Global Deferiprone Market By Type(Tablets, Oral Solutions, Capsules), By Application(Transfusional Iron Overload, NTDT Caused Iron Overload), By Distribution Channel(Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2024-2033

-

48732

-

July 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

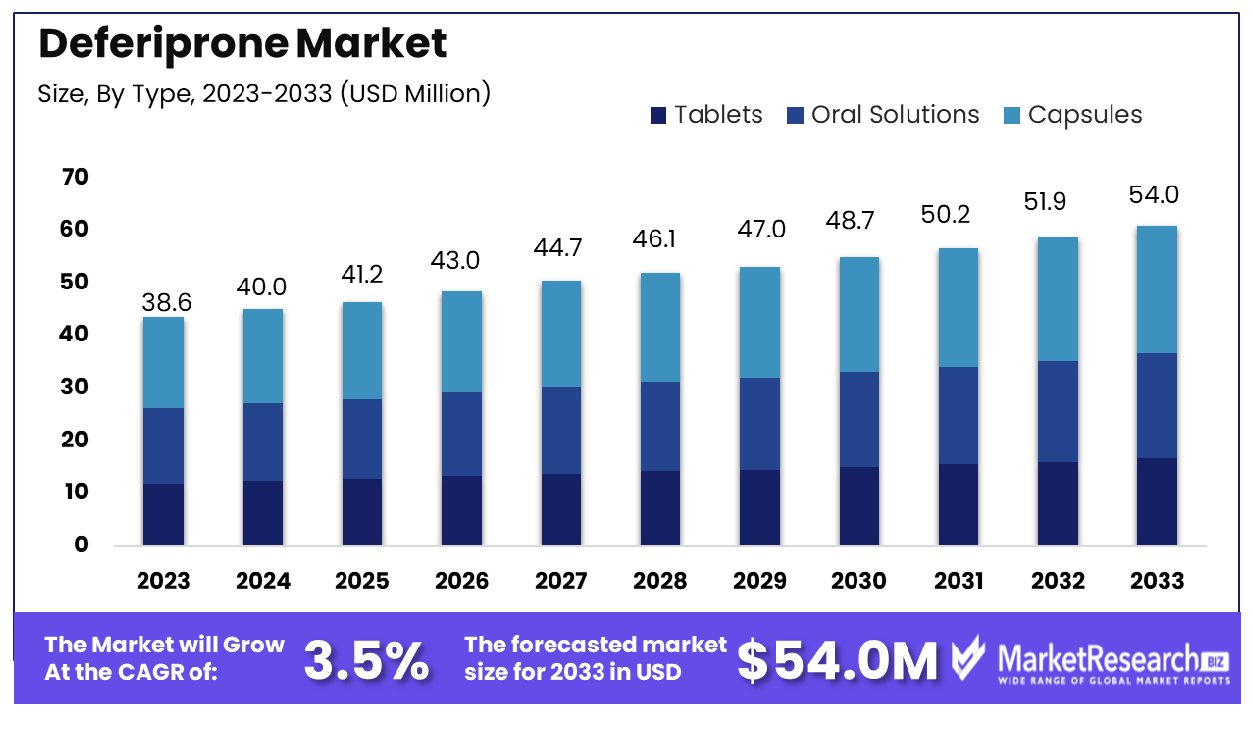

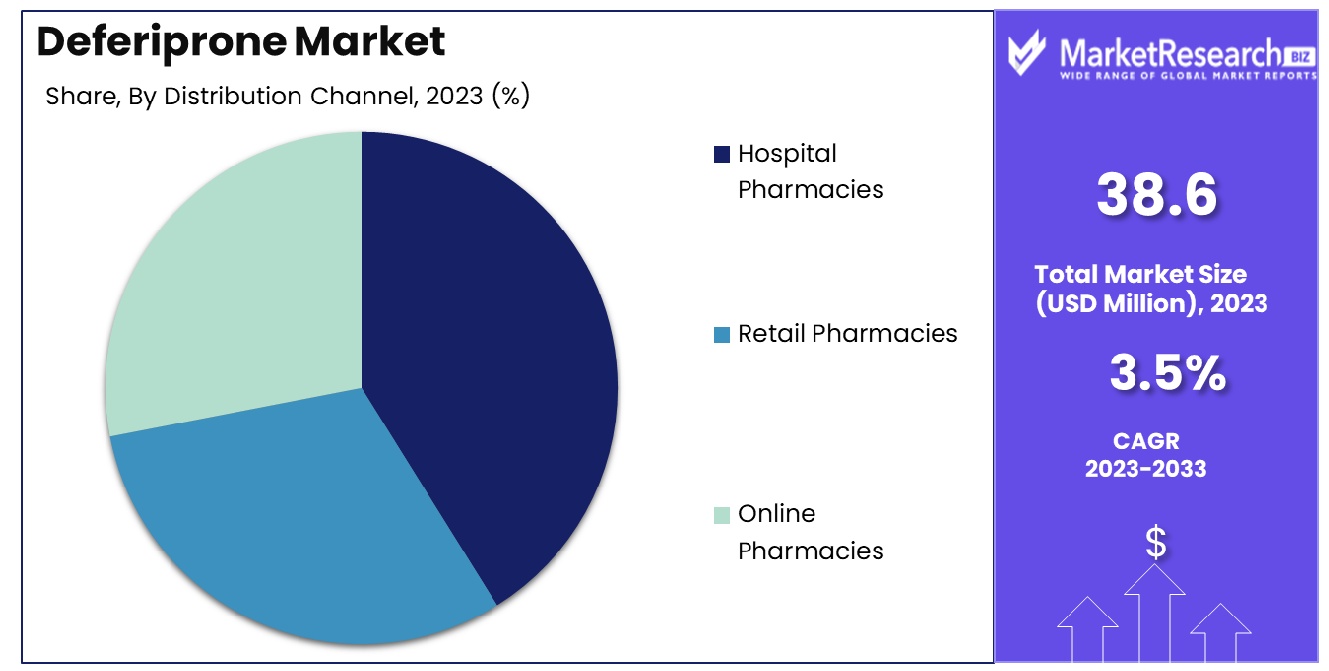

The Global Deferiprone Market was valued at USD 38.6 million in 2023. It is expected to reach USD 54.0 million by 2033, with a CAGR of 3.5% during the forecast period from 2024 to 2033.

The deferiprone market encompasses the production, distribution, and sale of deferiprone, a critical pharmaceutical agent used in chelation therapy for managing iron overload in patients. Particularly vital for individuals with thalassemia major, deferiprone binds to excess iron, facilitating its excretion and mitigating the risks associated with iron toxicity.

As market leaders and Product Managers—strategize, they must consider evolving regulatory landscapes, advancements in chelation therapy, and the increasing prevalence of blood disorders globally. The market's dynamics are influenced by research developments, patent expirations, and the integration of new treatment protocols, making strategic planning essential for sustaining growth and improving patient outcomes.

As a market research analyst specializing in pharmaceuticals, the deferiprone market presents a nuanced landscape of opportunity driven by medical necessity and scientific advancement. Deferiprone is a key therapeutic agent in the chelation treatment of diseases characterized by iron overload, such as thalassemia and sickle cell disease. Its importance is underscored by recent clinical trials and studies that highlight its efficacy and safety.

A 2022 multicenter randomized open-label noninferiority study involving 228 patients demonstrated that deferiprone is as effective as deferoxamine in reducing liver iron concentration (LIC) over 12 months. This finding is particularly significant as it supports deferiprone’s role in broader therapeutic protocols, offering a viable alternative with comparable outcomes in iron chelation therapy.

Moreover, a separate 2022 multicenter open-label phase 2 trial assessed the safety and acceptability of twice-daily administration of deferiprone in 30 patients. Results indicated that the regimen was well-tolerated, reinforcing deferiprone's potential for patient compliance and comfort.

A 2019 retrospective cohort study further explored deferiprone's impact by examining its effects on bone mass over one year in 256 transfusion-dependent thalassemia patients. The study provided insights into the long-term benefits of deferiprone-containing chelation regimens, contributing to a growing body of evidence supporting its use.

Key Takeaways

- Market Growth: The Global Deferiprone Market was valued at USD 38.6 million in 2023. It is expected to reach USD 54.0 million by 2033, with a CAGR of 3.5% during the forecast period from 2024 to 2033.

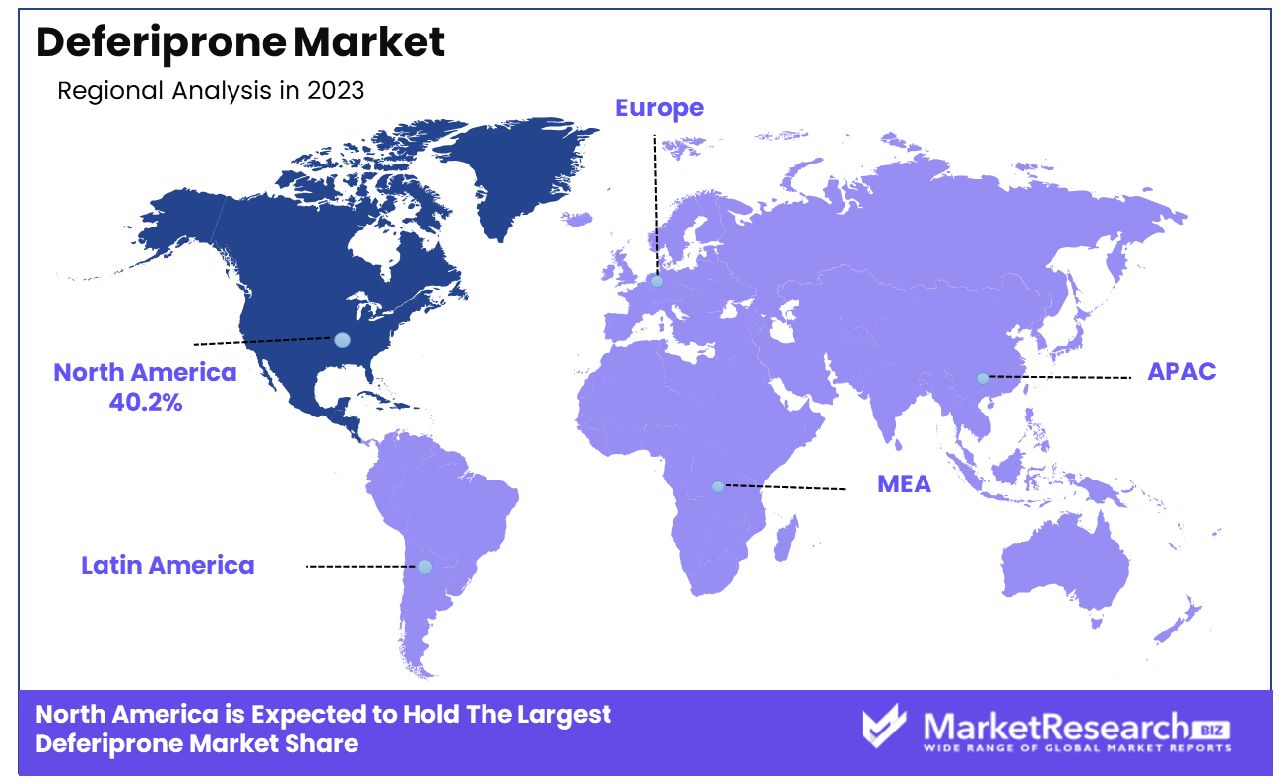

- Regional Dominance: The North American deferiprone market commands a significant 40.2% market share.

- By Type: Capsules dominate the deferiprone market with a 42% share.

- By Application: Transfusional iron overload leads applications, holding a 55% dominance.

- By Distribution Channel: Hospital pharmacies are the major distribution channel, controlling 60%.

Driving factors

Expanding Disease Prevalence Driving Demand

The growing global incidence of thalassemia and sickle cell disease significantly contributes to the expansion of the deferiprone market. These genetic disorders, characterized by chronic blood transfusions and subsequent iron overload, necessitate effective chelation therapy to prevent organ damage.

As the prevalence of these diseases increases, particularly in regions with genetic predispositions, the demand for deferiprone escalates. This heightened demand is anchored in the essential need to manage iron levels effectively, positioning deferiprone as a critical component of ongoing care regimens.

Enhanced Diagnosis and Awareness Amplifying Market Growth

Advancements in medical technology and heightened global health awareness are leading to improved diagnosis rates of iron overload conditions. This development is crucial for the deferiprone market as early and accurate diagnosis of iron overload allows for timely intervention with chelation therapy.

Increased awareness among healthcare providers and patients about the complications associated with untreated iron overload encourages the adoption of therapies like deferiprone. Consequently, this growing awareness acts as a catalyst, enhancing market growth by broadening the user base and increasing the frequency of deferiprone use in clinical settings.

Superiority in Safety and Efficacy Reinforcing Market Position

The deferiprone market is further bolstered by clinical evidence supporting its efficacy and safety over other iron chelators. Studies, such as the 2022 trials mentioned earlier, have demonstrated that deferiprone offers comparable, if not superior, efficacy in reducing liver iron concentration and is well-tolerated by patients.

These findings enhance the therapeutic credibility of deferiprone, making it a preferred choice among healthcare providers and patients. The drug's favorable safety profile, coupled with its effectiveness, not only retains existing users but also attracts new ones, driving market growth through increased trust and preference.

Restraining Factors

Impact of Adverse Side Effects on Market Growth

One significant restraint in the deferiprone market is the concern over adverse side effects associated with its long-term use. Deferiprone, while effective, has been linked to a range of potential side effects, including gastrointestinal disturbances and neutropenia, which can be severe and limit its usability in certain patient populations.

These side effects present a considerable challenge, as they may lead to discontinuation of therapy or reluctance among physicians to prescribe this chelator, particularly when patients have pre-existing conditions that could exacerbate these effects. The impact of these adverse reactions on the market is twofold: they not only restrict the adoption among new patients but also increase the rate of discontinuation among current users.

Competition from Alternative Chelation Therapies

The availability of alternative chelation therapies poses another significant barrier to the growth of the deferiprone market. Competing chelators like deferoxamine and deferasirox, which also have established efficacy profiles and are potentially associated with fewer or less severe side effects, offer substantial competition. These alternatives are often preferred in scenarios where deferiprone’s side effects are deemed too risky.

Moreover, ongoing research and development into newer, more efficacious, and safer chelation therapies continue to intensify this competition. As patients and healthcare providers have more options to choose from, the market share of deferiprone could be eroded, particularly if competitors offer a better balance of efficacy and tolerability.

By Type Analysis

Capsules lead the deferiprone market type segment, holding a dominant share of 42%.

In 2023, the Deferiprone Market was distinctly segmented into three primary forms: Tablets, Oral Solutions, and Capsules. Capsules held a dominant market position in the By Type segment, capturing more than a 42% share. This prominence is attributed to the ease of administration and the efficacy in dosage accuracy that capsules offer, making them a preferred choice among healthcare providers and patients.

Tablets accounted for a substantial portion of the market as well, marked by a robust consumption pattern due to their cost-effectiveness and widespread availability. Oral solutions, while less prevalent compared to capsules and tablets, were notably favored in pediatric and geriatric patient groups, where swallowing solid dosage forms is often challenging.

The market dominance of capsules can be largely ascribed to their enhanced bioavailability and the ability to provide a controlled release of Deferiprone, which is critical for maintaining optimal therapeutic iron levels in patients with conditions like thalassemia major. The formulation advancements in capsule technology, which improve patient compliance by minimizing gastrointestinal side effects associated with Deferiprone, also played a significant role in consolidating their market position.

Moving forward, the market is expected to witness continued growth in the capsules segment due to ongoing research and development aimed at further improving the delivery mechanisms of Deferiprone. However, the evolving patient demographics and the increasing preference for more patient-centric formulations could influence the growth dynamics across all segments. The strategic focus for stakeholders, therefore, remains on enhancing product formulations and expanding the accessibility of all dosage forms to meet diverse patient needs efficiently.

By Application Analysis

Transfusional iron overload applications dominate, accounting for 55% of the deferiprone market.

In 2023, the Deferiprone Market was segmented by application into Transfusional Iron Overload and NTDT Caused Iron Overload. Transfusional Iron Overload held a dominant market position, capturing more than a 55% share. This significant market share is primarily due to the high prevalence of blood transfusion therapies in conditions like thalassemia and sickle cell disease, which necessitate the use of iron chelators like Deferiprone to manage excess iron in the body.

Transfusional Iron Overload arises from the frequent blood transfusions required to treat various chronic hematological disorders, leading to an accumulation of iron in the body. Deferiprone serves as a critical therapeutic agent in managing this overload, thus driving its demand in this segment. The drug’s efficacy in removing excess iron from the heart and endocrine organs crucially supports its adoption and market dominance.

On the other hand, NTDT Caused Iron Overload, while occupying a smaller share of the market, is nonetheless significant. Non-transfusion-dependent thalassemia (NTDT) patients develop iron overload primarily through increased gastrointestinal absorption of iron, independent of transfusion. The treatment needs for this group are gradually being recognized, indicating potential growth in this segment.

The market's current dynamics suggest that while Transfusional Iron Overload will continue to dominate, increasing awareness and improved diagnostic practices for NTDT could shift some market dynamics toward more balanced segmental growth. Stakeholders are therefore advised to monitor advancements in treatment protocols and patient management strategies, which could influence future demand across both segments.

By Distribution Channel Analysis

Hospital pharmacies are the leading distribution channel, capturing 60% of the deferiprone market share.

In 2023, the Deferiprone Market was segmented by distribution channel into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Hospital Pharmacies held a dominant market position, capturing more than a 60% share. This dominance is largely attributed to the critical role hospital pharmacies play in the direct administration of therapies for conditions requiring Deferiprone, such as thalassemia and sickle cell disease, where patient monitoring and immediate access to medication are crucial.

Hospital Pharmacies are integral to the healthcare infrastructure, providing not only medication but also the necessary pharmacological guidance and support to patients undergoing treatment. Their proximity to treatment centers and integration within hospitals facilitate the immediate and effective management of iron overload conditions, driving their substantial share of the Deferiprone market.

Meanwhile, Retail Pharmacies held a significant share as well, serving as an accessible option for patients on long-term therapy who do not require immediate hospital care. The convenience and widespread availability of retail pharmacies enhance their role in the distribution of Deferiprone.

Online Pharmacies, though holding the smallest share, are emerging as a growing force in the market. They offer the advantages of convenience and often lower costs, appealing to a digitally savvy consumer base that values privacy and ease of access.

Looking ahead, the distribution landscape may evolve with advancements in digital health technologies and changes in consumer behavior, potentially increasing the market share of online pharmacies. Nonetheless, hospital pharmacies are expected to maintain their dominance due to the critical nature of the therapies involved and the essential services they provide in patient care regimes.

Key Market Segments

By Type

- Tablets

- Oral Solutions

- Capsules

By Application

- Transfusional Iron Overload

- NTDT Caused Iron Overload

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Growth Opportunity

Innovation through Combination Therapies

A pivotal growth opportunity for the deferiprone market in 2023 lies in the exploration of combination therapies. The integration of deferiprone with other chelators or complementary medications presents a significant potential to enhance treatment efficacy and patient outcomes. Research and development efforts are increasingly focused on these combination therapies to address the multifaceted nature of iron overload and its complications.

By improving the overall safety and effectiveness of chelation therapy, these innovative combinations could significantly increase deferiprone’s market appeal, encouraging broader use and acceptance among healthcare providers. This R&D push not only aims to mitigate the adverse effects associated with deferiprone but also to amplify its therapeutic benefits, making it a more compelling option in the treatment landscape.

Strategic Market Expansion

Another significant growth vector for deferiprone in 2023 is its expansion into untapped markets, particularly regions with high incidences of thalassemia and sickle cell disease. Countries in the Middle East, Africa, and certain areas of Asia present robust opportunities due to the genetic prevalence of these blood disorders.

Targeting these markets requires strategic initiatives, including local partnerships and tailored marketing strategies that address specific regional healthcare needs and regulatory landscapes. By focusing on these high-need areas, the deferiprone market can achieve substantial growth, not only by increasing the patient base but also by becoming an integral part of the standard care protocol in these regions, thus securing a long-term demand for the product.

Latest Trends

Novel Formulations Enhancing Patient Compliance

A significant trend shaping the global deferiprone market in 2023 is the development of novel drug formulations and dosing schedules aimed at improving patient compliance. Deferiprone's traditional dosing regimen can be burdensome, requiring multiple daily doses that may lead to poor adherence, especially in chronic conditions like thalassemia and sickle cell disease where long-term treatment is essential.

Pharmaceutical companies are investing in research to develop extended-release formulations and more convenient dosing schedules that reduce the frequency of administration. These advancements are not only expected to enhance patient quality of life but also improve therapeutic outcomes by ensuring consistent drug levels in the body. By addressing one of the key challenges in iron chelation therapy, these novel formulations are poised to drive increased adoption and patient retention, contributing to market growth.

Personalized Medicine Tailoring Chelation Therapy

Another emerging trend in the deferiprone market is the increased focus on personalized medicine, specifically tailored chelation therapies that consider individual patient needs and genetic profiles. This approach aims to optimize treatment efficacy and minimize side effects by adjusting dosages and treatment combinations based on genetic markers, severity of iron overload, and patient response to therapy.

Personalized medicine in chelation therapy represents a shift towards more targeted and effective management of iron overload conditions. As precision medicine continues to gain traction within the healthcare sector, deferiprone's integration into personalized treatment protocols could significantly enhance its market position by offering more customized and responsive care solutions, thereby meeting the evolving needs of patients and clinicians alike.

Regional Analysis

The North American deferiprone market commands a significant 40.2% share of the global market.

North America dominates the deferiprone market, holding a substantial 40.2% market share. This region's leadership in the market can be attributed to well-established healthcare infrastructure, high awareness about blood disorders, and significant investment in healthcare research and development. The prevalence of thalassemia and sickle cell disease, coupled with strong regulatory support for advanced therapeutic solutions, drives robust demand for deferiprone in North America.

Europe follows closely, with widespread adoption of deferiprone facilitated by comprehensive healthcare systems and active government initiatives promoting early diagnosis and treatment of iron overload conditions. The presence of several key pharmaceutical companies in Europe engaged in the development of iron chelators also supports the region’s strong market position.

The Asia Pacific region presents a high-growth segment in the deferiprone market due to the rising incidence of genetic blood disorders and improving healthcare infrastructure. Countries like India and China are witnessing an increase in the number of diagnosed cases, coupled with growing healthcare expenditure which together fuel the demand for effective treatments like deferiprone.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global deferiprone market is significantly influenced by the strategic movements and developments of key players, including Apotex Inc., Cipla Limited, VHB Life Sciences Limited, Taro Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Novartis International AG, Chiesi Farmaceutici S.p.A., and Zydus Cadila. Each of these companies plays a pivotal role in shaping the competitive landscape and driving innovation within the market.

Apotex Inc. and Cipla Limited are renowned for their robust generic drug portfolios, which include deferiprone, offering cost-effective solutions in markets with high price sensitivity. Their aggressive pricing strategies and established distribution networks enhance accessibility to chelation therapies, particularly in underserved regions.

VHB Life Sciences Limited and Taro Pharmaceutical Industries Ltd. focus on niche markets and have carved out a significant presence by specializing in the production of high-quality pharmaceutical formulations, including deferiprone. Their commitment to rigorous quality control and enhancement of formulation techniques positions them as reliable suppliers in the market.

Sun Pharmaceutical Industries Ltd. and Novartis International AG bring extensive R&D capabilities, investing in new formulations and combination therapies that could redefine treatment standards. Their global footprint and strong regulatory expertise allow them to navigate complex market dynamics effectively.

Chiesi Farmaceutici S.p.A. and Zydus Cadila emphasize innovation and patient-centric approaches, investing in new drug delivery systems that improve patient compliance and treatment outcomes. Their efforts in expanding into new geographic areas with tailored marketing strategies are crucial for tapping into emerging markets.

Market Key Players

- Apotex Inc.

- Cipla Limited

- VHB Life Sciences Limited

- Taro Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Novartis International AG

- Chiesi Farmaceutici S.p.A.

- Zydus Cadila

Recent Development

- In April 2024, Apotex announced its acquisition of Searchlight Pharma, a significant move that marks the company's entry into the branded pharmaceuticals sector, specifically within the Canadian market. This acquisition integrates over 60 products from Searchlight into Apotex's portfolio, enhancing its capabilities in branded pharmaceuticals across the Americas.

- In April 2023, Sun Pharma launched CEQUA in India, a novel treatment for Dry Eye Disease, expanding its portfolio in specialty segments. They also continue to focus on financial growth, reporting an increase in gross sales by 10.1% in the fourth quarter of fiscal year 2024.

Report Scope

Report Features Description Market Value (2023) USD 38.6 Million Forecast Revenue (2033) USD 54.0 Million CAGR (2024-2032) 3.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type(Tablets, Oral Solutions, Capsules), By Application(Transfusional Iron Overload, NTDT Caused Iron Overload), By Distribution Channel(Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Apotex Inc., Cipla Limited, VHB Life Sciences Limited, Taro Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Novartis International AG, Chiesi Farmaceutici S.p.A., Zydus Cadila Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

Our Clients

View Our Licence Options