Global Doppler Ultrasound Systems Market By Device Type(Trolley-Based, Handheld), By Application(Radiology, Cardiology, Obstetrics and Gynecology, Others), By End-use(Hospitals, Diagnostic Imaging Centers, Home Care, Academic & Research Institutes), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48792

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

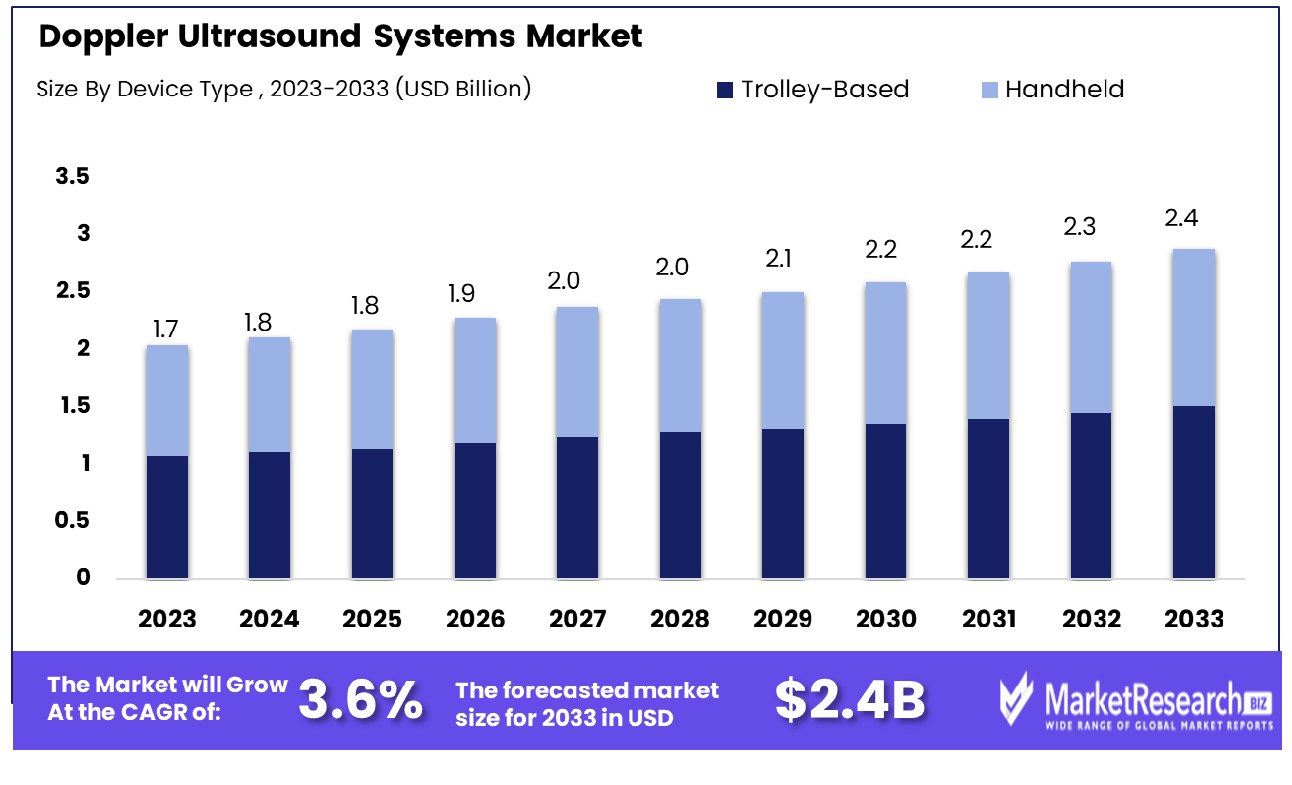

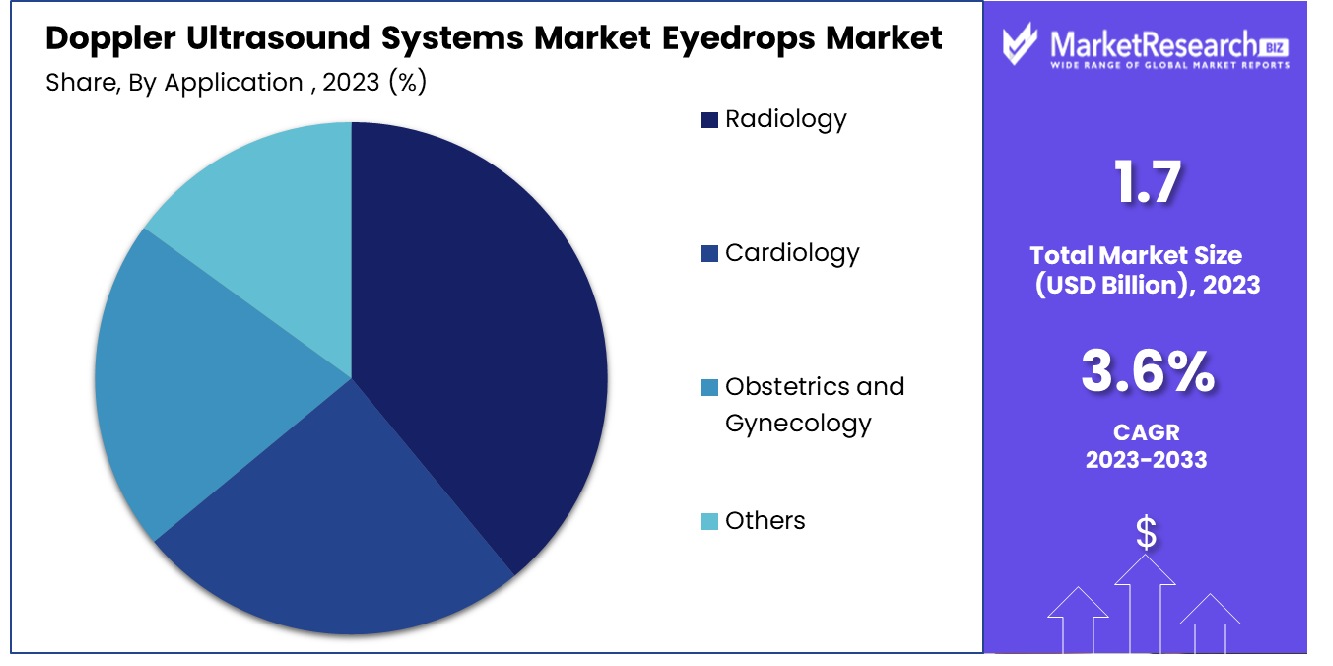

The Global Doppler Ultrasound Systems Market was valued at USD 1.7 billion in 2023. It is expected to reach USD 2.4 billion by 2033, with a CAGR of 3.6% during the forecast period from 2024 to 2033.

The Doppler Ultrasound Systems Market comprises advanced medical imaging technology that measures and visualizes blood flow through veins, arteries, and cardiac chambers using the Doppler effect. These systems are pivotal in diagnosing conditions such as blood clots, poor circulation, blocked arteries, and heart valve defects.

Utilizing sound waves to capture moving blood cells, Doppler ultrasound systems offer non-invasive, real-time insights into cardiovascular health, aiding healthcare professionals in making precise assessments. This market is integral to the evolution of diagnostic modalities, promising enhanced patient outcomes through technological innovation. Leaders in the healthcare and medical technology sectors prioritize understanding and leveraging these systems for optimal clinical effectiveness.

The Doppler Ultrasound Systems Market is positioned for significant growth, driven by advancements in medical imaging technology and an increasing prevalence of cardiovascular diseases globally. Doppler ultrasound systems, renowned for their capacity to provide detailed images of blood flow and tissues, are crucial in diagnosing and managing various vascular conditions and cardiac anomalies. This technology's ability to deliver real-time data with high precision makes it indispensable in clinical settings.

A 2023 study underscores the efficacy of Doppler ultrasound in diagnosing supraspinatus tendinopathy, a common shoulder disorder. The study highlighted that specific gray-level values obtained from supraspinatus tendon ultrasound images yielded Area Under the Receiver Operating Characteristic (AUROC) values between 0.951 and 0.960. These impressive metrics indicate a high diagnostic accuracy, with optimal thresholds delivering sensitivities ranging from 93.3% to 96.7% and specificities from 85.3% to 88.2%.

Furthermore, a multimodal approach that integrates Doppler ultrasound with other diagnostic techniques demonstrated an AUROC of 0.939, achieving a sensitivity of 97.8%, specificity of 85.6%, and accuracy of 90.5%. Such findings confirm the system's superior diagnostic capabilities, which are critical for effective treatment planning and improved patient outcomes.

Key Takeaways

- Market Growth: The Global Doppler Ultrasound Systems Market was valued at USD 1.7 billion in 2023. It is expected to reach USD 2.4 billion by 2033, with a CAGR of 3.6% during the forecast period from 2024 to 2033.

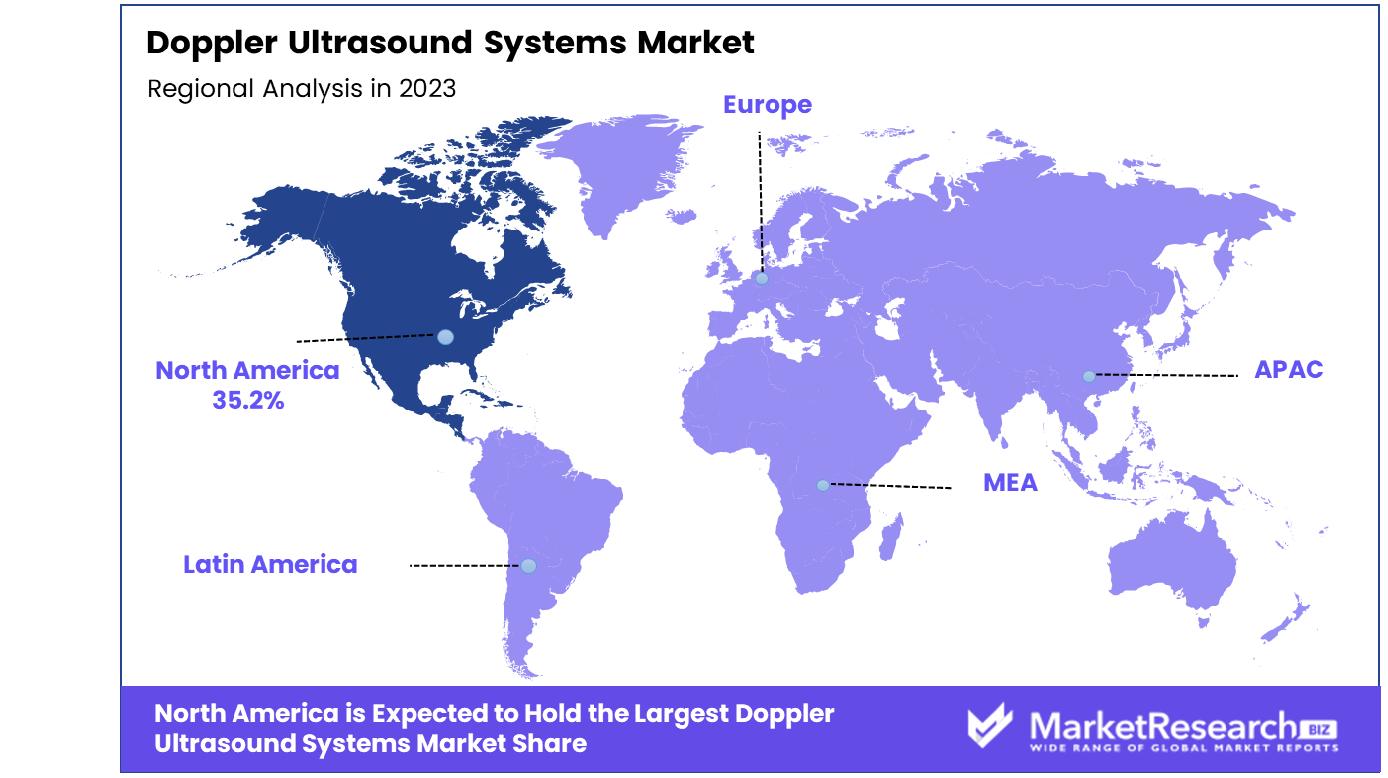

- Regional Dominance: North America leads with 35.2% of the Doppler Ultrasound Systems Market.

- By device type: Trolley-based systems dominate the market with a 65% share.

- By Application: Radiology applications dominate the market, accounting for 40% of total usage.

- By End-use: Hospitals are the primary end-use, representing 50% of market demand.

Driving factors

Rising Prevalence of Cardiovascular Diseases and Chronic Conditions

The increasing incidence of cardiovascular diseases and chronic health conditions globally serves as a primary catalyst for the expansion of the Doppler Ultrasound Systems Market. With heart disease consistently ranking as a leading cause of mortality worldwide, the demand for effective, non-invasive diagnostic tools like Doppler ultrasound systems is escalating.

These systems are instrumental in the early detection and management of conditions by providing detailed images of the heart and blood vessels, facilitating timely medical intervention. The growing global burden of these health issues directly correlates with heightened demand for advanced diagnostic solutions, thus propelling market growth.

Advancements in Imaging Technology Enhancing Resolution and Accuracy

Technological advancements in imaging systems have significantly enhanced the resolution and accuracy of Doppler ultrasound devices. Modern systems are equipped with high-definition imaging capabilities and sophisticated software that allow for better visualization of blood flow and tissue structures, thereby improving diagnostic accuracy.

For instance, enhancements in transducer sensitivity and image processing algorithms have allowed for clearer, more detailed images, which are crucial for diagnosing a range of cardiovascular and vascular conditions effectively. These technological improvements not only enhance clinical outcomes but also boost the adoption of these systems across various healthcare settings.

Growing Demand for Non-Invasive Diagnostic Procedures

The shift towards non-invasive diagnostic methods has been a notable trend in the medical field, reflecting a broader preference for procedures that minimize patient discomfort and risk of complications. Doppler ultrasound systems, which use sound waves to assess the blood flow in arteries and veins non-invasively, meet this demand perfectly.

This shift is driven by the need for safer diagnostic options that do not require incisions or exposure to ionizing radiation, making Doppler ultrasound a preferred choice for both patients and healthcare providers. The ease and safety of these procedures, combined with their cost-effectiveness and efficiency in delivering real-time results, substantially contribute to the market's growth.

Restraining Factors

High Cost of Advanced Doppler Ultrasound Systems

The significant financial investment required for advanced Doppler ultrasound systems is a major restraining factor impacting their market growth. These systems incorporate cutting-edge technology and software that enhance diagnostic capabilities but also come at a steep price.

The high cost not only limits the ability of smaller and resource-constrained medical facilities to acquire such equipment but also affects the market penetration in developing regions where budget constraints are more pronounced. Consequently, the affordability factor can deter widespread adoption, restricting the market's expansion primarily to well-funded healthcare institutions in developed countries.

Limited Reimbursement Policies Affecting Adoption in Certain Regions

Reimbursement policies play a critical role in the adoption of new medical technologies. In regions where these policies do not fully cover the costs of Doppler ultrasound procedures, there is a noticeable reluctance among healthcare providers to invest in such expensive diagnostic tools.

This is especially true in healthcare systems that are largely insurance-driven, where inadequate reimbursement can lead to lower usage rates of advanced diagnostic tools like Doppler ultrasound systems. The variability in insurance coverage across different countries and even within regions can therefore significantly influence the market dynamics, stymieing growth in areas where policy support is lacking.

By Device Type Analysis

By Device Type, trolley-based ultrasound systems captured 65% of the market share, leading the segment dominantly.

In 2023, Trolley-Based held a dominant market position in the By Device Type segment of the Doppler Ultrasound Systems Market, capturing more than a 65% share. On the other hand, Handheld devices accounted for a smaller portion of the market. This considerable disparity in market share is reflective of several underlying trends and factors influencing user preferences and technology adoption.

Trolley-based Doppler Ultrasound Systems are preferred primarily due to their advanced capabilities and robust feature sets, which include higher power settings, superior image quality, and greater functionality compared to their handheld counterparts. These systems are extensively utilized in hospital settings where the need for comprehensive diagnostic procedures and continuous usage is paramount. The stability, extended battery life, and integration with other diagnostic tools make trolley-based systems indispensable in these environments.

Handheld Doppler Ultrasound Systems, while offering portability and convenience, generally find favor in settings requiring bedside examination and in smaller clinics where space constraints and budget considerations play significant roles. Despite these advantages, the handheld segment has not penetrated the market as deeply, primarily due to limitations in battery life, screen size, and the overall scope of diagnostic capabilities.

By Application Analysis

Radiology applications accounted for 40% of the market share, establishing their primary role within the sector.

In 2023, Radiology held a dominant market position in the By Application segment of the Doppler Ultrasound Systems Market, capturing more than a 40% share. Other notable segments included Cardiology, Obstetrics and Gynecology, and Others, each contributing to the market dynamics in varied capacities.

The preeminence of Radiology in this market can be attributed to the extensive application of Doppler ultrasound systems in diagnosing and monitoring a broad spectrum of conditions. These include vascular disorders, which are highly prevalent across global populations. Radiology departments rely on Doppler ultrasound for its non-invasive nature and its ability to provide real-time imaging of blood flow and tissue movement, making it indispensable in settings ranging from emergency care to routine check-ups.

Cardiology, the second-largest segment, utilizes Doppler ultrasound to assess heart conditions, particularly valvular insufficiencies and blood flow issues in and around the heart. This segment benefits from advancements in ultrasound technology that improve the accuracy and diagnostic capabilities of cardiac assessments.

The Obstetrics and Gynecology segment also significantly utilizes Doppler ultrasound for monitoring fetal health and blood circulation within the uterus and placenta. This application is critical for the early detection of potential health issues in both mother and child, underpinning the importance of Doppler ultrasound in prenatal care programs.

By End-use Analysis

Hospitals represented 50% of the market share in end-use categories, highlighting their significant utilization and demand.

In 2023, Hospitals held a dominant market position in the By End-use segment of the Doppler Ultrasound Systems Market, capturing more than a 50% share. The remaining market share was distributed among Diagnostic Imaging Centers, Home Care, and Academic & Research Institutes, each playing a crucial role in the broader ecosystem.

Hospitals are pivotal in the widespread adoption of Doppler ultrasound systems due to their critical role in diagnostic and monitoring services across numerous departments, from cardiology to obstetrics. The high throughput of patients and the complex cases typically handled in hospital settings necessitate robust, high-performance imaging equipment, thereby driving the preference for advanced Doppler ultrasound systems. These facilities often invest in state-of-the-art equipment to ensure high diagnostic accuracy and improved patient care, which supports their dominant position in the market.

Diagnostic Imaging Centers follow hospitals in terms of market share, serving as vital points for outpatient care where Doppler ultrasound systems are utilized for a wide array of diagnostic purposes. These centers are preferred by patients seeking quick and specialized imaging services outside of the traditional hospital setting.

Home Care has emerged as a growing segment, particularly for chronic disease management and elderly care, where portable Doppler devices are favored for their convenience and capability to provide real-time data about patients' conditions remotely.

Key Market Segments

By Device Type

- Trolley-Based

- Handheld

By Application

- Radiology

- Cardiology

- Obstetrics and Gynecology

- Others

By End-use

- Hospitals

- Diagnostic Imaging Centers

- Home Care

- Academic & Research Institutes

Growth Opportunity

Expansion into Emerging Markets with Growing Healthcare Infrastructure

The global Doppler Ultrasound Systems Market stands to benefit significantly from expansion into emerging markets that are currently experiencing rapid growth in healthcare infrastructure. As countries like India, Brazil, and parts of Africa invest heavily in modernizing their healthcare facilities, there is a burgeoning demand for advanced medical imaging technologies.

These markets present a ripe opportunity for the deployment of Doppler ultrasound systems, which are essential for diagnosing cardiovascular and vascular diseases. The increasing healthcare spending and governmental focus on enhancing medical facilities in these regions could drive substantial market growth, making them key targets for companies looking to increase their global footprint.

Integration of AI and Machine Learning for Enhanced Imaging Analysis

Another major growth opportunity in 2023 for the Doppler Ultrasound Systems Market lies in the integration of artificial intelligence (AI) and machine learning technologies. These technologies can significantly enhance the capabilities of Doppler systems by improving the accuracy and efficiency of imaging analysis.

AI algorithms can help in the automatic detection and classification of potential health issues from ultrasound scans, reducing the workload on healthcare professionals and increasing diagnostic precision. The continued advancements in AI and machine learning not only promise to elevate the operational effectiveness of Doppler ultrasound systems but also position these systems at the forefront of innovation in diagnostic imaging.

Latest Trends

Development of Portable and Handheld Doppler Ultrasound Devices

The development of portable and handheld Doppler ultrasound devices is a prominent trend reshaping the global Doppler Ultrasound Systems Market in 2023. This innovation caters to the growing need for mobility and flexibility in medical diagnostics, allowing healthcare providers to perform critical vascular and cardiac assessments directly at the patient’s bedside or in remote areas.

These compact devices not only enhance the accessibility of diagnostic services but also reduce the time and logistical constraints associated with traditional, larger ultrasound systems. The portability factor is particularly advantageous in emergency medical situations and regions with limited access to comprehensive medical facilities, thereby broadening the scope and utility of Doppler ultrasound technology across various healthcare settings.

Increasing Use of Doppler Ultrasound in Obstetrics for Fetal Monitoring

Another significant trend in the Doppler Ultrasound Systems Market is the increasing application of this technology in obstetrics, specifically for fetal monitoring. Doppler ultrasound is being extensively used to assess the health and development of the fetus by evaluating the blood flow in the umbilical cord and fetal vessels.

This application is crucial for detecting and managing potential complications during pregnancy, such as fetal anemia, intrauterine growth restriction, and other circulatory issues. The reliability and safety of Doppler ultrasound make it an indispensable tool in prenatal care, contributing to its growing adoption among obstetricians and gynecologists worldwide.

Regional Analysis

The Doppler Ultrasound Systems Market in North America dominates with a significant share of 35.2%.

North America remains the dominant region in the Doppler Ultrasound Systems Market, holding a substantial market share of 35.2%. This leadership is driven by advanced healthcare infrastructure, significant investment in R&D, and a high prevalence of cardiovascular diseases. The region's strong emphasis on non-invasive diagnostic modalities further solidifies its market position.

Europe follows closely, with a well-established healthcare system and increasing adoption of advanced medical technologies. European countries have been proactive in integrating Doppler ultrasound systems into routine clinical practice, supported by favorable healthcare policies and a focus on reducing invasive procedures.

Asia Pacific is identified as a rapidly growing segment in the market, propelled by expanding healthcare infrastructure and rising healthcare expenditures in emerging economies like China and India. The region's large population base and increasing incidence of chronic diseases are key factors driving the demand for advanced diagnostic solutions such as Doppler ultrasound systems.

Middle East & Africa and Latin America are emerging markets with significant growth potential. These regions are gradually adopting modern healthcare technologies, although growth is somewhat tempered by economic variability and less consistent healthcare investments. However, increasing awareness about the benefits of early diagnosis and the gradual improvement in healthcare facilities are expected to boost the market growth in these regions over the coming years.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Doppler Ultrasound Systems market was significantly shaped by the activities and innovations of key players including Siemens Healthineers, Philips, GE Healthcare, Canon Medical Systems, Samsung Electronics, FUJIFILM Sonosite, Esaote SpA, and Mindray Medical. Each of these companies has contributed distinctively to the technological advancements and market dynamics.

Siemens Healthineers remained a frontrunner, driven by its continuous innovation in high-quality imaging and user-friendly interfaces, which have broadened its market reach. The company's strategic focus on integrating artificial intelligence (AI) with Doppler systems has set new standards for diagnostic precision and operational efficiency.

Philips has maintained its competitive edge through a combination of robust product offerings and strong customer relationships. Its dedication to sustainability and patient-centered technology has appealed to environmentally conscious healthcare providers, enhancing its market position.

GE Healthcare has leveraged its extensive industry experience to introduce highly versatile Doppler ultrasound systems that cater to various medical fields, from cardiology to obstetrics. GE’s emphasis on training and support services has also solidified its reputation for customer care.

Canon Medical Systems and Samsung Electronics have both expanded their market presence by offering cost-effective and high-performance systems that meet the rigorous demands of both large hospitals and small clinics.

FUJIFILM Sonosite and Esaote SpA have focused on enhancing the portability and ease of use of their Doppler systems, targeting the growing home care and private clinic markets.

Mindray Medical has distinguished itself with its aggressive pricing strategy and rapid adoption of emerging technologies, making advanced diagnostics accessible to a broader audience.

Market Key Players

- Siemens Healthineers

- Philips

- GE Healthcare

- Canon Medical Systems

- Samsung Electronics

- FUJIFILM Sonosite

- Esaote SpA

- Mindray Medical

Recent Development

- In April 2024, Canon Medical Systems launched a compact Doppler ultrasound system designed for use in smaller clinics and remote areas. This launch is part of Canon’s effort to make high-quality medical imaging more accessible and affordable, expanding its market reach and supporting better patient outcomes worldwide.

- In March 2024, Siemens Healthineers, a leader in medical imaging, introduced a new line of advanced Doppler ultrasound systems. These systems are designed to provide more detailed and clearer imaging, particularly beneficial for cardiac and vascular examinations.

- In January 2024, GE Healthcare released an upgrade for its existing Doppler ultrasound systems, focusing on enhancing image clarity and patient comfort during scans. This upgrade reflects GE's dedication to continuous improvement in patient care technology, ensuring that healthcare providers have access to the latest advancements.

Report Scope

Report Features Description Market Value (2023) USD 1.7 Billion Forecast Revenue (2033) USD 2.4 Billion CAGR (2024-2032) 3.6% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Device Type(Trolley-Based, Handheld), By Application(Radiology, Cardiology, Obstetrics and Gynecology, Others), By End-use(Hospitals, Diagnostic Imaging Centers, Home Care, Academic & Research Institutes) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Siemens Healthineers, Philips, GE Healthcare, Canon Medical Systems, Samsung Electronics, FUJIFILM Sonosite, Esaote SpA, Mindray Medical Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Siemens Healthineers

- Philips

- GE Healthcare

- Canon Medical Systems

- Samsung Electronics

- FUJIFILM Sonosite

- Esaote SpA

- Mindray Medical

Our Clients

View Our Licence Options