Global Digital Stethoscope Market By Product Type(Amplifying Stethoscope, Digitalization Stethoscope), By Technology(Integrated Chest-Piece System, Wireless Transmission System, Integrated Receiver Head-Piece System), By Application(General Medicine, Cardiology, Telemedicine, Veterinary, Pediatrics), By End-use(Hospitals & Clinics, Home Healthcare, Nurse Practitioners, EMT/ First Responders, Veterinary), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46743

-

May 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

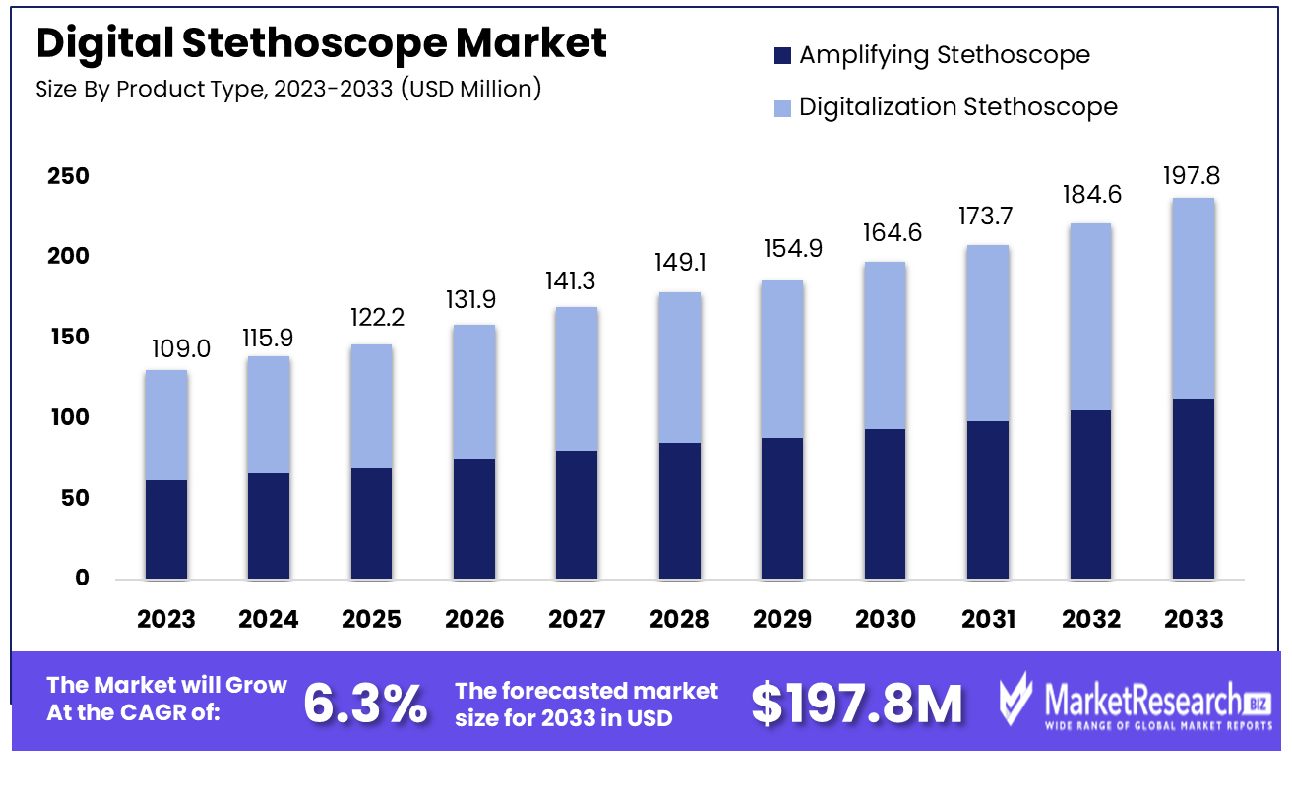

The Global Digital Stethoscope Market was valued at USD 109.0 million in 2023. It is expected to reach USD 197.8 million by 2033, with a CAGR of 6.3% during the forecast period from 2024 to 2033.

The Digital Stethoscope Market encompasses the evolving landscape of medical diagnostics, driven by advancements in technology and healthcare digitization. This market segment pertains to the development, production, and distribution of innovative stethoscope devices integrated with digital functionalities. Digital stethoscopes offer enhanced auscultation capabilities through features like amplification, noise reduction, and data recording, revolutionizing patient care and clinical workflows.

With the convergence of artificial intelligence, telemedicine, and IoT, the Digital Stethoscope Market presents unprecedented opportunities for healthcare providers to improve diagnostic accuracy, remote patient monitoring, and overall healthcare delivery efficiency.

In the realm of healthcare technology, the Digital Stethoscope Market presents a compelling narrative of innovation intersecting with necessity. Traditional stethoscopes, while indispensable in medical diagnosis, have long grappled with issues of hygiene and precision. However, recent findings underscore the urgency for change.

A study spanning from September to December 2022 revealed that a staggering 100% of conventional stethoscopes tested harbored bacterial growth, with Staphylococcus spp. emerging as the predominant contaminant at 50.5%. Moreover, a concurrent survey among medical students in 2022 exposed a disconcerting reality: merely 30.3% of students adhered to cleaning their stethoscopes after each patient encounter, while a concerning 1.5% neglected cleaning altogether.

These revelations serve as catalysts for the burgeoning digital stethoscope market, where advancements in technology converge with imperatives for infection control and diagnostic precision. The demand for digital alternatives, equipped with features such as wireless connectivity, real-time data transmission, and advanced signal processing, is propelled by a confluence of factors including the pressing need for infection prevention, rising healthcare standards, and the pursuit of enhanced patient care outcomes.

As the healthcare landscape continues its digital transformation journey, stakeholders within the industry must recognize the imperative to adopt innovative solutions that not only mitigate risks associated with conventional practices but also elevate the standard of care delivery. The Digital Stethoscope Market stands at the precipice of transformative growth, poised to revolutionize auscultation practices and redefine the paradigm of patient-centric care.

Key Takeaways

- Market Growth: The Global Digital Stethoscope Market was valued at USD 109.0 million in 2023. It is expected to reach USD 197.8 million by 2033, with a CAGR of 6.3% during the forecast period from 2024 to 2033.

- By Product Type: In terms of product type, Digitalization Stethoscope commands a significant 55.6% market share.

- By Technology: Wireless Transmission System leads in technology with 41.2% dominance.

- By Application: Cardiology emerges as the dominant application, capturing a 25.2% share.

- By End-use: Hospitals & Clinics constitute the primary end-use, holding 60.2% dominance.

- Regional Dominance: In North America, the digital stethoscope market holds a 33.2% share.

- Growth Opportunity: The global digital stethoscope market is set for significant growth in 2023, driven by expanding opportunities across regions and segments, along with advancements in technology enhancing diagnostic capabilities.

Driving factors

Integration of Artificial Intelligence in Stethoscopes Drives Market Growth

The Digital Stethoscope Market is experiencing significant growth, primarily fueled by the adoption of next-generation technologies, including artificial intelligence (AI). With rapid technological advancements offering machine learning and AI capabilities, digital stethoscopes are revolutionizing diagnostic practices. AI integration enhances the functionality of stethoscopes by enabling advanced analysis of heart and lung sounds, leading to more accurate diagnoses.

According to recent statistics, the global AI in the healthcare market is projected to reach $45.2 billion by 2026, indicating a substantial opportunity for growth within the digital stethoscope sector. The utilization of AI not only improves diagnostic accuracy but also facilitates remote monitoring, making healthcare more accessible and efficient.

Technological Advancements Enhance Diagnostic Capabilities

The rapid technological advancements in digital stethoscopes are driving market growth by offering enhanced diagnostic capabilities. With features such as noise cancellation, amplification, and customizable frequency settings, modern stethoscopes provide clinicians with clearer and more detailed auscultation. This facilitates early detection methods for diseases, aligning with the growing demand for improved diagnostics.

Furthermore, the integration of machine learning algorithms enables digital stethoscopes to analyze vast amounts of data, identifying subtle abnormalities that may indicate underlying health issues. As a result, healthcare professionals can make more informed decisions, leading to better patient outcomes and increased trust in digital stethoscope technology.

Addressing the Demand for Early Detection and Enhanced Diagnostics

The growing demand for enhanced diagnostics and early detection methods for diseases is a key driver of market growth in the digital stethoscope industry. As the prevalence of chronic diseases continues to rise, there is an urgent need for more accurate and efficient diagnostic tools. Digital stethoscopes offer a solution by providing clinicians with real-time data and actionable insights, facilitating early intervention and improving patient outcomes.

Moreover, the shift towards preventive healthcare further emphasizes the importance of early detection, driving the adoption of digital stethoscopes among healthcare providers. By enabling the timely detection of cardiac and respiratory conditions, digital stethoscopes contribute to reducing healthcare costs and improving overall patient well-being.

Restraining Factors

Lack of Standardization Hinders Market Expansion

The absence of standardization in digital stethoscope technology poses a significant challenge to market growth. With various manufacturers implementing different specifications and features, interoperability issues arise, limiting the widespread adoption of digital stethoscopes across healthcare systems.

This lack of standardization complicates the integration of digital stethoscopes into existing medical workflows, leading to a reluctance among healthcare providers to invest in new technologies. Statistics indicate that the global smart medical device market faces challenges due to the lack of standardization, with estimates suggesting that non-standardized medical devices contribute to approximately 70% of medical errors.

In the context of digital stethoscopes, the absence of uniform standards impedes innovation and inhibits market expansion, as manufacturers prioritize proprietary technologies over interoperability.

Regulatory Hurdles Impede Market Entry

Regulatory and compliance challenges present significant barriers to entry for digital stethoscope manufacturers. Stringent regulations governing medical devices require thorough testing, certification, and approval processes before products can enter the market.

Delays in regulatory approval not only prolong time-to-market but also increase development costs, constraining innovation and investment in digital stethoscope technology. According to industry reports, navigating the regulatory landscape can add years to the product development cycle and millions of dollars in additional expenses.

These challenges discourage new entrants and smaller companies from competing in the digital stethoscope market, limiting competition and stifling innovation. Furthermore, compliance with evolving regulatory requirements, such as data privacy and cybersecurity standards, adds complexity to product development and increases the regulatory burden on manufacturers.

By Product Type Analysis

In terms of product type, Digitalization Stethoscope holds a commanding market share at 55.6%.

In 2023, Digitalization Stethoscope held a dominant market position in the By Product Type segment of the Digital Stethoscope Market, capturing more than a 55.6% share. The Amplifying Stethoscope and Digitalization Stethoscope categories represented key segments within this market landscape, with the latter exhibiting remarkable growth and adoption rates.

The ascent of Digitalization Stethoscopes can be attributed to several factors, including technological advancements, the increasing prevalence of chronic diseases, and the growing demand for remote patient monitoring solutions. Healthcare practitioners and institutions are increasingly recognizing the value of digital stethoscopes in enhancing diagnostic accuracy, facilitating telemedicine consultations, and streamlining patient care processes.

Moreover, Digitalization Stethoscopes offer a range of features and functionalities such as audio amplification, wireless connectivity, and integration with electronic health records (EHR) systems, thereby enabling healthcare professionals to efficiently capture, analyze, and store patient data. These devices are also equipped with advanced signal processing algorithms and noise reduction capabilities, ensuring clearer auscultation and more precise diagnosis even in noisy clinical environments.

As healthcare systems worldwide continue to embrace digital transformation initiatives, the demand for Digitalization Stethoscopes is poised to escalate further. Market players are investing in research and development activities to introduce innovative product offerings with enhanced performance and usability, thereby expanding their market presence and catering to evolving end-user requirements.

Moving forward, the Digitalization Stethoscope segment is anticipated to maintain its momentum, driven by ongoing technological innovation, increasing healthcare expenditure, and the growing emphasis on preventive and personalized medicine. Market stakeholders must remain agile and proactive in adapting to changing market dynamics and leveraging emerging opportunities to sustain their competitive advantage in this rapidly evolving landscape.

By Technology Analysis

Wireless Transmission System leads in technology with a dominant 41.2% share.

In 2023, within the By-technology segment of the Digital Stethoscope Market, the Integrated Chest-Piece System, Wireless Transmission System, and Integrated Receiver Head-Piece System emerged as pivotal components shaping market dynamics. Among these, the Wireless Transmission System stood out, exhibiting a commanding presence by securing a dominant market position with an impressive share exceeding 41.2%. This significant market share underscores the pivotal role played by wireless transmission technologies in revolutionizing the landscape of digital stethoscopes.

The Wireless Transmission System's ascendancy can be attributed to several factors. Firstly, its ability to seamlessly transmit auscultation data wirelessly enables healthcare professionals to conduct examinations with greater mobility and flexibility, enhancing patient care delivery. Moreover, the elimination of cumbersome cords and cables reduces interference during examinations, ensuring optimal signal quality and accuracy in diagnosis. Additionally, the compatibility of wireless transmission systems with various digital devices and platforms fosters interoperability, facilitating seamless integration into existing healthcare infrastructures.

Furthermore, the growing emphasis on telemedicine and remote patient monitoring solutions amid the global healthcare paradigm shift has propelled the adoption of wireless transmission systems. These systems empower healthcare providers to remotely monitor patients' vital signs and cardiac health, thereby enhancing disease management and preventive care initiatives. Moreover, the ongoing advancements in wireless technology, including enhanced connectivity, reduced power consumption, and increased data transmission speeds, further bolster the appeal and utility of wireless transmission systems in the digital stethoscope market.

As the healthcare industry continues to embrace digital transformation and innovation, the Wireless Transmission System is poised to maintain its prominence, driving continued growth and evolution within the digital stethoscope market landscape.

By Application Analysis

Cardiology emerges as the top application, commanding 25.2% of the market.

In 2023, the Cardiology application segment emerged as a dominant force within the Digital Stethoscope Market, securing a substantial market share exceeding 25.2%. This market dominance underscores the pivotal role played by digital stethoscopes in advancing cardiac healthcare diagnostics and treatment modalities.

Cardiology's prominent position within the market can be attributed to several key factors. Firstly, the increasing prevalence of cardiovascular diseases worldwide has heightened the demand for advanced diagnostic tools capable of accurately assessing cardiac health. Digital stethoscopes equipped with innovative features such as digital signal processing and auscultation analysis algorithms empower cardiologists to detect subtle cardiac abnormalities with enhanced precision, facilitating timely intervention and treatment planning.

Moreover, the versatility of digital stethoscopes in cardiology practice extends beyond traditional auscultation, encompassing functionalities such as phonocardiography and telecardiology. These capabilities enable healthcare providers to conduct comprehensive cardiac assessments, monitor patients remotely, and collaborate with specialists in real time, thereby optimizing patient care delivery and outcomes.

Furthermore, the integration of digital stethoscopes into telemedicine platforms has revolutionized the delivery of cardiac healthcare services, particularly in remote or underserved areas. Telecardiology initiatives leveraging digital stethoscopes enable remote consultation, diagnosis, and monitoring of cardiac patients, bridging geographical barriers and expanding access to specialized cardiac care.

As the burden of cardiovascular diseases continues to escalate globally, the Cardiology application segment is poised for sustained growth and innovation within the Digital Stethoscope Market. Advancements in technology, coupled with evolving healthcare paradigms emphasizing preventive cardiology and personalized medicine, will further propel the adoption of digital stethoscopes in cardiac healthcare settings.

By End-use Analysis

Hospitals & Clinics lead end-use, with a commanding 60.2% dominance.

In 2023, the Hospitals & Clinics segment asserted its dominance within the Digital Stethoscope Market, commanding a significant market share exceeding 60.2%. This substantial market position underscores the pivotal role played by hospitals and clinics in driving the adoption and utilization of digital stethoscopes across diverse healthcare settings.

Hospitals & Clinics emerged as the leading end-user segment due to several key factors. Firstly, the widespread deployment of digital stethoscopes within hospital environments reflects the growing recognition of these advanced diagnostic tools as indispensable assets in modern healthcare practice. Equipped with cutting-edge features such as electronic amplification, noise reduction, and Bluetooth connectivity, digital stethoscopes enable healthcare professionals to conduct thorough auscultation examinations with unparalleled precision and efficiency.

Moreover, the versatility of digital stethoscopes in catering to a broad spectrum of medical specialties further solidifies their appeal within hospital and clinic settings. From cardiology and pulmonology to pediatrics and internal medicine, digital stethoscopes offer clinicians a multifaceted diagnostic tool capable of addressing diverse patient needs and clinical scenarios.

Furthermore, the integration of digital stethoscopes into hospital information systems and electronic health records enhances workflow efficiency and data management, facilitating seamless documentation and communication of auscultation findings among healthcare teams.

As the demand for advanced diagnostic solutions continues to grow within the healthcare industry, hospitals and clinics are expected to remain at the forefront of digital stethoscope adoption and utilization. Ongoing technological advancements, coupled with evolving healthcare delivery models emphasizing patient-centric care and clinical efficiency, will further propel the integration of digital stethoscopes into hospital and clinic workflows, shaping the future landscape of the Digital Stethoscope Market.

Key Market Segments

By Product Type

- Amplifying Stethoscope

- Digitalization Stethoscope

By Technology

- Integrated Chest-Piece System

- Wireless Transmission System

- Integrated Receiver Head-Piece System

By Application

- General Medicine

- Cardiology

- Telemedicine

- Veterinary

- Pediatrics

By End-use

- Hospitals & Clinics

- Home Healthcare

- Nurse Practitioners

- EMT/ First Responders

- Veterinary

Growth Opportunity

Expansion of Market Opportunities by Region and Segment

The digital stethoscope market is poised for significant expansion in 2023, driven by burgeoning opportunities across various regions and segments. Regions such as North America, Europe, and Asia-Pacific are witnessing robust growth due to increasing healthcare expenditure, rising awareness about advanced diagnostic tools, and the adoption of telemedicine practices.

North America, in particular, is anticipated to maintain its dominance, fueled by the presence of key market players and favorable reimbursement policies. Moreover, emerging economies in Asia-Pacific, such as China and India, are experiencing rapid digitization of healthcare systems, presenting lucrative prospects for market players.

Development of Technologically Advanced Digital Stethoscopes

Technological advancements in digital stethoscopes are reshaping the market landscape, offering enhanced functionalities and diagnostic capabilities. Innovations such as wireless connectivity, noise cancellation algorithms, and integration with mobile applications are driving the adoption of digital stethoscopes among healthcare professionals.

These advancements not only enable remote patient monitoring and telemedicine services but also facilitate real-time data analysis and interpretation. Furthermore, the integration of artificial intelligence (AI) and machine learning algorithms is revolutionizing auscultation, providing clinicians with valuable insights and improving diagnostic accuracy.

Latest Trends

Growing Emphasis on Cost-effective Solutions

The global digital stethoscope market is witnessing a notable trend towards the development and adoption of cost-effective solutions, particularly tailored to economically constrained regions. This trend is fueled by the pressing need to enhance healthcare accessibility and affordability worldwide. By offering digital stethoscopes at more affordable price points, manufacturers are poised to penetrate emerging markets while simultaneously addressing healthcare disparities.

This strategic shift aligns with broader initiatives aimed at achieving universal health coverage and improving healthcare outcomes across diverse socioeconomic landscapes. Furthermore, the emphasis on cost-effectiveness underscores the industry's commitment to fostering inclusivity and equitable access to advanced medical technologies.

Regulatory Milestones Propel Commercialization

Regulatory approvals for the commercialization of digital stethoscope technologies mark a significant milestone for the industry, heralding a new era of innovation and accessibility. These approvals validate the safety, efficacy, and quality of digital stethoscopes, instilling confidence among healthcare professionals and consumers alike. By complying with rigorous regulatory standards, manufacturers pave the way for the widespread adoption and integration of digital stethoscopes into clinical practice.

Moreover, regulatory clearance facilitates market entry, enabling companies to capitalize on burgeoning opportunities and expand their global footprint. As regulatory frameworks continue to evolve and streamline, the digital stethoscope market is poised for accelerated growth and transformation. These regulatory advancements underscore the industry's commitment to upholding stringent quality standards and fostering patient-centric healthcare solutions.

Regional Analysis

In North America, the digital stethoscope market is projected to grow by 33.2% annually.

In the digital stethoscope market, various regions exhibit unique dynamics, reflecting diverse healthcare infrastructures, technological advancements, and regulatory landscapes.

North America, dominating with a significant market share of 33.2%, stands at the forefront of digital stethoscope adoption. The region's robust healthcare infrastructure, coupled with substantial investments in healthcare technology, fuels market growth. Moreover, the presence of key market players and favorable reimbursement policies further propels the market forward.

Europe, characterized by a mature healthcare system and increasing adoption of digital health solutions, holds a noteworthy share in the global digital stethoscope market. Countries like Germany, France, and the UK are key contributors, driven by rising healthcare expenditures and a growing focus on patient-centric care.

Asia Pacific emerges as a promising market for digital stethoscopes, propelled by rapid technological advancements, expanding healthcare access, and increasing healthcare spending in countries like China, India, and Japan. Additionally, the growing prevalence of chronic diseases and the shift towards preventive healthcare drive the demand for advanced diagnostic tools, including digital stethoscopes, in the region.

In the Middle East & Africa and Latin America regions, the digital stethoscope market is witnessing gradual but steady growth. Factors such as improving healthcare infrastructure, rising awareness about telemedicine, and government initiatives to enhance healthcare accessibility contribute to market expansion. While these regions currently hold a smaller market share compared to others, ongoing developments in healthcare delivery systems and increasing investments in digital health initiatives are expected to drive significant growth in the coming years.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global digital stethoscope market witnessed a dynamic landscape shaped by key players striving for innovation, market expansion, and strategic collaborations. Among the notable contenders, 3M, a renowned multinational conglomerate, exhibited a robust presence and played a pivotal role in driving market advancements.

3M's prominence in the digital stethoscope market stems from its commitment to delivering high-quality, technologically advanced medical devices. The company's extensive experience in healthcare solutions, coupled with its focus on research and development, positions it as a frontrunner in the industry. In 2023, 3M continued to leverage its expertise to introduce innovative digital stethoscope models, catering to evolving clinical needs and enhancing diagnostic accuracy.

Moreover, 3M's global reach and established distribution channels enabled widespread market penetration, contributing to its sustained market leadership. The company's strategic initiatives, including strategic partnerships with healthcare institutions and continuous investment in product enhancement, further solidified its position in the competitive landscape.

Furthermore, 3M's commitment to sustainability and adherence to regulatory standards resonated well with healthcare professionals and end-users, fostering trust and brand loyalty. As the digital stethoscope market continues to evolve, 3M remains well-positioned to capitalize on emerging opportunities and maintain its competitive edge through a combination of innovation, quality, and customer-centric approach.

Market Key Players

- 3M

- eKuore

- American Diagnostic Corporation

- Contec Medical Systems Co., Ltd.

- Meditech Equipment Co., Ltd.

- Ayu Devices

- Thinklabs Medical LLC

- Cardionics

Recent Developement

- In March 2024, Monash University student Meagan Roff receives the Women in STEMM Student Leader Award for innovative research on neonatal digital stethoscope technology, aiming to enhance newborn healthcare.

- In October 2022, Peter Ma and the MixPose team won the COVID-19 Detect and Protect Challenge with their AI Digital Stethoscope, offering a low-cost solution for remote patient diagnosis and monitoring. They aim to empower doctors and enhance healthcare accessibility globally.

Report Scope

Report Features Description Market Value (2023) USD 109.0 Million Forecast Revenue (2033) USD 197.8 Million CAGR (2024-2032) 6.3% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type(Amplifying Stethoscope, Digitalization Stethoscope), By Technology(Integrated Chest-Piece System, Wireless Transmission System, Integrated Receiver Head-Piece System), By Application(General Medicine, Cardiology, Telemedicine, Veterinary, Pediatrics), By End-use(Hospitals & Clinics, Home Healthcare, Nurse Practitioners, EMT/ First Responders, Veterinary) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape 3M, eKuore, American Diagnostic Corporation, Contec Medical Systems Co., Ltd., Meditech Equipment Co., Ltd., Ayu Devices, Thinklabs Medical LLC, Cardionics Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- 3M

- eKuore

- American Diagnostic Corporation

- Contec Medical Systems Co., Ltd.

- Meditech Equipment Co., Ltd.

- Ayu Devices

- Thinklabs Medical LLC

- Cardionics

Our Clients

View Our Licence Options