Disaster Preparedness Systems Market By Type(Surveillance System, Others), By Solution(Disaster Recovery Solutions, Geospatial Solutions), By Services (Consulting Services, Training & Education Services), By Communication Technology (Emergency Response Radars, First Responder Tools), By End-use (BFSI, Energy and Utilities), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

42442

-

Dec 2023

-

179

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Disaster Preparedness Systems Market Size, Share, Trends Analysis

- Disaster Preparedness Systems Market Dynamics

- Disaster Preparedness Systems Market Segmentation Analysis

- Disaster Preparedness Systems Industry Segments

- Disaster Preparedness Systems Market Growth Opportunity

- Disaster Preparedness Systems Market Regional Analysis

- Disaster Preparedness Systems Industry By Region

- Disaster Preparedness Systems Market Share Analysis

- Disaster Preparedness Systems Industry Key Players

- Disaster Preparedness Systems Market Recent Development

- Report Scope

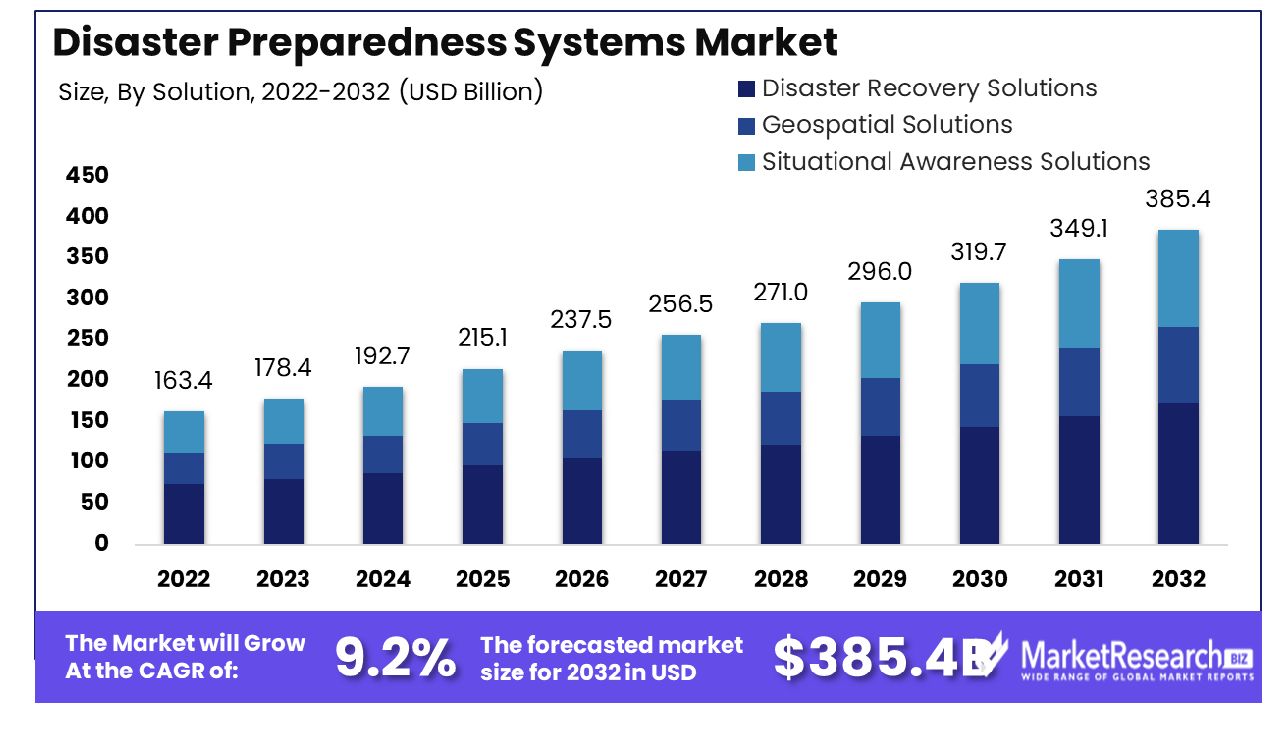

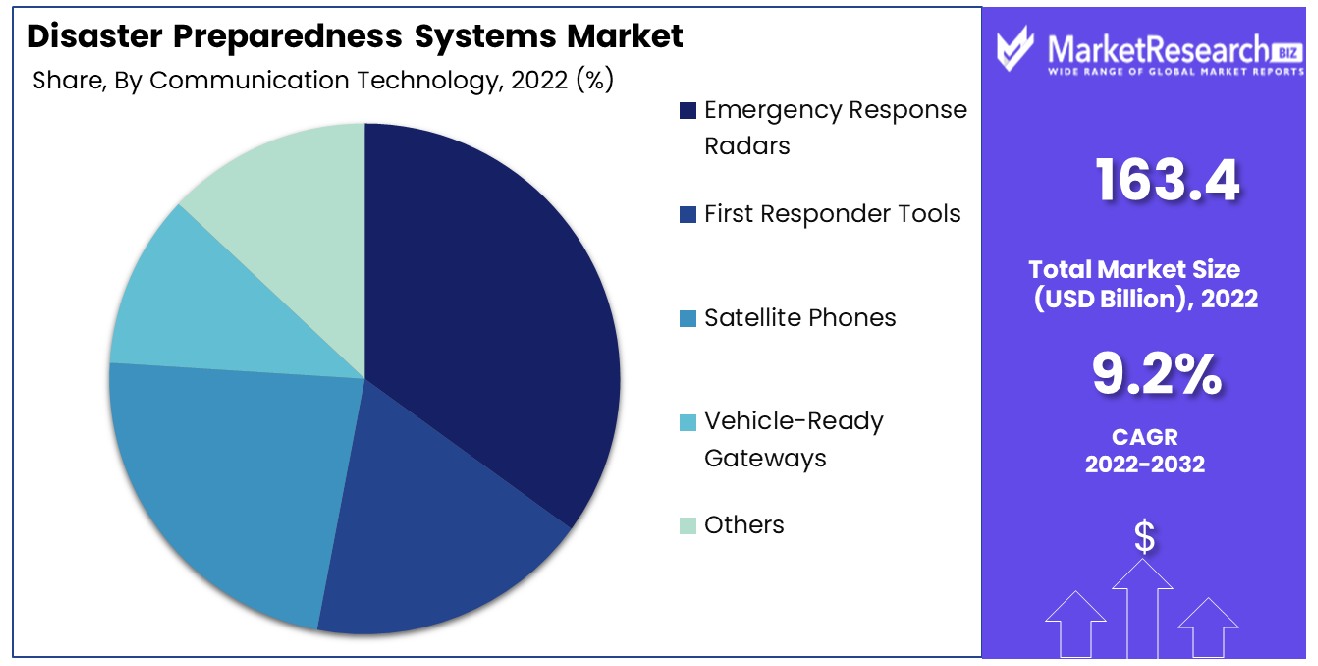

Disaster Preparedness Systems Market size is expected to be worth around USD 385.4 Bn by 2032 from USD 163.4 Bn in 2022, growing at a CAGR of 9.2% during the forecast period from 2023 to 2032.

Disaster preparedness systems are protocols and infrastructure being put in place to minimize loss of life and damage in the event of a natural or human-made catastrophic event. They are being used across vulnerable regions and communities around the world to improve resilience and response capabilities when disasters strike.

Warning systems are being installed to detect impending floods, storms, or other threats, while procedures for evacuation, provision of aid, and recovery efforts are being developed. Training programs for emergency personnel and education campaigns for the public on what to do in emergencies are also being conducted as key elements of preparation, empowering communities to act when a crisis is unfolding to reduce panic and ensure a coordinated reaction.

There are several key factors driving growth in the Disaster Preparedness Systems Market. Firstly, climate change has led to an increase in natural disasters like floods, wildfires, and storms around the world. Governments therefore face more pressure to invest in disaster preparedness systems to protect citizens and infrastructure.

In June 2023, Fujitsu Limited and Hexagon's Safety, Infrastructure & Geospatial division collaborated to develop digital twin applications aimed at predicting and mitigating natural disasters and enhancing traffic safety. These applications leverage advanced technologies to create a digital twin that replicates real-world conditions, enabling the analysis and verification of disaster threats and optimal disaster preparedness.

Secondly, technological improvements in areas like AI, sensors, and satellite imagery enable more accurate disaster prediction and early warning. This is leading the Disaster Preparedness Systems Market to develop smarter systems that leverage these technologies.

Urbanization also plays a role – with more populations concentrated in cities, the impact of events like earthquakes and disease outbreaks is multiplied. Hence disaster management is critical. Moreover, the COVID-19 pandemic highlighted cracks in preparedness globally, calling for increased investments after seeing firsthand how much economic and human loss can stem from a health crisis.

In April 2023, the WHO launched a new initiative, the Preparedness and Resilience for Emerging Threats Initiative (PRET), aimed at improving global pandemic preparedness. The initiative focuses on integrated planning for responding to respiratory pathogens such as influenza and coronaviruses. It incorporates lessons learned from the COVID-19 pandemic and other health emergencies, emphasizing the need for shared learning and collective action.

Lastly, costs of components like solar panels, batteries, and cloud architecture have lowered over time, making disaster preparedness systems more affordable especially in developing countries. The demand outlook remains strong in the global Disaster Preparedness Systems Market as both governments and private entities seek to reinforce their ability to plan, coordinate, and implement disaster management protocols. With climate change intensifying threats exponentially, the market for supporting technologies and systems stands to grow.

Disaster Preparedness Systems Market Dynamics

Escalating Disasters Propel Disaster Preparedness Market

The rising frequency and intensity of natural disasters, such as natural disasters and climate-related events are the main drivers for this Disaster Preparedness Systems Market. This is a reflection of the global climate where extreme earthquakes, weather-related events, as well as floods, are getting increasingly frequent and damaging. The heightened risk and impact of these disasters necessitate robust preparedness systems to mitigate damage and protect populations.

Governments and organizations worldwide are recognizing the need for advanced disaster response strategies and technologies, resulting in increased investment in preparedness systems. The ongoing and expected rise in disaster occurrences suggests a continued and growing reliance on these systems, indicating sustained market expansion driven by the need to adapt to an increasingly volatile global climate.

COVID-19 Pandemic Highlights Disaster Preparedness Necessity

The COVID-19 pandemic has underscored critical gaps in global disaster response and management systems, significantly impacting the Disaster Preparedness Systems Market. The pandemic's unprecedented nature has exposed vulnerabilities in handling large-scale health crises, leading to a reevaluation of disaster preparedness strategies.

This reevaluation is driving the adoption of more comprehensive and advanced preparedness solutions, including early warning systems, emergency response protocols, and resource allocation strategies. The experience of the pandemic will likely have long-term implications, resulting in increased market growth potential as societies worldwide seek to strengthen their resilience against future health emergencies and other disasters.

Regulatory Policies and Security Threats Enhance Market Growth

Rising regulatory policies for population safety and increasing incidences of criminal and terrorist attacks are accelerating the growth of the Disaster Preparedness Systems Market. Governments are implementing stringent safety regulations, requiring enhanced preparedness measures against man-made threats.

The rise in global terrorism and criminal activities necessitates advanced systems for threat detection, emergency response, and population protection. This regulatory and security landscape is driving the demand for sophisticated disaster preparedness solutions, ensuring compliance and enhancing public safety. The market is expected to grow further, driven by the ongoing need to address these security challenges and adhere to evolving safety regulations.

Critical Infrastructure Protection Necessitates Advanced Preparedness

The need for Critical Infrastructure Protection is a significant factor contributing to the growth of the Disaster Preparedness Systems Market. Essential services such as energy, transportation, and communication rely on resilient infrastructure capable of withstanding various disaster scenarios.

The protection of these vital systems involves the integration of advanced technologies and strategies to prevent, respond to, and recover from disruptive events. The increasing emphasis on safeguarding critical infrastructure, both from natural and human-made hazards, is leading to greater investment in disaster preparedness solutions. This industry trend indicates a market evolving in response to the imperative of maintaining continuous operation of key societal functions, forecasting continued growth driven by the necessity of protecting critical infrastructure.

High Implementation Costs Restrain Disaster Preparedness Systems Market Growth

The growth of the disaster preparedness systems market is significantly limited by high implementation costs. Developing, installing, and maintaining these systems involves substantial financial investment. These costs include not only the technology itself but also the training of personnel, regular system updates, and infrastructure modifications.

For many regions, especially those with limited budgets or in developing countries, these expenses can be prohibitive. High implementation costs can deter governments and organizations from investing in comprehensive disaster preparedness systems, thereby hindering the market's expansion and limiting the widespread adoption of advanced preparedness technologies.

Difficulty in Predicting and Assessing Disasters Limits Disaster Preparedness Systems Market Growth

The inherent difficulty in accurately predicting and assessing disasters also poses a challenge to the growth of the disaster preparedness systems market. Despite advances in technology, predicting the timing, magnitude, and impact of natural disasters remains a complex task with significant uncertainties.

This unpredictability can lead to skepticism about the effectiveness of disaster preparedness systems, affecting investment decisions. Furthermore, the challenge of assessing diverse disaster scenarios requires highly sophisticated and adaptable systems, which can add to the complexity and cost. The limitations in prediction and assessment capabilities can restrain market growth, as potential users might be uncertain about the return on investment in these systems.

Disaster Preparedness Systems Market Segmentation Analysis

By Type Analysis

The Surveillance system segment is pivotal in the Disaster Preparedness Systems Market. Their dominance is driven by the critical need for real-time monitoring and assessment of disaster-prone areas. These systems utilize advanced technologies like CCTV, drones, and sensors to provide continuous surveillance, enabling early warning and rapid response to potential disasters. Their role in enhancing situational awareness and facilitating timely evacuation and resource allocation makes them indispensable in disaster management strategies.

Emergency/Mass Notification Systems are essential for disseminating information quickly. Safety Management Systems help in coordinating disaster response efforts. Earthquake/Seismic Warning Systems are crucial in regions prone to seismic activities. Disaster Recovery and Backup Systems ensure data integrity and continuity of operations post-disaster.

By Solution Analysis

Disaster recovery solutions are the most crucial in ensuring business continuity and data protection. They involve strategies and tools to restore hardware, applications, and data crucial for business operations after a disaster. This segment growth is propelled by the increasing digitalization of enterprises and the need to safeguard digital assets against natural and human-made disasters.

Geospatial solutions provide critical mapping and analysis for disaster planning and response. Situational awareness solutions aggregate and analyze data to provide a comprehensive view of disaster impacts, enhancing decision-making processes. The integration of artificial intelligence and machine learning within geospatial solutions is on the rise, offering predictive modeling capabilities and further improving the accuracy and speed of disaster response and recovery efforts.

By Services Analysis

Consulting services are fundamental in the Disaster Preparedness Systems Market, guiding organizations in developing effective disaster preparedness plans. These services range from risk assessment to the formulation of response strategies, tailored to specific organizational needs and regional risks.

Training and education services are crucial for building disaster response capabilities. Design and integration services ensure the seamless implementation of preparedness systems. Support and maintenance services are vital for the ongoing effectiveness of these systems. Continuous training programs and simulated exercises are becoming more sophisticated, addressing evolving threats and ensuring that response teams remain agile and well-prepared in the face of new challenges.

By Communication Technology Analysis

Emergency response radars lead the market in communication technology. They are essential for tracking and managing disaster responses, offering real-time data critical for coordinating efforts and resources during emergencies. These radars play a pivotal role in enhancing situational awareness, allowing responders to make informed decisions and deploy resources effectively.

First responder tools enhance the efficiency of on-ground response teams. Satellite phones provide reliable communication in areas where traditional networks fail. Vehicle-ready gateways ensure connectivity for mobile response units. These tools are designed to operate seamlessly in challenging environments, enabling swift and effective communication even in remote or disaster-stricken areas.

By End-use Analysis

The Banking, Financial Services, and Insurance (BFSI) sector is heavily reliant on disaster preparedness systems to protect assets, and data, and maintain operations. The financial implications of disasters make robust preparedness essential for this sector. BFSI institutions prioritize the integration of advanced technologies, such as predictive analytics and real-time monitoring, to ensure a proactive response to potential threats.

Each of these sectors requires tailored disaster preparedness strategies, given their unique vulnerabilities and the critical nature of their operations. The integration of disaster preparedness systems is crucial across these industries for resilience and continuity. Furthermore, constant monitoring and regular drills are imperative to refine and optimize these strategies, ensuring the readiness of each sector to mitigate potential risks effectively.

Disaster Preparedness Systems Industry Segments

By Type

- Surveillance System

- Emergency/Mass Notification System

- Safety Management System

- Earthquake/Seismic Warning System

- Disaster Recovery and Backup Systems

- Others

By Solution

- Disaster Recovery Solutions

- Geospatial Solutions

- Situational Awareness Solutions

By Services

- Consulting Services

- Training & Education Services

- Design & Integration Services

- Support & Maintenance Services

By Communication Technology

- Emergency Response Radars

- First Responder Tools

- Satellite Phones

- Vehicle-Ready Gateways

- Others

By End-use

- BFSI

- Energy and Utilities

- Aerospace and Defense

- Manufacturing

- IT and Telecom

- Public Sector

- Transportation and Logistics

- Healthcare

- Others

Disaster Preparedness Systems Market Growth Opportunity

Application Expansion Offers Growth Opportunity in Disaster Preparedness Systems Market

The expansion of applications for disaster preparedness systems across various sectors presents significant growth opportunities in the market. As these systems evolve, they are increasingly being adopted not only by government agencies but also by businesses, schools, healthcare segment institutions, and community organizations.

This broadening application spectrum is driven by the recognition of the importance of disaster preparedness in minimizing risks and ensuring safety. Innovations in technology are enabling more comprehensive and customized disaster preparedness solutions, suitable for different environments and scenarios. This trend indicates a growing market as diverse sectors seek to enhance their resilience to disasters.

Increasing Needs for Emergency Preparedness and Management Fuels Market Growth

The rising need for emergency preparedness and management is a key driver for growth in the disaster preparedness systems market. In an era of increasing natural disasters, geopolitical tensions, and public health emergencies, the demand for effective preparedness and response systems is more critical than ever.

Governments, corporations, and communities are investing more in systems that can predict, mitigate, and manage the impact of various emergencies. This increasing focus on preparedness, coupled with technological advancements in emergency management, signifies a robust expansion in the market, as these systems become essential tools in safeguarding people and assets.

Disaster Preparedness Systems Market Regional Analysis

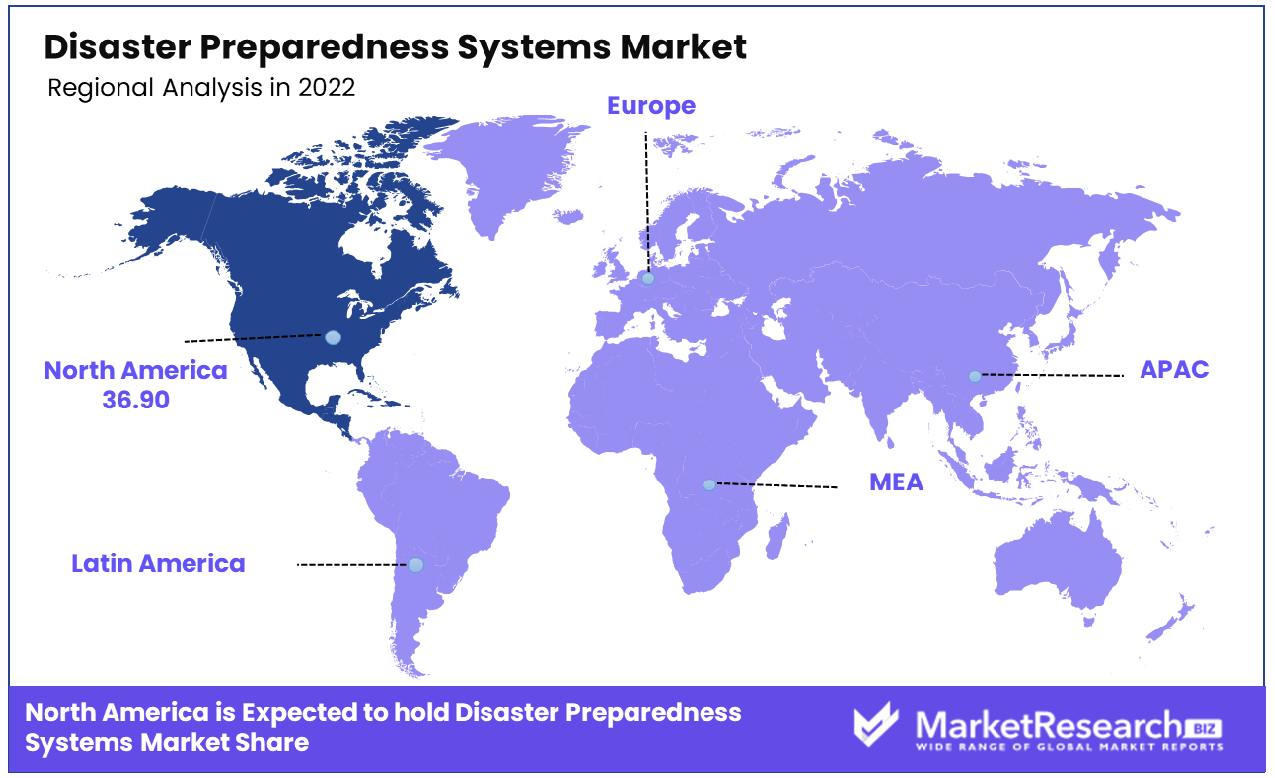

North America Dominates with 36.90% Market Share

North America’s significant 36.90% share in the global Disaster Preparedness Systems Market is primarily driven by the region's high exposure to various natural disasters, such as hurricanes, wildfires, and earthquakes, particularly in the United States. This exposure necessitates robust disaster preparedness and response systems. Additionally, the advanced technological infrastructure in the region allows for the development and implementation of sophisticated disaster preparedness solutions. The strong emphasis on public safety and security by governments in the region, coupled with substantial investments in emergency management, further contributes to the market's growth.

The market dynamics in North America are influenced by the region’s focus on integrating cutting-edge technologies, such as AI, IoT, and big data analytics, into disaster management systems. The ongoing efforts to enhance communication and coordination during emergencies, along with the development of early warning systems, boost the market. Furthermore, the active participation of various non-governmental organizations and private entities in disaster preparedness initiatives complements governmental efforts, enhancing the overall market ecosystem.

Europe's Comprehensive Disaster Management Strategies

Europe’s disaster preparedness systems market is driven by comprehensive disaster management strategies and a strong focus on emergency planning and response. The European Union’s collaborative approach to disaster risk reduction, involving cross-border cooperation and standardization of emergency protocols, supports the market's growth. The region's emphasis on integrating technology in disaster management, along with its well-developed infrastructure, contributes to the development of effective preparedness systems.

Asia-Pacific's Rapid Market Growth Due to Increasing Risk Exposure

In Asia-Pacific, the disaster preparedness systems market is experiencing rapid growth, driven by the region’s increasing exposure to natural disasters like floods, earthquakes, and tsunamis. The growing need to protect densely populated areas, coupled with rising economic development, necessitates robust disaster preparedness measures. The region’s focus on enhancing its emergency management capabilities, along with technological advancements, positions Asia-Pacific as a key emerging market in disaster preparedness systems.

Disaster Preparedness Systems Industry By Region

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of Middle East & Africa

In the Disaster Preparedness Systems Market, the major companies listed are instrumental in enhancing response capabilities and resilience against various emergencies. The market leaders Alertus Technologies LLC and Singlewire Software specialize in mass notification systems, playing critical roles in disseminating timely information during crises, a cornerstone of effective disaster preparedness.

Honeywell International Inc., Siemens, and Johnson Controls, with their vast experience in building and industrial safety solutions, contribute significantly to the market with integrated systems that enhance emergency response and facility safety. IBM and Juvare, LLC, leveraging advanced analytics and data management, provide critical insights for emergency planning and response, underscoring the market's shift towards data-driven preparedness strategies.

Lockheed Martin Corporation and NEC Corporation, key companies known for their defense and technology solutions, offer sophisticated systems for monitoring, simulation, and response coordination, reflecting the increasing complexity and technological integration in disaster preparedness. Motorola Solutions, Inc. and Collins Aerospace, focusing on communication technologies, are key in ensuring robust and reliable communication channels during disasters.

OnSolve and Everbridge, specializing in critical event management solutions, demonstrate the industry's focus on comprehensive platforms that manage the entire lifecycle of disaster response, from alerting to recovery. The major players Esri and LTI Mindtree, with their GIS and IT solutions, respectively, contribute to the market by enhancing situational awareness and decision-making capabilities through spatial analysis and IT infrastructure.

Disaster Preparedness Systems Industry Key Players

- Alertus Technologies LLC

- Honeywell International Inc.

- IBM Corporation

- Juvare, LLC

- Lockheed Martin Corporation

- Motorola Solutions, Inc.

- NEC Corporation

- OnSolve

- Siemens

- Singlewire Software

- Collins Aerospace

- Esri Inc.

- LTI Mindtree

- Johnson Controls

- Everbridge

- Intergraph Corporation

Disaster Preparedness Systems Market Recent Development

- In November 2023, the Virginia Department of Emergency Management (VDEM) announced the allocation of over $2.6 million in grant funding for the Emergency Management Performance Grant Program (EMPG).

- In August 2023, the B.C. government allocated more than $880,000 in funding to 19 communities for emergency preparedness. This funding was provided through the Community Emergency Preparedness Fund to enhance evacuation plans and local emergency alerting systems in these communities.

- In 2023, Commissioner Janez Lenarčič of the European Union (EU) announced the release of over €43 million in humanitarian aid for the entire Latin American and Caribbean region. The 'Disaster Preparedness Saves Lives' event, co-hosted by the EU and the United Nations Office for Disaster Risk Reduction (UNDRR), as part of the EU-Latin America and Caribbean Forum, leading up to the EU-CELAC Summit 2023.

- In 2022, NEC Corporation announced today its collaboration with Haven for Hope, a non-profit charity. Together they will develop technology-enabled solutions designed to increase safety while streamlining operations and providing clients with all of the tools needed. NEC will offer automated emergency notification systems capable of multi-channel broadcasts at critical moments.

Report Scope

Report Features Description Market Value (2022) USD 163.4 Billion Forecast Revenue (2032) USD 385.4 Billion CAGR (2023-2032) 9.2% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type(Surveillance System, Emergency/Mass Notification System, Safety Management System, Earthquake/Seismic Warning System, Disaster Recovery and Backup Systems, Others), By Solution(Disaster Recovery Solutions, Geospatial Solutions, Situational Awareness Solutions), By Services (Consulting Services, Training & Education Services, Design & Integration Services, Support & Maintenance Services), By Communication Technology (Emergency Response Radars, First Responder Tools, Satellite Phones, Vehicle-Ready Gateways, Others), By End-use (BFSI, Energy and Utilities, Aerospace and Defense, Manufacturing, IT and Telecom, Public Sector, Transportation and Logistics, Healthcare, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Alertus Technologies LLC, Honeywell International Inc., IBM Corporation, Juvare, LLC, Motorola Solutions, Inc., OnSolve, Siemens, Singlewire Software, Collins Aerospace, Esri Inc., LTI Mindtree, Johnson Controls, Everbridge, Intergraph Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Alertus Technologies LLC

- Honeywell International Inc.

- IBM Corporation

- Juvare, LLC

- Lockheed Martin Corporation

- Motorola Solutions, Inc.

- NEC Corporation

- OnSolve

- Siemens

- Singlewire Software

- Collins Aerospace

- Esri Inc.

- LTI Mindtree

- Johnson Controls

- Everbridge

- Intergraph Corporation

Our Clients

View Our Licence Options