Global Electroretinography Market By Product(Fixed Electroretinography, Portable Electroretinography), By Application(Clinical, Research), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46038

-

May 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

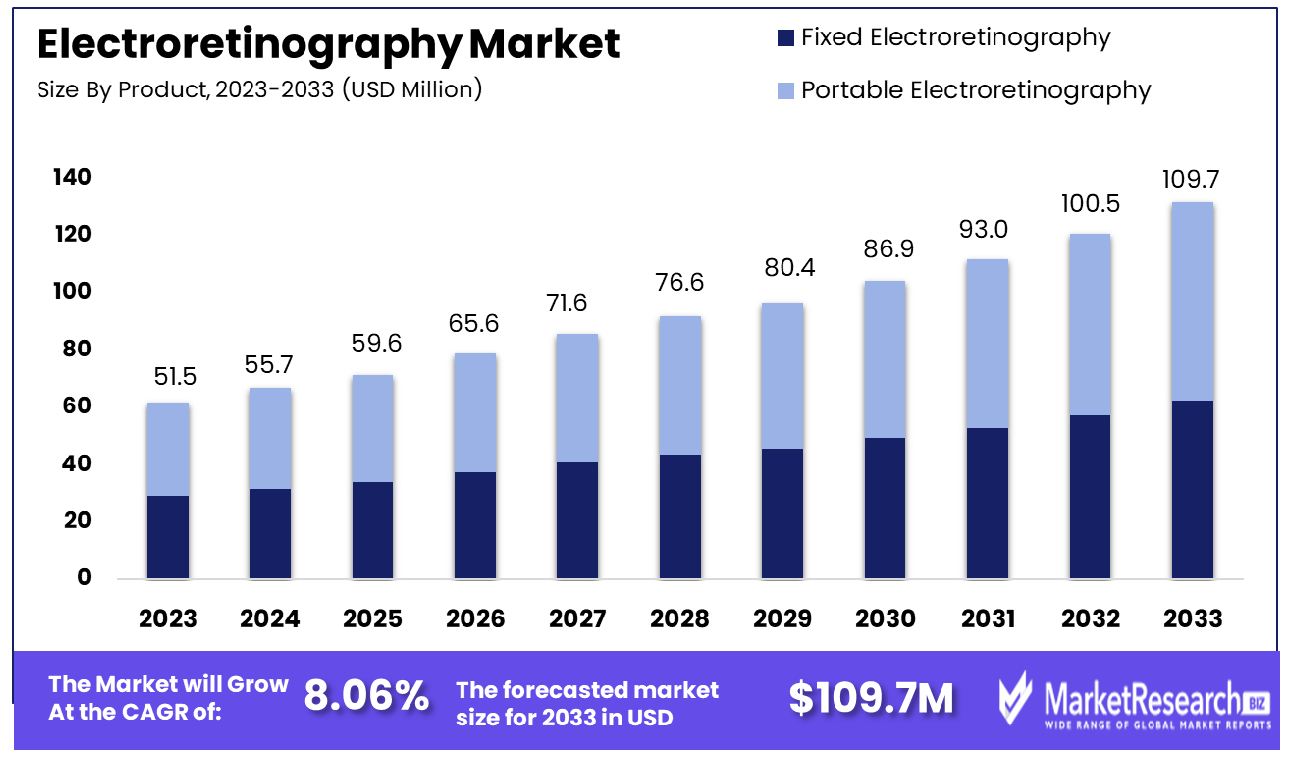

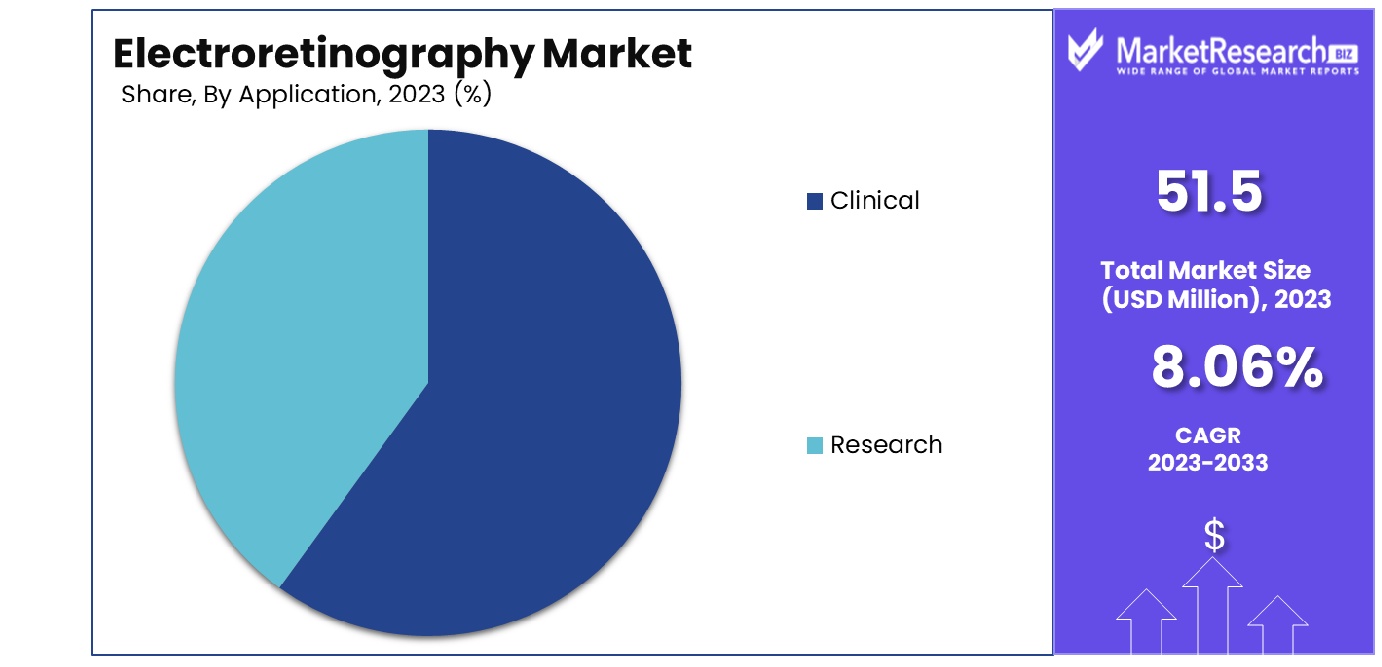

The Global Electroretinography Market was valued at USD 51.5 million in 2023. It is expected to reach USD 109.7 million by 2033, with a CAGR of 8.06% during the forecast period from 2024 to 2033.

The Electroretinography (ERG) Market pertains to the segment within the medical devices industry focused on diagnostic tools for evaluating retinal health and function. Utilizing advanced technologies, such as electroretinography, this market offers indispensable solutions for ophthalmologists and optometrists in diagnosing various retinal disorders and monitoring treatment efficacy.

Key offerings include portable ERG devices, coupled with sophisticated software for comprehensive analysis, enhancing diagnostic precision and patient care. With a surge in demand for early detection and management of ocular diseases, the Electroretinography Market presents lucrative opportunities for innovation and expansion, positioning it as a pivotal player in advancing eye healthcare globally.

The electroretinography (ERG) market is poised for significant growth, driven by its crucial role in diagnosing retinal conditions. Electroretinography, a diagnostic test that measures the electrical response of the eye's light-sensitive cells, is pivotal in detecting various retinal diseases.

For instance, in conditions such as central retinal artery occlusion (CRAO), ERG outcomes are distinctly negative, highlighting a reduction in b-wave amplitude while maintaining a relatively preserved a-wave. Conversely, in central retinal vein occlusion (CRVO), a negative ERG or delayed response in the 30-Hz flicker test often indicates severe ischemia, aiding in early intervention strategies.

Recent advancements in technology, such as the integration of machine learning with full-field ERG, have enhanced the diagnostic accuracy for inherited retinal degenerations like ABCA4 retinopathy. This integration not only improves phenotyping accuracy but also propels research and development within the field, potentially opening new therapeutic avenues.

Furthermore, the utility of ERG extends to pediatric care, as it provides reliable functional data for children of all ages, reaching adult ERG values around 6–9 months. This broad applicability across age groups significantly widens the market, underscoring the demand for advanced diagnostic tools in pediatric ophthalmology and beyond.

Given these dynamics, the electroretinography market is set to expand, fueled by technological advancements and the increasing need for precise diagnostic procedures across a range of retinal conditions.

Key Takeaways

- Market Growth: The Global Electroretinography Market was valued at USD 51.5 million in 2023. It is expected to reach USD 109.7 million by 2033, with a CAGR of 8.06% during the forecast period from 2024 to 2033.

- By Product: Portable Electroretinography dominated with a 45% market share.

- By Application: Clinical applications led, holding a 21% dominance.

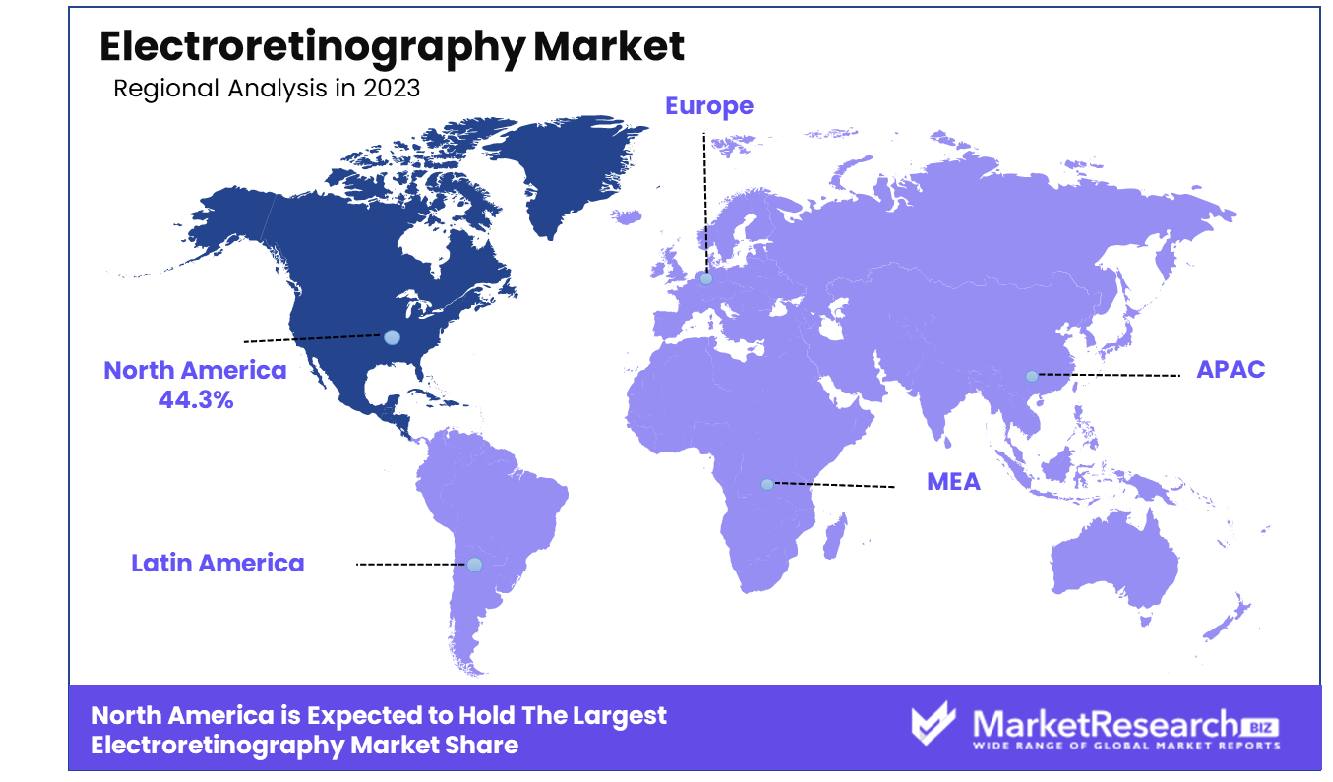

- Regional Dominance: The Electroretinography market in North America constitutes 44.3% of the global share.

- Growth Opportunity: The expansion of ophthalmic clinics and the adoption of non-invasive diagnostic techniques are driving the growth of the Electroretinography market, enhancing diagnostic precision and patient comfort.

Driving factors

Constant Innovation and Growth in Ophthalmology Clinics and Research Centers

The Electroretinography (ERG) market is primarily driven by constant innovation and the expansion of ophthalmology clinics and research centers globally. As these facilities increase in number, the demand for advanced diagnostic tools, including ERG devices, also rises.

Innovations in ERG technology, such as the development of portable and non-invasive devices, enhance diagnostic capabilities, making them more accessible to healthcare providers. This expansion is critical in meeting the growing need for specialized ophthalmic care and supports early and accurate diagnosis of eye conditions, thereby boosting the market growth.

Rising Demand for Ophthalmic Diagnostic Tools

The increasing demand for sophisticated ophthalmic diagnostic tools directly influences the growth of the Electroretinography market. ERG devices, which are pivotal in diagnosing retinal disorders, are seeing a surge in demand due to their ability to provide detailed insights into retinal function.

This demand is fueled by a growing awareness among healthcare professionals about the importance of early diagnosis and the effectiveness of ERG in guiding treatment decisions. As a result, the adoption of ERG technology is increasing, further propelled by improvements in device accuracy and patient comfort.

Increasing Prevalence of Eye Disorders

A significant growth driver for the ERG market is the increasing prevalence of eye disorders such as diabetic retinopathy, glaucoma, and macular degeneration. These conditions affect millions worldwide and are leading causes of vision impairment and blindness. The rising incidence rate necessitates robust diagnostic procedures to manage these diseases effectively.

Electroretinography plays a crucial role in this context by enabling the early detection and monitoring of changes in retinal function associated with these disorders. The critical need for effective diagnostic strategies in managing the growing burden of eye diseases substantiates the expansion of the ERG market.

Restraining Factors

High Cost of Electroretinogram Devices

The high cost of electroretinogram devices significantly restrains the growth of the Electroretinography Market. Electroretinogram (ERG) systems, essential for diagnosing and monitoring disorders affecting the retina, require sophisticated technology and high-quality components, contributing to their steep prices. This financial barrier can deter healthcare facilities, particularly in emerging economies, from acquiring these devices, thereby limiting market expansion.

Smaller clinics and hospitals might opt for alternative diagnostic methods that do not provide the same accuracy as ERG, potentially affecting the quality of patient care. Consequently, the market's growth is impeded as the adoption rate of these advanced devices remains low in cost-sensitive regions.

Non-availability of Skilled Professionals

The scarcity of skilled professionals to operate electroretinogram devices further hampers the Electroretinography Market's expansion. ERG testing requires specific expertise to interpret complex data accurately, but there is a noticeable gap in trained ophthalmologists and technicians who can efficiently handle these systems. This shortage is more pronounced in underdeveloped and some developing countries where medical training and equipment are not as advanced or widespread.

Without adequate professionals, even if healthcare facilities can afford the latest ERG technology, its utilization and thus its potential market penetration are severely limited. This situation creates a cyclical challenge, as fewer skilled professionals lead to underutilization of available technology, which in turn discourages further investment in ERG devices.

By Product Analysis

Portable Electroretinography dominated, accounting for 45% of the market, emphasizing its versatility and convenience.

In 2023, the Electroretinography Market was prominently led by Portable Electroretinography, which held more than a 45% share of the market in the By Product segment. This substantial market share underscores the increasing preference for portable diagnostic solutions that offer flexibility and ease of use in various clinical settings. Portable devices have been pivotal in facilitating early and efficient diagnosis of retinal conditions, directly contributing to enhanced patient outcomes and greater adaptability in healthcare environments.

On the other hand, Fixed Electroretinography, while being essential in stationary clinical settings for detailed and comprehensive retinal examinations, captured a smaller segment of the market. The fixed systems continue to be indispensable for in-depth diagnostic procedures and are predominantly used in hospitals and specialized eye care centers. The differentiation in market share between portable and fixed systems reflects a broader trend toward mobility and patient-centric care in medical technologies.

The growth of the Portable Electroretinography segment can be attributed to several factors. Technological advancements have led to the development of lightweight, compact models that ensure convenience without compromising diagnostic accuracy. Moreover, the rising incidence of retinal diseases and the growing geriatric population, combined with a shift towards outpatient care settings, have significantly fueled the demand for portable electroretinography systems.

Despite the dominance of portable units, fixed electroretinography systems remain relevant due to their advanced capabilities in handling complex cases and providing high-resolution imaging. The market dynamics between these two segments are influenced by ongoing innovations and changing healthcare practices, pointing towards a continued evolution of the Electroretinography Market.

By Application Analysis

Clinical applications led, comprising 21% of the market, highlighting the crucial role in patient diagnostics.

In 2023, Clinical applications held a dominant position in the By Application segment of the Electroretinography Market, capturing more than a 21% share. This segment includes the use of electroretinography in routine clinical practices and hospitals for diagnosing and monitoring various retinal conditions. The significant share held by clinical applications is indicative of the critical role that electroretinography plays in the healthcare sector, particularly in ophthalmology.

Conversely, the Research segment, while smaller in market share, is integral to advancing the understanding and treatment of retinal diseases. This segment focuses on the use of electroretinography in academic and pharmaceutical research settings to study the functional aspects of the retina under various conditions and to evaluate the efficacy of new therapeutic drugs.

The prominence of the Clinical segment is driven by the increasing prevalence of retinal diseases such as diabetic retinopathy, age-related macular degeneration, and retinitis pigmentosa. The aging global population and the rising incidence of diabetes contribute to the growth of this market segment. Furthermore, the need for precise diagnostic tools in clinical settings to provide timely and accurate treatments enhances the demand for electroretinography devices.

Despite the larger share of clinical applications, the research segment is poised for growth, propelled by technological innovations and increasing investments in ophthalmic research. As researchers continue to explore the complexities of the human eye, the potential for new applications and improvements in electroretinography technology is vast, suggesting a dynamic future for both segments of the market.

Key Market Segments

By Product

- Fixed Electroretinography

- Portable Electroretinography

By Application

- Clinical

- Research

Growth Opportunity

Expansion of Ophthalmic Clinics and Diagnostic Centers

The expansion of ophthalmic clinics and diagnostic centers globally is a significant growth driver for the Electroretinography market in 2023. As populations age and the prevalence of eye-related disorders increases, there is a heightened demand for specialized ophthalmic services, including advanced diagnostic capabilities. Electroretinography, which records electrical responses of various cell types within the retina, is becoming increasingly vital in diagnosing and monitoring retinal diseases.

The establishment of new clinics and centers equipped with such diagnostic technologies not only extends the reach of healthcare services but also enhances the precision of retinal assessments. This expansion is expected to boost the adoption of electroretinography devices, contributing to the market's growth.

Adoption of Non-invasive Diagnostic Techniques

The shift towards non-invasive diagnostic techniques is another critical opportunity for growth in the Electroretinography market. Traditional diagnostic methods for eye conditions often involve invasive procedures that can be uncomfortable and carry risks of complications. In contrast, electroretinography offers a non-invasive alternative, providing significant benefits in terms of patient comfort and safety.

This advantage aligns with the broader healthcare trends emphasizing patient-centric and minimally invasive diagnostic approaches. As awareness and preference for non-invasive techniques grow, so does the potential market for electroretinography, positioning it as a preferred choice for retinal diagnostics in various healthcare settings.

Latest Trends

Integration of Artificial Intelligence for Data Analysis

The integration of artificial intelligence (AI) in the electroretinography market represents a transformative trend in 2023. AI's capability to analyze large volumes of diagnostic data rapidly and with high accuracy is particularly beneficial in the field of ophthalmology, where early detection and precise monitoring of retinal conditions are crucial.

By leveraging AI algorithms, healthcare providers can enhance the interpretation of electroretinography results, leading to more accurate diagnoses and personalized treatment plans. This trend not only improves patient outcomes but also increases the efficiency of healthcare services by reducing the time and resources needed for data analysis.

Development of Portable and Handheld Electroretinography Devices

Another significant trend in the electroretinography market is the development of portable and handheld devices. These innovations address the growing demand for accessible and convenient diagnostic solutions, particularly in remote and underserved areas. Portable electroretinography devices allow for on-site patient diagnostics, bypassing the need for visits to specialized clinics and thereby reducing barriers to care.

Additionally, these devices are proving invaluable in situations where mobility is essential, such as in emergency care and in-home assessments for bedridden patients. The proliferation of portable and handheld devices not only expands the market reach but also aligns with the global push towards more decentralized and patient-centered healthcare models.

Regional Analysis

The Electroretinography market in North America holds a significant 44.3% market share.

North America remains the dominant region, accounting for 44.3% of the global ERG market. This prominence can be attributed to advanced healthcare infrastructure, significant investments in ophthalmic research, and the prevalence of retinal disorders. The region's market is further buoyed by the presence of leading medical device companies and robust FDA activities ensuring the availability of advanced ERG systems.

Europe follows, driven by increasing healthcare expenditure, an aging population, and rising awareness of eye-related ailments. The region's market benefits from supportive government policies promoting eye health and substantial research funding in countries such as Germany, the UK, and France.

The Asia Pacific region is noted for its fast-paced growth, primarily due to improving healthcare facilities, rising disposable incomes, and the expanding presence of international players in emerging economies like China and India. The increase in diabetic populations, who are at high risk of developing retinal diseases, also propels the demand for ERG testing in this region.

Middle East & Africa show promising growth, albeit from a smaller base, spurred by gradual healthcare advancements and the rising awareness of preventive care in countries like Saudi Arabia and the UAE.

Latin America, though the smallest segment, is witnessing gradual growth driven by improvements in healthcare infrastructure and the growing prevalence of non-communicable diseases that affect vision.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Electroretinography (ERG) market features a diverse array of key players, each contributing uniquely to the sector’s dynamics and innovation. LKC Technologies, Inc., stands out with its cutting-edge RETeval device, facilitating portable ERG testing that is crucial for reaching underserved populations. This adaptability to varying clinical settings significantly enhances its market penetration.

Diagnosys LLC continues to cement its reputation through its wide range of ERG systems, notably excelling in the provision of customizable solutions that cater to specific research and clinical needs, thereby ensuring a strong foothold in both academic and healthcare facilities.

Electro-Diagnostic Imaging, Inc. leverages its expertise in imaging technology to deliver high-quality ERG and visual electrophysiology devices. Their emphasis on integrating technology with user-centric designs is pivotal in their sustained growth and acceptance in the market.

Diopsys, Inc. is at the forefront of innovation in non-invasive, office-based ERG and Visual Evoked Potential (VEP) testing systems. Their technology’s ease of use and reliability make it a preferred choice for routine clinical assessments, driving their expansion in ophthalmology practices globally.

Roland Consult Stasche & Finger GmbH distinguishes itself with robust, high-precision systems tailored for complex diagnostic applications, supporting their strong presence, particularly in European markets.

Metrovision, Costruzione Strumenti Oftalmici, and Konan Medical USA, Inc. contribute significantly with specialized products that meet both clinical and research demands, enhancing their visibility and adoption.

Welch Allyn rounds out this group by integrating ERG functionalities into broader diagnostic devices, appealing to practices looking for versatile and cost-effective solutions. This strategic positioning helps them maintain competitiveness in a market that values integrated healthcare solutions.

Market Key Players

- LKC Technologies, Inc

- Diagnosys LLC

- Electro-Diagnostic Imaging, Inc.

- Diopsys, Inc.

- Roland Consult Stasche & Finger GmbH

- Metrovision

- Costruzione Strumenti Oftalmici

- Konan Medical USA, Inc.

- Welch Allyn

Recent Development

- In May 2024, Waseda University develops a soft multi-electrode system for electroretinography, improving the diagnosis of ocular diseases. The system, integrated into disposable contact lenses, offers comfort and precise spatial measurements of retinal signals.

- In February 2024, Advancements in ERG technology aim to enhance accessibility and diagnostic capabilities. Portable devices like RETeval and Espion simplify testing, aiding the early detection of ocular diseases.

Report Scope

Report Features Description Market Value (2023) USD 51.5 Million Forecast Revenue (2033) USD 109.7 Million CAGR (2024-2032) 8.06% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product(Fixed Electroretinography, Portable Electroretinography), By Application(Clinical, Research) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape LKC Technologies, Inc, Diagnosys LLC, Electro-Diagnostic Imaging, Inc., Diopsys, Inc., Roland Consult Stasche & Finger GmbH, Metrovision, Costruzione Strumenti Oftalmici, Konan Medical USA, Inc., Welch Allyn Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- LKC Technologies, Inc

- Diagnosys LLC

- Electro-Diagnostic Imaging, Inc.

- Diopsys, Inc.

- Roland Consult Stasche & Finger GmbH

- Metrovision

- Costruzione Strumenti Oftalmici

- Konan Medical USA, Inc.

- Welch Allyn

Our Clients

View Our Licence Options