Global Dental Insurance Market By Coverage(Dental Health Maintenance Organizations (DHMO), Dental Preferred Provider Organizations (DPPO), Dental Indemnity Plans, Others), By Type(Major, Basic, Preventive), By Demographics(Adults, Minors, Senior Citizens), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

46954

-

June 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

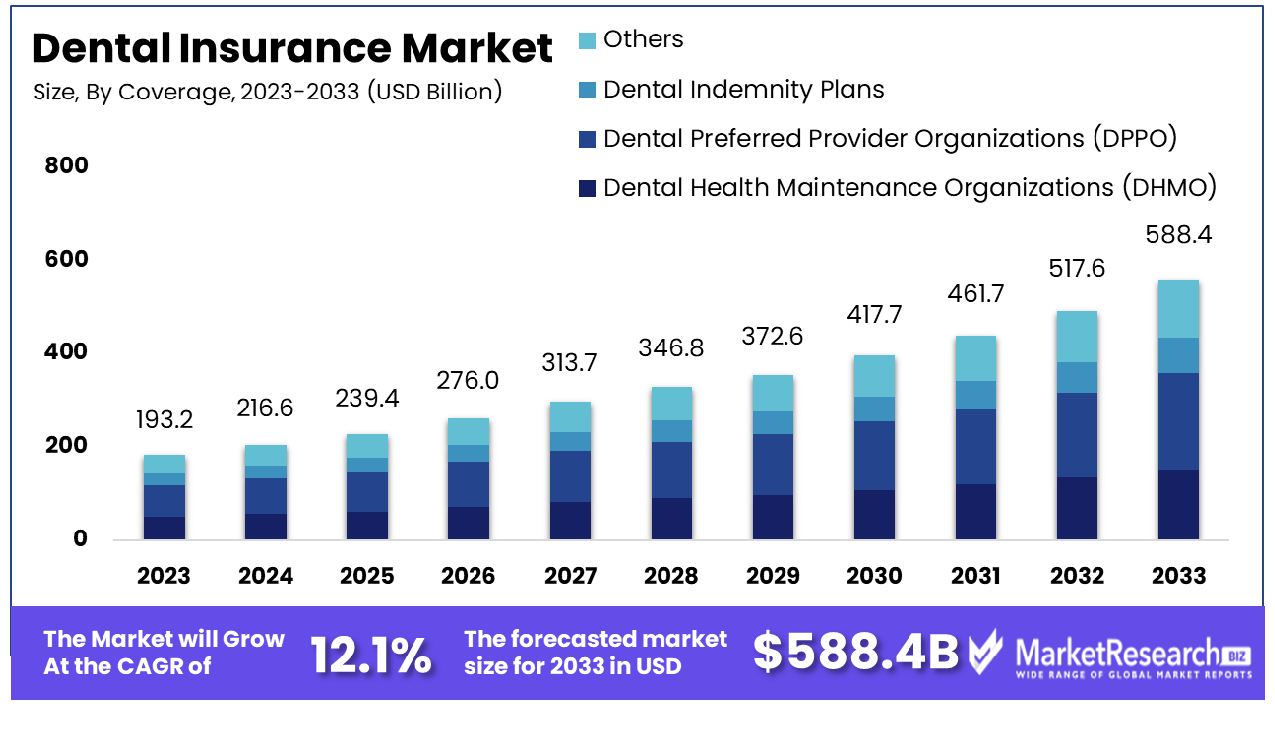

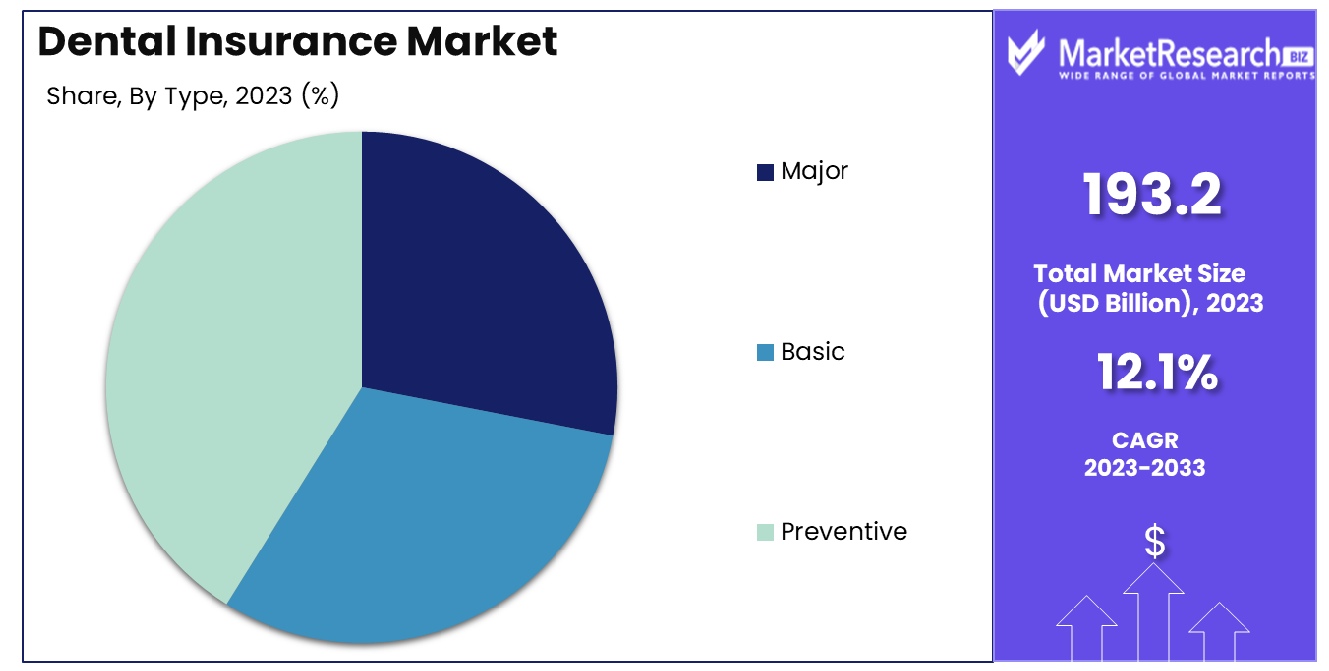

The Global Dental Insurance Market was valued at USD 193.2 billion in 2023. It is expected to reach USD 588.4 billion by 2033, with a CAGR of 12.1% during the forecast period from 2024 to 2033.

The Dental Insurance Market comprises services offering coverage for preventive, minor, and major dental care treatments. It is structured to reduce the financial burden of dental procedures for individuals and families. This market is pivotal for stakeholders in the healthcare sector, promising avenues for growth through diversified plan options and increasing awareness about oral health.

The potential for expansion is driven by rising healthcare expenditures and the integration of dental services into broader health insurance plans. This market's evolution is also influenced by regulatory changes and the adoption of digital solutions for plan management. The dental insurance market is observing nuanced dynamics, heavily influenced by demographic shifts and varying healthcare priorities across regions.

In recent years, there has been a discernible decline in dental service utilization in certain countries, notably Sweden. Data from 2022 highlights that approximately 3.9 million Swedes aged 24 years or older sought dental care, marking the second-lowest annual figure since 2009. This trend is more pronounced in public dental clinics than in private ones, suggesting a potential shift in consumer preference or access issues in the public sector.

Conversely, in the United States, dental care remains a critical component of health maintenance across all age groups. In 2022, 64% of individuals aged 18-44 reported visiting a dentist within the year, with slightly higher rates among those aged 45-64 (68%). However, the persistence of high dental disease rates, such as edentulism, affecting 20% of the elderly, and gum disease impacting two-thirds of this demographic, underscores the ongoing need for comprehensive dental coverage.

Furthermore, a staggering 96% of older adults have experienced cavities at some point. These disparities in dental health service utilization and the prevalent oral health issues highlight the significant potential for growth in the dental insurance market. Insurers who tailor their offerings to address the specific needs of diverse demographic groups, especially by enhancing accessibility and affordability in regions showing declining service utilization, may find substantial opportunities. There is also a crucial role for educational initiatives to raise awareness about the importance of regular dental care, which could drive a higher uptake of dental insurance plans.

Key Takeaways

- Market Growth: The Global Dental Insurance Market was valued at USD 193.2 billion in 2023. It is expected to reach USD 588.4 billion by 2033, with a CAGR of 12.1% during the forecast period from 2024 to 2033.

- By Coverage: DPPOs led the coverage segment with a 32% market share.

- By Type: Preventive dental services led the type category, holding 47%.

- By Demographics: Senior citizens dominated demographics, representing 54% of users.

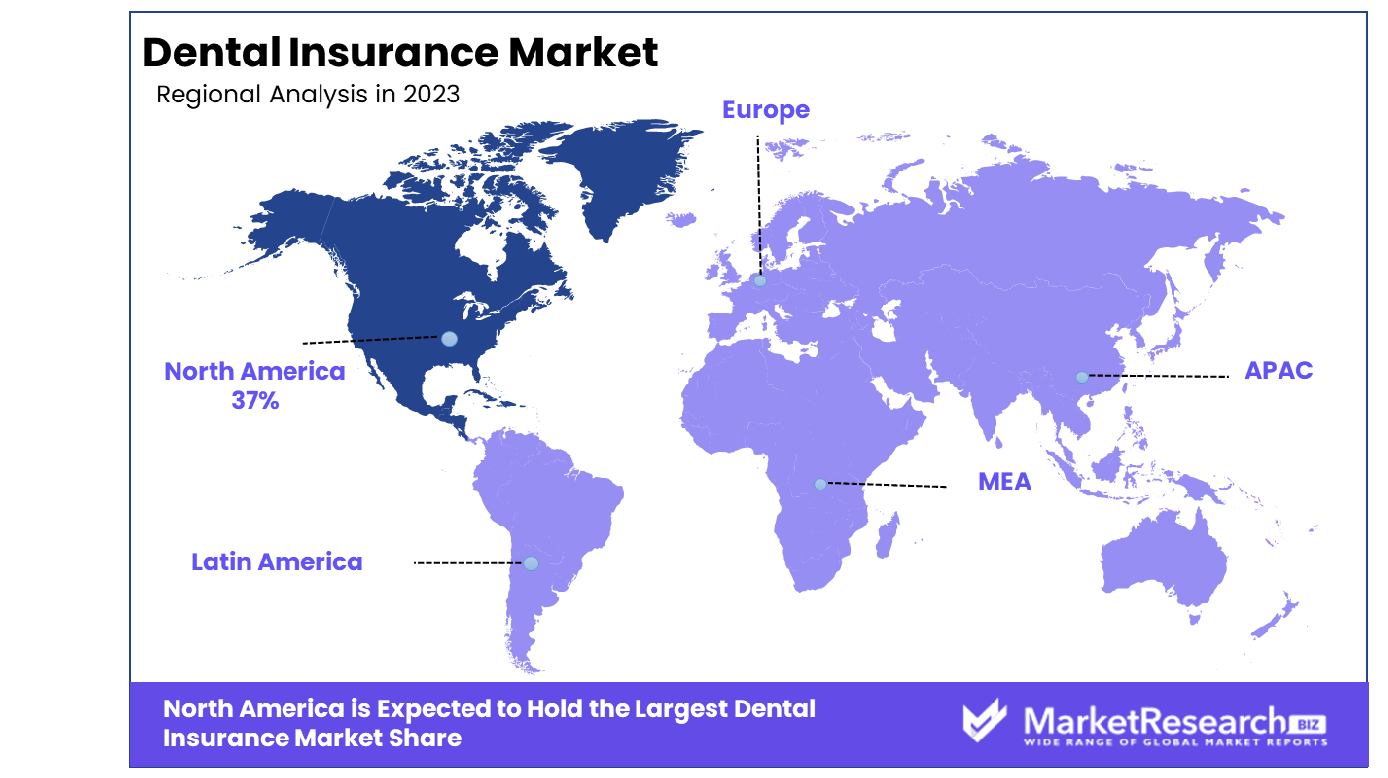

- Regional Dominance: North America holds 37% of the global dental insurance market.

- Growth Opportunity: In 2023, the global dental insurance market will grow through the convergence of health and dental policies and the integration of AI and ML in the Insurtech platform.

Driving factors

Escalating Dental Care Costs and Enhanced Oral Health Awareness Propel Demand for Dental Insurance

The dental insurance market is significantly driven by the rising costs of dental care, which have become increasingly prohibitive for many individuals without insurance coverage. As dental procedures become more expensive, the perceived value of dental insurance grows, compelling more consumers to seek insurance plans that make dental care more affordable. Concurrently, there is a growing awareness about the importance of maintaining oral health and its impact on overall health.

Educational campaigns and public health initiatives have successfully increased public knowledge about oral hygiene and the need for regular dental check-ups, further boosting the adoption of dental insurance. Statistics often highlight a direct correlation between rising healthcare costs and increased insurance uptake, suggesting a robust growth trajectory for the dental insurance market in response to these economic dynamics.

Increasing Incidence of Dental Diseases Accelerates the Necessity for Dental Insurance

The prevalence of dental conditions such as tooth decay, gum diseases, and oral cancers is on the rise, influenced by factors such as poor dietary habits, lack of proper oral hygiene, and genetic predispositions. These diseases necessitate frequent and sometimes costly dental interventions, which are financially burdensome without insurance.

As more individuals become affected by these conditions, the demand for dental insurance plans that cover regular and specialized treatments increases. This trend not only supports market growth but also emphasizes the essential role of dental insurance in managing healthcare expenses related to oral diseases.

Favorable Demographic Shifts and Rising Disposable Incomes Boost Dental Insurance Coverage

Demographic trends, particularly the aging population, significantly impact the dental insurance market. Older adults typically experience more dental problems, which increases their need for dental services and, consequently, dental insurance. Furthermore, as global economies grow and disposable incomes rise, more individuals can afford insurance products, including dental coverage.

This financial ability allows for greater consumer spending on health and wellness, including preventive dental care, which is often facilitated by insurance coverage. The synergy of these demographic and economic factors creates a fertile environment for the expansion of the dental insurance market, making it an increasingly vital component of the healthcare insurance industry.

Restraining Factors

Limited Awareness of Oral Health Impedes Market Expansion

One significant barrier to the growth of the dental insurance market is the limited awareness among the general population about the importance of oral health. In regions where oral health education is not adequately emphasized, individuals may not recognize the need for regular dental care, thus devaluing the benefits of dental insurance. This lack of awareness can lead to a lower prioritization of dental insurance compared to other types of health insurance, stalling market growth.

The limited understanding of the link between oral health and overall health further exacerbates this issue, as people may not be aware of the potential long-term health consequences of neglected dental care. Addressing this challenge requires targeted educational campaigns and outreach efforts to enhance the perceived value of dental insurance by highlighting the critical nature of maintaining oral health.

High Costs and Complexity of Dental Insurance Deter Potential Consumers

The cost and complexity of dental procedures often reflect directly on the premiums and terms of dental insurance plans, making them less attractive to potential subscribers. High premiums can deter individuals, especially those in lower income brackets, from purchasing dental insurance, even if they acknowledge the necessity of dental care. Additionally, the complexity and perceived inadequacy of certain plans, which may not cover all necessary procedures or have high deductibles and copays, can further discourage enrollment.

This situation is exacerbated by a general lack of transparency in insurance plan details, which can confuse consumers and lead them to forego purchasing coverage altogether. Simplifying dental insurance offerings and increasing transparency in coverage terms and costs are essential steps toward mitigating these restraining factors and fostering market growth.

By Coverage Analysis

In the coverage category, Dental Preferred Provider Organizations (DPPOs) dominated with a 32% market share.

In 2023, Dental Preferred Provider Organizations (DPPO) held a dominant market position in the By Coverage segment of the Dental Insurance Market, capturing more than 32% share. This segment is characterized by its comprehensive network of dental service providers offering various dental care plans at reduced rates. The DPPO model facilitates lower out-of-pocket costs for patients while providing a wide range of dental services, which enhances its attractiveness to consumers seeking flexibility and affordability in dental care.

Furthermore, Dental Health Maintenance Organizations (DHMO) also represent a significant portion of the market. These plans are typically the most cost-effective for patients, involving lower premiums and no deductibles, but they require patients to choose from a specified network of dentists for services.

Dental Indemnity Plans, offering the highest degree of provider flexibility, allow patients to visit any dentist of their choice without network restrictions. However, this segment often comes with higher premiums and deductibles, reflecting the increased freedom it provides.

The 'Others' category includes various minor plans and discount programs that do not fit neatly into the traditional insurance categories but offer alternative forms of financial protection and discounts on dental services.

The segmentation of the Dental Insurance Market by coverage type highlights the diversity of options available to consumers and indicates a highly competitive landscape where DPPOs lead due to their balance of cost and flexibility. The choice of plan typically aligns with consumer priorities regarding cost, service freedom, and the breadth of available dental care services.

By Type Analysis

By type, preventive dental services led, capturing 47% of the market segment.

In 2023, Preventive held a dominant market position in the By Type segment of the Dental Insurance Market, capturing more than a 47% share. This segment encompasses services such as annual cleanings, routine check-ups, and other preventive measures that are essential for maintaining oral health. The high demand for preventive dental insurance plans can be attributed to their role in mitigating more severe dental problems, reducing the need for expensive treatments, and lowering overall healthcare costs.

The Basic segment also plays a crucial role in the dental insurance market, covering procedures like fillings, extractions, and periodontal treatments. These services are generally more frequent than major procedures and represent a significant portion of dental care needs for the average consumer.

Lastly, the Major segment includes more complex and costly procedures such as crowns, bridges, dentures, and orthodontics. Although this segment captures a smaller market share compared to Preventive and Basic services, it is critical for comprehensive dental virtual care and typically commands higher premium costs due to the complexity and cost of the treatments involved.

The segmentation of the Dental Insurance Market by type underscores the diverse needs of consumers, with Preventive services leading due to their fundamental role in maintaining oral health and reducing long-term costs. This segment's prominence reflects a growing consumer awareness of the importance of regular dental care and its impact on overall health.

By Demographics Analysis

Among demographics, senior citizens were the largest group, dominating with a 54% share.

In 2023, Senior Citizens held a dominant market position in the By Demographics segment of the Dental Insurance Market, capturing more than a 54% share. This substantial market share underscores the critical importance of dental care for older adults, who often face numerous dental challenges such as gum diseases, tooth loss, and other age-related dental issues. Dental insurance for senior citizens is designed to mitigate the financial burden of dental treatments, which becomes increasingly vital as dental health impacts overall health significantly in later years.

Adults, constituting the next significant segment, also represent a substantial portion of the market. This group typically requires dental insurance to cover routine care as well as unforeseen dental procedures that can arise due to lifestyle, dietary habits, or neglect accumulated over the years.

Minors, the third demographic segment, include dependents typically covered under family dental plans. Coverage for minors focuses on preventive care and treatments such as orthodontics, which are common in younger age groups. Ensuring good dental health at an early age sets the foundation for healthy oral care habits and reduces the need for extensive dental work later in life.

Overall, the segmentation of the Dental Insurance Market by demographics highlights the tailored approaches needed to address the specific dental care needs of different age groups, with senior citizens leading due to their heightened needs and the increasing acknowledgment of the integral connection between dental health and general health.

Key Market Segments

By Coverage

- Dental Health Maintenance Organizations (DHMO)

- Dental Preferred Provider Organizations (DPPO)

- Dental Indemnity Plans

- Others

By Type

- Major

- Basic

- Preventive

By Demographics

- Adults

- Minors

- Senior Citizens

Growth Opportunity

Convergence of Health and Dental Insurance

In 2023, a significant growth opportunity within the global dental insurance market can be attributed to the increasing convergence of health and dental insurance. This trend is driven by the growing recognition of oral health's critical role in overall health outcomes. As healthcare providers and insurance companies acknowledge the interconnectedness of dental and general health, integrated policies are becoming more prevalent.

These integrated insurance products not only offer a comprehensive health coverage solution but also promise enhanced customer satisfaction through simplified policy management and potentially lower premiums. The integration encourages preventative care, which can lead to reduced long-term medical costs, underpinning the market's expansion.

Integration of AI and ML Technologies in Insurtech Platforms

The integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies into Insurtech platforms represents another robust growth avenue for the global dental insurance market in 2023. AI and ML are revolutionizing the insurance landscape by enabling more personalized, efficient, and accurate service offerings. In dental insurance, these technologies facilitate advanced data analytics for risk assessment and fraud detection, and streamline claims processing, enhancing operational efficiencies.

Moreover, AI-driven tools can provide predictive analytics, helping insurers design products that better meet the evolving needs of consumers. The adoption of these technologies not only improves customer engagement through tailored interactions but also helps in maintaining a competitive edge in a rapidly evolving insurance market.

Latest Trends

Market Consolidation Among Dental Insurance Providers

The global dental insurance market in 2023 is witnessing significant consolidation, as major players merge and acquire smaller entities to expand their market reach and streamline operations. This consolidation is driven by the need to leverage economies of scale, enhance bargaining power, and diversify service offerings.

By consolidating, companies are better positioned to invest in advanced technologies and improve their service delivery, which is critical in an increasingly competitive market. The trend toward consolidation is also a response to rising healthcare costs and the need for more robust financial stability within the insurance sector.

Shift Towards Consumer-Driven Dental Insurance Models

A pivotal trend shaping the global dental insurance market in 2023 is the shift towards consumer-driven models. These models emphasize giving consumers more control over their dental care decisions and finances. High-deductible health plans (HDHPs) coupled with health savings accounts (HSAs) or flexible spending accounts (FSAs) are becoming popular, allowing consumers to manage their dental care expenses better.

This shift is fueled by a growing demand for transparency in pricing and the need for personalized insurance solutions that cater to individual health needs and budget constraints. Consumer-driven models not only enhance customer satisfaction but also encourage preventative dental care, thereby potentially reducing overall healthcare costs and claim frequencies for insurers.

Regional Analysis

North America holds a 37% share of the global dental insurance market, dominating the sector.

The global dental insurance market is segmented into five key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each exhibiting distinct market dynamics and growth potentials.

North America dominates the dental insurance landscape, accounting for 37% of the global market. The region's leadership is underpinned by a well-established healthcare infrastructure, high healthcare expenditure per capita, and a strong presence of major insurance companies. Regulatory support for healthcare benefits also drives substantial market growth in this region.

Europe holds a significant share of the market, driven by widespread awareness of oral health and robust healthcare policies that include dental insurance as part of public health benefits. The market is mature, with high penetration rates of dental insurance policies, particularly in Western European countries.

The Asia Pacific region is experiencing the fastest growth in dental insurance, fueled by rising disposable incomes, increasing awareness about oral health, and governmental initiatives promoting health insurance. Countries like China and India are pivotal markets, with their large populations and growing middle class investing more in health insurance products.

The Middle East & Africa region, although smaller in comparison, is witnessing gradual growth. Improvements in healthcare infrastructure and increasing private health expenditures are key drivers. The market's expansion is further supported by the rising expatriate population, which often receives health benefits including dental coverage.

Latin America's market is emerging, with gradual increases in consumer demand for dental insurance driven by improving economic conditions and a growing emphasis on personal health and wellness.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global dental insurance market is significantly shaped by key players such as Cigna, AFLAC Inc., AXA, Allianz SE, Ameritas Life Insurance Corp, Aetna, United HealthCare Services Inc., Delta Dental Plans Association, Metlife Services & Solutions, United Concordia, HDFC Ergo Health Insurance Ltd, and other pivotal entities. Each of these companies plays a critical role in defining market dynamics through strategic initiatives, product diversification, and technological integration.

Cigna continues to stand out for its extensive global network and customizable dental plans, catering to both individual and corporate clients. AFLAC Inc. distinguishes itself with specialized policies that focus on supplemental dental coverage, enhancing its attractiveness to a niche market segment.

AXA and Allianz SE are leveraging their strong European presence to expand their dental insurance offerings, incorporating innovative coverage options that address a broad spectrum of consumer needs from preventive care to major dental surgeries.

Ameritas is noted for its focus on customer service excellence and flexible benefits solutions, while Aetna and United HealthCare Services Inc. are integrating advanced digital tools to simplify the customer journey, from enrollment through claims processing.

Delta Dental Plans Association remains a dominant player in the U.S., known for its extensive network of dental care providers and tailored insurance products. MetLife Services & Solutions and United Concordia are enhancing their competitive edge through partnerships and customer-centric health benefit solutions.

Emerging players like HDFC Ergo Health Insurance Ltd are capturing market share in rapidly growing regions like Asia, offering tailored dental insurance products that cater to the specific health needs and economic conditions of local populations.

Together, these key companies are not only driving competitive strategies but also significantly influencing market growth through innovation and customer engagement in the dental insurance sector.

Market Key Players

- Cigna

- AFLAC Inc

- AXA

- Allianz SE

- Ameritas Life Insurance Corp

- Aetna

- United HealthCare Services Inc.

- Delta Dental Plans Association

- Metlife Services & Solutions

- United Concordia

- HDFC Ergo Health Insurance Ltd

- Other Key Players

Recent Development

- In May 2024, Loma Linda University School of Dentistry graduates celebrate innovation and community support. Chief Information Officer David Tsao shares insights, emphasizing persistence and service. Students reflect on compassion and diversity in dentistry.

- In May 2024, Plum founders Abhishek Poddar and Saurabh Arora innovated health insurance with comprehensive features like dental plans and chronic disease management. They aim for wider reach and tech integration, serving 4,000+ firms.

Report Scope

Report Features Description Market Value (2023) USD 193.2 Billion Forecast Revenue (2033) USD 588.4 Billion CAGR (2024-2032) 12.1% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Coverage(Dental Health Maintenance Organizations (DHMO), Dental Preferred Provider Organizations (DPPO), Dental Indemnity Plans, Others), By Type(Major, Basic, Preventive), By Demographics(Adults, Minors, Senior Citizens) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Cigna, AFLAC Inc, AXA, Allianz SE, Ameritas Life Insurance Corp, Aetna, United HealthCare Services Inc., Delta Dental Plans Association, Metlife Services & Solutions, United Concordia, HDFC Ergo Health Insurance Ltd, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Cigna

- AFLAC Inc

- AXA

- Allianz SE

- Ameritas Life Insurance Corp

- Aetna

- United HealthCare Services Inc.

- Delta Dental Plans Association

- Metlife Services & Solutions

- United Concordia

- HDFC Ergo Health Insurance Ltd

- Other Key Players

Our Clients

View Our Licence Options