Encryption Software Market By Component (Software,Services), By Deployment Mode(On-premise, Cloud), By Services(Professional Services, Managed Services), By Enterprise Size(Large Enterprise,S mall and Medium-sized Enterprises), By Function (Disk Encryption, Communication Encryption, and Others ), By Industry Vertical (BFSI,IT and Telecom, and Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51345

-

Sept 2024

-

285

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Report Overview

- Key Takeaways

- Driving Factors

- Restraining Factors

- By Component Analysis

- By Deployment Mode Analysis

- By Services Analysis

- By Enterprise Size Analysis

- By Function Analysis

- By Industry Vertical Analysis

- Key Market Segments

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

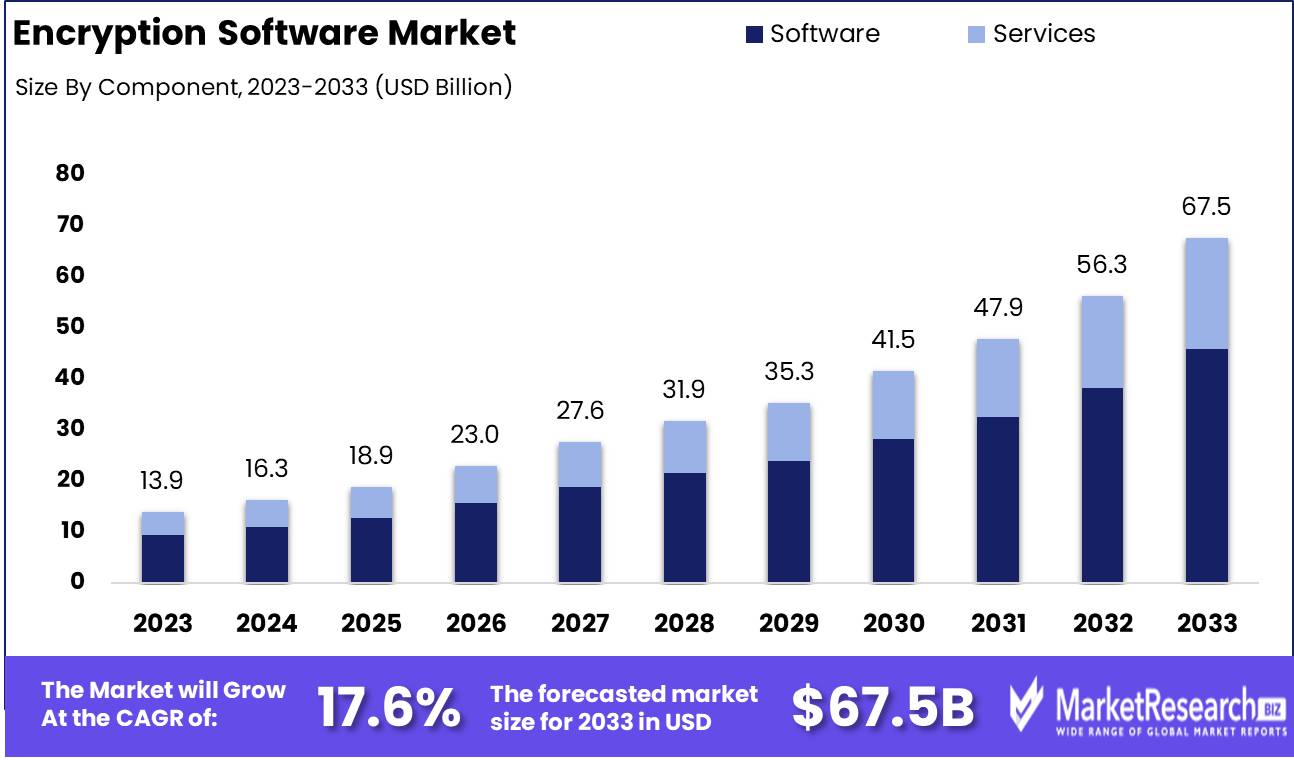

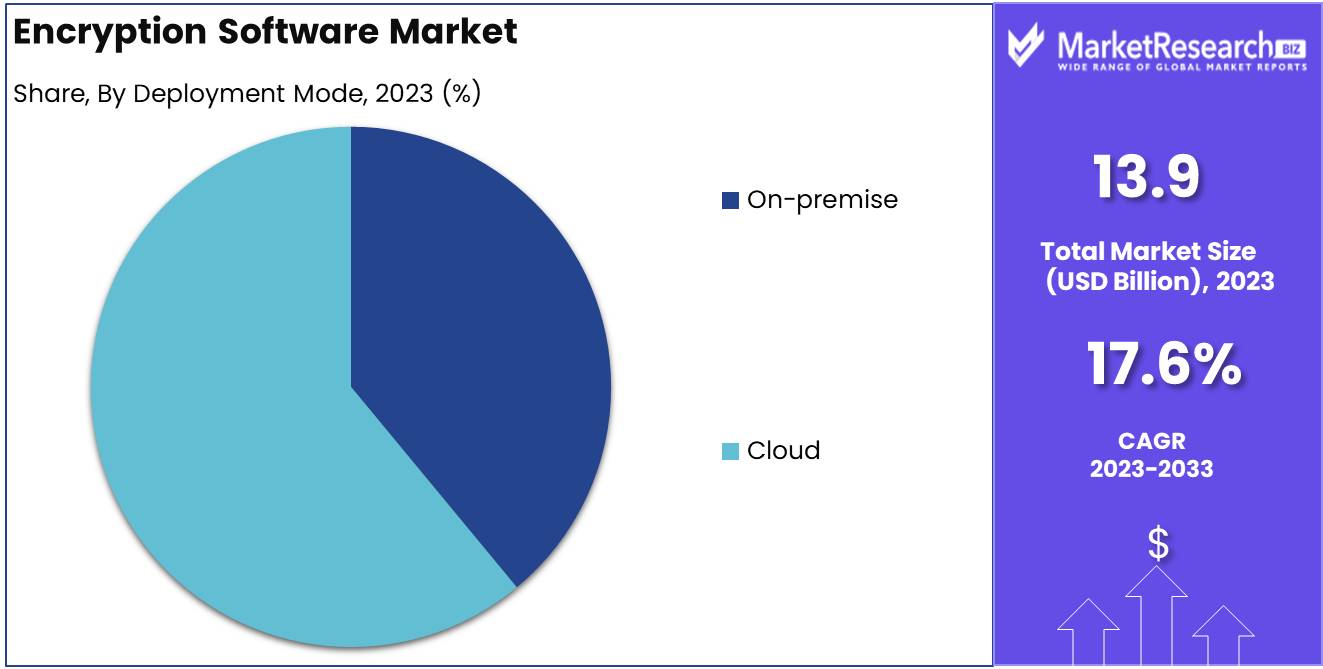

The Encryption Software Market was valued at USD 13.9 billion in 2023. It is expected to reach USD 67.5 billion by 2033, with a CAGR of 17.6% during the forecast period from 2024 to 2033.

The Encryption Software Market encompasses technologies designed to secure digital data by converting it into unreadable formats, which can only be deciphered with specific decryption keys. Essential in protecting sensitive information against unauthorized access, this market serves various industries, including finance, healthcare, and government. As cyber threats evolve, the demand for robust encryption solutions grows, prompting advancements in encryption algorithms and user-friendly software interfaces. Market growth is further fueled by stringent regulatory compliance requirements for data protection worldwide, making encryption software an indispensable component of modern cybersecurity strategies.

The global encryption software market is witnessing rapid growth, driven by increasing concerns over data security, the rise of quantum computing threats, and the expanding regulatory landscape. With sensitive data becoming more valuable and vulnerable, industries such as finance, healthcare, and regulated sectors are heavily investing in advanced encryption technologies to mitigate risks associated with cyberattacks and data breaches. A significant shift in the market has been the growing adoption of quantum-safe encryption techniques, particularly Quantum Key Distribution (QKD).

By 2024, the quantum encryption market is expected to reach approximately $5 billion, underscoring the urgency for organizations to adopt encryption solutions that are resilient against emerging quantum threats. Furthermore, the rise in bring-your-own-device (BYOD) policies and the proliferation of IoT devices have intensified the need for robust encryption strategies to safeguard corporate networks from potential vulnerabilities.

Recent industry developments underscore the strategic importance of encryption as a core component of IT security. In April 2023, Utimaco’s acquisition of Conpal GmbH highlights how firms are enhancing their encryption portfolios, particularly in regulated industries like finance and healthcare, where public key infrastructure (PKI) plays a critical role. Similarly, Accenture’s July 2024 partnership with SandboxAQ aims to address the threats posed by AI and quantum technologies, focusing on improving data encryption, observability, and resilience.

These collaborations reflect an increasing trend where enterprises are preparing for the next wave of cyber threats driven by advanced technologies. Additionally, Cisco’s acquisition of Splunk for $28 billion, completed in September 2023, is set to bolster its cybersecurity and observability offerings, further integrating AI-driven threat prediction and prevention capabilities. The launch of Arqit WalletSecure by Arqit Quantum Inc. in 2023 also signifies the growing convergence of quantum technology with encryption solutions, particularly in sectors like banking, where secure key management is paramount. These developments indicate a clear trajectory towards a more secure, quantum-resilient encryption ecosystem, with key players positioning themselves to meet rising demand in a highly regulated and rapidly evolving threat landscape.

Key Takeaways

- Market Growth: The Encryption Software Market is poised for robust expansion, set to reach USD 67.5 billion by 2033, driven by a CAGR of 17.6% from 2024 to 2033.

- Analyst Viewpoint Summary: Encryption software is critical in addressing the complexities of modern cybersecurity, with growing investments in advanced technologies and compliance driving market growth.

- By Component: The software segment dominates the Encryption Software Market, holding over 68.1% of the market share, underlining its pivotal role in global data security efforts.

- By Deployment Mode: Cloud-based encryption solutions lead the deployment modes with a 61.2% market share, reflecting their increasing adoption due to scalability and cost efficiency.

- By Services: Managed Services dominate the services segment, capturing more than 55.2% of the market, highlighting their importance in managing complex encryption needs.

- By Enterprise Size: Large Enterprises hold a dominant position in the enterprise size segment with over 64% market share, primarily due to their extensive IT infrastructures and higher compliance requirements.

- Regional Growth: North America leads the global encryption software market with a 39.1% share in 2024, driven by stringent compliance requirements and advanced technology adoption.

- Growth Opportunity (IoT and 5G Networks): The expansion of IoT devices and deployment of 5G networks are key drivers, necessitating robust encryption to secure vast, fast-transmitting networks.

- Restraining Factor (High Implementation Costs): The significant costs associated with encryption software implementation pose barriers, particularly for SMEs and emerging markets, potentially hindering widespread adoption.

Driving Factors

Mobile Device Security

The rapid proliferation of mobile devices has become a central factor in the growth of the encryption software market. With an increasing number of businesses and individuals relying on smartphones and tablets for sensitive communications, financial transactions, and data storage, the need for robust mobile security has surged. The rise of mobile-first workplaces, combined with remote work trends accelerated by the COVID-19 pandemic, has led to a significant increase in mobile device vulnerability.

According to a 2023 report by Lookout, mobile phishing attacks have risen by 37%, highlighting the pressing need for advanced encryption solutions to protect sensitive data. Mobile applications now transmit and store vast amounts of corporate and personal data, making encryption vital to safeguarding against cyber threats such as data breaches, ransomware, and phishing attacks.

Encryption software is crucial to securing not just mobile devices but also the apps and networks they connect to. With mobile operating systems like Android and iOS integrating more sophisticated encryption features, there is a complementary rise in demand for third-party encryption tools to offer enhanced, enterprise-level protection. The interoperability between mobile device security and broader IT security frameworks ensures that encryption software remains indispensable in protecting data across both personal and enterprise devices, further bolstering market expansion.

Cloud Adoption

As businesses increasingly migrate their data, applications, and infrastructure to cloud platforms, the need for effective encryption solutions has become paramount. Cloud adoption has grown exponentially, with Study predicting that global spending on public cloud services will reach $591.8 billion by 2023. This shift to the cloud has heightened concerns about data privacy, compliance with regulatory standards (such as GDPR and HIPAA), and protection against unauthorized access.

Encryption software plays a crucial role in securing data in transit and at rest within cloud environments, ensuring that sensitive information remains protected even if cloud infrastructure is compromised. The flexibility and scalability of cloud services have prompted businesses to adopt encryption tools that can integrate seamlessly across hybrid and multi-cloud environments.

The convergence of cloud adoption with rising data privacy regulations has amplified the need for advanced encryption strategies. Companies are increasingly prioritizing encryption to comply with industry-specific regulations and meet the rising expectations of stakeholders for secure data handling. Encryption-as-a-Service (EaaS) has emerged as a growing sub-sector, allowing businesses to deploy encryption with minimal operational overhead, which is expected to further boost market growth.

By driving demand for scalable, high-performance encryption solutions, cloud adoption is not only expanding the encryption software market but also creating opportunities for innovation in secure data management across industries. As companies increasingly depend on cloud infrastructure, encryption software will remain an integral part of their cybersecurity strategy.

Restraining Factors

High Cost of Implementation: Barrier to Adoption in Emerging Markets

The high cost of implementing encryption software acts as a significant barrier to entry for small to medium enterprises (SMEs) and organizations in emerging markets. This factor often restrains market expansion by limiting adoption rates among these entities, which are typically more sensitive to initial investment costs. The expense associated with advanced encryption technologies, including the need for hardware and professional services for deployment and maintenance, contributes to higher overall costs.

This cost factor can interplay with the rapid advancements in technology that require frequent updates and investments, potentially slowing down the adoption rate. However, it also encourages the development of cost-effective solutions by vendors aiming to penetrate these untapped markets, thus driving innovation and ultimately contributing to market growth in the long term.

Use of Pirated and Open-Source Encryption Solutions

The availability and use of pirated and open-source encryption solutions present a dual-edged sword in the encryption software market. On one hand, these solutions can limit the revenue growth for established encryption software vendors by offering low-cost or free alternatives to proprietary software. On the other hand, the widespread use of open-source solutions can promote a broader understanding and integration of encryption, raising overall market awareness and potentially increasing the demand for professional, secure, and compliant encryption solutions for enterprise use.

The use of non-commercial solutions often lacks the support, updates, and compliance assurances that come with licensed software, which can pose significant risks in terms of data breaches and non-compliance with regulations like GDPR. This situation drives a need for robust, commercial encryption solutions that are regularly updated to counteract emerging threats. As awareness of these risks grows, organizations are likely to transition from open-source to commercial products, particularly in industries where data security is paramount. This shift underscores a growing market segment that demands advanced, compliant, and secure encryption solutions, thus catalyzing growth within the industry.

By Component Analysis

In 2023, Software held a dominant market position within the By Component segment of the Encryption Software Market, capturing more than 68.1% share.

This significant share highlights the increasing reliance on encryption software solutions as enterprises and governments prioritize data security amidst rising cyber threats. The demand for robust encryption tools across industries such as BFSI, healthcare, and IT has fueled the rapid adoption of software-based encryption technologies.

Software solutions have become the backbone of modern encryption systems, offering flexibility, scalability, and integration capabilities that address the growing complexities of data protection. This segment includes comprehensive encryption platforms that safeguard sensitive information at various touchpoints, such as data at rest, in transit, and during transactions. The constant development of advanced encryption algorithms and seamless cloud integration features further strengthens the market's dependence on encryption software.

In contrast, Services accounted for a smaller yet steadily growing portion of the market. These services, including implementation, consulting, and managed services, are critical in supporting the deployment and ongoing maintenance of encryption solutions. As organizations continue to navigate regulatory frameworks and data privacy laws, the role of specialized services in ensuring compliance and optimizing encryption performance is expected to grow in the coming years.

While the Software segment's dominance is expected to persist, the rising complexity of encryption deployments and increasing regulatory scrutiny may fuel growth in the Services segment, driving a more balanced market share distribution over time.

By Deployment Mode Analysis

In 2023, Cloud lead the by Deployment Mode segment of the Encryption Software Market, holding the largest market share at 61.2%.

The Cloud deployment mode saw widespread adoption, driven by its scalability, cost-efficiency, and enhanced accessibility. Organizations across various industries, particularly in finance, healthcare, and technology, increasingly preferred cloud-based encryption solutions due to the rising need for securing data in transit and at rest in remote and hybrid work environments. As cloud infrastructure continues to mature, the integration of encryption-as-a-service (EaaS) and cloud-native security tools has further solidified its position in the market.

Conversely, On-premise deployment, while still prevalent in sectors with stringent regulatory and compliance requirements such as government and defense saw a gradual decline in market share. The on-premise segment continues to cater to organizations with legacy infrastructure or those prioritizing direct control over their encryption protocols. However, the need for high upfront investment and operational complexity has restricted its growth, with a noticeable shift toward hybrid solutions where on-premise systems are integrated with cloud environments.

Looking forward, the cloud segment is projected to sustain its dominance as organizations increasingly prioritize agility and data security amid growing cybersecurity threats and evolving regulatory landscapes. This shift reflects broader market trends toward cloud-first strategies, digital transformation, and zero-trust security models.

By Services Analysis

In 2023, Managed Services held a dominant market position within the "By Services" segment of the Encryption Software Market, capturing more than 55.2% of the total market share.

This segmental growth reflects the increasing reliance on outsourced solutions for encryption management, which enable organizations to mitigate security risks while reducing the burden on internal IT teams. Managed Services offer comprehensive solutions, including encryption deployment, monitoring, and maintenance, providing scalability and cost efficiency for enterprises seeking to safeguard their data in an evolving threat landscape.

The Managed Services segment, as noted, accounted for the largest share in 2023. The key factors driving this dominance include the rising complexity of data encryption requirements and the growing need for continuous protection against advanced cyber threats. Organizations across industries are prioritizing the outsourcing of encryption services to managed service providers (MSPs) for access to specialized expertise, enhanced security infrastructure, and round-the-clock monitoring. This outsourcing model is particularly attractive to small and medium-sized enterprises (SMEs) that may lack the internal resources to handle increasingly sophisticated encryption demands.

While Managed Services lead the market, Professional Services also constitute a critical part of the Encryption Software Market, encompassing consulting, implementation, training, and support services. Professional Services are essential for enterprises needing expert guidance in encryption strategy development, system integration, and regulatory compliance. Although this segment's growth rate trails Managed Services, the demand for consultancy services remains robust, particularly in sectors requiring custom encryption solutions tailored to specific security and regulatory environments, such as healthcare, finance, and government.

The ongoing expansion of the encryption software market, coupled with increasing concerns over data breaches and privacy, suggests that the Managed Services segment will likely continue its market leadership. However, Professional Services will remain integral for firms requiring tailored solutions and ongoing advisory support to meet industry-specific encryption needs.

By Enterprise Size Analysis

In 2023, Large Enterprise held a dominant market position within the By Enterprise Size segment of the Encryption Software Market, capturing more than 64% of the total market share.

This can be attributed to the increased adoption of encryption software driven by the need for advanced data protection across extensive and complex IT infrastructures. Large enterprises, typically with higher levels of data storage, more significant risk exposure, and stringent compliance requirements, are increasingly prioritizing encryption solutions to safeguard sensitive information against cyber threats and ensure regulatory compliance.

In contrast, Small and Medium-sized Enterprises (SMEs) accounted for the remaining share in this segment but have exhibited growing interest in encryption solutions. The rise of cloud services, digital transformation, and an increasing number of cyberattacks have driven SMEs to adopt encryption technologies, although budget constraints and limited in-house technical expertise have historically been barriers. However, with the proliferation of affordable and scalable encryption tools, SMEs are expected to witness increased adoption rates, potentially accelerating their market share growth over the coming years.

By Function Analysis

In 2023, Disk Encryption held a dominant market position within the By Function segment of the Encryption Software Market, capturing more than 36% of the total market share.

This significant share reflects the increasing demand for securing entire hard drives and storage devices, particularly as organizations prioritize comprehensive data protection against unauthorized access. Disk encryption is particularly critical for industries handling sensitive information, such as finance, healthcare, and government, where compliance and data security standards necessitate robust, end-to-end encryption solutions.

Communication Encryption followed closely, as businesses face heightened cybersecurity risks associated with real-time data exchange across various channels, such as emails, instant messaging, and voice-over-IP (VoIP) communications. The growing prevalence of remote work and cloud-based communication tools has further spurred the adoption of communication encryption, driving demand for secure transmission protocols.

File/Folder Encryption captured a significant portion of the market as well, with businesses increasingly adopting this technology to encrypt specific files and folders, allowing for granular control over data access. This segment has gained traction due to the need for protecting sensitive files shared within and outside organizations, particularly in regulated industries.

Finally, Cloud Encryption is rapidly emerging as a critical component in this segment, driven by the accelerated adoption of cloud computing and the need to protect data stored in cloud environments. While currently holding a smaller market share compared to disk and communication encryption, cloud encryption is expected to experience robust growth as businesses migrate more of their operations to cloud infrastructures and prioritize the security of cloud-stored data.

By Industry Vertical Analysis

In 2023, BFSI held a dominant market position in the By Industry Vertical segment of the Encryption Software Market, capturing more than a 26% share.

This substantial market share is attributed to the increasing need for data privacy and compliance with stringent regulatory requirements in the financial sector. Financial institutions are increasingly adopting encryption solutions to protect sensitive information against cyber threats and breaches, driving significant growth in this segment.

The IT and Telecom sector also showed notable adoption, reflecting the industry's expanding necessity to secure data transmissions and safeguard communications. The push towards digital transformation and cloud-based solutions has particularly underscored the importance of encryption in protecting data integrity and privacy.

Government and Public Sector entities have similarly invested in encryption technologies, driven by the need to secure sensitive government data and protect national security interests. This sector's emphasis on encryption is also motivated by the rising threats of cyber espionage and data leaks.

Retail organizations are increasingly adopting encryption solutions to protect consumer data and maintain customer trust, especially in the face of growing online transactions and e-commerce platforms.

The Healthcare sector's use of encryption is crucial for protecting patient information, complying with health data regulations such as HIPAA in the United States, and ensuring the confidentiality and integrity of health records.

Aerospace and Defense industry's adoption of encryption technologies is critical for securing highly sensitive defense-related communications and data, with national security being a paramount concern.

In the Media and Entertainment sector, encryption is utilized to safeguard digital content from unauthorized access and piracy, protecting intellectual property rights and revenue streams.

Other industries, including manufacturing, education, and energy, are progressively recognizing the importance of data encryption to mitigate risks associated with intellectual property theft and industrial espionage.

This diverse adoption across various industry verticals highlights the pervasive recognition of encryption's role as a fundamental component of contemporary cyber defense strategies.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- On-premise

- Cloud

By Services

- Professional Services

- Managed Services

By Enterprise Size

- Large Enterprise

- Small and Medium-sized Enterprises

By Function

- Disk Encryption

- Communication Encryption

- File/Folder Encryption

- Cloud Encryption

By Industry Vertical

- BFSI

- IT and Telecom

- Government and Public Sector

- Retail

- Healthcare

- Aerospace and Defense

- Media and Entertainment

- Others

Growth Opportunity

Growth of IoT and 5G Networks

The rapid expansion of Internet of Things (IoT) devices and the widespread deployment of 5G networks are amplifying the demand for robust encryption solutions. With billions of interconnected devices transmitting sensitive data in real-time, the need for end-to-end encryption has become critical. IoT devices, often lacking built-in security features, pose vulnerabilities that encryption can effectively address. As 5G enables faster data transfers and increased network capacity, safeguarding communication channels with encryption will be imperative for enterprises and governments alike.

Cloud Adoption and Hybrid Work Models

The ongoing shift toward cloud adoption, accelerated by the rise of hybrid work models, presents another key growth opportunity for encryption software providers. As organizations store and process vast amounts of data in cloud environments, ensuring data privacy and regulatory compliance has become a top priority. Hybrid work models, which involve employees accessing corporate networks from various locations, create new security challenges. Encryption software solutions that secure remote access and protect cloud-stored data from breaches are seeing increased demand, particularly in sectors like finance, healthcare, and government.

Latest Trends

Zero Trust Security Models

As cyber threats grow in sophistication, organizations are increasingly moving away from perimeter-based security to adopt Zero Trust security frameworks. This model assumes that no user or device, internal or external, can be trusted by default, leading to the need for strong encryption at every access point. Encryption software is critical in enforcing Zero Trust principles, ensuring that sensitive data remains protected even if other security measures fail. In 2024, we expect to see increased demand for encryption solutions that integrate seamlessly with Zero Trust architectures, particularly in sectors such as finance, healthcare, and government.

Post-Quantum Cryptography

The rise of quantum computing poses a looming threat to current encryption standards, which may become obsolete as quantum algorithms can potentially break classical cryptographic techniques. Post-Quantum Cryptography (PQC) is emerging as a key area of focus for encryption software developers. In 2024, organizations will increasingly explore PQC solutions to future-proof their encryption strategies. Leading industry players are expected to accelerate investments in research and development of quantum-resistant algorithms, preparing for the eventual shift to quantum-safe encryption protocols.

Regional Analysis

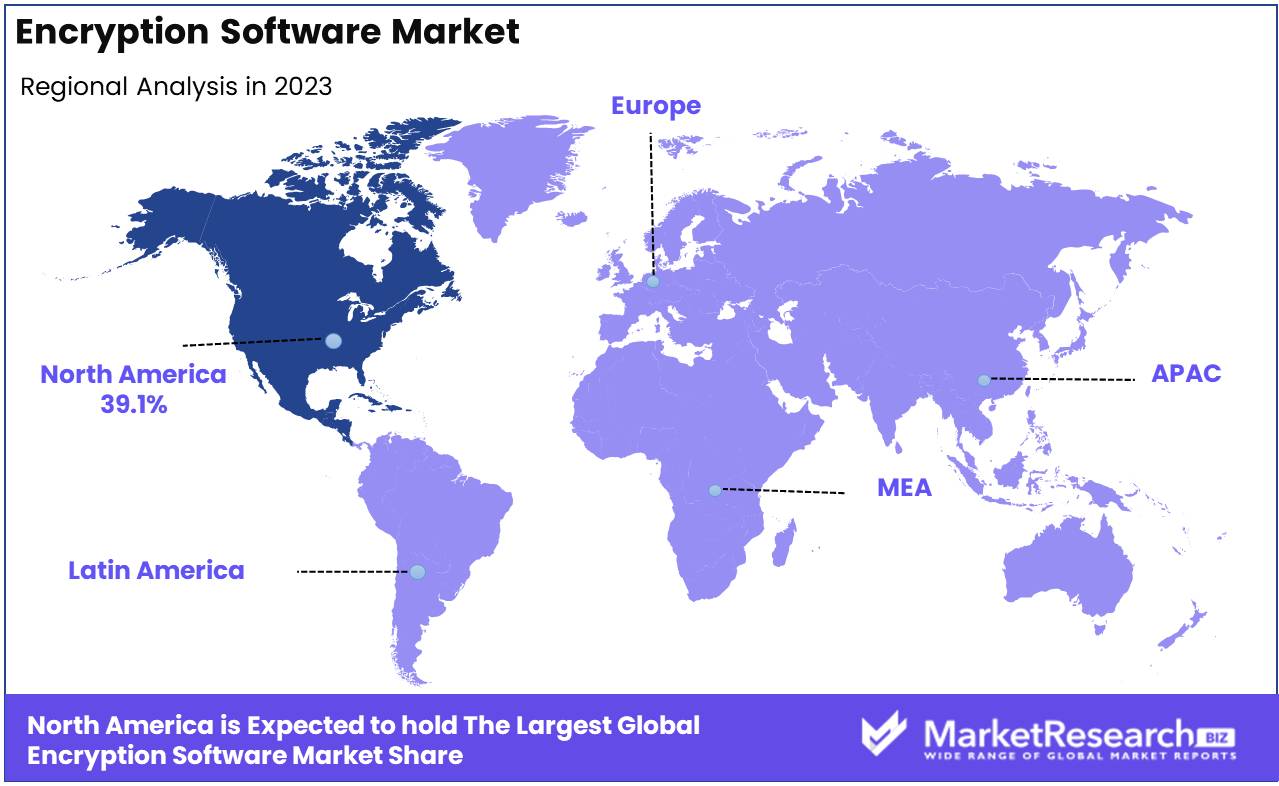

Encryption Software Market in 2024 North America Leads with 39.1% Market Share

In 2024, North America is poised to maintain its leadership in the global encryption software market, commanding a substantial 39.1% of the total market share. The United States spearheads this dominance, propelled by rigorous regulatory standards such as the California Consumer Privacy Act (CCPA) and the Health Insurance Portability and Accountability Act (HIPAA). These regulations necessitate the broad implementation of encryption solutions across critical sectors including finance, healthcare, and technology. Meanwhile, Canada and other North American nations are also witnessing significant growth, driven by an enhanced focus on data privacy and the escalating threats to cybersecurity.

Europe emerges as a significant player in the encryption software arena, bolstered by the General Data Protection Regulation (GDPR) and escalating investments in cybersecurity infrastructure. Leading nations such as Germany, France, the United Kingdom, and Italy are vigorously adopting encryption technologies to protect sensitive data. Germany and the United Kingdom are particularly prominent, leading in innovation within the region, with a strong emphasis on digital security fostering a robust demand for encryption solutions.

The Asia-Pacific region is experiencing rapid advancement, attributed to the expansion of digital infrastructure and an increase in cyber threats in countries like China, Japan, India, and South Korea. Anticipated to register the highest Compound Annual Growth Rate (CAGR), this growth is supported by governmental efforts to strengthen data protection and the rising prominence of encryption in critical sectors such as e-commerce and financial services.

In Latin America, countries like Mexico and Brazil are recognizing growth due to the mounting incidence of cyberattacks and the increasing adoption of cloud computing, prompting organizations to implement more stringent encryption protocols.

The Middle East & Africa region is gradually embracing encryption software, with nations like Saudi Arabia, the United Arab Emirates, and South Africa leading the market expansion. This uptake is spurred by national data protection laws and the digital transformation initiatives within key industries.

These regional dynamics underscore a global movement towards enhanced data security and position encryption as a fundamental measure to counter evolving cyber threats.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In the highly competitive global Encryption Software Market, the year 2024 has seen strategic advancements from major players, such as Bloombase, Cisco Systems, Inc., and Thales Group. These companies, along with others like Check Point Software Technologies Ltd. and Dell Inc., continue to dominate the landscape through innovative integration of digital technologies and enhanced security protocols.

Bloombase has been noteworthy for its agile responses to the growing demands for security in mobile technology, positioning itself as a critical market player. Cisco Systems, Inc., with its robust internet service security solutions, remains a stalwart in the market by leveraging its extensive expertise and comprehensive security suites.

Thales Group has expanded its encryption offerings to encompass a wider range of digital and mobile platforms, enhancing data protection across both public and private sectors. Similarly, IBM Corporation and McAfee, LLC have fortified their market positions through continuous advancements in their encryption technologies, addressing the evolving security challenges presented by increasing digital connectivity.

Microsoft and Oracle Corporation are recognized for their detailed analysis and development of encryption solutions that integrate seamlessly with cloud and enterprise environments, thus supporting widespread digital transformation. Sophos Ltd., Broadcom, and Trend Micro Incorporated continue to enhance their encryption technologies, focusing on user-friendly solutions that do not compromise on security.

Lastly, WinMagic remains a pivotal market player with its specialized focus on securing emerging technologies and endpoints, ensuring comprehensive protection for enterprises navigating the complex digital landscape. The collective efforts of these companies not only drive the market forward but also establish a foundation of trust and reliability essential for the adoption of advanced encryption technologies.

Market Key Players

- Bloombase

- Cisco Systems, Inc.

- Thales Group

- Check Point Software Technologies Ltd.

- Dell Inc.

- IBM Corporation

- McAfee, LLC

- Microsoft

- Oracle Corporation

- Sophos Ltd.

- Broadcom

- Trend Micro Incorporated

- WinMagic

Recent Development

- In April 2023, Utimaco acquired Conpal GmbH, a German data protection company, to strengthen its IT security portfolio, particularly in data encryption and public key infrastructure (PKI) for regulated industries.

- In July 2024, Accenture and SandboxAQ: Accenture and SandboxAQ partnered to address AI and quantum-related threats to enterprise data encryption, focusing on enhancing security, observability, and resilience against third-party risks.

- In September 2023, Arqit Quantum Inc.: Arqit launched Arqit WalletSecure, a platform-as-a-service for secure symmetric key agreements, targeting digital assets used by banks and advancing the use of quantum technology in encryption.

- In 2023, Cisco completed a $28 billion acquisition of Splunk, a cybersecurity and asset management company, to bolster its AI-driven security and observability solutions, aiming to improve threat prediction and prevention.

- In 2024, Quantum Encryption Market: The global quantum encryption market, including Quantum Key Distribution (QKD), is projected to reach $5 billion, driven by the rising need for quantum-safe encryption, especially in finance and healthcare.

- In June 2023 : AWS launched Amazon S3 dual-layer server-side encryption (DSSE-KMS) to offer enhanced data protection by applying two layers of encryption, helping users meet regulatory requirements and improve data security.

Report Scope

Report Features Description Market Value (2023) USD 13.9 Bn Forecast Revenue (2033) USD 67.5 Bn CAGR (2024-2032) 17.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component(Software,Services),By Deployment Mode(On-premise, Cloud), By Services(Professional Services, Managed Services),By Enterprise Size(Large Enterprise,Small and Medium-sized Enterprises),By Function (Disk Encryption,Communication Encryption,File/Folder Encryption,Cloud Encryption),By Industry Vertical (BFSI,IT and Telecom, Government and Public Sector, Retail, Healthcare, Aerospace and Defense, Media and Entertainment, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Bloombase,Cisco Systems, Inc.,Thales Group,Check Point Software Technologies Ltd.,Dell Inc.,IBM Corporation,McAfee, LLC,Microsoft,Oracle Corporation,Sophos Ltd.,Broadcom,Trend Micro Incorporated,WinMagic Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

Our Clients

View Our Licence Options