Edge Computing Market By Component (Hardware, Software, Services), By Organization Size (SMEs, Large Enterprises), By Application(Smart Cities, Augmented Reality (AR) and Virtual Reality (VR), and Others), By Verticals(BFSI, Manufacturing, Energy & Utilities and Other) By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast Period 2024-2033

-

51244

-

Sept 2024

-

350

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

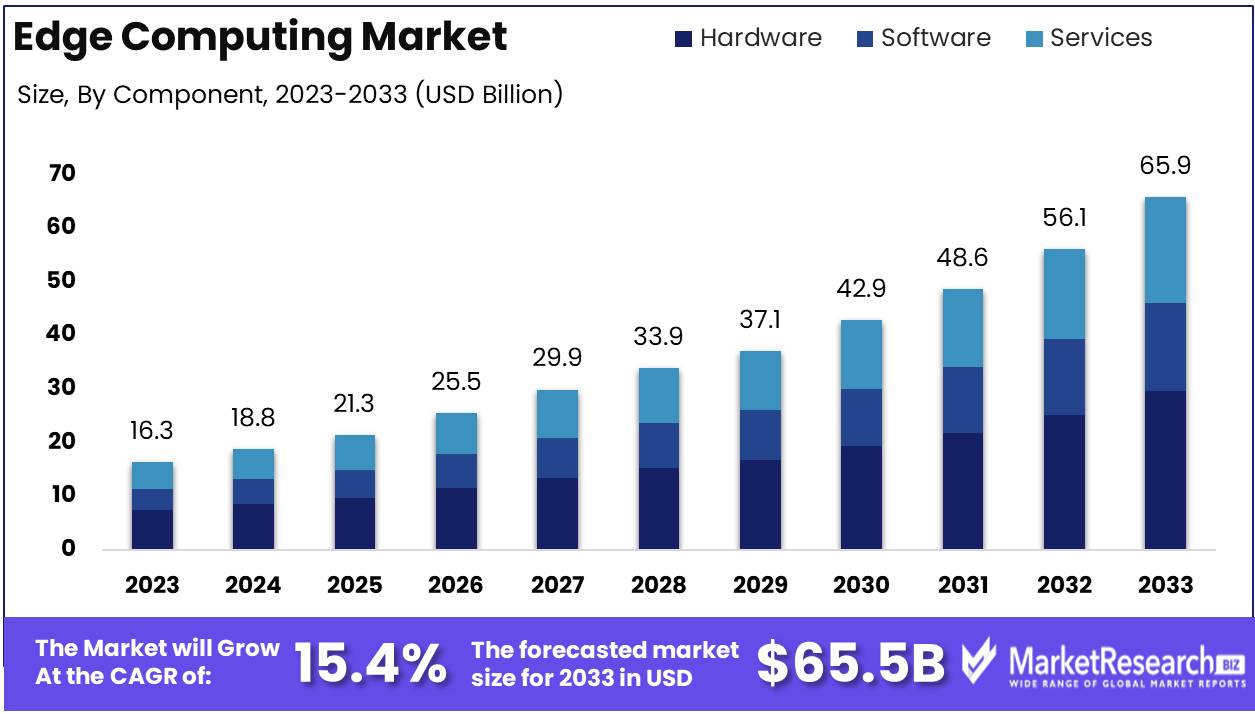

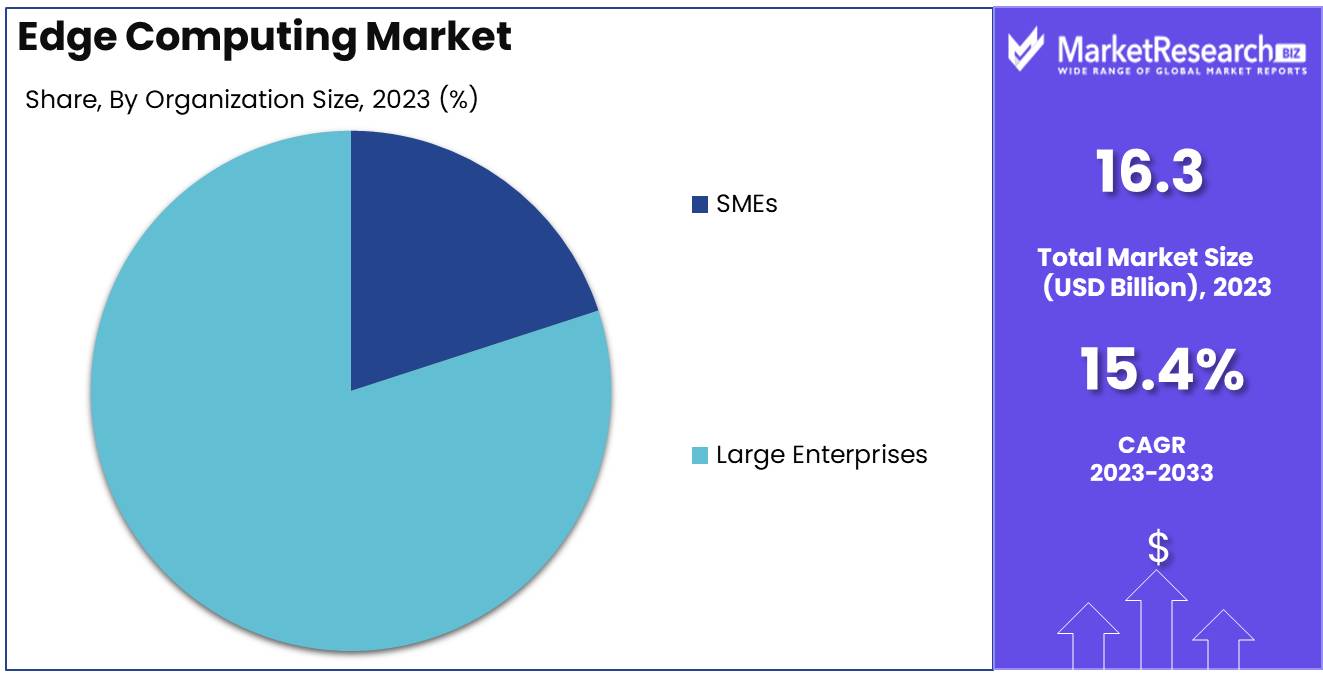

Edge Computing Market size was valued at USD 16.3 Billion in 2023. It is expected to reach USD 65.9 Billion by 2033, with a Compound annual growth rate (CAGR) of 15.4% during the forecast period from 2024 to 2033.

The Edge Computing Market encompasses technologies and solutions that facilitate data processing at or near the source of data generation. This market is driven by the need for real-time computing power and reduced latency in various applications such as IoT, AI, and autonomous systems. Edge computing enhances operational efficiency by enabling swift data analysis and decision-making while minimizing bandwidth usage and dependency on central data centers. The proliferation of connected devices and expanding data volumes underscore the critical role of edge computing in optimizing network architectures, fostering innovations across industries including manufacturing, healthcare, and telecommunications.

The edge computing market is experiencing rapid transformation, fueled by advancements in cloud technology, AI integration, and 5G networks. As enterprises shift from ad hoc approaches to more integrated strategies, edge computing is emerging as a critical enabler of innovation and new revenue streams. Recent research by Accenture highlights the potential of edge computing to accelerate innovation and create differentiated customer experiences when combined with cloud, data, and AI capabilities. This shift allows businesses to leverage distributed computing power at the edge to process data closer to the source, driving efficiency and lowering latency a critical advantage for industries relying on real-time processing, such as IoT and autonomous systems.

Key developments in 2023 and 2024 are driving the expansion of edge infrastructure and capabilities. For example, American Tower's collaboration with IBM, incorporating hybrid cloud solutions and Red Hat OpenShift, aims to facilitate the deployment of edge technologies such as IoT, 5G, and AI. Similarly, the acquisition of Connectria by LightEdge and nLighten's purchase of seven data centers from EXA Infrastructure underscore the growing demand for robust edge infrastructure to support next-generation applications. In Asia, Foxconn's planned high-performance computing center in Taiwan, powered by Nvidia's Blackwell platform, signals a major push towards enhancing edge AI processing capabilities.

Meanwhile, EdgeConneX's $1.4 billion investment to expand in Texas and Intel’s edge computing solution with AT&T further illustrate the increasing focus on edge infrastructure development. Partnerships like the one between Vantiq and Blaize, which aims to democratize real-time AI orchestration, are set to unlock significant market potential, particularly as the integration of AI, IoT, and 5G continues to reshape industries. These efforts point to a future where edge computing becomes a foundational element of digital transformation, enabling enterprises to operate more efficiently, deliver enhanced customer experiences, and tap into new business opportunities.

Key Takeaways

- Market Growth: The Edge Computing Market is projected to grow from USD 16.3 billion in 2023 to USD 65.9 billion by 2033, at a CAGR of 15.4% during the forecast period.

- By Component : Hardware holds the largest share in the Edge Computing Market at 44.6%, emphasizing its pivotal role in establishing robust edge infrastructure.

- By Organization Size: Large Enterprises dominate the Edge Computing Market with an 80.4% share, underscoring their significant investment in edge technologies to enhance operational efficiencies.

- By Application Analysis: IIoT leads the application segments with 28% of the market share, highlighting its critical role in industrial automation and real-time data processing.

- By Verticals Analysis: Energy & Utilities sector leads with over 16% market share, driven by the need for real-time data management and operational efficiency in smart grids and renewable energy.

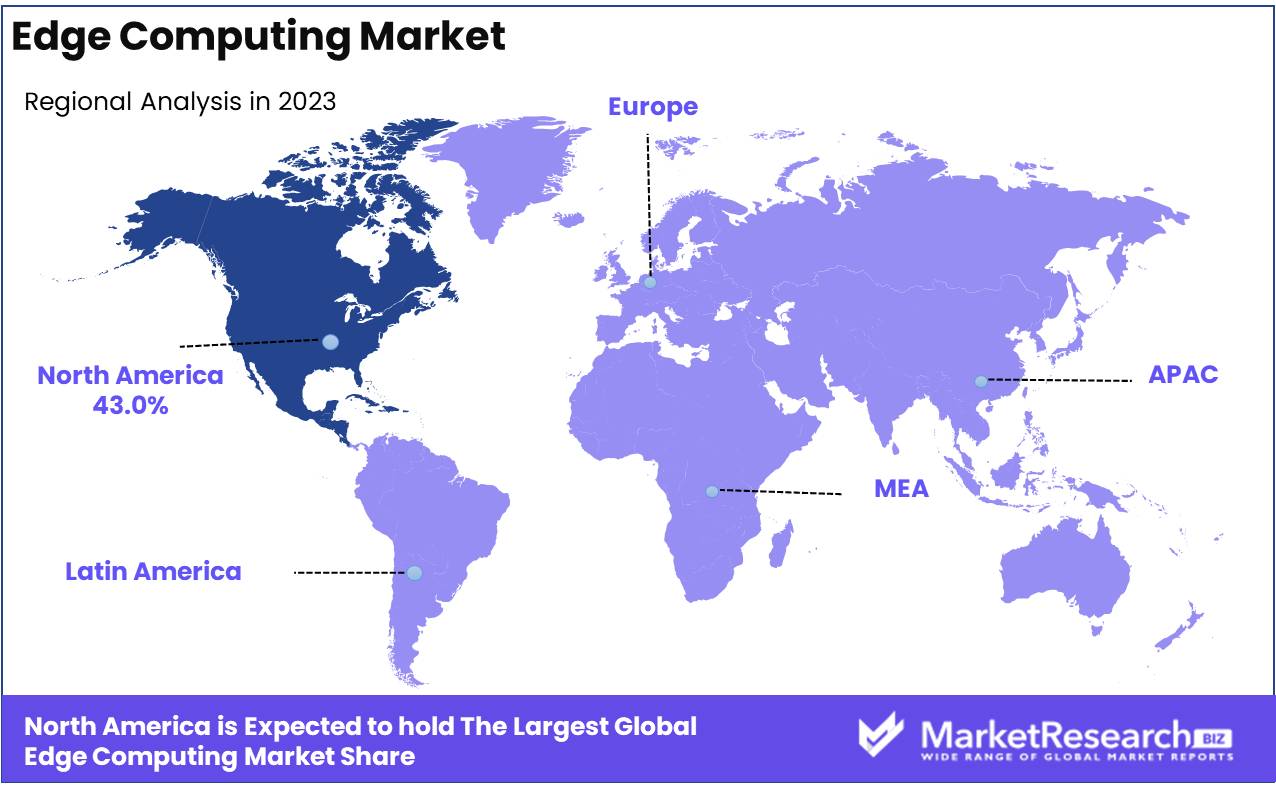

- Regional Analysis: North America remains the frontrunner in the Edge Computing Market, holding a 43.0% share, propelled by rapid advancements in IoT and 5G technologies.

- Growth Opportunities and Driving Factors: The integration of IoT is a significant growth driver, with the proliferation of connected devices necessitating robust edge computing solutions to handle real-time data processing efficiently.

- Restraining Factors: Network Connectivity Challenges: Limited network connectivity is a major barrier, hindering the effective deployment of edge computing solutions in real-time data processing scenarios.

Driving Factors

5G Technology Deployment

The global deployment of 5G technology is one of the primary catalysts for the accelerated growth of the edge computing market. 5G offers significantly lower latency and higher bandwidth compared to its predecessors, which enables real-time data processing and the ability to support a vast number of connected devices. This makes edge computing, which brings computation closer to the source of data, more efficient and scalable.

By providing the necessary network infrastructure for faster and more reliable data transmission, 5G not only improves the performance of edge computing solutions but also broadens their application across industries like manufacturing, healthcare, and autonomous vehicles. These sectors rely heavily on real-time analytics and near-instantaneous processing, which edge computing and 5G together make possible.

Moreover, the deployment of 5G allows for the management of the increasing volume of data generated by IoT devices (discussed below), amplifying edge computing’s role in reducing network congestion and improving overall system efficiency. In this sense, the symbiotic relationship between 5G and edge computing lays the foundation for widespread adoption and operationalization across sectors, particularly in smart cities, logistics, and retail.

Increasing Adoption of IoT Devices

The growing number of Internet of Things (IoT) devices is another pivotal factor driving the growth of the edge computing market. By 2030, the number of IoT-connected devices is projected to reach 24.1 billion, generating an immense volume of data that requires localized processing to minimize latency and improve responsiveness. Edge computing addresses this need by processing data close to the device, reducing the burden on centralized data centers and enabling real-time decision-making.

IoT devices are widely adopted across industries such as manufacturing, healthcare, and agriculture, where the need for immediate data insights is paramount. For example, in industrial IoT (IIoT) settings, edge computing allows for the monitoring of equipment and predictive maintenance in real time, enhancing operational efficiency and reducing downtime. In healthcare, IoT devices used for patient monitoring generate continuous streams of data that edge computing can process on-site, improving the speed and accuracy of diagnoses.

The rise in IoT adoption amplifies the need for scalable, low-latency infrastructure, a demand that edge computing fulfills by offloading data processing from central servers to local nodes. This trend, combined with 5G’s ability to manage large volumes of device connections efficiently, creates a compelling case for the continued integration of edge computing into IoT ecosystems, further propelling market growth.

Restraining Factors

Network Connectivity Challenges

Network connectivity remains a fundamental challenge in the expansion of the edge computing market. Effective edge computing requires robust and continuous network connections to process and relay data between edge devices and central data centers. Limited connectivity in remote or underdeveloped areas can severely restrict the real-time data processing capabilities that are hallmark of edge computing solutions. A lack of reliable connectivity not only affects the performance but also limits the adoption of edge technology in regions that could benefit the most from its deployment.

This challenge is particularly pronounced in industries where real-time data and processing are critical, such as autonomous vehicles, manufacturing, and healthcare. For instance, in healthcare, edge computing is instrumental for remote monitoring and real-time data analysis, but connectivity issues can hinder the reliability of these services, impacting patient care. The ongoing expansion of 5G networks could alleviate some of these challenges by providing faster, more reliable connections that enhance the capabilities of edge computing devices.

Data Security and Privacy Concerns

Data security and privacy concerns are significant restraining factors in the edge computing market. As data processing moves closer to the source of data collection, it bypasses some of the centralized security measures that protect data within core networks. This decentralization exposes data to new vulnerabilities, making it a prime target for cyber-attacks. The proliferation of IoT devices increases the risk, as many devices lack robust built-in security.

The impact of these concerns is felt across multiple sectors, particularly in industries handling sensitive information, such as finance, healthcare, and government. For example, financial institutions using edge computing for faster transaction processing must ensure that data breaches do not compromise client data integrity. Similarly, in healthcare, protecting patient information while utilizing edge computing for real-time health monitoring is crucial. The industry's response has been to invest in advanced security protocols and AI-driven security solutions that predict and mitigate potential threats at the edge. This is creating a sub-market within the edge computing landscape focused on security solutions, thereby influencing both market growth and technological evolution.

By Component Analysis

Hardware Segment Dominates Edge Computing Market in 2023 with 44.6% Largest Share

In 2023, Hardware held a dominant market position within the "By Component" segment of the global edge computing market, capturing over 44.6% of the market share. This strong performance underscores the critical role that physical infrastructure such as edge devices, gateways, and servers plays in supporting the deployment and functionality of edge computing solutions. The increasing demand for processing power at the network’s edge, particularly for applications requiring low latency and real-time data processing, has driven substantial investment in high-performance edge hardware.

The Software segment followed closely, contributing significantly to the market's growth. Software solutions, including edge orchestration platforms, security frameworks, and application development environments, have seen rising adoption. As enterprises seek to optimize and manage edge infrastructure, software solutions are crucial for enabling the seamless integration of edge devices with centralized cloud services, enhancing scalability and operational efficiency.

Services also represented a key component of the edge computing ecosystem in 2023. The service segment, encompassing consulting, implementation, and managed services, accounted for a notable share of the market as organizations increasingly rely on external expertise to deploy and manage complex edge architectures. This trend reflects the growing need for specialized knowledge and support in configuring, maintaining, and securing edge environments to meet evolving business and technical requirements.

Together, these components Hardware, Software, and Services constitute the backbone of the edge computing market, each playing a distinct role in enabling the real-time processing and analysis of data at the network edge.

By Organization Size Analysis

Large Enterprises Segment Dominates Edge Computing Market in 2023 with 80.4% Largest Share

In 2023, Large Enterprises held a dominant market position within the "By Organization Size" segment of the global edge computing market, capturing more than 80.4% of the market share. This strong foothold can be attributed to the substantial resources large organizations allocate toward advanced technologies like edge computing. These enterprises leverage edge computing solutions to enhance operational efficiency, improve data processing at the network's edge, and support real-time decision-making in sectors such as manufacturing, healthcare, and financial services.

In contrast, Small and Medium-sized Enterprises (SMEs) represented a smaller portion of the market. While their adoption of edge computing solutions is growing, SMEs typically face budgetary constraints and challenges related to infrastructure scalability. However, the increasing availability of flexible, cloud-integrated edge solutions tailored to SMEs' needs is expected to drive further adoption in this segment in the coming years.

The large enterprises’ commanding market share highlights their focus on integrating cutting-edge technologies to gain competitive advantages, particularly in industries where real-time data processing is essential for maintaining operational efficiency, reducing latency, and enhancing customer experiences.

By Application Analysis

Industrial Internet of Things (IIoT) Leads Edge Computing Market in 2023 with 28% Largest Share

In 2023, the Industrial Internet of Things (IIoT) held a dominant market position within the "By Application" segment of the global edge computing market, capturing more than 28% of the market share. The IIoT’s leadership can be attributed to the increasing integration of edge computing solutions within industrial environments, such as manufacturing, energy, and transportation sectors. Edge computing is essential for enabling real-time data processing and analytics on factory floors, optimizing operations, reducing downtime, and ensuring more efficient use of resources.

The Smart Cities segment also accounted for a notable portion of the market. Municipalities worldwide are adopting edge computing to enhance urban infrastructure, improve traffic management, and support smart utilities, all requiring low-latency data processing at the network’s edge.

Augmented Reality (AR) and Virtual Reality (VR) applications are another emerging area within edge computing, particularly in fields like healthcare, gaming, and education. The need for minimal latency and high computational power at the edge to deliver immersive experiences is driving growth in this segment.

Remote Monitoring solutions, often used in sectors such as energy, agriculture, and logistics, are benefiting from edge computing by enabling real-time surveillance and condition monitoring of distributed assets, reducing reliance on centralized cloud systems for processing.

Other applications such as autonomous vehicles and content delivery networks (CDNs) also play significant roles in driving edge computing adoption, though their market share remains smaller compared to IIoT.

The IIoT's prominent position underscores the transformative impact of edge computing in industrial sectors, where real-time, data-driven decision-making is becoming a critical component of competitive advantage.

By Industry Vertical Analysis

Energy & Utilities Segment Leads Edge Computing Market in 2023 with Over 16% largest Market Share

In 2023, the Energy & Utilities sector held a dominant market position within the by Industry Vertical segment of the global edge computing market, capturing more than 16% of the market share. The sector's significant adoption of edge computing is driven by the growing need for real-time data processing in smart grids, energy distribution, and renewable energy management. Edge computing enables these companies to efficiently monitor, analyze, and optimize energy use while ensuring minimal latency in critical infrastructure operations.

The Manufacturing vertical followed closely, as edge computing has become integral to enabling Industry 4.0 initiatives. Manufacturers are leveraging edge computing to enhance predictive maintenance, optimize production processes, and improve overall equipment effectiveness (OEE) in real time, thereby driving operational efficiency.

BFSI (Banking, Financial Services, and Insurance) is another key adopter, utilizing edge computing to enhance fraud detection, streamline financial transactions, and enable secure, real-time data processing at distributed locations such as ATMs and branch offices.

Government & Defense and Telecommunications sectors also made significant contributions to the market. Governments are deploying edge solutions for smarter infrastructure management and critical defense applications, while telecommunications providers use edge computing to improve network performance, particularly in 5G rollouts.

Other notable verticals include Healthcare & Life Sciences, where edge computing supports telemedicine and real-time diagnostics, Retail & Consumer Goods, which benefit from improved customer engagement through edge-powered analytics, and Media & Entertainment, which are harnessing edge capabilities for content delivery and immersive experiences.

The Energy & Utilities sector's leading position reflects the critical need for efficient, real-time data processing in an increasingly decentralized and digitized energy landscape, positioning edge computing as a key enabler of innovation in this space.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Organization Size

- SMEs

- Large Enterprises

By Application

- Smart Cities

- Augmented Reality (AR) and Virtual Reality (VR)

- Industrial Internet of Things (IIoT)

- Remote Monitoring

- Others

By Industry Vertical

- BFSI

- Manufacturing

- Energy & Utilities

- Government & Defense

- Telecommunications

- Media & Entertainment

- Retail & Consumer Goods

- Transportaion & Logistics

- Healthcare & Life Sciences

- Other

Growth Opportunity

IoT Integration

One of the primary growth drivers for edge computing in 2024 is the increasing adoption of the Internet of Things (IoT). As organizations deploy millions of connected devices across industries like healthcare, manufacturing, and smart cities, the demand for local data processing will escalate. Edge computing enables efficient, real-time analytics by processing data closer to the source, reducing the reliance on centralized cloud infrastructures. This trend is particularly critical in sectors where real-time insights and rapid decision-making are paramount, unlocking new use cases for predictive maintenance, asset tracking, and autonomous systems.

Low Latency Requirements

Edge computing’s ability to reduce latency is another key factor driving market expansion. Applications such as autonomous vehicles, industrial automation, and augmented reality require near-instantaneous data processing, which cannot be achieved with traditional cloud models. By minimizing the distance data must travel, edge computing ensures that latency-sensitive applications operate seamlessly. In 2024, this shift is expected to fuel greater adoption in high-speed, data-intensive industries such as telecommunications, finance, and gaming.

Latest Trends

Demand for Low-Latency Processing

As organizations continue to adopt digital-first strategies, the demand for low-latency processing is becoming paramount. In 2024, the need to process data in real-time, particularly in industries like autonomous vehicles, healthcare, and manufacturing, is driving growth in the edge computing market. Enterprises are seeking faster data insights with minimal delays, reducing the dependency on cloud infrastructure. By processing data closer to the source, edge computing offers significant advantages in reducing response times, enhancing user experiences, and improving operational efficiency.

Integration of AI and Machine Learning

One of the most transformative trends in the edge computing landscape is the integration of artificial intelligence (AI) and machine learning capabilities. These technologies enable edge devices to perform real-time data analytics and decision-making directly at the network edge, minimizing the need for data transmission to centralized servers. This development empowers businesses to extract actionable insights at unprecedented speeds. AI-powered edge computing is especially crucial for industries relying on predictive maintenance, video analytics, and smart cities. It helps optimize operations, reduce costs, and improve decision-making processes, all while maintaining data security and compliance.

Regional Analysis

Edge Computing Market North America Leads with 43.0% Market Share

North America holds the largest Market share of the global edge computing market, representing approximately 43.0% of the market revenue. This dominance is largely due to the robust presence of major technology companies, early adoption of IoT, and significant investments in cloud and edge infrastructure. The United States leads within North America, followed by Canada, with advancements in 5G technology and initiatives in smart cities propelling demand. The rest of North America also contributes to market growth, with government initiatives promoting edge computing solutions across various sectors.

In Europe, nations such as Germany, France, the UK, and the Netherlands are pivotal in the region's increasing involvement in edge computing. The focus here is on boosting industrial automation, smart manufacturing, and energy management systems, particularly within Industry 4.0 applications. The rest of Europe, including Spain, Russia, and Italy, is progressively embracing edge technologies, especially in transportation & logistics, to enhance operational efficiency and reduce latency.

The Asia-Pacific region is witnessing the fastest growth in the edge computing market, driven by rapid digital transformation and burgeoning IoT adoption in countries like China, Japan, South Korea, and India. China is at the forefront, with substantial government initiatives promoting smart infrastructure, while Japan and South Korea utilize 5G to expedite the adoption of edge technology in sectors such as automotive, manufacturing, and telecommunications. The rest of the Asia-Pacific, including nations like Singapore, Thailand, and Vietnam, displays strong potential, particularly in smart city projects and industrial automation.

In South America, markets in Mexico and Brazil are primary catalysts for the adoption of edge computing, with increasing investments in telecommunications and IT infrastructure. The focus in this region is on leveraging edge computing to enhance connectivity and service delivery, especially in remote areas. The rest of South America is gradually embracing edge solutions, particularly in industries like agriculture, energy, and manufacturing.

The Middle East & Africa region is emerging as a significant market for edge computing, with countries like Saudi Arabia, the UAE, and South Africa leading the way. The development of smart cities, coupled with extensive IoT deployments in industries such as oil & gas and telecommunications, is driving market growth. The rest of the Middle East & Africa is slowly adopting edge technologies, with rising investments in cloud infrastructure and digital transformation initiatives to promote economic growth and sustainability across various sectors.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2024, the global edge computing market is witnessing robust growth, driven by the accelerating demand for real-time data processing and low-latency solutions. Several key players are at the forefront of this transformation, each leveraging their unique capabilities to address the evolving needs of industries across sectors.

Amazon Web Services (AWS) and Microsoft Corporation dominate the cloud-to-edge continuum, providing scalable infrastructure and edge-specific solutions that empower businesses to process data closer to the source. AWS's "AWS Greengrass" and Microsoft's "Azure IoT Edge" are pivotal in expanding the edge ecosystem, enhancing their leadership in cloud computing.

Cisco Systems, Inc. and Huawei Technologies Co. Ltd. are integral to the networking and connectivity landscape. Their expertise in edge routers, switches, and gateways provides the backbone for seamless data transmission, essential for the growth of the Internet of Things (IoT) and industrial edge applications.

On the industrial front, General Electric and Siemens AG play a crucial role, particularly in integrating edge computing into manufacturing and industrial processes. Their focus on industrial automation, coupled with edge intelligence, improves operational efficiency and predictive maintenance.

Companies like IBM Corporation, Hewlett Packard Enterprise (HPE), and Intel Corporation are pushing the boundaries of edge hardware and software integration, offering cutting-edge solutions that drive innovation in sectors such as healthcare, finance, and retail.

Finally, ABB, Rockwell Automation, and Honeywell International provide specialized industrial solutions, incorporating edge capabilities into their automation and control systems, thereby streamlining processes and enhancing productivity in mission-critical environments.

Market Key Players

- ABB

- Amazon Web Services (AWS), Inc.

- Aricent, Inc.

- Atos

- Cisco Systems, Inc.

- General Electric Company

- Hewlett Packard Enterprise Development

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- Rockwell Automation, Inc

- SAP SE

- Siemens AG

- Other

Recent Developments

- Accenture (2023): New research from Accenture (NYSE: ACN) revealed on September 13, 2023, emphasizes that edge computing is poised to accelerate innovation and create new revenue opportunities through integrated approaches leveraging cloud, data, and AI. This integration is crucial for accelerating edge innovation affordably and delivering differentiated experiences.

- American Tower (2023): American Tower announced a collaboration with IBM to expand its neutral-host, Access Edge Data Center ecosystem to incorporate IBM Hybrid Cloud capabilities and Red Hat OpenShift. This initiative, aimed at enabling technologies such as IoT, 5G, AI, and network automation, enhances service offerings to customers.

- LightEdge (2024): In April 2024, LightEdge advanced its cloud and colocation services by acquiring Connectria. This acquisition is designed to strengthen its edge infrastructure capabilities.

- nLighten (2024): Concurrently in April 2024, nLighten acquired seven data centers from EXA Infrastructure, aiming to enhance its presence in European edge computing markets.

- Foxconn (2024): In June 2024, Foxconn announced plans to construct a high-performance computing center in Taiwan, utilizing Nvidia’s Blackwell platform. This new facility is expected to boost edge AI processing capabilities, furthering the edge computing goals of both Foxconn and Nvidia.

Report Scope

Report Features Description Market Value (2023) USD 16.3 Bn Forecast Revenue (2033) USD 65.9 Bn CAGR (2024-2032) 15.4% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component(Hardware, Software, Services), By Organization Size (SMEs, Large Enterprises), By Application(Smart Cities, Augmented Reality (AR) and Virtual Reality (VR), Industrial Internet of Things (IIoT), Remote Monitoring, Others), By Verticals(BFSI, Manufacturing, Energy & Utilities, Government & Defense, Telecommunications, Media & Entertainment, Retail & Consumer Goods, Transportaion & Logistics, Healthcare & Life Sciences, Other) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape ABB, Amazon Web Services (AWS), Inc., Aricent, Inc., Atos, Cisco Systems, Inc., General Electric Company, Hewlett Packard Enterprise Development, Honeywell International Inc., Huawei Technologies Co. Ltd., IBM Corporation, Intel Corporation, Microsoft Corporation, Rockwell Automation, Inc, SAP SE, Siemens AG, Other Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- ABB

- Amazon Web Services (AWS), Inc.

- Aricent, Inc.

- Atos

- Cisco Systems, Inc.

- General Electric Company

- Hewlett Packard Enterprise Development

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- Rockwell Automation, Inc

- SAP SE

- Siemens AG

- Other

Our Clients

View Our Licence Options