Electroceuticals Market By Product (Cardiac Pacemakers and Implantable Cardioverter Defibrillators, Cochlear Implants, Spinal Cord Stimulators, Deep Brain Stimulators, Vagus Nerve Stimulators, Sacral Nerve Stimulators, Others), By Device Type (Implantable Devices and Non-invasive Devices), By Application (Arrhythmia, Sensorineural Hearing Loss, Epilepsy, Parkinson's Disease, Others), By End User (Hospitals, Ambulatory Surgical Centers, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And F

-

47941

-

Feb 2025

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

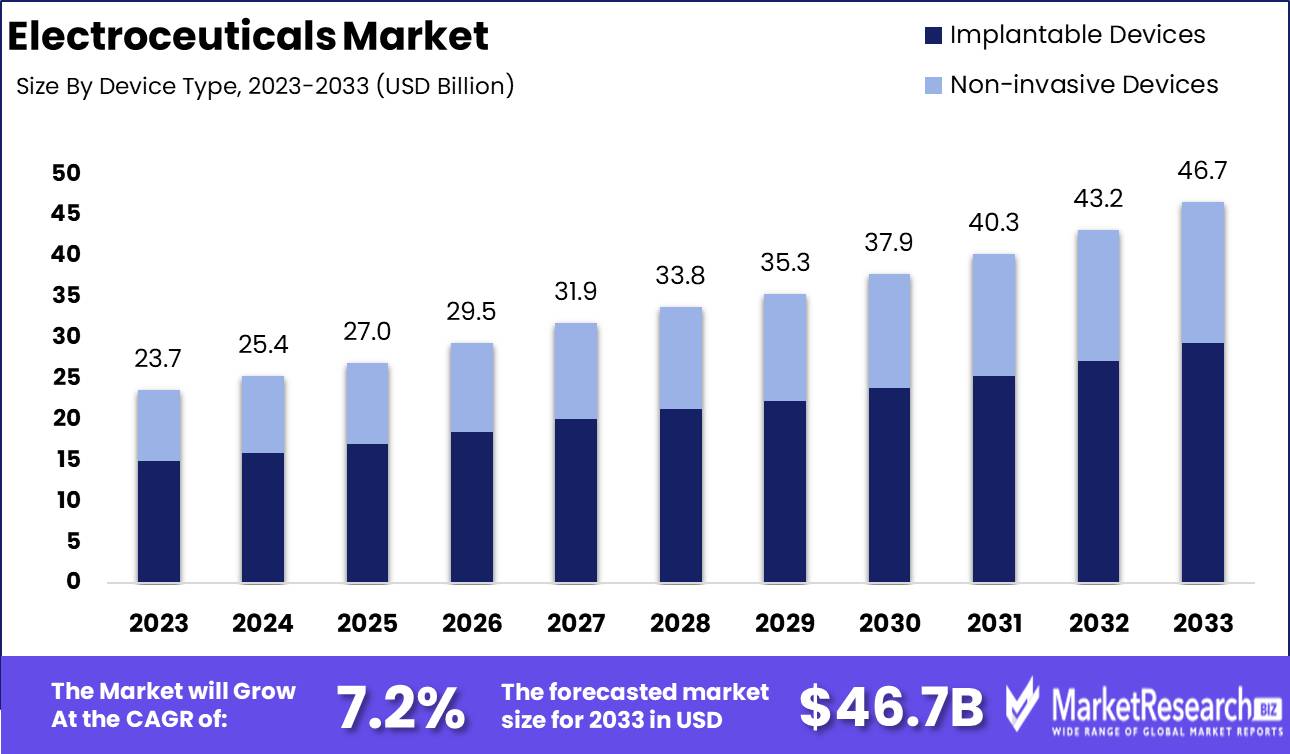

The Electroceuticals Market was valued at USD 23.7 billion in 2023. It is expected to reach USD 46.7 billion by 2033, with a CAGR of 7.2% during the forecast period from 2024 to 2033.

The Electroceuticals Market encompasses a rapidly growing segment of healthcare technology that utilizes electrical stimulation to treat various medical conditions. This market includes devices such as pacemakers, cochlear implants, and neurostimulators, which modulate the nervous system to manage ailments like chronic pain, epilepsy, and Parkinson's disease. Advancements in bioelectronics and miniaturization technologies are driving innovation, enhancing device efficacy and patient outcomes. The increasing prevalence of chronic diseases, coupled with a rising demand for non-pharmacological therapies, is fueling market growth. Strategic partnerships and regulatory advancements further accelerate the adoption of electroceuticals, positioning this market as a pivotal player in the future of medicine.

The electroceuticals market is poised for significant growth, driven by technological advancements, increasing adoption of personalized medicine, and the ongoing quest for innovative therapeutic solutions. The rapid pace of innovation in bioelectronic medicine, coupled with the miniaturization of devices, is enabling more precise and less invasive treatments for a variety of chronic conditions. These advancements are not only enhancing the efficacy of electroceutical devices but also broadening their application scope.

However, the high costs associated with electroceutical devices remain a significant barrier to widespread adoption, limiting accessibility for many patients and posing a challenge for healthcare systems globally. Despite these cost-related hurdles, the trend toward personalized medicine is offering new growth opportunities. Electroceutical treatments tailored to individual patient needs are gaining traction, promising more effective and targeted therapeutic outcomes. As the industry continues to evolve, stakeholders must navigate these complexities, balancing innovation with cost containment to unlock the full potential of electroceuticals in modern healthcare.

In addition to technological advancements and the push for personalized medicine, the electroceuticals market must address several strategic challenges to sustain its growth trajectory. The integration of bioelectronic therapies into standard medical practices requires robust clinical validation and regulatory approvals, necessitating substantial investment in research and development.

Furthermore, the high upfront costs of these devices necessitate innovative pricing strategies and reimbursement models to enhance patient access and affordability. Collaborative efforts among manufacturers, healthcare providers, and policymakers are crucial in overcoming these financial barriers. By fostering partnerships and leveraging advancements in digital health, the electroceuticals market can achieve scalable growth and establish itself as a cornerstone of future therapeutic modalities. This strategic focus on innovation, cost management, and patient-centric care positions the electroceuticals market for a transformative impact on global health outcomes.

Key Takeaways

- Market Growth: The Electroceuticals Market was valued at USD 23.7 billion in 2023. It is expected to reach USD 46.7 billion by 2033, with a CAGR of 7.2% during the forecast period from 2024 to 2033.

- By Product: Cardiac Pacemakers and Implantable Defibrillators dominated the Electroceuticals Market.

- By Device Type: Implantable Devices dominate electroceuticals due to efficacy and long-term solutions.

- By Application: Arrhythmia segment dominated the electroceuticals market across diverse applications.

- By End User: Hospitals dominated the electroceuticals market by end user.

- Regional Dominance: North America leads the global electroceuticals market with a 40% largest share.

- Growth Opportunity: The global electroceuticals market will grow significantly due to non-invasive therapy trends and supportive regulatory frameworks.

Driving factors

Rising Prevalence of Chronic Diseases Fuels Demand for Electroceuticals

The increasing prevalence of chronic diseases, such as cardiovascular disorders, diabetes, and neurological conditions, is a primary driver of growth in the electroceuticals market. Chronic diseases are becoming more common due to aging populations, lifestyle changes, and environmental factors. For instance, the World Health Organization (WHO) reports that chronic diseases are responsible for approximately 71% of all deaths globally, emphasizing the critical need for effective treatments.

Electroceuticals, which offer targeted and minimally invasive therapeutic options, are well-positioned to address this growing healthcare burden. Devices such as pacemakers, cochlear implants, and neurostimulators are crucial in managing these conditions, providing significant relief and improving patient outcomes. As the incidence of these diseases continues to rise, so too does the market potential for electroceuticals, creating a robust demand for innovative therapeutic solutions.

The surge in Demand for Non-Invasive Therapies Boosts Market Adoption

The growing demand for non-invasive and minimally invasive therapies is significantly propelling the electroceuticals market. Patients and healthcare providers are increasingly favoring treatments that offer fewer risks, reduced recovery times, and improved quality of life compared to traditional surgical procedures. Electroceuticals, which often involve less invasive techniques such as electrical stimulation and neuromodulation, align perfectly with these preferences. For example, neuromodulation devices like spinal cord stimulators provide pain relief without the need for invasive surgery. This trend is supported by a broader movement towards patient-centric care, where treatment options are tailored to enhance patient comfort and convenience. Consequently, the market is witnessing accelerated adoption rates, as these devices meet the growing demand for safer and more efficient therapeutic alternatives.

Enhanced Healthcare Infrastructure Supports Market Expansion

The global enhancement of healthcare infrastructure is a pivotal factor contributing to the expansion of the electroceuticals market. Governments and private sectors worldwide are investing heavily in healthcare facilities, advanced medical equipment, and innovative treatment technologies. Improved healthcare infrastructure ensures better access to cutting-edge medical treatments, including electroceuticals, especially in emerging economies where healthcare systems are rapidly evolving. For instance, increased healthcare expenditure and the establishment of specialized medical centers facilitate the integration and widespread adoption of electroceutical devices.

Furthermore, advancements in healthcare delivery systems, coupled with robust reimbursement frameworks, are making these therapies more accessible and affordable for a larger patient population. This infrastructural progress not only enhances the quality of care but also stimulates market growth by creating a conducive environment for the adoption of advanced therapeutic technologies.

Restraining Factors

Competition from Traditional Therapies: A Significant Barrier to Electroceuticals Adoption

The Electroceuticals market faces significant competition from established traditional therapies, including surgery and pharmaceuticals. These conventional treatment methods are deeply entrenched in the healthcare system, with a long history of clinical use, well-established efficacy, and strong patient and physician trust. For instance, pharmaceuticals have a vast body of research supporting their use, making it challenging for newer technologies like electroceuticals to gain a foothold.

The familiarity and reliability associated with traditional therapies make it difficult for electroceuticals to be considered a primary treatment option. Many patients and healthcare providers are hesitant to shift from tried-and-true methods to newer, less understood technologies. Additionally, the established pharmaceutical and surgical industries benefit from robust infrastructure and significant marketing budgets, further overshadowing emerging treatments. This competitive landscape can slow the growth of the electroceuticals market, as gaining widespread acceptance and trust is a gradual process.

Limited Research and Regulatory Hurdles: Slowing Innovation and Market Penetration

Electroceuticals face significant challenges related to limited research and stringent regulatory requirements. The development of new electroceutical devices often requires extensive clinical trials to demonstrate safety and efficacy, a process that can be both time-consuming and costly. These trials are crucial for gaining regulatory approval, but they also create substantial barriers to entry and slow down the pace of innovation.

Regulatory bodies, such as the FDA in the United States and the EMA in Europe, have rigorous standards for approving new medical devices. These standards are designed to ensure patient safety but can be particularly burdensome for emerging technologies. The lack of comprehensive clinical data supporting electroceutical treatments compared to well-established pharmaceuticals can lead to longer approval times and higher costs.

Furthermore, the limited research funding dedicated to electroceuticals compared to traditional therapies impedes progress. Pharmaceutical companies, which often have more substantial financial resources, dominate medical research, leaving fewer funds available for exploring alternative treatments like electroceuticals. This disparity in research funding results in fewer advancements and slower adoption of electroceutical technologies.

By Product Analysis

In 2023, Cardiac Pacemakers and Implantable Defibrillators dominated the Electroceuticals Market.

In 2023, Cardiac Pacemakers and Implantable Cardioverter Defibrillators held a dominant market position in the by-product segment of the Electroceuticals Market. This dominance is primarily driven by the increasing prevalence of cardiovascular diseases, advancements in device technology, and the growing elderly population. Cardiac pacemakers, essential for managing arrhythmias, and implantable cardioverter defibrillators, critical for preventing sudden cardiac arrest, continue to see high demand due to their life-saving benefits and continuous innovation in device miniaturization and battery life.

Cochlear Implants represent another significant segment, propelled by rising incidences of hearing loss and advancements in auditory technology, which improve user experience and hearing outcomes. Spinal Cord Stimulators are gaining traction due to their effectiveness in managing chronic pain, particularly in patients who do not respond to conventional therapies.

Deep Brain Stimulators are increasingly utilized for neurological disorders such as Parkinson’s disease and epilepsy, reflecting their growing acceptance in clinical settings. Vagus Nerve Stimulators, used for epilepsy and depression, are also expanding in application due to ongoing research and favorable clinical outcomes. Sacral Nerve Stimulators, primarily for urinary and fecal incontinence, are benefiting from increased awareness and technological improvements.

Lastly, the 'Others' category, encompassing emerging devices and niche applications, is witnessing innovation-driven growth, underpinned by research in bioelectronics and personalized medicine. This comprehensive development across sub-segments underscores the robust and diversified growth trajectory of the Electroceuticals Market.

By Device Type Analysis

Implantable Devices dominate electroceuticals due to efficacy and long-term solutions.

In 2023, Implantable Devices held a dominant market position in the "By Device Type" segment of the Electroceuticals Market. This segment includes two primary categories: Implantable Devices and Non-invasive Devices. Implantable devices, such as pacemakers, cochlear implants, and neurostimulators, are surgically inserted into the body to deliver precise electrical stimulation to target nerves or organs. Their dominance can be attributed to their efficacy in managing chronic conditions, offering sustained therapeutic effects, and advancing technology that enhances patient outcomes.

On the other hand, Non-invasive Devices, which include transcutaneous electrical nerve stimulation (TENS) units and wearable devices, provide electrical stimulation externally without surgical intervention. These devices are favored for their ease of use, lower risk profiles, and growing acceptance in managing pain and other conditions. Although non-invasive devices are gaining traction due to their non-surgical nature and convenience, implantable devices' ability to offer long-term solutions for severe conditions secures their leading market position. The balance between these two segments reflects the diverse needs of patients and the evolving landscape of electroceutical therapies.

By Application Analysis

In 2023, The Arrhythmia segment dominated the electroceuticals market across diverse applications.

In 2023, The Arrhythmia segment held a dominant market position in the By Application segment of the Electroceuticals Market. This leadership can be attributed to the significant advancements in cardiac pacemakers and implantable cardioverter defibrillators (ICDs), which have proven effective in managing arrhythmia. The high prevalence of cardiovascular diseases globally has further fueled demand for these life-saving devices.

Sensorineural Hearing Loss follows as a key segment, driven by innovations in cochlear implants and auditory brainstem implants that provide significant improvements in hearing capabilities for individuals with severe hearing loss. The aging population, particularly in developed regions, has spurred market growth in this category.

Epilepsy remains a critical segment, with the development of neurostimulation devices like vagus nerve stimulators and responsive neurostimulation systems offering new hope for patients with refractory epilepsy. These devices help in reducing seizure frequency and improving the quality of life for patients who do not respond to traditional pharmacological treatments.

Parkinson's Disease is another vital area within the electroceuticals market. Deep brain stimulation (DBS) devices have become increasingly popular, offering substantial benefits in managing symptoms and improving motor functions in Parkinson’s patients. The rising incidence of neurodegenerative disorders propels the demand in this segment.

Lastly, the Others category encompasses various applications such as chronic pain management, overactive bladder, and migraine. The ongoing research and development efforts in bioelectronic medicine continue to expand the therapeutic potential of electroceuticals, positioning this market for robust growth across multiple medical conditions.

By End User Analysis

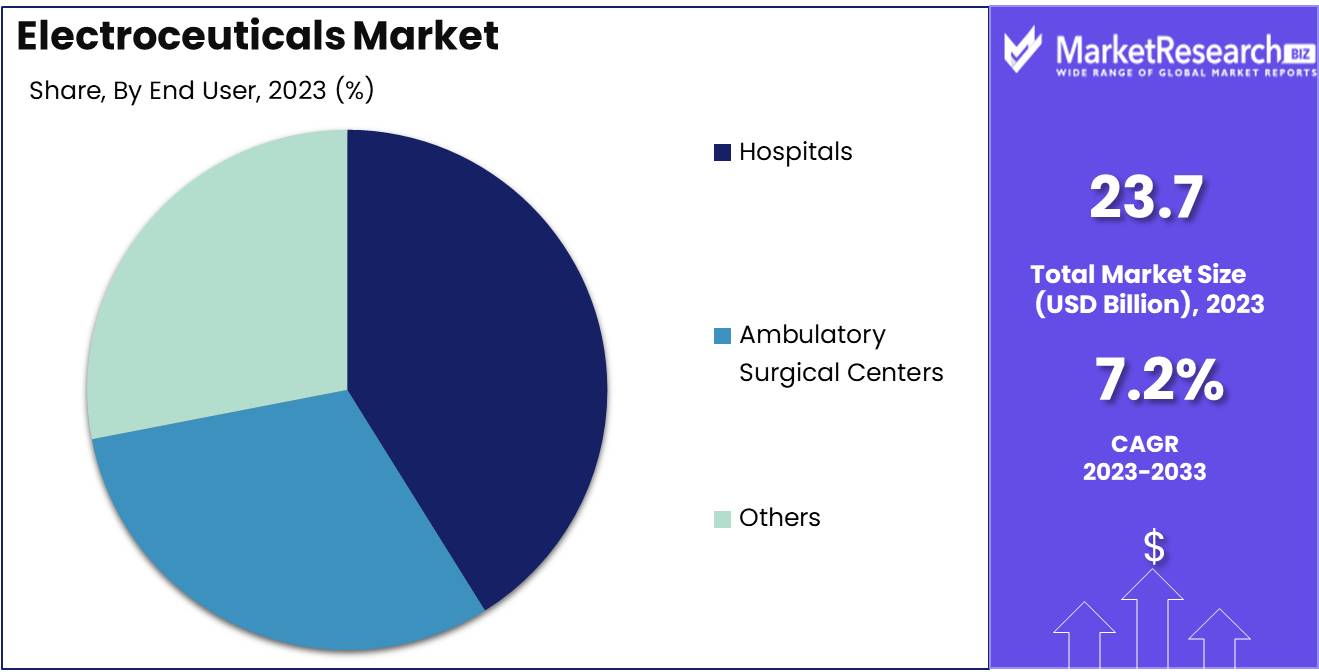

In 2023, Hospitals dominated the electroceuticals market by end users.

In 2023, Hospitals held a dominant market position in the "By End User" segment of the electroceuticals market. This dominance is driven by the increasing adoption of electroceutical devices for managing chronic diseases and post-surgical recovery, where hospitals are primary facilitators due to their advanced medical infrastructure and comprehensive care capabilities.

Ambulatory surgical centers (ASCs) also represent a significant segment, benefiting from the rising preference for outpatient surgeries that necessitate minimally invasive treatments with electroceuticals. These centers provide cost-effective, convenient alternatives to traditional hospital settings, attracting a growing patient demographic.

The "Others" category encompasses various healthcare providers, including specialized clinics and home healthcare services, which are gradually incorporating electroceutical devices to enhance patient outcomes and improve the quality of life. Collectively, these segments highlight the diverse application landscape of electroceuticals, with hospitals leading the way due to their extensive resources, followed by ASCs leveraging operational efficiency, and other healthcare providers expanding access to these innovative therapies. This segmentation underscores the crucial role each category plays in the broader adoption and utilization of electroceuticals in contemporary medical practice.

Key Market Segments

By Product

- Cardiac Pacemakers and Implantable Cardioverter Defibrillators

- Cochlear Implants

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Vagus Nerve Stimulators

- Sacral Nerve Stimulators

- Others

By Device Type

- Implantable Devices

- Non-invasive Devices

By Application

- Arrhythmia

- Sensorineural Hearing Loss

- Epilepsy

- Parkinson's Disease

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Others

Growth Opportunity

Shift Towards Non-Invasive Therapies

The global electroceuticals market is poised for significant growth driven primarily by the increasing preference for non-invasive therapies. As healthcare systems worldwide pivot towards patient-centric approaches, the demand for minimally invasive treatment options has surged. Electroceuticals, which utilize electrical stimulation to modulate nerve activity and treat various chronic conditions, offer a compelling alternative to conventional pharmaceuticals and invasive procedures. This shift is underpinned by growing patient awareness and acceptance, coupled with advancements in bioelectronics technology. Innovations in device miniaturization and targeted stimulation have further enhanced the efficacy and safety profiles of electroceuticals, positioning them as a critical component in the future of medical treatments.

Favorable Regulatory Environment

A favorable regulatory environment is another crucial factor catalyzing the expansion of the electroceuticals market. Regulatory bodies across key markets, including the FDA in the United States and the EMA in Europe, have streamlined approval processes for electroceutical devices. These agencies recognize the potential of these devices to address unmet medical needs and have thus implemented policies that facilitate quicker market entry while ensuring patient safety. Recent approvals of pioneering electroceutical devices underscore this supportive stance, providing a robust framework for innovation and commercialization. As a result, companies in this sector are better positioned to bring cutting-edge therapies to market, driving both competitive advantage and market growth.

Latest Trends

Partnerships and Collaborations: Catalysts for Innovation and Market Expansion

Strategic partnerships and collaborations are expected to play a pivotal role in driving the growth and innovation within the electroceuticals market. Leading industry players are increasingly forming alliances with academic institutions, research organizations, and technology firms to leverage their combined expertise and resources. These collaborations are not only enhancing the R&D capabilities but are also accelerating the development of novel electroceutical therapies. For instance, joint ventures between biotech firms and medical device companies are fostering the integration of cutting-edge technology with advanced biological research, paving the way for more effective and personalized treatment options. Additionally, these partnerships are facilitating smoother regulatory approval processes and more robust clinical trial designs, thereby shortening the time-to-market for new therapies.

Increasing Investment and Funding: Fueling Growth and Innovation

The electroceuticals market is witnessing a significant influx of investment and funding, which is crucial for its sustained growth and innovation. Venture capitalists, private equity firms, and governmental grants are increasingly channeling funds into this burgeoning sector. This financial backing is enabling startups and established companies alike to scale their operations, invest in advanced technologies, and expand their product portfolios. The rise in funding is also stimulating research into new therapeutic applications of electroceuticals, such as neuromodulation and bioelectronic medicine. Consequently, increased financial support is expected to accelerate product development cycles and enhance the market's overall competitiveness. Investors are particularly drawn to the promising potential of electroceuticals to address unmet medical needs and improve patient outcomes, which further reinforces the sector's attractiveness.

Regional Analysis

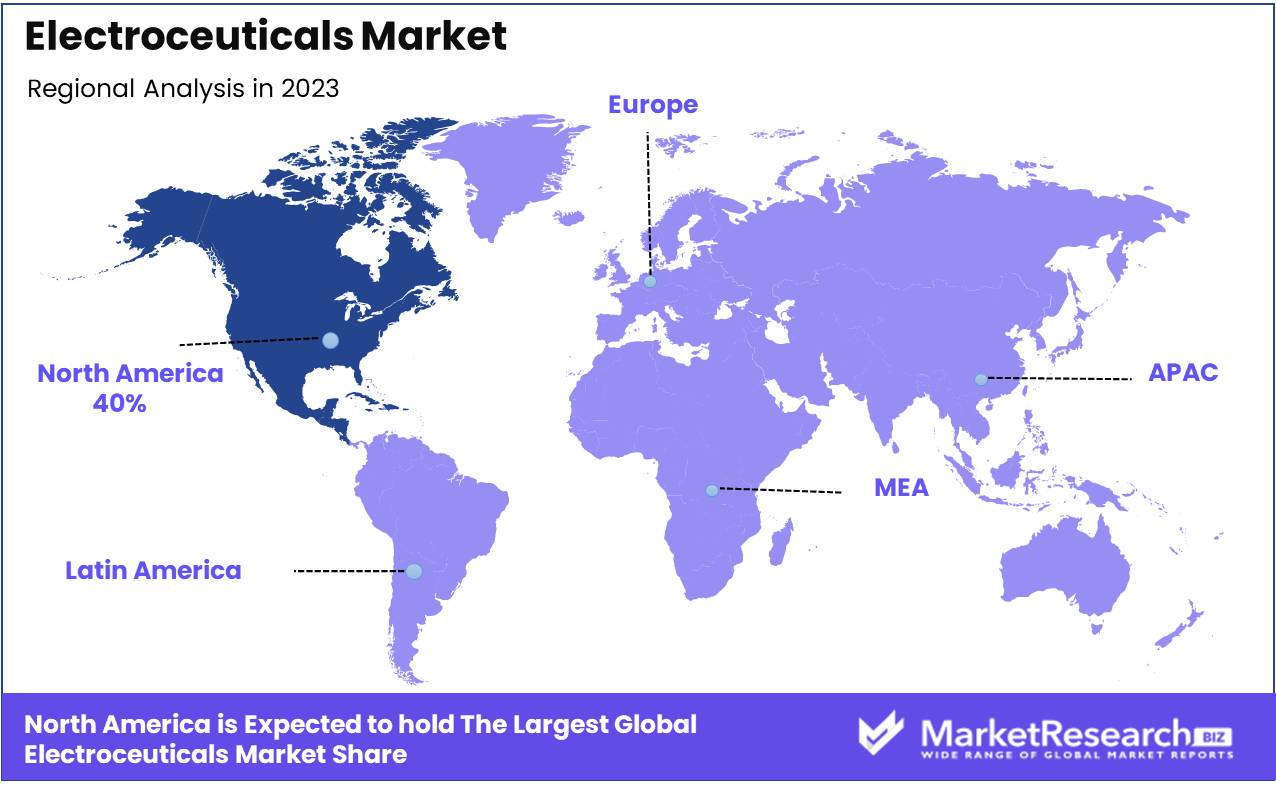

North America leads the global electroceuticals market with a 40% largest share.

The global electroceuticals market, segmented by region, demonstrates varied growth dynamics and opportunities. North America, commanding a significant largest market share of approximately 40%, dominates due to advanced healthcare infrastructure, robust R&D activities, and high adoption rates of innovative medical technologies. The U.S., in particular, drives regional market growth, supported by substantial investments in medical device development and a strong presence of key industry players.

Europe follows, with a market share of around 30%, propelled by the increasing prevalence of chronic diseases, favorable reimbursement policies, and technological advancements. The region benefits from well-established healthcare systems and growing awareness of electroceutical therapies, with countries like Germany, France, and the UK leading the market.

The Asia Pacific region, accounting for roughly 20% of the market, is experiencing rapid growth, fueled by rising healthcare expenditures, expanding medical tourism, and increasing investments in healthcare infrastructure. Key markets such as China, Japan, and India are witnessing significant demand, driven by a growing aging population and an increase in chronic disease cases.

The Middle East & Africa and Latin America regions collectively hold the remaining 10% of the market, with growth driven by improving healthcare facilities, increasing prevalence of neurological and cardiovascular disorders, and rising awareness of advanced treatment options. However, these regions face challenges such as limited healthcare access and economic constraints, which may hinder faster market expansion.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global electroceuticals market is characterized by robust competition among key players, each driving innovation and market expansion through distinct strategic initiatives.

Boston Scientific Corporation and Medtronic maintain their leadership positions by leveraging extensive portfolios and strong R&D capabilities. Their focus on developing advanced neuromodulation devices continues to set industry standards. Abbott and Cochlear Limited excel in the auditory space, with Cochlear Limited leading in cochlear implants. Abbott’s investment in minimally invasive solutions positions it well in the cardiovascular segment.

Livanova Plc and Sonova demonstrate strong growth potential through targeted acquisitions and geographic expansion. Sonova's advancements in hearing aids and cochlear implants reinforce its competitive edge. Emerging players like Axonics Inc. and Electrocore Inc. are gaining traction with innovative solutions in neuromodulation and bioelectronic medicine. Axonics' minimally invasive sacral neuromodulation therapy is particularly noteworthy.

Neuropace Inc. and Medico SRL are making significant strides in responsive neurostimulation for epilepsy, showcasing substantial clinical efficacy. Biotronik and Aleva Neurotherapeutics focus on cardiac rhythm management and deep brain stimulation, respectively, each driving forward technological advancements and clinical outcomes.

Smaller entities like Neurosigma Inc., Biowave Corporation, and Softerix Medical Inc. contribute niche innovations, addressing specific therapeutic needs and enhancing the overall market landscape.

As competition intensifies, strategic collaborations, technological advancements, and expanding therapeutic applications will be pivotal in shaping the future trajectory of the electroceuticals market.

Market Key Players

- Boston Scientific Corporation

- Medtronic

- Abbott

- Cochlear Limited

- Livanova Plc

- Sonova

- Axonics Inc.

- Electrocore Inc.

- Neuropace Inc.

- Medico SRL

- Biotronik

- Aleva Neurotherapeutics

- Neurosigma Inc.

- Biowave Corporation

- Softerix Medical Inc.

- others

Recent Development

- In January 2024, Medtronic received FDA approval for its Percept PC Deep Brain Stimulation (DBS) system. This system is designed to deliver personalized therapy for patients with Parkinson’s disease, enhancing the precision and effectiveness of neurostimulation treatments.

- In May 2023, Abbott received FDA approval for its spinal cord stimulation (SCS) devices aimed at treating chronic back pain. This development marks a significant step forward in expanding the therapeutic applications of electroceuticals to manage chronic pain conditions.

- In February 2023, LivaNova launched the SenTiva DUO, an implantable pulse generator for Vagus Nerve Stimulation (VNS) therapy. This device is intended for patients with drug-resistant epilepsy, providing a new treatment option that leverages the latest in neuromodulation technology.

Report Scope

Report Features Description Market Value (2023) USD 23.7 Billion Forecast Revenue (2033) USD 46.7 Billion CAGR (2024-2032) 7.2% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (Cardiac Pacemakers and Implantable Cardioverter Defibrillators, Cochlear Implants, Spinal Cord Stimulators, Deep Brain Stimulators, Vagus Nerve Stimulators, Sacral Nerve Stimulators, Others), By Device Type (Implantable Devices and Non-invasive Devices), By Application (Arrhythmia, Sensorineural Hearing Loss, Epilepsy, Parkinson's Disease, Others), By End User (Hospitals, Ambulatory Surgical Centers, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Boston Scientific Corporation, Medtronic, Abbott, Cochlear Limited, Livanova Plc, Sonova, Axonics Inc., Electrocore Inc., Neuropace Inc., Medico SRL, Biotronik, Aleva Neurotherapeutics, Neurosigma Inc., Biowave Corporation, Softerix Medical Inc., and others Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Boston Scientific Corporation

- Medtronic

- Abbott

- Cochlear Limited

- Livanova Plc

- Sonova

- Axonics Inc.

- Electrocore Inc.

- Neuropace Inc.

- Medico SRL

- Biotronik

- Aleva Neurotherapeutics

- Neurosigma Inc.

- Biowave Corporation

- Softerix Medical Inc.

- others

Our Clients

View Our Licence Options