Doxorubicin Hydrochloride Market By Type (10mg/Bottle, 50mg/Bottle), By Application (Hospital Pharmacy, Retail Pharmacy, Others), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

50847

-

August 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

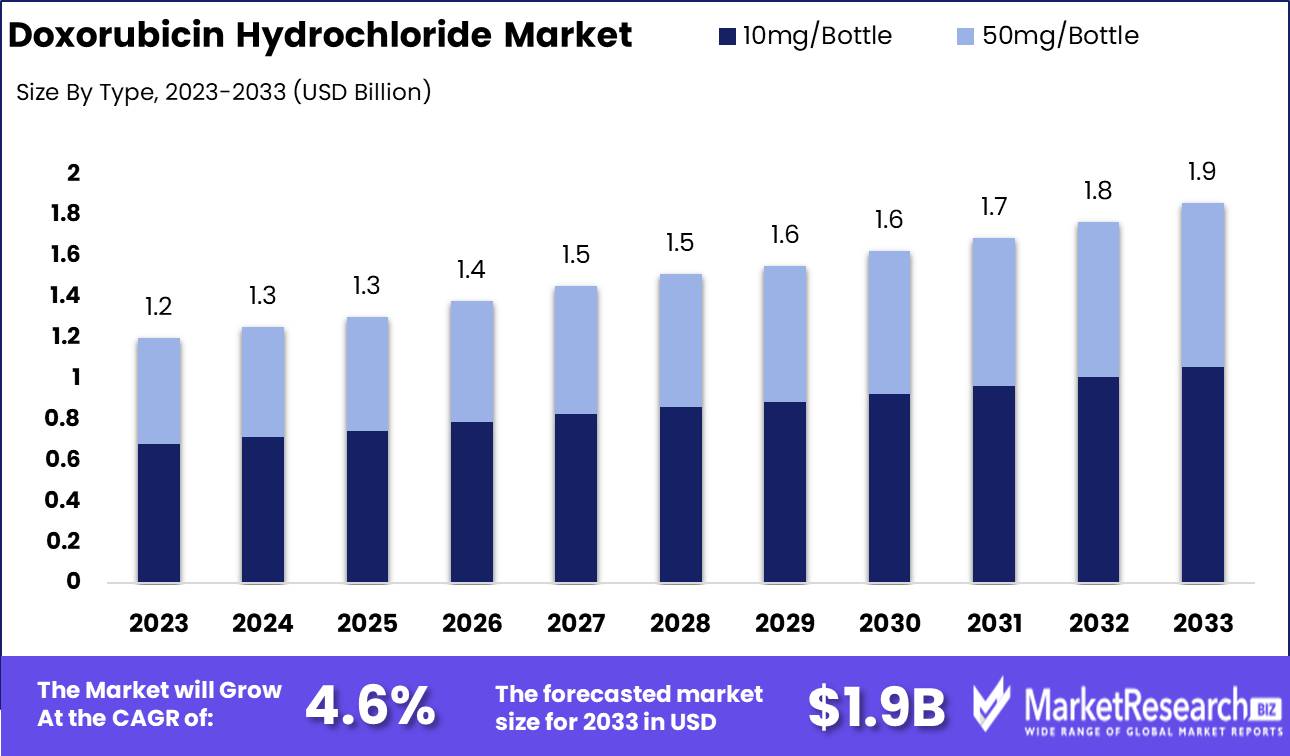

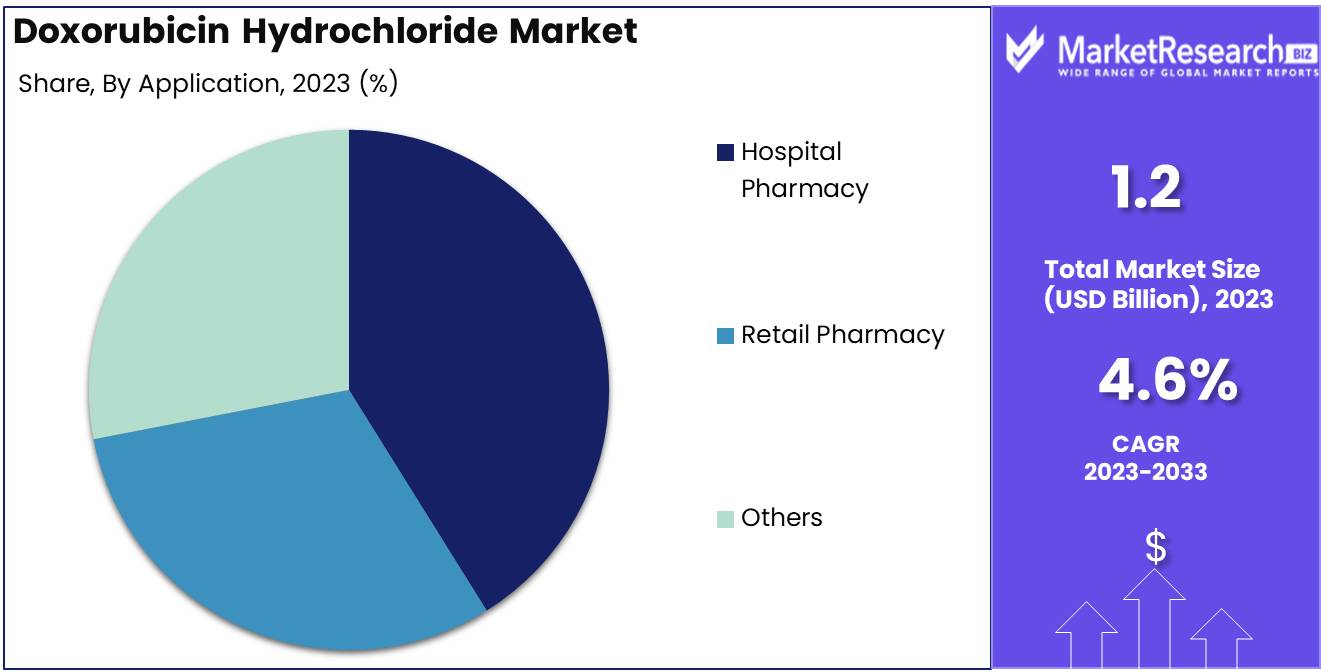

The Doxorubicin Hydrochloride Market was valued at USD 1.2 billion in 2023. It is expected to reach USD 1.9 billion by 2033, with a CAGR of 4.6% during the forecast period from 2024 to 2033.

The Doxorubicin Hydrochloride Market encompasses the global landscape of this chemotherapeutic agent, widely used in oncology to treat various cancers, including breast cancer, lymphoma, and leukemia. Market growth is driven by the increasing incidence of cancer, advancements in drug delivery systems, and the rising adoption of combination therapies. Regulatory approvals and patent expirations influence market dynamics, impacting branded and generic segments.

The Doxorubicin Hydrochloride market is poised for significant growth, driven primarily by the escalating incidence of cancer globally. As cancer remains one of the leading causes of mortality, the demand for effective chemotherapeutic agents, such as Doxorubicin Hydrochloride, is expected to rise. The compound's efficacy in treating various types of cancer, including breast cancer, lymphoma, and leukemia, has solidified its position as a cornerstone in oncology treatment protocols.

However, the market's expansion is not without challenges. The adverse side effects associated with Doxorubicin, particularly cardiotoxicity, present a substantial barrier to its widespread adoption. These side effects have prompted ongoing research and development efforts to mitigate the drug's toxicity, which could further fuel market growth by enhancing patient outcomes and broadening its therapeutic application.

Despite these challenges, the overall outlook for the Doxorubicin Hydrochloride market remains positive. Advances in drug delivery systems, such as liposomal formulations, have been instrumental in reducing the drug's toxicity, thereby increasing its clinical utility. Additionally, the increasing emphasis on combination therapies, where Doxorubicin is used alongside other agents to improve efficacy and reduce adverse effects, is likely to drive demand further. As healthcare systems worldwide continue to grapple with the rising cancer burden, the Doxorubicin Hydrochloride market is expected to witness robust growth, underscored by the compound's critical role in cancer treatment regimens and the ongoing innovations aimed at optimizing its therapeutic profile.

Key Takeaways

- Market Growth: The Doxorubicin Hydrochloride Market was valued at USD 1.2 billion in 2023. It is expected to reach USD 1.9 billion by 2033, with a CAGR of 4.6% during the forecast period from 2024 to 2033.

- By Type: The 10mg/Bottle segment dominated the Doxorubicin Hydrochloride Market.

- By Application: Hospital Pharmacy dominated the Doxorubicin Hydrochloride market by application.

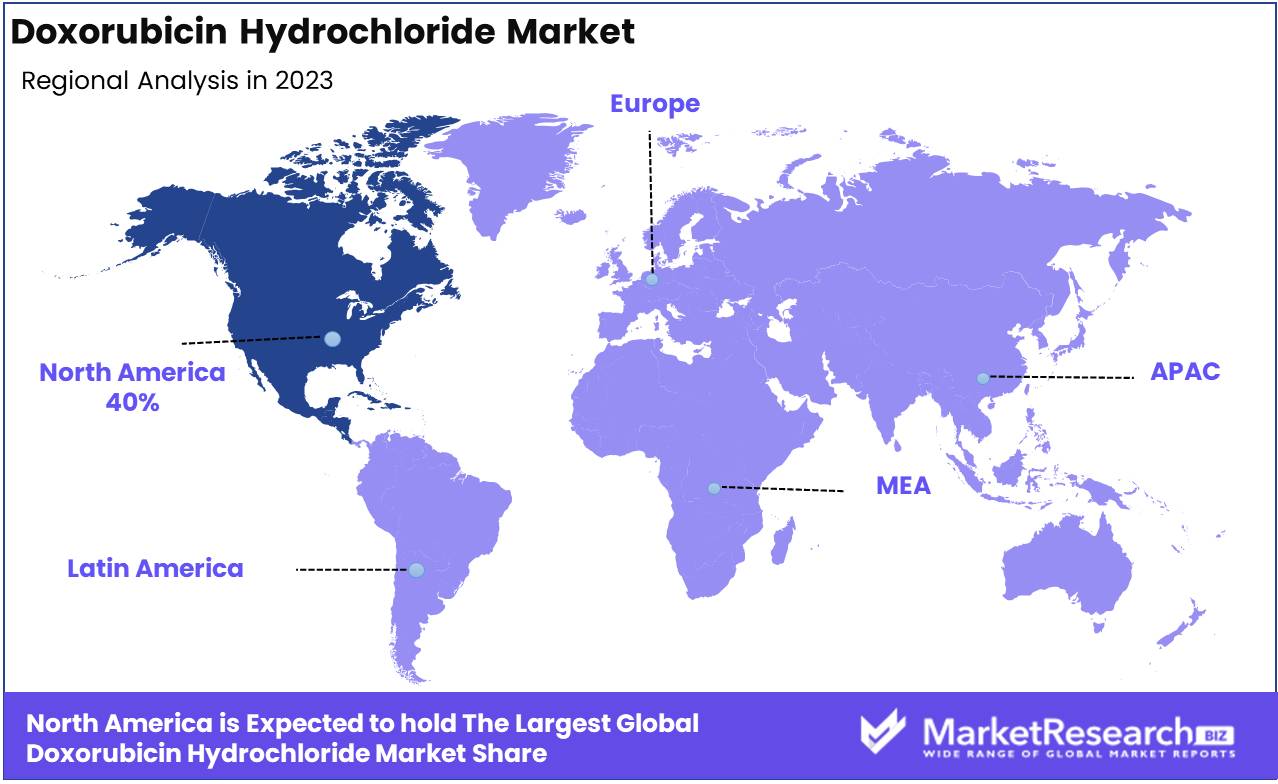

- Regional Dominance: North America dominates the Doxorubicin Hydrochloride market with a 40% largest share.

- Growth Opportunity: The global Doxorubicin Hydrochloride market is poised for robust growth driven by advancements in drug delivery systems and the rise of personalized medicine in oncology.

Driving factors

Rising Prevalence of Cancer Worldwide: A Fundamental Driver of Market Expansion

The global increase in cancer cases represents a significant catalyst for the growth of the Doxorubicin Hydrochloride market. According to the World Health Organization, cancer is the second leading cause of death globally, accounting for nearly 10 million deaths in 2020. This alarming rise in cancer prevalence has fueled the demand for effective chemotherapeutic agents, including Doxorubicin Hydrochloride, which is widely recognized for its efficacy in treating various types of cancers such as breast cancer, leukemia, and lymphomas. The growing incidence of cancer, particularly in developing regions where industrialization and lifestyle changes have led to higher cancer rates, directly translates to increased demand for this chemotherapy drug, thus driving market growth.

Increasing Number of Regulatory Approvals: Accelerating Market Access and Adoption

The Doxorubicin Hydrochloride market is experiencing growth due to a surge in regulatory approvals, which facilitates the drug's accessibility and broadens its application. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have granted numerous approvals for new formulations and indications of Doxorubicin Hydrochloride. These approvals not only enhance the drug's market presence but also build trust among healthcare providers and patients, encouraging its adoption.

For instance, liposomal formulations of Doxorubicin have received regulatory endorsements for use in specific patient populations, which has expanded the drug’s utilization and contributed to market growth. The streamlined approval processes and increased regulatory support globally are pivotal in accelerating market penetration, particularly in regions with previously limited access to advanced oncology treatments.

Rising Demand for Targeted Therapies: Shifting Towards Personalized Cancer Treatment

The rising demand for targeted therapies is another critical factor propelling the growth of the Doxorubicin Hydrochloride market. Targeted therapies, which focus on specific molecular targets associated with cancer, are becoming increasingly popular due to their efficacy and reduced side effects compared to traditional chemotherapy. Doxorubicin Hydrochloride, particularly in its liposomal form, has been integrated into combination therapies that target specific cancer cells while sparing healthy tissues, aligning with the trend toward personalized medicine. This approach not only improves patient outcomes but also reduces the overall toxicity of cancer treatments.

The growing preference for such targeted therapies, which are often used in conjunction with Doxorubicin Hydrochloride, is driving demand for the drug as part of comprehensive cancer treatment protocols. The market is expected to grow as these therapies become more widespread, supported by advancements in oncology research and the increasing availability of personalized treatment options.

Restraining Factors

Drug Resistance: A Major Constraint on Doxorubicin Hydrochloride Market Expansion

Drug resistance remains one of the most significant challenges to the growth of the Doxorubicin Hydrochloride market. Doxorubicin, while effective in treating various cancers, often encounters the problem of cancer cells developing resistance to the drug over time. This phenomenon, known as multidrug resistance (MDR), significantly reduces the therapeutic efficacy of Doxorubicin, necessitating higher doses or combination therapies, which can lead to increased toxicity and adverse side effects for patients.

The development of drug resistance is driven by various mechanisms, including the overexpression of efflux pumps like P-glycoprotein, which actively expel the drug from cancer cells, reducing its intracellular concentration and effectiveness. The high incidence of drug resistance limits the broader application of Doxorubicin Hydrochloride, thereby restraining market growth. The need for ongoing research to overcome or circumvent drug resistance adds to the cost burden on manufacturers, impacting profitability and market expansion.

Limited Bioavailability: A Critical Barrier to Doxorubicin Hydrochloride Market Growth

Limited bioavailability further hampers the growth potential of the Doxorubicin Hydrochloride market. Bioavailability refers to the proportion of a drug that enters the circulation when introduced into the body and is thus able to have an active effect. Doxorubicin Hydrochloride, when administered intravenously, faces challenges related to its distribution and absorption within the body, leading to suboptimal therapeutic outcomes.

The poor bioavailability of Doxorubicin is primarily attributed to its rapid metabolism and clearance from the bloodstream, which necessitates frequent dosing to maintain effective therapeutic levels. This not only increases the treatment cost but also enhances the risk of side effects, including cardiotoxicity, which is a well-documented adverse effect of Doxorubicin therapy. Consequently, the limited bioavailability restricts its widespread use, particularly in patient populations that require long-term treatment, thereby impeding market growth.

By Type Analysis

In 2023, The 10mg/Bottle segment dominated the Doxorubicin Hydrochloride Market.

In 2023, The 10mg/Bottle segment held a dominant market position in the Doxorubicin Hydrochloride Market by type, driven by its widespread adoption in the treatment of various cancers, including breast cancer, lymphomas, and solid tumors. This segment's dominance can be attributed to its high demand in oncology treatments, where precise and lower dosages are preferred to minimize adverse effects while maintaining therapeutic efficacy. Additionally, the 10mg/Bottle formulation offers greater flexibility for dose adjustments, catering to the needs of personalized medicine, which is increasingly becoming a standard in oncology care. The ability to tailor doses based on patient-specific factors has reinforced the market preference for this segment, contributing to its substantial market share.

Conversely, the 50mg/Bottle segment, while significant, serves more specialized applications where higher dosages are required, particularly in aggressive cancer treatments. However, its usage is comparatively limited due to the higher risk of toxicity and side effects. Consequently, the 10mg/Bottle segment remains the preferred choice among healthcare providers, thereby solidifying its leading position in the Doxorubicin Hydrochloride Market.

By Application Analysis

In 2023, Hospital Pharmacy dominated the Doxorubicin Hydrochloride market by application.

In 2023, The Hospital Pharmacy segment held a dominant market position in the By Application segment of the Doxorubicin Hydrochloride Market. This leadership can be attributed to the growing prevalence of cancer worldwide, which necessitates specialized and continuous treatment regimens often managed through hospital settings. Hospital pharmacies are integral in administering complex chemotherapy treatments, including doxorubicin hydrochloride, due to their ability to handle high-risk medications and ensure patient safety. The segment’s dominance is further reinforced by the availability of advanced healthcare infrastructure, which supports the distribution and monitoring of such potent oncology drugs. Additionally, hospital pharmacies benefit from established relationships with drug manufacturers and suppliers, ensuring a steady supply chain. This has led to increased adoption of doxorubicin hydrochloride in inpatient settings, where tailored and supervised treatment protocols are critical.

The Retail Pharmacy segment also plays a significant role in the market, particularly in outpatient care and the distribution of follow-up medications. However, its market share is constrained by the complexity of doxorubicin hydrochloride administration, which often requires professional healthcare oversight, limiting its use in retail settings. Retail pharmacies cater primarily to maintenance therapies and supportive care drugs, providing accessibility and convenience to patients.

The Others segment, comprising specialized clinics and homecare settings, represents a smaller yet growing portion of the market. This segment is gaining traction as healthcare trends shift towards more personalized and home-based care options. Innovations in drug delivery systems and an increasing focus on outpatient care are expected to drive growth in this segment, although it remains secondary to hospital pharmacies due to the highly specialized nature of doxorubicin hydrochloride treatment. The segment's potential is significant as healthcare systems continue to evolve towards more patient-centric approaches.

Key Market Segments

By Type

- 10mg/Bottle

- 50mg/Bottle

By Application

- Hospital Pharmacy

- Retail Pharmacy

- Others

Growth Opportunity

Advancements in Drug Delivery Systems

The global Doxorubicin Hydrochloride market is poised to experience significant growth, largely driven by advancements in drug delivery systems. Traditional chemotherapy methods, while effective, often result in systemic toxicity, affecting patients quality of life. However, innovations in drug delivery technologies, such as nanoparticle-based delivery systems, liposomal formulations, and targeted drug delivery mechanisms, are mitigating these challenges. These technologies enhance the precision of Doxorubicin Hydrochloride administration, ensuring higher concentrations of the drug reach the tumor site with reduced off-target effects. As these technologies continue to mature, the demand for Doxorubicin Hydrochloride is expected to rise, offering lucrative opportunities for market players.

Growth in Personalized Medicine

The shift towards personalized medicine represents another critical opportunity for the Doxorubicin Hydrochloride market. Personalized medicine tailors treatment plans based on an individual's genetic makeup, ensuring that patients receive the most effective therapies with minimized side effects. Doxorubicin Hydrochloride is increasingly being integrated into personalized oncology treatment regimens, particularly for cancers such as breast cancer and lymphoma. With the growing adoption of genetic profiling and biomarker-based therapies, the utilization of Doxorubicin Hydrochloride is anticipated to increase. This trend will likely expand the market, driven by the pharmaceutical industry's focus on developing targeted therapies that align with the principles of personalized medicine.

Latest Trends

Focus on Combination Therapies

The outlook for the Doxorubicin Hydrochloride market is significantly influenced by the growing focus on combination therapies. As the oncology landscape evolves, there is a discernible shift towards utilizing Doxorubicin Hydrochloride in tandem with other therapeutic agents to enhance efficacy and reduce adverse effects. This trend is particularly pronounced in the treatment of complex cancers, where monotherapies have shown limited success. The combination of Doxorubicin Hydrochloride with novel immunotherapies and targeted therapies is anticipated to improve patient outcomes and extend survival rates. This strategic shift is expected to bolster the market demand, as combination therapies become the preferred approach in clinical settings.

Investment in R&D

Investment in research and development (R&D) is another critical trend shaping the Doxorubicin Hydrochloride market. With the continuous push for more effective cancer treatments, pharmaceutical companies are increasingly channeling resources into the development of next-generation formulations of Doxorubicin Hydrochloride. This includes advancements in liposomal formulations and the exploration of new delivery mechanisms that aim to minimize cardiotoxicity a significant side effect associated with Doxorubicin.

Moreover, R&D investments are likely to lead to the discovery of new indications for Doxorubicin Hydrochloride, thereby expanding its application scope. This sustained focus on innovation is expected to drive market growth and reinforce the drug's position as a cornerstone in oncology therapy.

Regional Analysis

North America dominates the Doxorubicin Hydrochloride market with a 40% largest share.

The Doxorubicin Hydrochloride market exhibits diverse regional dynamics, with North America emerging as the dominant region, accounting for approximately 40% of the global market share. This dominance is attributed to the well-established healthcare infrastructure, high prevalence of cancer, and substantial investment in research and development. The United States, within North America, is the primary contributor, driven by advanced pharmaceutical manufacturing capabilities and a strong presence of key industry players.

In Europe, the market holds a significant share, driven by increasing cancer cases and favorable government initiatives aimed at improving cancer treatment. Germany, France, and the United Kingdom are the leading markets within the region, supported by robust healthcare systems and ongoing advancements in oncology.

The Asia Pacific region is witnessing the fastest growth, with a CAGR of approximately 7.5% during the forecast period. This growth is fueled by the rising incidence of cancer, increasing healthcare expenditure, and improving access to advanced treatments in countries like China, India, and Japan.

The Middle East & Africa and Latin America regions represent emerging markets with considerable growth potential. In these regions, market expansion is driven by improving healthcare infrastructure, increasing awareness of cancer treatments, and growing government support. However, these regions account for a smaller share of the global market due to limited access to advanced therapies and lower healthcare spending compared to more developed regions.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global Doxorubicin Hydrochloride market is characterized by the competitive presence of both established pharmaceutical giants and emerging players, each contributing to the market's robust growth trajectory.

Shanxi PUDE Pharmaceutical and Shenzhen Main Luck Pharmaceuticals are notable Chinese manufacturers, leveraging their domestic market strength and expanding their footprint globally. Their strategic focus on cost-effective production and innovation in drug formulations positions them as formidable competitors in the Asian market. HAN HUI Pharmaceuticals and Shantou Special Economic Zone Mingzhi Medicine further solidify China’s influence, emphasizing high-quality production standards and an increasing focus on international regulatory compliance, which enables them to penetrate markets in Europe and North America.

Zhejiang Hisun Pharmaceutical stands out with its extensive experience in oncology therapeutics and a strong R&D pipeline. Hisun’s global partnerships and emphasis on biosimilars provide it with a competitive edge, especially in price-sensitive markets. Mylan, a global pharmaceutical leader, continues to maintain a strong position due to its extensive distribution network and comprehensive portfolio of oncology drugs, including Doxorubicin Hydrochloride. Mylan's recent merger with Upjohn has further enhanced its market reach and operational efficiency.

Rm Healthcare, Advacare Pharma, and Cipla are recognized for their generic drug offerings, providing cost-effective alternatives that are crucial in developing markets. Their emphasis on accessibility and affordability is expected to sustain their market presence. Actavis and Getwell are key players in the generic market, known for their strategic acquisitions and investments in expanding their oncology portfolios, thereby ensuring their relevance in an increasingly competitive landscape.

In summary, the global Doxorubicin Hydrochloride market is shaped by strategic expansions, competitive pricing, and innovations, with both established and emerging companies vying for market leadership through diversified product portfolios and global distribution strategies.

Market Key Players

- Shanxi PUDE Pharmaceutical

- Shenzhen Main Luck Pharmaceuticals

- HAN HUI Pharmaceuticals

- Shantou Special Economic Zone Mingzhi Medicine

- Zhejiang Hisun Pharmaceutical

- Mylan

- Rm Healthcare

- Advacare Pharma

- Cipla

- Actavis

- Getwell

Recent Development

In July 2024, Pfizer announced the expansion of its manufacturing capacity for Doxorubicin Hydrochloride at its facility in Kalamazoo, Michigan. This expansion is part of Pfizer’s broader strategy to ensure a stable supply of oncology drugs, including Doxorubicin Hydrochloride, which is critical in chemotherapy treatments. The increased production capacity is expected to meet rising global demand, particularly in emerging markets.

In June 2024, Zydus Cadila received FDA approval in June 2024 for its new formulation of Doxorubicin Hydrochloride in an injectable form. This approval allows Zydus Cadila to market its product in the U.S., expanding its footprint in the oncology segment. The injectable form is designed to improve patient compliance and reduce side effects compared to traditional formulations.

In April 2024, Sun Pharmaceutical Industries Ltd. launched a generic version of Doxorubicin Hydrochloride Liposomal Injection in the U.S. market. This launch followed the approval from the U.S. FDA, and it is expected to increase accessibility to cost-effective chemotherapy options. This development positions Sun Pharma as a significant player in the generic oncology drug market.Report Scope

Report Features Description Market Value (2023) USD 1.2 Billion Forecast Revenue (2033) USD 1.9 Billion CAGR (2024-2032) 4.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (10mg/Bottle, 50mg/Bottle), By Application (Hospital Pharmacy, Retail Pharmacy, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Shanxi PUDE Pharmaceutical, Shenzhen Main Luck Pharmaceuticals, HAN HUI Pharmaceuticals, Shantou Special Economic Zone Mingzhi Medicine, Zhejiang Hisun Pharmaceutical, Mylan, Rm Healthcare, Advacare Pharma, Cipla, Actavis, Getwell Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Shanxi PUDE Pharmaceutical

- Shenzhen Main Luck Pharmaceuticals

- HAN HUI Pharmaceuticals

- Shantou Special Economic Zone Mingzhi Medicine

- Zhejiang Hisun Pharmaceutical

- Mylan

- Rm Healthcare

- Advacare Pharma

- Cipla

- Actavis

- Getwell

Our Clients

View Our Licence Options