By Service segment of the Fire Protection System Market, capturing more than a 35% share. This segment encompasses comprehensive solutions that include the ongoing management, monitoring, and optimization of fire protection systems. The growing complexity of fire safety technologies and the need for compliance with stringent regulatory standards drive the demand for managed services, as they ensure systems are not only effectively implemented but also maintained at peak operational status.

Installation and Design Service also plays a crucial role in the market. This segment deals with the initial setup and design of fire protection systems, tailored to meet the specific requirements of different buildings and facilities. As new construction projects continue to rise, especially in emerging markets, the demand for specialized installation and design services that incorporate the latest technologies and compliance measures is expected to grow.

Maintenance Service follows closely, underlining the importance of regular inspections, repairs, and updates to fire safety systems to ensure their functionality over time. Maintenance is critical not only for safety but also for compliance with fire safety regulations, which often require documented evidence of regular system checks and maintenance.

The "Others" category encompasses various ancillary services that support the fire protection system market, including training, consulting, and upgrade services. These services are integral to ensuring that the systems are not only designed and maintained properly but also used effectively by building management and safety personnel.

By Application Analysis

Commercial sectors dominated at 50%, driven by stringent safety regulations and infrastructure demands.

In 2023, the Commercial sector held a dominant market position in the By Application segment of the Fire Protection System Market, capturing more than a 50% share. This dominance is primarily due to the extensive deployment of advanced fire protection systems across various commercial facilities, including office buildings, shopping centers, and entertainment venues. The high traffic and the valuable assets within these establishments necessitate robust fire safety measures, driving significant investments in both traditional and cutting-edge fire safety technologies.

The Industrial sector also represents a significant portion of the market. In industries such as manufacturing, oil and gas, and chemicals, where the risk of fire is inherently higher, fire protection systems are critical. These environments often require specialized solutions that can handle the unique hazards they present, such as flammable materials and high-temperature processes. The focus in this segment is on integrating highly responsive fire detection and suppression systems that can prevent catastrophic damage and ensure continuity of operations.

Lastly, the Residential sector is experiencing steady growth, spurred by increasing awareness of fire safety and stricter regulations mandating the installation of fire protection systems in homes. Developments in affordable and easy-to-install fire alarms and smoke detectors are particularly appealing to the residential market, making it easier for homeowners to equip their properties with essential fire safety measures. This trend is further bolstered by the rising number of residential construction projects, especially in urban areas, contributing to the overall expansion of the fire protection system market in the residential sector.

Key Market Segments

By Product

- Fire Detection

- Fire Suppression

- Fire Response

- Fire Analysis

- Fire Sprinkler System

By Service

- Managed Service

- Installation and Design Service

- Maintenance Service

- Others

By Application

- Commercial

- Industrial

- Residential

Growth Opportunity

Strategic Expansion into Emerging Markets

The year 2023 presents significant growth opportunities for the Fire Protection System Market, particularly through strategic expansion into emerging markets. These regions are experiencing rapid urbanization and extensive new construction projects that require state-of-the-art fire protection solutions. Emerging economies in Asia, Africa, and Latin America are seeing a surge in both residential and commercial construction activities, driven by population growth and economic development.

By entering these markets, companies can tap into new customer bases that are currently underserved, offering tailored solutions that meet the specific needs and regulations of these diverse regions. Furthermore, government initiatives and infrastructure investments in these countries provide a conducive environment for the adoption of advanced fire safety systems, making them attractive targets for market expansion.

Advancements in Smart and Integrated Fire Protection Systems

Another major growth avenue in 2023 is the development and deployment of smart and integrated fire protection systems. The industry is moving towards more sophisticated systems that not only detect and suppress fires but also predict and prevent them through the use of AI, IoT, and big data analytics. These smart-systems can communicate with other building management systems, providing holistic safety solutions that are more efficient and effective.

The integration of these technologies enhances the responsiveness and reliability of fire protection systems, offering substantial improvements over traditional methods. As buildings become smarter, the demand for interconnected fire safety solutions that can seamlessly integrate into these environments increases, representing a substantial growth opportunity for industry players. These advancements not only meet the current demands of modern infrastructure but also set the stage for future innovation in fire safety technology.

Latest Trends

IoT Adoption for Enhanced Connectivity and Monitoring

In 2023, the global Fire Protection System Market is witnessing a significant trend towards the adoption of the Internet of Things (IoT) to enhance system connectivity and real-time monitoring capabilities. IoT technology integrates fire safety components into a unified network, allowing for seamless communication between devices. This connectivity facilitates the continuous monitoring of environmental conditions, enabling systems to detect and respond to fire hazards more swiftly and accurately.

Furthermore, IoT allows for the collection of large volumes of data, which can be analyzed to predict potential fire outbreaks, optimize maintenance schedules, and improve overall system performance. The adoption of IoT not only increases the effectiveness of fire protection systems but also enhances operational efficiency, providing a compelling value proposition for businesses and safety regulators looking to leverage technology to bolster fire safety measures.

Rise of Environmentally Friendly Fire Suppression Agents

Concurrently, there is an increasing trend toward the use of environmentally friendly fire suppression agents within the Fire Protection System Market. Traditional fire suppression chemicals, while effective, often carry significant environmental risks, including ozone depletion and high global warming potential. In response, the market is shifting towards agents that have minimal environmental impact, such as water mist systems, and fluorine-free foam. These green alternatives provide effective fire suppression while supporting sustainability goals, appealing to a growing segment of eco-conscious consumers and enterprises.

Regulatory pressures and increasing environmental awareness are driving the adoption of these agents, positioning them as a key trend that not only addresses safety concerns but also aligns with global sustainability efforts. This shift is expected to gain further momentum as more companies and regulations move towards environmentally responsible fire safety solutions.

Regional Analysis

North America holds a commanding share of 35.1% in the Fire Protection System Market as of the latest report.

The Fire Protection System Market exhibits distinct characteristics and growth trajectories across various global regions, with North America emerging as the dominant market, accounting for 35.1% of the global share. This region's leadership is driven by rigorous regulatory standards, a high degree of technological adoption, and substantial investments in infrastructure safety.

In contrast, Europe follows closely, leveraging advanced technology and stringent EU regulations that mandate the installation of fire safety systems across new and renovated structures, thereby fostering a proactive fire safety culture.

Asia Pacific is experiencing rapid growth in the fire protection system market, spurred by urbanization, industrialization, and heightened awareness of fire safety. This region benefits from significant construction activities, particularly in China and India, where government initiatives to enhance building safety are in place. The market is expanding due to increasing investments in smart city projects that integrate advanced fire safety technologies.

Meanwhile, the Middle East & Africa region is gradually advancing, with growth driven by infrastructure developments and the oil & gas sector, which demands highly reliable fire safety systems due to its inherent risk profile. Latin America, though smaller in comparison, shows growth potential, influenced by urban development and industrial safety regulations.

Each region's market dynamics are shaped by local regulations, technological penetration, and specific industrial demands, making regional strategies pivotal for companies aiming to capitalize on the diverse opportunities within the global Fire Protection System Market.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Fire Protection System Market remains highly competitive, with key players such as Eaton, GENTEX CORPORATION, Halma plc, Hitachi Ltd., Honeywell International, Inc., Iteris, Inc., Johnson Controls, Raytheon Technologies Corporation, Robert Bosch GmbH, and Siemens AG leading the charge. These companies are at the forefront of innovation, integrating cutting-edge technologies into their offerings to enhance the efficacy and reliability of fire protection systems.

Eaton and Siemens AG are particularly notable for their comprehensive portfolios that span various components of fire safety, including detection, alarm systems, and suppression solutions. These firms are advancing fire safety through smart technologies that not only improve response times but also minimize false alarms, which are a significant issue highlighted by recent data.

Honeywell International, Inc. and Johnson Controls are driving the integration of Internet of Things (IoT) capabilities into fire safety systems, facilitating real-time monitoring and data analytics to predict and prevent fire incidents before they escalate. Their focus on creating interconnected systems aligns with the growing demand for smarter, more autonomous safety solutions in both residential and commercial buildings.

Meanwhile, companies like GENTEX CORPORATION and Halma plc are enhancing their product offerings with innovative fire detection technologies that provide greater accuracy and faster detection times. This technological edge is crucial in maintaining competitiveness in a market that is increasingly driven by regulatory compliance and technological advancement.

The collective efforts of these companies are not only expanding the technological boundaries of fire protection systems but also shaping the strategic landscape of the market, ensuring that safety remains a paramount concern across industries worldwide.

Market Key Players

- Eaton

- GENTEX CORPORATION

- Halma plc

- Hitachi Ltd.

- Honeywell International, Inc.

- Iteris, Inc.

- Johnson Controls

- Raytheon Technologies Corporation

- Robert Bosch GmbH

- Siemens AG

Recent Development

- In May 2024, Eaton, a global power management company, launched an advanced fire protection system designed for commercial buildings. This new system integrates smart technology to provide real-time monitoring and faster response times. Eaton aims to enhance safety and efficiency in fire protection through this innovative solution.

- In April 2024, GENTEX CORPORATION, known for its safety products, introduced a new line of smoke detectors featuring enhanced sensitivity and reliability. These detectors are aimed at both residential and commercial markets. GENTEX CORPORATION's commitment to safety innovation is evident in its continuous product improvements.

- In February 2024, Hitachi Ltd., a Japanese multinational conglomerate, secured a $100 million funding round to develop next-generation fire protection systems. Hitachi's new systems will incorporate advanced AI and IoT technologies to improve detection and response times. This funding round highlights Hitachi's dedication to innovation in fire safety.

Report Scope

Report Features Description Market Value (2023) USD 75.2 Billion Forecast Revenue (2033) USD 157.8 Billion CAGR (2024-2032) 7.9% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Fire Detection, Fire Suppression, Fire Response, Fire Analysis, Fire Sprinkler System), By Service(Managed Service, Installation and Design Service, Maintenance Service, Others), By Application(Commercial, Industrial, Residential) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Eaton, GENTEX CORPORATION, Halma plc, Hitachi Ltd., Honeywell International, Inc., Iteris, Inc., Johnson Controls, Raytheon Technologies Corporation, Robert Bosch GmbH, Siemens AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Eaton

- GENTEX CORPORATION

- Halma plc

- Hitachi Ltd.

- Honeywell International, Inc.

- Iteris, Inc.

- Johnson Controls

- Raytheon Technologies Corporation

- Robert Bosch GmbH

- Siemens AG

Our Clients

View Our Licence Options