Edge Computing in Healthcare Market By Component (Hardware, Software, Services), By Application (Telehealth & Remote Patient Monitoring, Diagnostics, Robotic Surgery, Ambulances, Others), By End User (Hospitals & Clinics, Long-term Care Centers & Home Care Settings, Ambulatory Care Centers, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

51400

-

September 2024

-

300

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

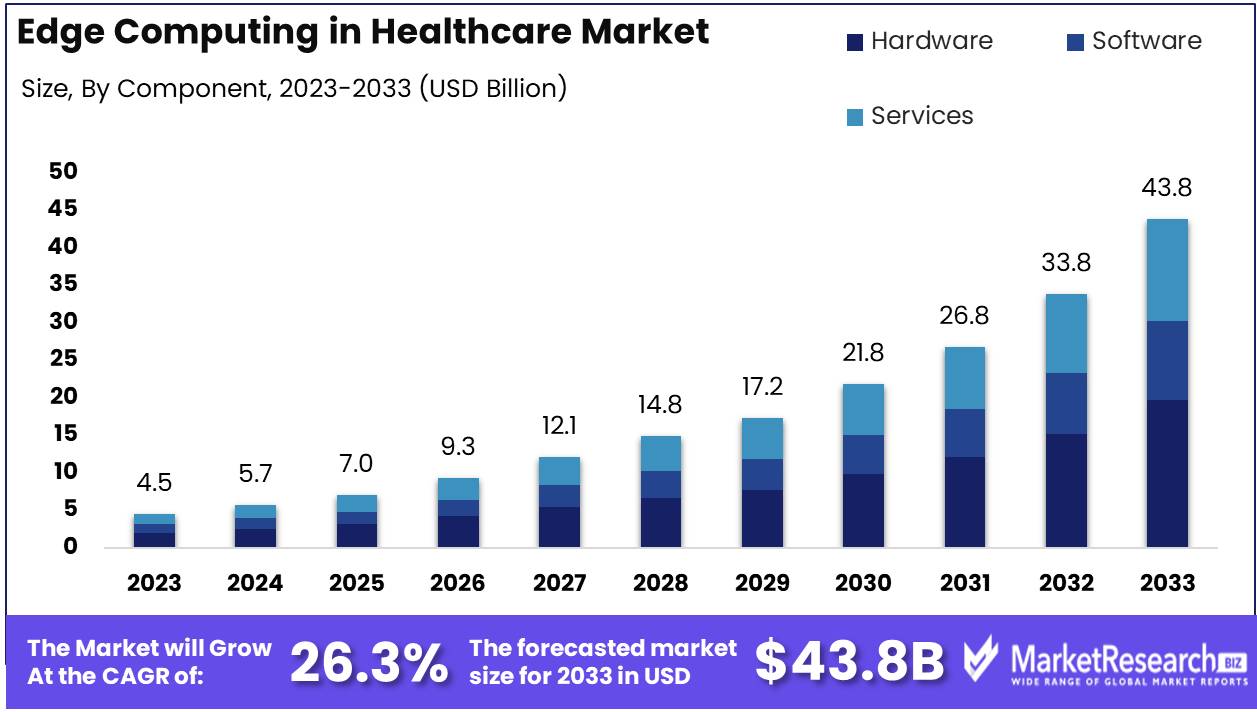

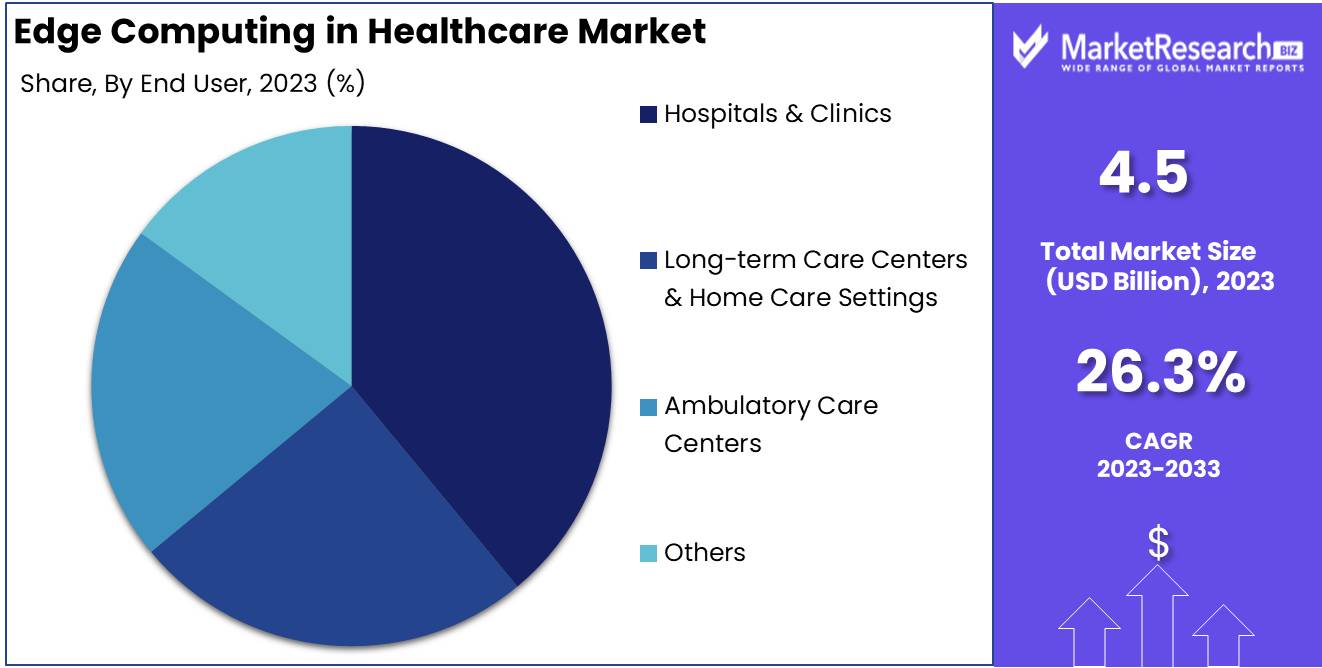

The Edge Computing in Healthcare Market was valued at USD 4.5 billion in 2023. It is expected to reach USD 43.8 billion by 2033, with a CAGR of 26.3% during the forecast period from 2024 to 2033.

Edge computing in healthcare refers to the decentralized processing of data near the source of data generation, such as medical devices or sensors, instead of relying solely on centralized cloud-based systems. This approach reduces latency, enhances real-time decision-making, and improves data security by processing sensitive patient information locally. Edge computing enables healthcare providers to deliver faster, more personalized care, optimize remote monitoring, and support the growing use of IoT devices in medical settings.

The Edge Computing in Healthcare Market is poised for significant growth, driven by the increasing adoption of IoT and wearable devices, which generate vast amounts of patient data that demand real-time processing. The rising need for real-time analytics in healthcare, particularly for critical applications like remote monitoring and telemedicine, has underscored the value of edge computing by reducing latency and enabling faster decision-making. This shift towards decentralized healthcare models is further supported by advancements in AI and machine learning, which are increasingly being integrated at the edge to optimize diagnostics, personalize treatments, and enhance operational efficiencies. However, the complex integration of edge computing with existing legacy systems remains a significant challenge for healthcare providers, requiring considerable investment and expertise to ensure seamless interoperability.

The market’s expansion is further bolstered by the focus on decentralized healthcare, which aims to bring healthcare services closer to the patient, especially in underserved regions. Edge computing facilitates this by processing data locally, minimizing the need for large-scale centralized data centers and improving service delivery in real-time. As healthcare continues to embrace digital transformation, edge computing is expected to play a crucial role in supporting these efforts, addressing the increasing data load from connected devices and enabling more efficient and responsive healthcare services. While challenges such as integration complexity persist, the benefits of real-time analytics, enhanced AI capabilities, and decentralized care are likely to drive the broader adoption of edge computing in the healthcare sector.

Key Takeaways

- Market Growth: The Edge Computing in Healthcare Market was valued at USD 4.5 billion in 2023. It is expected to reach USD 43.8 billion by 2033, with a CAGR of 26.3% during the forecast period from 2024 to 2033.

- By Component: Hardware dominated edge computing in healthcare by component.

- By Application: Telehealth & Remote Patient Monitoring dominated healthcare edge computing applications.

- By End User: Hospitals & Clinics dominated edge computing adoption in healthcare.

- Regional Dominance: North America dominates the Edge Computing in the Healthcare market, leading with a 40% share.

- Growth Opportunity: The adoption of edge computing in healthcare is accelerating due to its ability to enhance real-time remote patient monitoring, improve data management, and address security concerns, driven by IoMT device integration.

Driving factors

Rising Acceptance of IoT Medical Devices Driving Edge Computing Integration

The increasing adoption of IoT-enabled medical devices is a significant driver of Edge Computing in the Healthcare market. As IoT devices proliferate in healthcare settings, the volume of data generated from these devices, such as wearables, sensors, and diagnostic tools, has surged. This data, which includes critical patient information, needs to be processed and analyzed efficiently to ensure timely and accurate clinical decisions. Edge computing plays a pivotal role in managing this data deluge by enabling decentralized processing, where data is processed closer to the source (i.e., at the edge), reducing latency and alleviating the strain on central data centers.

According to market data, the global IoT in healthcare market is expected to grow at a CAGR of 19.9% from 2021 to 2028. This growth in IoT usage is directly fueling the demand for edge computing solutions in healthcare, as these solutions ensure that data is processed in real time without overburdening the central cloud infrastructure. The convergence of IoT and edge computing is thus creating a seamless ecosystem where healthcare providers can access vital patient information instantly, improving patient outcomes and operational efficiency.

Increasing Need for Real-Time Data Processing Accelerates Adoption

In healthcare, real-time data processing is crucial for applications such as remote monitoring, telemedicine, and emergency care. The ability to analyze and act on data in real time is often a matter of life and death in medical scenarios, and edge computing addresses this challenge by minimizing the latency involved in data transmission to centralized cloud systems. For example, in cases of remote patient monitoring, edge computing ensures that critical data like heart rate, glucose levels, or blood pressure are processed immediately, allowing healthcare professionals to respond swiftly to any abnormalities.

The need for real-time data processing is becoming more pressing as healthcare providers increasingly rely on data-driven technologies such as artificial intelligence (AI) and machine learning (ML) for diagnostics and decision support. By processing data closer to the point of care, edge computing ensures that AI and ML algorithms can operate in real time, providing immediate insights and improving the speed and accuracy of diagnoses. This capability is expected to significantly enhance patient care, particularly in critical care environments and emergency situations, thus driving the growth of edge computing in healthcare.

Enhanced Data Privacy and Security Fuels Market Expansion

Healthcare organizations face stringent regulatory requirements regarding patient data privacy and security, such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States and the General Data Protection Regulation (GDPR) in Europe. With the growing volume of sensitive medical data generated by IoT devices, securing this data has become paramount. Edge computing offers a solution by processing data locally rather than sending it to centralized cloud servers, thus reducing the risk of data breaches during transmission.

By keeping sensitive data closer to the source and implementing security measures at the edge, healthcare organizations can better comply with data protection regulations while minimizing vulnerabilities. Additionally, edge computing allows healthcare facilities to employ advanced encryption, firewall, and anomaly detection protocols more efficiently on localized data, significantly enhancing the security posture of healthcare systems. This focus on data privacy and security is a key factor driving the adoption of edge computing in healthcare, as it helps institutions mitigate the risks of cyberattacks while ensuring regulatory compliance.

Restraining Factors

High Capital Expenditure (CAPEX) as a Barrier to Market Expansion

The significant capital expenditure associated with the deployment of edge computing in healthcare acts as a key restraining factor for market growth. The implementation of edge computing requires substantial investments in infrastructure, including hardware, software, and network architecture. For many healthcare organizations, particularly smaller facilities and clinics, these upfront costs can be prohibitive. According to industry reports, the initial outlay for edge computing can range from hundreds of thousands to several million dollars, depending on the scale of implementation. This high cost is further compounded by the ongoing expenses related to maintenance, updates, and cybersecurity measures.

Moreover, healthcare organizations often operate on tight budgets, with many prioritizing other critical investments such as medical equipment, staffing, and patient care technologies. As a result, the allocation of large portions of their budget to edge computing infrastructure becomes challenging. The financial pressure on organizations to justify these costs, alongside the risk of not achieving a return on investment within a reasonable timeframe, may limit the speed and scale at which edge computing is adopted within the healthcare sector. Consequently, this financial burden hinders the widespread implementation of edge computing, slowing the overall growth of the market.

Cultural Resistance to Change Slows Adoption

The adoption of edge computing in healthcare is also hindered by cultural resistance to change. Healthcare providers and organizations are often conservative in adopting new technologies, particularly when it involves major operational changes. The healthcare industry is known for its reliance on proven, established processes and systems that prioritize patient safety and data security. Introducing edge computing requires a paradigm shift in how data is processed, stored, and analyzed, which may lead to apprehension among stakeholders.

Medical professionals and administrators may be reluctant to transition from traditional cloud-based or on-premises computing to edge computing, given concerns about data integrity, security, and the learning curve associated with the new technology. Additionally, integrating edge computing into existing healthcare workflows demands significant staff training, which can lead to disruptions in daily operations. These disruptions, along with a fear of compromising patient care due to unfamiliarity with the new technology, contribute to the slow adoption of edge computing solutions.

By Component Analysis

In 2023, Hardware dominated edge computing in healthcare by component.

In 2023, Hardware held a dominant market position in the By Component segment of Edge Computing in the Healthcare Market. The hardware segment includes essential components such as edge servers, gateways, sensors, and storage devices, which are critical for real-time data processing at the edge of healthcare networks. The growing need for real-time patient monitoring and faster diagnostic results, coupled with the rise of IoT devices in hospitals and clinics, has propelled hardware demand in this market.

Meanwhile, the software segment is witnessing significant growth as healthcare organizations increasingly adopt AI-driven analytics, data management tools, and security software to enhance operational efficiency and data security. As edge computing deployments expand, software is becoming a vital enabler of seamless integration and data processing.

The services segment, comprising consulting, deployment, and maintenance, is expected to grow steadily due to the increasing complexity of edge computing infrastructure. Healthcare providers are investing in service solutions to ensure the proper implementation and long-term sustainability of their edge computing systems. Together, these components are transforming healthcare operations by enabling faster, decentralized data processing and decision-making at the network edge.

By Application Analysis

In 2023, Telehealth & Remote Patient Monitoring dominated healthcare edge computing applications.

In 2023, Telehealth & Remote Patient Monitoring held a dominant market position in the By Application segment of the Edge Computing in Healthcare Market. The demand for telehealth surged due to the need for remote patient care, particularly in the wake of the COVID-19 pandemic. Enhanced connectivity, combined with edge computing, allowed for real-time monitoring of patients, reducing the burden on healthcare facilities and ensuring continuous care. The increased adoption of wearable devices and smart health technologies further fueled the growth in this segment.

Diagnostics also saw significant advancements, as edge computing enabled faster and more accurate data analysis for disease detection and management. AI-driven edge devices improved diagnostic capabilities, leading to more personalized treatments.

Robotic Surgery benefited from the low-latency capabilities of edge computing, allowing for more precise and remote-controlled surgical interventions. This technology has been especially useful in complex, minimally invasive surgeries.

In Ambulances, edge computing allowed real-time data transmission from the field to hospitals, improving emergency response times and patient outcomes.

Lastly, the Others segment, which includes applications such as medical imaging and pharmaceutical research, also leveraged edge computing for better operational efficiencies. Overall, edge computing in healthcare has enhanced the effectiveness of medical interventions and patient care across multiple applications.

By End User Analysis

In 2023, Hospitals & Clinics dominated edge computing adoption in healthcare.

In 2023, Hospitals & Clinics held a dominant market position in the By End User segment of the Edge Computing in Healthcare Market. This dominance can be attributed to the increasing adoption of advanced computing technologies to enhance real-time data processing, diagnostics, and treatment capabilities within these settings. Hospitals and clinics are leveraging edge computing for applications such as AI-driven imaging, predictive analytics, and remote patient monitoring, significantly improving operational efficiency and patient outcomes.

The Long-term Care Centers & Home Care Settings segment is also gaining traction as the demand for personalized and remote care continues to rise. Edge computing enables these facilities to manage large volumes of patient data locally, ensuring faster decision-making and improved patient care.

Ambulatory Care Centers are utilizing edge computing to streamline workflows, reduce latency in accessing critical information, and optimize patient management systems, which further enhances care delivery outside traditional hospital environments.

Lastly, the Others category, encompassing specialized healthcare facilities and diagnostic centers, is expected to see gradual adoption of edge computing technologies as the benefits of real-time data processing become more apparent. These settings are likely to experience growth driven by the need for precision medicine and the integration of IoT devices in healthcare.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Application

- Telehealth & Remote Patient Monitoring

- Diagnostics

- Robotic Surgery

- Ambulances

- Others

By End User

- Hospitals & Clinics

- Long-term Care Centers & Home Care Settings

- Ambulatory Care Centers

- Others

Growth Opportunity

Telehealth and Remote Patient Monitoring

The widespread adoption of telehealth services has accelerated the need for edge computing solutions, particularly for remote patient monitoring. As healthcare providers increasingly rely on real-time data to monitor patients outside traditional clinical settings, edge computing allows for the processing of this data closer to the source. By minimizing latency, healthcare professionals can make timely decisions, improving patient outcomes and enabling better management of chronic conditions. This trend is expected to intensify, with the growing integration of Internet of Medical Things (IoMT) devices driving demand for localized data processing solutions.

Enhanced Data Management Solutions

Another significant opportunity for edge computing in healthcare lies in enhanced data management. The healthcare industry is experiencing exponential growth in data volume, ranging from electronic health records to imaging data. Edge computing offers a scalable solution for managing and processing this data more efficiently, reducing the burden on centralized cloud systems. As healthcare organizations increasingly prioritize data security and privacy, the decentralized nature of edge computing becomes more attractive, offering lower latency and improved security features. This will be a crucial growth driver.

Latest Trends

Expansion of 5G Technology

The deployment of 5G technology is expected to significantly accelerate the growth of edge computing in the healthcare sector. The high-speed, low-latency capabilities of 5G enable real-time data processing at the edge, reducing the need for data transmission to centralized cloud servers. This is particularly beneficial for time-sensitive healthcare applications such as remote patient monitoring and telemedicine, where swift data analysis and response are critical. With more healthcare providers adopting 5G-enabled devices, edge computing will become an integral component of healthcare infrastructure, facilitating faster diagnostics and improved patient outcomes. As 5G networks expand globally, the healthcare industry is positioned to benefit from enhanced connectivity and data processing efficiency.

Robotic Surgery Applications

Robotic surgery is emerging as a key area where edge computing will play a transformative role. The integration of edge computing with robotic surgical systems is anticipated to drive advancements in precision, safety, and efficiency. Edge computing allows robotic systems to process and analyze surgical data locally, reducing latency and enhancing real-time decision-making during procedures. This is crucial for complex surgeries requiring high accuracy, as delays in data transmission can have serious implications. Furthermore, with the growing demand for minimally invasive surgeries, the adoption of robotic surgery powered by edge computing is set to rise, leading to improved patient recovery times and reduced operational risks.

Regional Analysis

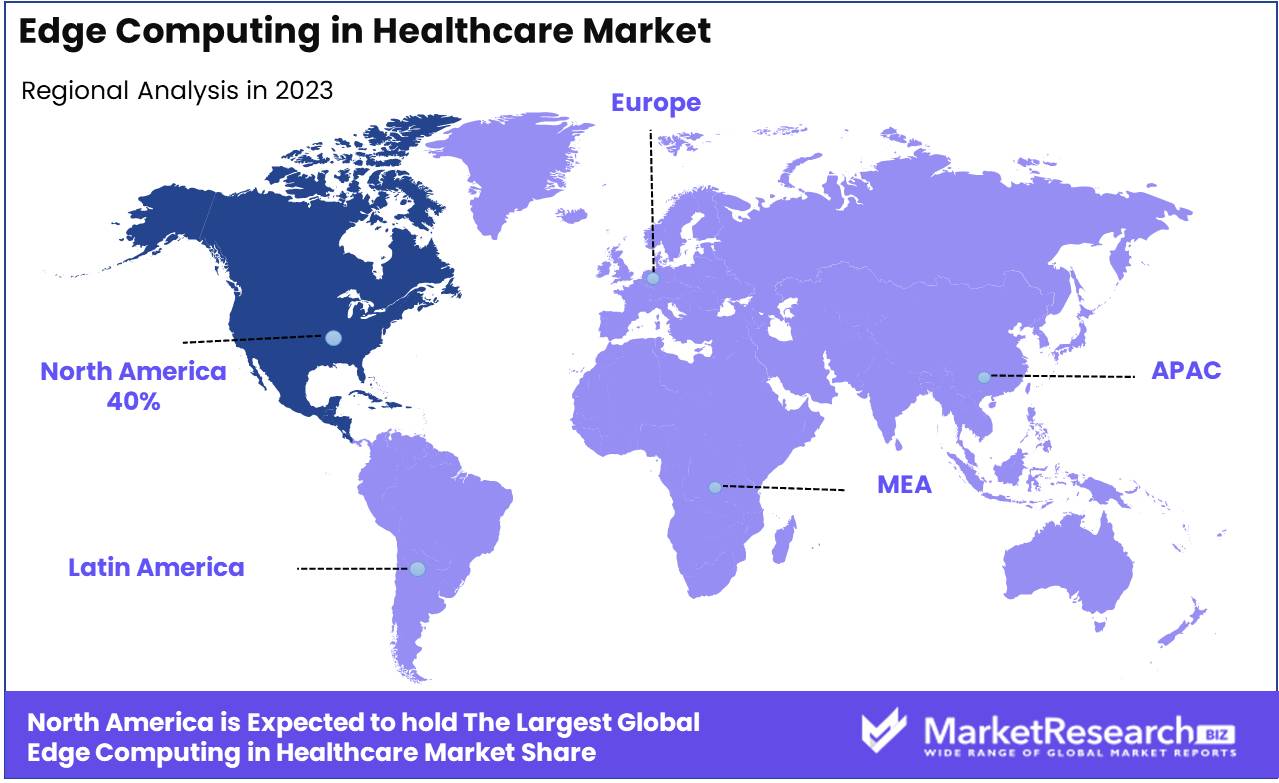

North America dominates the Edge Computing in the Healthcare market, leading with a 40% share.

The Edge Computing in Healthcare market exhibits regional variability, with North America leading the market, driven by the region's advanced healthcare infrastructure, widespread adoption of IoT-enabled devices, and strong investments in cutting-edge technologies. North America accounted for over 40% of the market share in 2023, bolstered by key players such as Cisco Systems, IBM, and Hewlett Packard Enterprise, along with regulatory support fostering innovation in healthcare. The U.S., in particular, is a dominant contributor to market growth due to its focus on reducing latency and enhancing patient data management through edge solutions.

In Europe, the market is expanding significantly due to government initiatives promoting digital health transformation and increasing investments in healthcare infrastructure. Countries such as Germany and the UK are key players, leveraging edge computing to improve healthcare services in rural areas and address the growing demand for real-time data processing.

The Asia-Pacific region is projected to witness the fastest growth, driven by rapid digitalization in countries like China, Japan, and India. The increasing demand for telemedicine, coupled with expanding 5G networks, accelerates the adoption of edge computing solutions in healthcare. APAC is expected to exhibit a CAGR exceeding 25% during the forecast period.

In the Middle East & Africa, while the adoption rate is lower, emerging economies like the UAE and South Africa are focusing on integrating edge computing to enhance healthcare accessibility.

Latin America is witnessing moderate growth, with Brazil and Mexico leading the way as governments and healthcare providers increasingly embrace digital health technologies, further promoting edge computing applications.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global edge computing in the healthcare market is expected to witness significant growth, driven by the increasing need for real-time data processing, lower latency, and enhanced decision-making capabilities at the edge of healthcare networks. Key players in this market are leveraging their expertise in cloud computing, networking, and healthcare technologies to address the growing demand for advanced healthcare solutions.

Amazon Web Services (AWS), Microsoft Corporation, and Google LLC, as leading cloud service providers, are likely to maintain a strong foothold in edge computing through their robust cloud infrastructure and AI-driven analytics platforms tailored for healthcare applications. Their edge computing solutions focus on enhancing patient care by enabling real-time processing of medical data at healthcare facilities.

IBM and Hewlett Packard Enterprise (HPE) are expected to provide specialized edge computing offerings that integrate AI and IoT capabilities for predictive analytics, supporting clinical decision-making and operational efficiencies in hospitals and clinics.

Advantech, Cisco Systems, Inc., and Aruba Networks are poised to capitalize on their networking and IoT expertise, offering secure, scalable edge computing platforms that enhance connectivity within healthcare environments.

Meanwhile, Intel Corporation, NVIDIA Corporation, and Dell Technologies, Inc. are likely to lead in hardware innovation, providing the high-performance processors and GPUs necessary for managing data-intensive workloads in edge computing systems.

Finally, healthcare-specific companies like Siemens Healthineers, Philips Healthcare, and General Electric Company are expected to play a pivotal role in delivering edge computing solutions designed specifically for imaging, diagnostics, and connected medical devices, further driving market expansion.

Market Key Players

- Advantech

- Amazon Web Services (AWS)

- Aruba Networks

- Cisco Systems, Inc

- Dell Technologies, Inc.

- General Electric Company

- Google LLC

- Hewlett Packard Enterprise Company

- IBM

- Intel Corporation

- Microsoft Corporation

- Nokia Corporation

- NVIDIA Corporation

- Philips Healthcare

- Siemens Healthineers

Recent Development

- In June 2024, IBM extended its edge computing capabilities in healthcare by collaborating with Cleveland Clinic. This partnership focuses on enhancing real-time patient monitoring through edge solutions that enable faster decision-making, particularly for high-risk patients in critical care. By processing data closer to its source, this project reduces latency and enables timely interventions.

- In July 2024, Cognizant introduced the Neuro Edge platform designed to empower industries, including healthcare, to leverage AI and generative AI at the edge. This platform allows healthcare organizations to process data locally, enhancing privacy, reducing bandwidth costs, and improving real-time operational resilience. This development enables real-time healthcare applications like telemedicine and diagnostics

- In September 2024, Teladoc Health is integrating edge AI technologies to enhance its telemedicine services. The edge computing architecture enables real-time processing of patient data from remote devices, improving the efficiency of virtual consultations and remote patient monitoring. This development helps address the growing demand for virtual healthcare, especially in underserved and rural areas

Report Scope

Report Features Description Market Value (2023) USD 4.5 Billion Forecast Revenue (2033) USD 43.8 Billion CAGR (2024-2032) 26.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Hardware, Software, Services), By Application (Telehealth & Remote Patient Monitoring, Diagnostics, Robotic Surgery, Ambulances, Others), By End User (Hospitals & Clinics, Long-term Care Centers & Home Care Settings, Ambulatory Care Centers, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Advantech, Amazon Web Services (AWS), Aruba Networks, Cisco Systems, Inc, Dell Technologies, Inc., General Electric Company, Google LLC, Hewlett Packard Enterprise Company, IBM, Intel Corporation, Microsoft Corporation, Nokia Corporation, NVIDIA Corporation, Philips Healthcare, Siemens Healthineers Customization Scope Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Advantech

- Amazon Web Services (AWS)

- Aruba Networks

- Cisco Systems, Inc

- Dell Technologies, Inc.

- General Electric Company

- Google LLC

- Hewlett Packard Enterprise Company

- IBM

- Intel Corporation

- Microsoft Corporation

- Nokia Corporation

- NVIDIA Corporation

- Philips Healthcare

- Siemens Healthineers

Our Clients

View Our Licence Options