Data Center Accelerator Market By Processor (GPU, CPU, FPGA, ASIC), By Type (Cloud Data Center, HPC Data Center), By Application (Deep Learning Training, Public Cloud Interface, Enterprise Interface), By Region And Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, And Forecast 2023-2032

-

6669

-

June 2023

-

400

-

-

This report was compiled by Vishwa Gaul Vishwa is an experienced market research and consulting professional with over 8 years of expertise in the ICT industry, contributing to over 700 reports across telecommunications, software, hardware, and digital solutions. Correspondence Team Lead- ICT Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

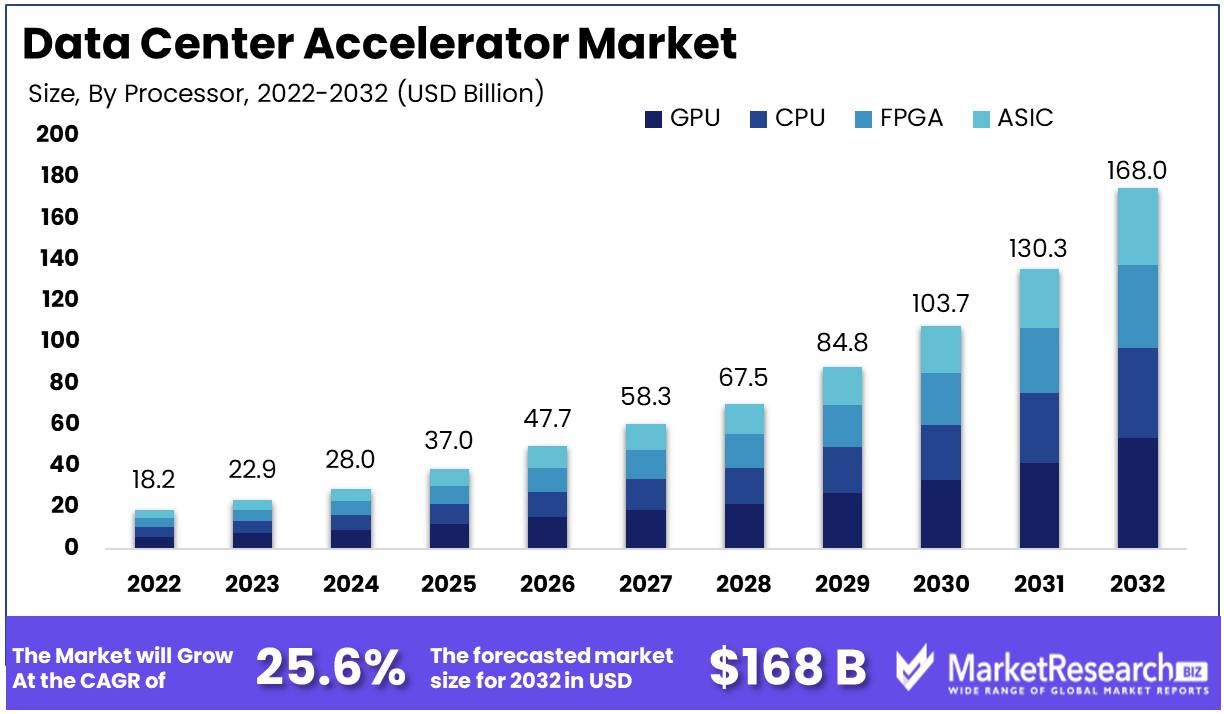

Data Center Accelerator Market size is expected to be worth around USD 168 Bn by 2032 from USD 18.2 Bn in 2022, growing at a CAGR of 25.6% during the forecast period from 2023 to 2032.

The Data Center Accelerator Market is currently experiencing a growth spurt and attracting attention with its innovative technology and diverse applications. Examining the Data Center Accelerator market's intricate definition and aspirational goals, as well as revealing its remarkable significance, advantages, notable innovations, substantial investments, expansive growth patterns, diverse applications, industries actively adopting this transformative technology, influential driving factors, ethical considerations that arise, and responsible considerations required to navigate this dynamic landscape.

The Data Center Accelerator Market is becoming an indispensable force propelling the global economy toward limitless opportunities as it continues its ascent. A data center accelerator exemplifies a paradigm-shifting computing system that propels the processing efficiency of data servers to unprecedented heights, effectively mitigating latency concerns and accelerating bandwidth to astronomical levels. This technology's increasing prevalence is a response to the growing demand for rapid data processing in a world where immediate access to information is paramount.

The market for data center accelerators is driven by the relentless pursuit of faster and more agile data processing capabilities, which in turn sets the groundwork for its surging popularity in cloud computing. It is the combination of hardware and software that powers the complex infrastructure of data center systems. The ultimate objective is to enhance the efficacy of data processing to facilitate real-time communication and astute data analysis, thereby paving the way for unimaginable possibilities in the future.

Considering the insatiable demand for enhanced data processing efficiency, the market for data center accelerators is unquestionably in an enviable position. By granting accelerated speeds, increased bandwidth capacities, and reduced latency issues, data centers assimilate and process data with unmatched efficiency. As a result, the ripple effects include faster response times, fewer instances of system outages, and a notable productivity increase. Moreover, the inherent optimization potential of data center accelerators transcends ordinary operational enhancements, enabling a substantial cost reduction through server performance optimization, reduced power consumption, and the elimination of excessive cooling expenses.

As a dynamic entity, the data center accelerator market continues to evolve in tandem with the ever-changing global market landscape. The ubiquitous integration of field-programmable gate arrays (FPGAs), which enable data centers to seamlessly adapt to the capricious ebbs and flows of fluctuating market demands, is a remarkable innovation in this field. In addition, the introduction of smart NICs as a key innovation propelling data center network security, speed, and load balancing capabilities to unprecedented heights is significant.

Driving Factors

High-Performance Computing Demands

High-performance computing is the application of advanced computing technologies to solve complex problems more quickly and effectively than conventional computing methods. In numerous fields, including scientific and engineering research, weather forecasting, and financial modeling, high-performance computation has become indispensable. The adoption of AI and ML also requires advanced computing capabilities to process vast amounts of data swiftly and accurately, which necessitates high-performance computing.

The demand for high-performance computation has spurred the expansion of the Data Center Accelerator Market, with GPU-powered servers and FPGAs leading the way. In managing complex workloads, GPU-powered servers have proved to be highly efficient and cost-effective, prompting widespread adoption by businesses. In contrast, FPGAs provide unparalleled flexibility and programmability, making them ideal for managing specialized workloads.

AI and ML Adoption

In recent years, enterprises have increasingly adopted Artificial Intelligence (AI) and Machine Learning (ML) to obtain insights from vast amounts of data. Effective AI and ML operation requires substantial computational resources, making high-performance computing a crucial aspect of their adoption.

The adoption of AI and ML has contributed to the expansion of the Data Center Accelerator Market, with GPU-powered servers and FPGAs leading the way. GPUs are ideal for training neural networks, one of the essential components of AI and ML, due to their ability to concurrently process massive amounts of data and provide high-performance computing. The adaptability and programmability of FPGAs make them ideal for executing specialized duties in the AI and ML domains.

Faster Data Processing

This trend is anticipated to persist into the foreseeable future. This data deluge is making it difficult for businesses to keep up, which is driving the demand for quicker data processing solutions.

The demand for quicker data processing solutions has propelled the expansion of the Data Center Accelerator Market. GPUs for high-performance computation and FPGAs for specialized workloads are being utilized to accelerate data processing.

The Accelerator Advancements

Accelerator technology advancements, such as GPUs, FPGAs, and ASICs, fuel the growth of the Data Center Accelerator Market. New architectures and technologies have been developed to enhance the performance and efficiency of GPUs over the past few years.

In addition, the hardware and software architecture of FPGAs continues to be augmented with new capabilities. FPGAs are suitable for specialized workloads such as cryptographic security and deep packet inspection because they can be reprogrammed on the fly.

Restraining Factors

Deployment Costs

The high cost of deployment is one of the most significant restraints on the market for data center accelerators. Costs associated with implementing data center accelerator solutions can be prohibitive, particularly for smaller businesses that may lack the financial resources to invest in this technology. In addition, the hardware requirements for deploying data center accelerator solutions can be quite complex and require specialized knowledge for proper installation.

Integration Challenges

Integration is an additional significant challenge for the data center accelerator market. The majority of organizations have existing infrastructure and are seeking methods to integrate data center accelerators with their existing systems. Due to the fact that data center accelerators require specialized hardware and software to function properly, integration can be a challenging process.

Competent Professionals

The shortage of qualified personnel capable of administering and deploying data center accelerators effectively is the third restraining factor. As the demand for this technology continues to increase, the skills and knowledge necessary to manage these systems will be in greater demand. However, there is a dearth of professionals with this specialized skill set at present.

Questions of Compatibility and Standardization

Compatibility and standardization issues pose a significant obstacle for the data center accelerator market. Many businesses are hesitant to implement data center accelerators out of concern that the technology will not be compatible with their existing infrastructure. In addition, there are unanswered concerns regarding the standardization of this technology, which increases the pressure on organizations to delay adoption until the industry reaches a consensus on common standards.

Processor Analysis

Over fifty percent of the data center accelerator market is controlled by the GPU segment. In the coming years, this market segment is anticipated to experience a constant increase in demand and a rapid growth rate. One of the primary factors driving the adoption of GPU-based data center accelerators is the development of emerging economies.

The GPU segment of the data center accelerator market is experiencing a significant transition in consumer trends and behavior. Increasing demand for high-performance computing (HPC) has led to an increase in demand for GPU-based computing platforms. With the increase in internet penetration, big data, and IoT, there is a significant demand for GPU-based data center accelerators that can manage complex computing tasks in real-time.

The growing trend of artificial intelligence and machine learning has substantially contributed to the expansion of the GPU segment of the data center accelerator market. AI and machine learning necessitate HPC capabilities, which can be provided by GPU-based data center accelerators. The demand for GPU-based data center accelerators is anticipated to increase as cloud computing and the demand for HPC applications grow in prevalence.

Type Analysis

Over 80% of the market share of the data center accelerator market is held by the cloud data center segment. This segment's development rate is anticipated to increase in the coming years due to factors such as the economic expansion of emerging economies. The adoption of cloud data centers can help organizations improve their infrastructure's adaptability and resiliency.

Emerging economies' economic growth is fueling demand for cloud data center accelerators. The increased adoption of cloud computing has increased the demand for high-performance computing capabilities to manage complex workloads. As cloud computing technology becomes more prevalent, it is anticipated that the cloud data center segment will experience a significant growth rate over the next few years.

The benefits of cloud data center accelerators, such as scalability, flexibility, and cost-effectiveness, are attracting an increasing number of consumers. Demand for cloud data center accelerators has increased as a result of organizations' efforts to optimize their operations by leveraging cloud computing technology. The trend toward cloud computing is anticipated to continue, resulting in a substantial growth rate for the cloud data center segment in the future years.

Application Analysis

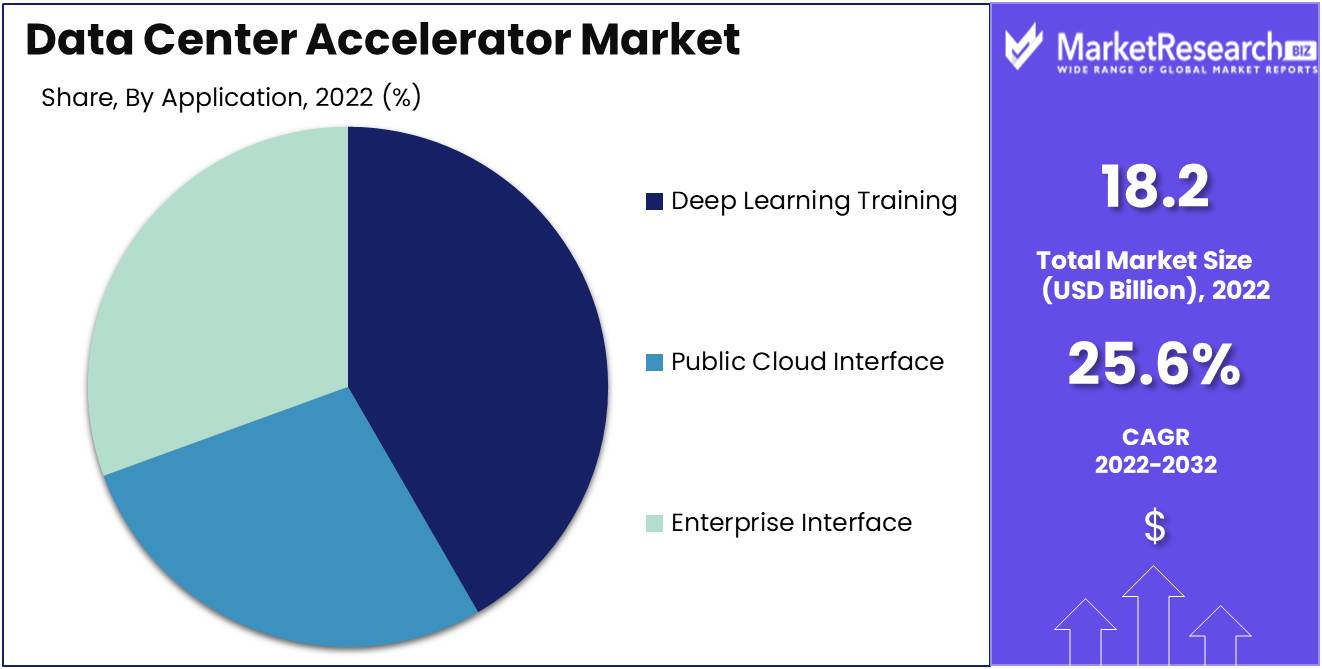

With a significant market share of more than 40%, the deep learning training segment dominates the data center accelerator market. This segment is anticipated to experience a rapid development rate in the coming years due to factors such as the economic expansion of emerging markets. The demand for HPC capabilities for AI and machine learning applications is propelling the adoption of data center accelerators for deep learning training.

Emerging economies' economic growth is one of the primary factors driving the adoption of deep learning training data center accelerators. Applications of AI and machine learning have the potential to revolutionize how organizations conduct business, resulting in enormous economic benefits. To capitalize on this opportunity, businesses are investing in deep learning training data center accelerators to facilitate the creation of AI and machine learning applications.

The increasing demand for AI and machine learning applications is driving consumer behavior and trends toward deep learning training data center accelerators. To develop these applications in real-time, organizations require HPC capabilities, resulting in a surge in demand for deep learning training data center accelerators. In the coming years, the deep learning training segment is anticipated to experience the highest growth rate, due to the increasing adoption of AI and machine learning applications.

Key Market Segments

By Processor

- GPU

- CPU

- FPGA

- ASIC

By Type

- Cloud Data Center

- HPC Data Center

By Application

- Deep Learning Training

- Public Cloud Interface

- Enterprise Interface

Growth Opportunity

Industry Expansion

Due to the expansion of various industries that rely on data centers, the data center accelerator market is anticipated to grow considerably in the upcoming years. Among these industries are healthcare, finance, and retail. In addition, the rise of the Internet of Things (IoT) and the rising volume of data generated by connected devices will fuel the expansion of this market. As a result, businesses are always looking for methods to increase data center efficiency and processing speeds, which is where data center accelerators come into play.

Cloud and Edge Integration

With the emergence of cloud computing and edge computing, the capacity of data centers is reaching its limit. Cloud computing has enabled businesses to offload their computing requirements to third-party providers, reducing the need for servers on-premises. Nonetheless, this has led to an increase in data traffic between data centers and cloud providers, posing new challenges for data center operators.

Edge computing, on the other hand, entails processing data closer to the source, thereby reducing the need to transport data between data centers. This strategy has led to the development of closer-to-user micro data centers and peripheral data centers. In these circumstances, data center accelerators are indispensable because they facilitate faster processing times and more efficient data transfer between cloud service providers and on-premises data centers.

Collaboration

The data center accelerator market is also expanding thanks to collaboration. Companies are collaborating to develop new solutions as data centers become more complex and require more advanced technologies. This collaboration is resulting in the development of industry- and use-specific data center accelerators that are more efficient and effective.

Energy Efficiency

Another significant factor propelling growth in the data center accelerator market is energy efficiency. Every year, the quantity of energy consumed by data centers increases, prompting businesses to search for ways to reduce energy consumption and save money. Accelerators in data centers are designed to be energy-efficient by consuming less electricity to increase processing speeds. In addition, these accelerators can be used to supplant multiple conventional CPUs, which further reduces energy consumption and costs.

Latest Trends

Growing Demand for High-Performance Computing (HPC)

Due to an increase in data-intensive workloads such as scientific simulations, weather forecasting, and genomics, the HPC market is expanding significantly. To meet these requirements, data centers must have parallel processing-optimized high-performance computing capabilities. Accelerators for high-performance computing, such as General-Purpose Graphics Processing Units (GPGPUs), have become popular due to their increased processing capacity and efficiency in high-performance computing tasks.

Integration of AI and ML Accelerators in Data Centers

The incorporation of AI and ML accelerators into data centers has paved the way for new applications in a variety of disciplines, including healthcare, finance, and autonomous vehicles. These accelerators allow organizations to perform real-time complex computations and predictive analytics. Natural Language Processing (NLP) frameworks and TensorFlow, for instance, have become industry standards for machine learning implementations, necessitating specialized hardware such as Tensor Processing Units (TPUs) and FPGA chips.

Adoption of FPGA and GPU Accelerators for Data Processing

Due to the increased demand for high-performance computation in data centers, the utilization of FPGA and GPU accelerators in data processing is growing. FPGA chips are gaining in popularity as a result of their adaptability and customizability, which enable organizations to develop their own custom chips for particular use cases. In contrast, GPU accelerators are favored for machine learning applications such as image processing and natural language recognition due to their high computational capacity and parallel processing capabilities.

Expansion of Data Center Accelerator Market in Cloud Computing

Because of its affordability and scalability, the data center accelerator market is expanding in cloud computing. Accelerators are being integrated into the infrastructures of cloud service providers such as Amazon Web Services (AWS) and Microsoft Azure in order to provide clients with faster performance and reduced latency. This has led to the development of novel cloud-native accelerators, such as Google's Tensor Processing Unit (TPU), which is optimized for cloud-based machine learning model execution.

Regional Analysis

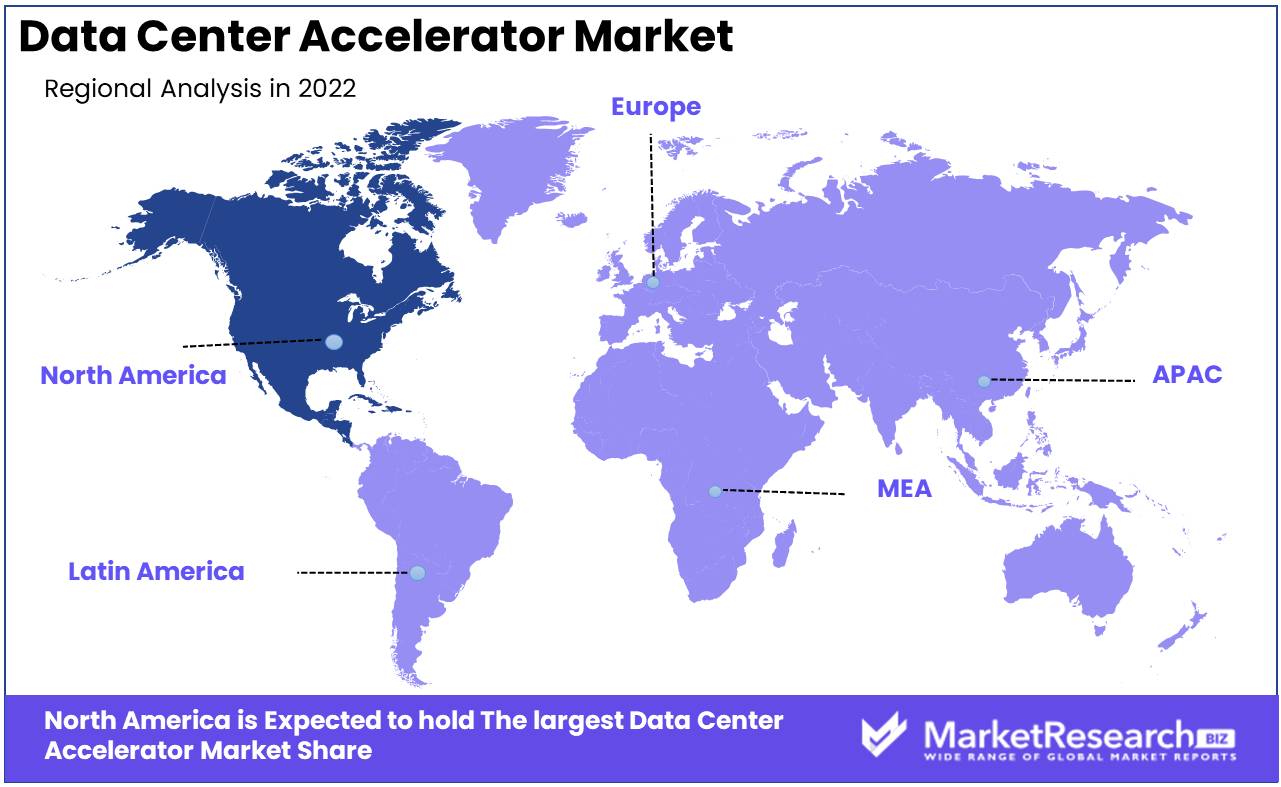

The Data Center Accelerator Market is firmly dominated by North America, which asserts its absolute dominance over this burgeoning industry.

In the domain of data center accelerators, North America is a veritable powerhouse, supported by an impressive foundation of advanced infrastructure and technological expertise. With a well-established network of data centers, high-speed connectivity, and cutting-edge facilities, the region paves the way for unmatched performance and scalability. This robust infrastructure functions as an innovation catalyst, fostering an environment conducive to ground-breaking data processing and acceleration of technology advancements.

In addition to its dominance, North America possesses an exceptional talent pool comprised of visionary entrepreneurs, experienced professionals, and research institutions at the forefront of technological progress. This convergence of expertise propels the region to the vanguard of the Data Center Accelerator Market by fueling a continuous flow of cutting-edge solutions.

Additionally, North America's strategic investments in research and development reinforce its preeminence. Government initiatives, private sector investments, and venture capital funding provide a substantial impetus for innovation and expansion in the data center accelerator market. These investments fuel the exploration of novel technologies, drive the development of advanced hardware and software solutions, and nurture collaborations between industry participants and academic institutions, thereby fostering an ecosystem that thrives on innovation and progress.

The size of North America's customer base is another crucial factor contributing to its preeminence. The region is home to numerous industries that significantly rely on data center infrastructure, such as technology, finance, healthcare, e-commerce, and entertainment. In these industries, the demand for rapid and efficient data processing is especially pronounced, driving the adoption of data center accelerators. The region's vast customer base provides fertile ground for market expansion, allowing North American businesses to capitalize on their domestic advantage and consolidate their dominance.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

Intel Corporation is a key participant in the Data Center Accelerator market. The company is a prominent provider of data center acceleration solutions, offering an extensive selection of products including Intel FPGA Programmable Acceleration Cards (PAC), Intel Optane SSDs, and Intel Ethernet Adapter. Intel's solutions offer a number of advantages, including speedier data processing, larger bandwidths, and increased power efficiency.

NVIDIA Corporation is another prominent player in the Data Center Accelerator market. The company's graphics processing units (GPUs) have become an increasingly popular option for data center acceleration. The GPUs developed by NVIDIA are intended to accelerate duties such as machine learning, data analytics, and high-performance computing. Additionally, the company provides a variety of software and hardware solutions that facilitate quicker and more efficient data processing.

In addition to AMD, Xilinx, Cisco Systems, Inc., and Hewlett Packard Enterprise, other key participants in the market for data center accelerators are Xilinx and Hewlett Packard Enterprise. These businesses provide a variety of products, including FPGA-based accelerators, specialized processors, and software-defined networking solutions.

Top Key Players in Data Center Accelerator Market

- Dell Technologies Inc.

- International Business Machines Corp.

- Intel Corporation

- Cisco Systems Inc.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Development LP

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- XILINX Inc.

- Achronix Semiconductor Corporation

Recent Development

- In 2022, Intel introduced Intel Optane DC Persistent Memory. This data center accelerator is designed specifically to increase the efficiency and dependability of data centers. With its innovative technology, Intel Optane DC Persistent Memory is a superior product that guarantees optimal performance.

- In 2023, NVIDIA announced the introduction of the NVIDIA Hopper GPU, which is anticipated to be the most powerful data center accelerator available. The futuristic design of the NVIDIA Hopper GPU is anticipated to provide superior performance and efficiency, thereby enhancing the user experience and streamlining data center management.

- In 2023, Qualcomm introduced its new data center accelerator, Qualcomm Cloud Engine. This incredibly affordable data center accelerator will provide enterprises and data centers with a cost-effective option. Qualcomm intends to revolutionize data center acceleration with these solutions, ensuring greater performance and dependability.

Report Scope

Report Features Description Market Value (2022) USD 18.2 Bn Forecast Revenue (2032) USD 168 Bn CAGR (2023-2032) 25.6% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Processor (GPU, CPU, FPGA, ASIC)

By Type (Cloud Data Center, HPC Data Center)

By Application (Deep Learning Training, Public Cloud Interface, Enterprise Interface)Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; the Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Dell Technologies Inc., International Business Machines Corp., Intel Corporation, Cisco Systems Inc., Lenovo Group Ltd., Hewlett Packard Enterprise Development LP, NVIDIA Corporation, Advanced Micro Devices Inc., XILINX Inc., Achronix Semiconductor Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Dell Technologies Inc.

- International Business Machines Corp.

- Intel Corporation

- Cisco Systems Inc.

- Lenovo Group Ltd.

- Hewlett Packard Enterprise Development LP

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- XILINX Inc.

- Achronix Semiconductor Corporation

Our Clients

View Our Licence Options