Global Dandruff Treatment Market By Treatment(Fluocinolone shampoos, Ketoconazole shampoos, Selenium sulfide shampoos, Shampoos containing salicylic acid, Tar-based shampoos, Pyrithione zinc shampoos), By Type(Fungal Dandruff, Dry Skin-Related Dandruff, Oily Scalp-Related Dandruff, Disease Related Dandruff), By Product(Non-Medicated, Medicated), By Drug Type(Branded, Generics), By Mode of Prescription(Over-the-counter (OTC), Prescription), By Distribution Channel(Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, Other Distribution Channel), By En

-

38229

-

August 2024

-

300

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

- Report Overview

- Key Takeaways

- Driving factors

- Restraining Factors

- By Treatment Analysis

- By Type Analysis

- By Product Analysis

- By Drug Type Analysis

- By Mode of Prescription Analysis

- By Distribution Channel Analysis

- By End-Users Analysis

- Key Market Segments

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

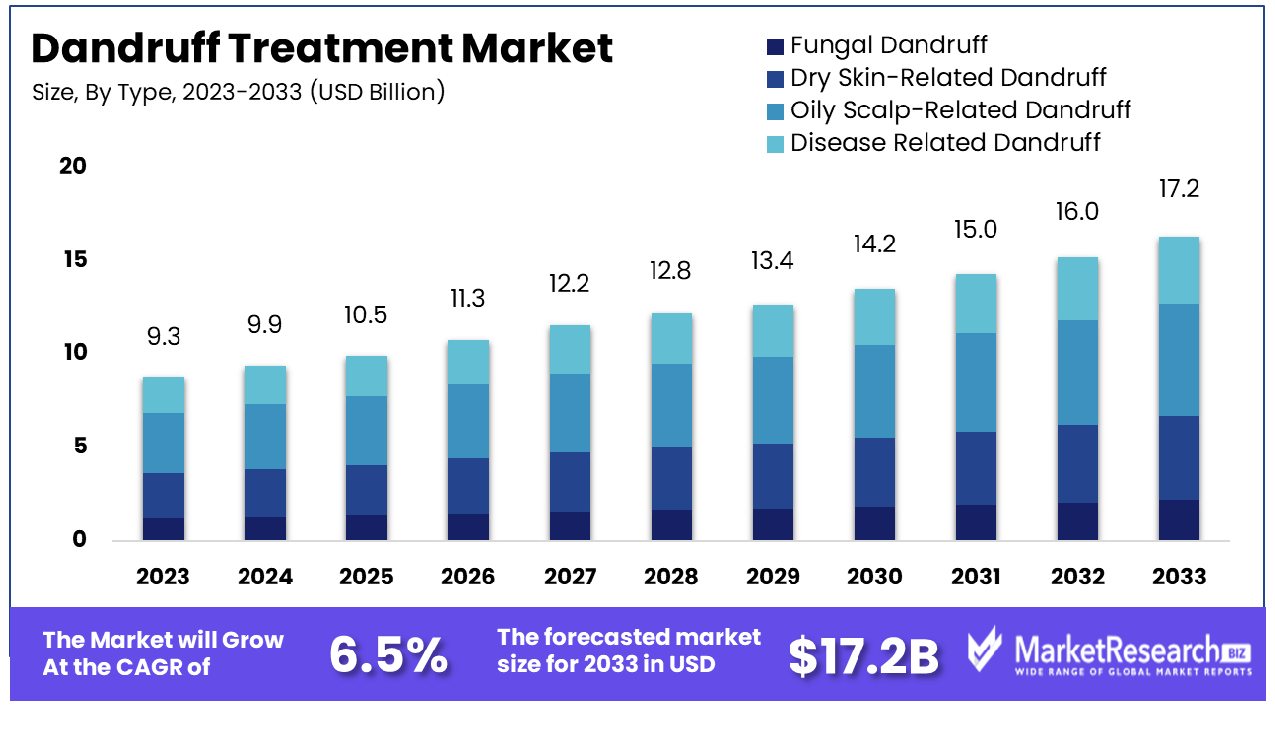

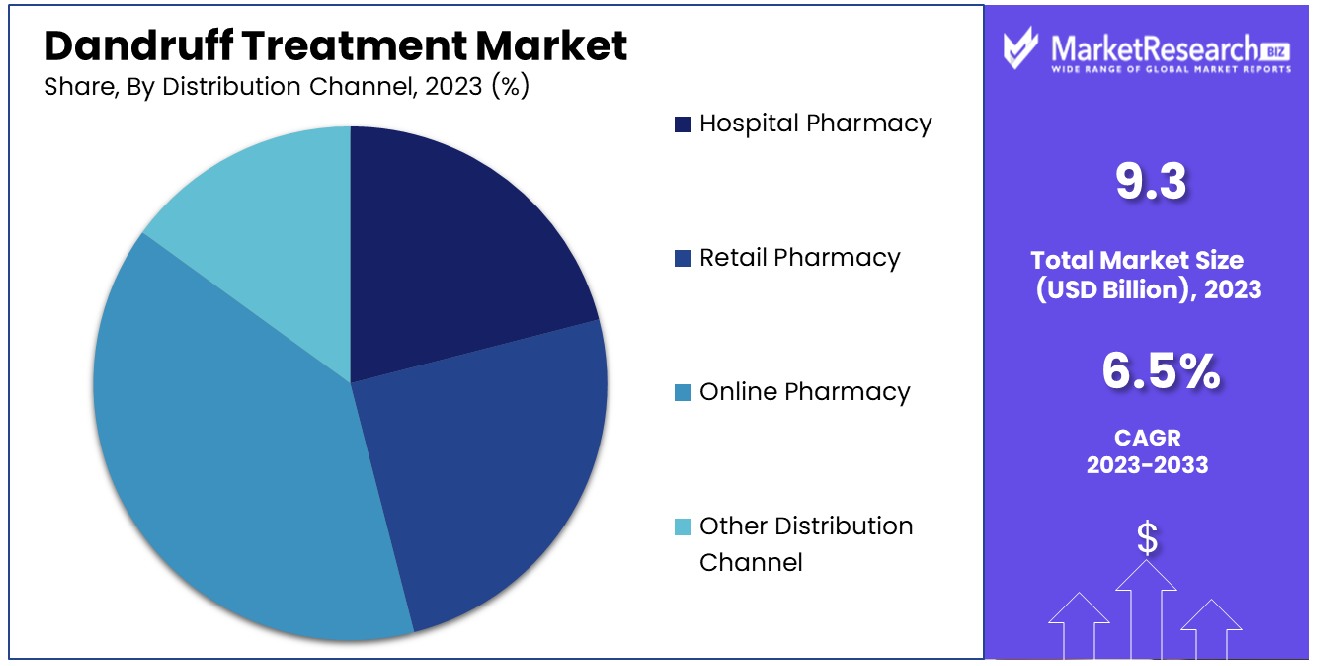

The Global Dandruff Treatment Market was valued at USD 9.3 billion in 2023. It is expected to reach USD 17.2 billion by 2033, with a CAGR of 6.5% during the forecast period from 2024 to 2033.

The Dandruff Treatment Market encompasses a range of products and services designed to combat dandruff, a common scalp condition marked by flaking and potential itchiness. This market includes medicated shampoos, conditioners, scalp treatments, and specialized clinics offering targeted therapies.

As consumer awareness and the pursuit of scalp health and aesthetic beauty grow, this market is expanding, driven by innovations in product formulations and marketing strategies. Key players are focusing on clinically proven ingredients and customized solutions to cater to diverse hair care needs and preferences, providing significant opportunities for growth and development in the personal care industry.

The Dandruff Treatment Market is poised for significant growth, fueled by increasing consumer awareness of scalp health and the efficacy of targeted treatments. Dandruff, a non-inflammatory condition characterized by an accelerated turnover of skin cells—approximately 800,000 cells per square centimeter during active dandruff phases, nearly double the 487,000 cells per square centimeter observed in normal scalp conditions—poses unique challenges in personal care. This increased cell turnover can exacerbate hair loss, with affected individuals shedding between 100-300 hairs daily, significantly more than the 50-100 hairs typically lost by those without dandruff.

As the market responds to these challenges, innovation in product development and marketing strategies becomes crucial. Companies are increasingly focusing on the formulation of products with clinically proven ingredients that not only reduce the visible symptoms of dandruff but also address underlying scalp health issues. This approach is complemented by personalized solutions tailored to diverse consumer needs and hair types, enhancing customer satisfaction and loyalty.

The potential for market expansion is substantial, driven by consumer demand for products that offer both aesthetic and therapeutic benefits. As brands continue to innovate and expand their product lines to include treatments that address both dandruff and associated conditions like hair loss, the market is expected to witness robust growth. Strategic marketing and consumer education are key as companies aim to differentiate themselves in a competitive landscape, emphasizing the clinical backing and holistic benefits of their offerings.

Key Takeaways

- Market Growth: The Global Dandruff Treatment Market was valued at USD 9.3 billion in 2023. It is expected to reach USD 17.2 billion by 2033, with a CAGR of 6.5% during the forecast period from 2024 to 2033.

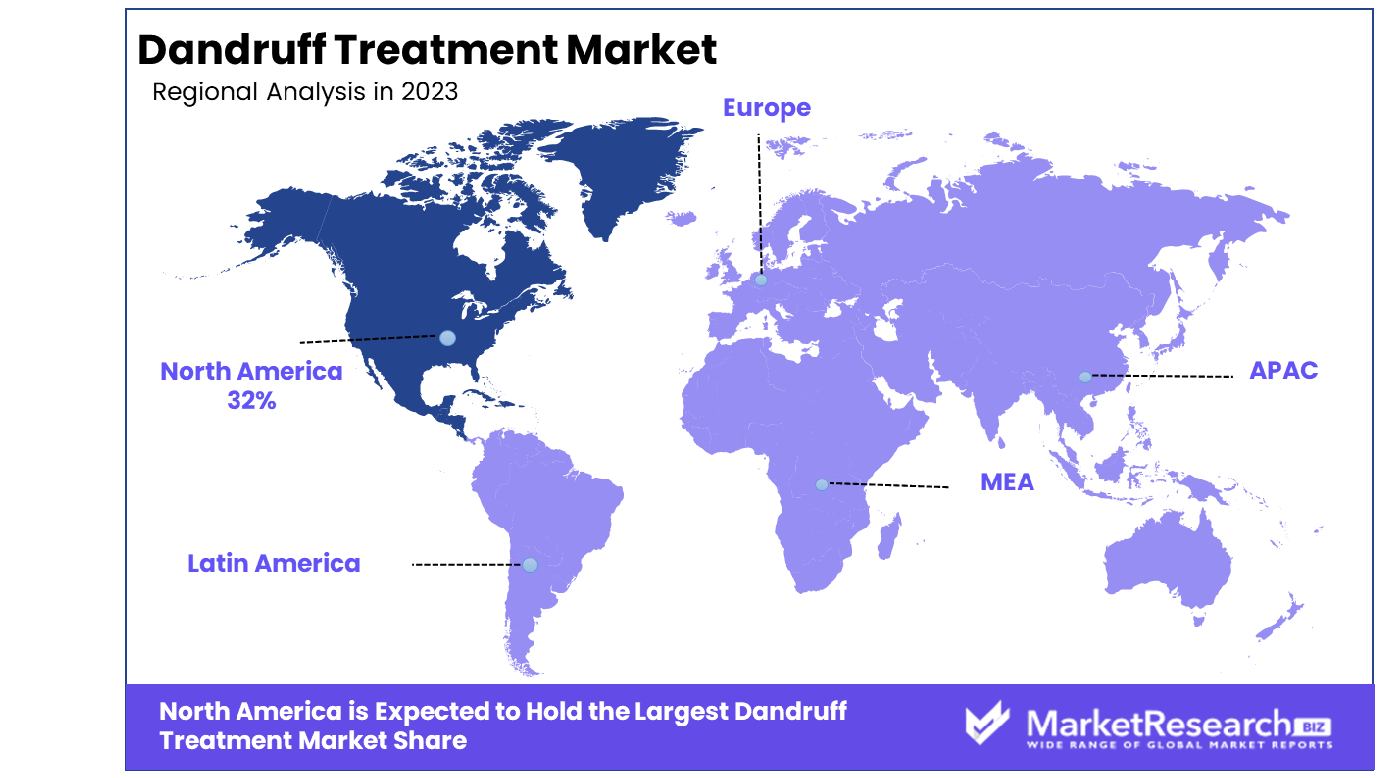

- Regional Dominance: The North American Dandruff Treatment Market commands a significant 32% share.

- By Treatment: Ketoconazole shampoos lead, holding 30% of the treatment market.

- By Type: Oily scalp-related dandruff dominates, accounting for 40% of cases.

- By Product: Medicated products are preferred, capturing a 65% market share.

- By Drug Type: Branded drug types lead with a 55% market dominance.

- By Mode of Prescription: Over-the-counter products are the most common, with a 70% prevalence.

- By Distribution Channel: Online pharmacies are popular, comprising 45% of distribution channels.

- By End-Users: Homecare is the primary end-user, dominating at 50%.

Driving factors

Escalating Incidence of Scalp Conditions and Enhanced Hygiene Consciousness

The dandruff treatment market is witnessing substantial growth, largely fueled by an increasing global prevalence of scalp-related conditions such as seborrheic dermatitis and psoriasis. This rise is coupled with heightened hygiene awareness among consumers.

A 2021 study revealed that approximately 50% of the global population will experience dandruff at some point in their lives, underscoring the urgent demand for effective treatment solutions. The growing consumer consciousness about personal hygiene and scalp health, especially post-pandemic, further amplifies the market expansion, as individuals are more vigilant about maintaining cleanliness and preventing scalp issues.

Expansion of Over-the-Counter Dandruff Treatment Solutions

The market is also benefiting from the growing availability and diversity of over-the-counter (OTC) dandruff treatments, which offer consumers convenient and immediate access to remedies. The variety of products, ranging from medicated shampoos to herbal options, caters to a broad spectrum of preferences and needs, encouraging trial and regular usage.

The ease of obtaining these treatments without a prescription has significantly propelled market growth, making it easier for consumers to address dandruff proactively.

Intensified Marketing and Consumer Education by Top Brands

Leading skincare and haircare brands are intensifying their marketing efforts and consumer education campaigns, which play a crucial role in driving the dandruff treatment market. Brands utilize aggressive marketing strategies and educational content to inform consumers about the causes of dandruff and the effectiveness of their solutions.

This strategy not only enhances brand visibility but also empowers consumers with knowledge, helping to reduce the stigma associated with dandruff and encouraging more open and frequent discussions about scalp care solutions.

Restraining Factors

Adverse Effects of Chemical-Based Dandruff Treatments

The growth of the dandruff treatment market is notably tempered by concerns over the side effects associated with chemical-based treatments. Many consumers experience adverse reactions such as scalp irritation, dryness, and hair loss, which can deter ongoing use of these products.

A survey indicated that up to 40% of users have experienced mild to severe side effects from traditional dandruff treatments, prompting them to seek alternative solutions. This significant proportion highlights a critical challenge for the market, as safety concerns can significantly impact consumer trust and product adoption.

Competition from Natural and Homemade Remedies

Further constraining the market growth is the increasing preference for natural and homemade dandruff solutions. With a growing global trend towards organic and chemical-free products, many consumers are turning to natural ingredients like tea tree oil, coconut oil, and apple cider vinegar, which are perceived as safer and gentler on the scalp.

The availability of these ingredients, coupled with a wealth of online DIY recipes, enables consumers to create effective treatments at home, posing a competitive threat to commercial dandruff products. This shift not only affects market dynamics but also forces manufacturers to innovate and potentially integrate more natural ingredients into their formulations to retain customer interest and market share.

By Treatment Analysis

Ketoconazole shampoos lead the treatment segment with a dominant market share of 30%.

In 2023, Ketoconazole shampoos held a dominant market position in the "By Treatment" segment of the Dandruff Treatment Market, capturing more than a 30% share. This segment encompasses a variety of treatments including Fluocinolone shampoos, Selenium sulfide shampoos, shampoos containing Salicylic acid, Tar-based shampoos, and Pyrithione zinc shampoos. Despite the wide array of available treatments, Ketoconazole shampoos have been particularly favored due to their effective antifungal properties, which not only alleviate symptoms but also reduce the recurrence of dandruff.

Ketoconazole's market leadership can be attributed to its broad acceptance among dermatologists and consumers for its efficacy and safety profile. It has been supported by clinical studies that underscore its capability to disrupt the cell membrane of the fungi, leading to fungal cell death and significant symptom relief. Consumer preference has been reinforced by the shampoo’s ability to integrate seamlessly into routine personal care without additional application inconvenience, which is a notable advantage over other treatment options.

Other treatments also maintain substantial market segments, though none as commanding as Ketoconazole. Pyrithione zinc shampoos follow closely, appreciated for their antibacterial and antifungal properties, while Tar-based shampoos are sought after by those preferring a strong approach for severe dandruff cases. Salicylic acid shampoos are favored for their ability to soften and remove scales, and Selenium sulfide shampoos are recognized for reducing scalp redness and irritation.

The diverse offerings within this market segment highlight the varied consumer needs and preferences, driving the continuous development and refinement of dandruff treatments. Each product caters to specific aspects of dandruff management, from mild to severe conditions, thereby sustaining a dynamic and competitive market landscape.

By Type Analysis

Oily scalp-related dandruff is the most prevalent type, accounting for 40% of cases.

In 2023, Oily Scalp-Related Dandruff held a dominant market position in the "By Type" segment of the Dandruff Treatment Market, capturing more than a 40% share. This segment includes Fungal Dandruff, Dry Skin-Related Dandruff, and Disease-Related Dandruff. The predominance of Oily Scalp-Related Dandruff is largely due to the common occurrence of seborrheic dermatitis among the global population, which often presents as oily, scaly flakes on the scalp.

The high incidence of Oily Scalp-Related Dandruff drives demand for specialized treatment products that not only control excess sebum but also address the flaking and itching associated with dandruff. This type of dandruff is particularly challenging to manage due to its association with an overproduction of oil and a yeast-like fungus that thrives in such environments. Effective treatments often involve the use of shampoos containing active ingredients like Ketoconazole, Salicylic acid, or Pyrithione zinc, which help regulate sebum production and inhibit fungal growth.

The market's response to the needs of consumers with Oily Scalp-Related Dandruff includes a range of formulations that offer varying strengths and combinations of active ingredients to suit different severity levels and scalp sensitivities. This has fostered a competitive landscape where innovation and efficacy are paramount to capturing consumer loyalty.

Other types of dandruff, such as Dry Skin-Related Dandruff and Disease-Related Dandruff, also hold significant shares of the market. These variations require different formulations, targeting moisture replenishment and addressing underlying skin conditions, respectively. This segmentation allows brands to cater specifically to the diverse needs of the consumer base, enhancing personalized treatment approaches in the dandruff treatment market.

By Product Analysis

Medicated products hold a commanding 65% majority in the dandruff treatment product category.

In 2023, Medicated products held a dominant market position in the "By Product" segment of the Dandruff Treatment Market, capturing more than a 65% share. This category is distinctly classified into Medicated and Non-Medicated products. The substantial lead in medicated products underscores the consumer preference for treatments that offer not only symptomatic relief but also target the underlying causes of dandruff such as fungal infections and excessive sebum production.

Medicated shampoos and conditioners, containing active ingredients like Ketoconazole, Pyrithione Zinc, Selenium Sulfide, and Salicylic Acid, have proven effective in managing the symptoms of dandruff. These ingredients are renowned for their antifungal, antibacterial, and keratolytic properties, making them indispensable in the formulation of dandruff treatments. The efficacy of these medicated products in reducing itchiness, flakiness, and irritation contributes to their prominent market share.

The preference for medicated solutions is further reinforced by endorsements from dermatologists and healthcare professionals, who often recommend these products for both acute and chronic dandruff issues. This professional backing, combined with aggressive marketing and consumer education, has helped maintain the visibility and credibility of medicated products in the market.

In contrast, non-medicated products, which typically focus on hydrating and nourishing the scalp to reduce dryness and flaking, hold a smaller market share. While they are beneficial for mild dandruff and regular scalp maintenance, they generally do not address the biological factors contributing to severe dandruff, which limits their appeal to consumers seeking targeted dandruff solutions. Thus, the medicated segment continues to lead the market, driven by strong consumer trust and documented therapeutic outcomes.

By Drug Type Analysis

Branded drugs lead the drug type category, representing 55% of the market.

In 2023, Branded products held a dominant market position in the "By Drug Type" segment of the Dandruff Treatment Market, capturing more than a 55% share. This segment is categorized into Branded and Generic products. The strong preference for branded treatments can be attributed to consumer trust in established brand names, which are often associated with higher quality, efficacy, and safety in the treatment of dandruff.

Branded dandruff treatments benefit from extensive research and development efforts that lead to innovative formulations. These products frequently contain patented active ingredients or unique combinations that are not available in generic versions. Additionally, branded products are supported by significant marketing budgets, which help in building brand awareness and loyalty. Such efforts are crucial in a market where consumer confidence plays a vital role in the purchasing decision.

The efficacy of branded products, often validated by clinical trials and endorsed by healthcare professionals, reinforces their market dominance. Consumers tend to rely on branded products for consistent results, particularly for managing severe or persistent dandruff conditions. This trust is further bolstered by user testimonials and professional recommendations, which are prominently featured in advertising and on product packaging.

On the other hand, generic products, while offering a cost-effective alternative with similar active ingredients, typically do not engage in extensive marketing or brand-building activities. Although they are gradually gaining acceptance due to their lower price points, the lack of brand identity and perceived inferiority in quality compared to their branded counterparts limit their market share. As such, branded products continue to lead the market, drawing on their strengths in innovation, consumer trust, and brand equity.

By Mode of Prescription Analysis

Over-the-counter (OTC) products overwhelmingly dominate, capturing 70% of the prescription mode market.

In 2023, Over-the-counter (OTC) products held a dominant market position in the "By Mode of Prescription" segment of the Dandruff Treatment Market, capturing more than a 70% share. This segment is clearly divided between Over-the-counter (OTC) and Prescription-based products. The overwhelming preference for OTC products highlights consumer tendencies toward self-diagnosis and treatment of mild to moderate dandruff, underscoring the convenience and accessibility of OTC solutions.

OTC dandruff treatments, including a wide array of shampoos, conditioners, and topical creams, offer consumers the ease of obtaining effective remedies without the need for a doctor's prescription. The strength of OTC products in the market is largely due to their widespread availability in pharmacies, supermarkets, and online platforms, coupled with their proven effectiveness for common dandruff issues. Many OTC products are formulated with active ingredients like Pyrithione Zinc, Salicylic Acid, and Selenium Sulfide, which are recognized for their ability to control flaking and itching.

Marketing strategies play a significant role in the dominance of OTC products. These strategies often involve direct advertising to consumers, emphasizing the ease of access and immediate relief from symptoms. Furthermore, the backing of trusted brands in the OTC space enhances consumer confidence in these products, often supported by user testimonials and clear labeling of benefits.

In contrast, Prescription products, which are typically reserved for more severe or treatment-resistant cases of dandruff, require a healthcare provider's approval and are often perceived as a last resort. While these products may offer specialized formulations for stubborn dandruff, their market share is limited by the necessity of medical consultation, making OTC products the more accessible and preferred choice for the majority of consumers.

By Distribution Channel Analysis

Online pharmacies are a leading distribution channel, holding a 45% market share.

In 2023, Online Pharmacy held a dominant market position in the "By Distribution Channel" segment of the Dandruff Treatment Market, capturing more than a 45% share. This segment includes Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Other Distribution Channels. The ascendancy of Online Pharmacy underscores the growing consumer preference for the convenience and discretion provided by digital shopping platforms.

The Online Pharmacy sector has seen substantial growth due to several key factors. First, the increasing penetration of the internet and the proliferation of e-commerce platforms have made it easier for consumers to access a wide range of dandruff treatment products from the comfort of their homes. Secondly, online pharmacies often offer competitive pricing, detailed product information, customer reviews, and easy comparison of different brands and formulations, enhancing the shopping experience and informed decision-making.

Additionally, the privacy offered by online transactions is particularly appealing for consumers seeking treatments for conditions like dandruff, which some may find embarrassing to purchase in person. Online platforms also facilitate frequent promotions, discounts, and loyalty programs, further attracting consumers.

While Online Pharmacy channels lead in market share, Hospital, and Retail Pharmacies continue to play critical roles, particularly for consumers preferring face-to-face interaction with pharmacists for immediate advice and product recommendations. Other Distribution Channels, including direct sales from dermatology clinics and specialized stores, also contribute to the market, catering to niche markets or providing specialized products not widely available in mainstream outlets.

By End-Users Analysis

Homecare remains the primary end-user in the market, constituting 50% of usage.

In 2023, Homecare held a dominant market position in the "By End-Users" segment of the Dandruff Treatment Market, capturing more than a 50% share. This segment includes Hospitals, Specialty Clinics, Homecare, and Other End-Users. The prominent position of home care highlights a significant trend towards self-managed treatments, which are increasingly favored by consumers seeking convenience and privacy in managing dandruff.

The preference for Homecare solutions is primarily driven by the availability of a wide array of over-the-counter (OTC) products that can be used comfortably and discreetly at home. These products include medicated shampoos, conditioners, and topical creams designed to treat mild to moderate dandruff without the need for professional supervision. The effectiveness of these products, coupled with their ease of use, supports the significant market share held by this end-user category.

Further bolstering the Homecare segment's dominance are advances in product formulations that offer improved efficacy with fewer side effects, making them suitable for long-term use. Additionally, the rise of digital platforms has made it easier for consumers to access detailed product information, reviews, and at-home treatment tips, enhancing their ability to make informed choices about dandruff management.

While Homecare packaging leads in market share, Hospitals, and Specialty Clinics also play essential roles, particularly for severe cases requiring specialized treatments prescribed by dermatologists. Other End-Users, including beauty salons and wellness centers, provide supplementary channels that cater to niche markets seeking professional scalp treatments alongside other beauty and wellness services.

Key Market Segments

By Treatment

- Fluocinolone shampoos

- Ketoconazole shampoos

- Selenium sulfide shampoos

- Shampoos containing salicylic acid

- Tar-based shampoos

- Pyrithione zinc shampoos

By Type

- Fungal Dandruff

- Dry Skin-Related Dandruff

- Oily Scalp-Related Dandruff

- Disease Related Dandruff

By Product

- Non-Medicated

- Medicated

By Drug Type

- Branded

- Generics

By Mode of Prescription

- Over-the-counter (OTC)

- Prescription

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- Other Distribution Channel

By End-Users

- Hospitals

- Specialty Clinics

- Homecare

- Other End-Users

Growth Opportunity

Capitalizing on Natural and Organic Product Trends

In 2023, the dandruff treatment market is poised to capitalize significantly from the burgeoning demand for natural and organic products. As consumers increasingly lean towards health-conscious, eco-friendly lifestyles, the appeal for chemical-free solutions in dandruff treatment is rapidly growing. This shift provides a substantial opportunity for brands to develop products that combine efficacy with natural ingredients, which are perceived as safer and more sustainable.

Such products not only cater to current consumer preferences but also align with global trends toward environmental sustainability and wellness-focused personal care. By investing in research and development to harness botanical extracts and organic compounds, companies can differentiate their offerings, enhance brand loyalty, and command premium pricing.

Expanding Market Reach through Enhanced Distribution Channels

Another significant opportunity in 2023 lies in the expansion of distribution channels, particularly in emerging markets where access to specialized personal care products is evolving. As infrastructure improves and e-commerce platforms proliferate, companies have a pivotal chance to penetrate these markets, which are experiencing increased consumer spending on personal care.

Leveraging online platforms alongside traditional retail can broaden consumer access to dandruff treatments, especially in areas previously underserved. This dual-channel strategy not only increases market visibility but also caters to a wider demographic, driving growth in global market reach and ultimately, revenue generation.

Latest Trends

Shift Toward Sulfate-Free and Paraben-Free Formulations

In 2023, a defining trend in the global dandruff treatment market is the escalating consumer preference for sulfate-free and paraben-free hair care products. This trend is driven by a broader consumer awareness of the potential health risks associated with these chemicals, including irritation and long-term scalp damage. As a result, consumers are increasingly seeking products with natural ingredients that promise safety without compromising efficacy.

This shift presents a strategic opportunity for market players to reformulate existing products and launch new lines that align with these health-conscious preferences. Brands that can successfully market these cleaner alternatives stand to gain a competitive edge, particularly among millennials and Gen Z consumers who prioritize ingredient transparency in their purchasing decisions.

Personalization Through Digital Platforms

Another prominent trend is the growth in the utilization of online platforms and mobile apps for personalized scalp and hair care solutions. With advances in technology, companies are now offering customized product recommendations based on individual scalp conditions and preferences, facilitated through sophisticated algorithms and AI-driven diagnostics tools.

This personalization enhances customer experience and satisfaction, leading to higher retention rates and increased sales. Moreover, the digital approach allows brands to collect valuable consumer data, enabling continuous improvement of their offerings. Companies that innovate in integrating these technologies into their customer interaction strategies are likely to see robust growth in both engagement and market share in 2023 and beyond.

Regional Analysis

The North American Dandruff Treatment Market commands a dominant 32% share of the global industry.

In North America, which dominates the market with a 32% share, the trend towards natural and organic products drives growth. This region benefits from a robust healthcare infrastructure and high consumer awareness, leading to a preference for advanced treatment solutions, including those integrating biotechnology. North America's market is bolstered by strong distribution networks and high spending power, facilitating widespread access to a variety of treatment options.

Europe follows closely, characterized by stringent regulations that promote the development of safer, more effective dandruff treatments. The market here is driven by a growing preference for sulfate-free and paraben-free products, mirroring global trends towards healthier lifestyle choices. Europe's rich history in cosmetic and pharmaceutical innovation supports a sophisticated market landscape where preventive hair care solutions are increasingly popular.

Asia Pacific is the fastest-growing region, driven by increasing disposable incomes and expanding awareness of scalp health. The rise in urbanization and changes in consumer lifestyles have led to higher demand for personal care products, including dandruff treatments. Local brands are thriving by leveraging natural ingredients traditionally known in regional cultures, which appeal to both local and global consumers.

The Middle East & Africa and Latin America are emerging markets with growing potential. These regions show increasing consumer awareness and gradual shifts towards premium, specialized hair care solutions, though market penetration is lower compared to more developed regions. The expansion of retail and online distribution channels in these areas presents significant growth opportunities for the dandruff treatment market.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Key Players Analysis

In 2023, the global Dandruff Treatment Market is highly competitive, with key players deploying various strategies to capture and expand market share. Notably, companies like AstraZeneca and Procter & Gamble are leading with innovation and extensive marketing campaigns that emphasize the efficacy and safety of their products. AstraZeneca, traditionally strong in pharmaceuticals, leverages its scientific expertise to develop advanced treatment formulations, while Procter & Gamble uses its broad consumer goods presence to ensure widespread distribution and brand trust.

Johnson & Johnson and L’Oreal are exploiting their established global distribution networks and brand loyalty to promote specialized dandruff treatment products. Their strategies focus on integrating dermatologically tested and consumer-friendly ingredients, catering to the growing demand for gentle yet effective solutions.

Emerging markets also present robust activity, with companies like Glenmark Pharmaceuticals and Cipla Inc. These firms are expanding their product lines to include affordable dandruff solutions tailored to local consumer needs and economic conditions, particularly in India where the market shows rapid growth potential.

Additionally, niche brands like Vyome Therapeutics and JOHN PAUL MITCHELL SYSTEMS are carving out unique positions by focusing on innovative and natural formulations, attracting a segment of consumers increasingly wary of chemical ingredients.

The market also sees a strong presence from companies like Kao Corporation and Henkel AG & Co. KGaA, which continuously innovate in both product development and marketing strategies to maintain their competitive edge in both Western and Asian markets.

Market Key Players

- AstraZeneca (U.K.)

- Procter & Gamble

- Johnson & Johnson Private Limited (U.S.)

- Glenmark Pharmaceuticals Limited (India)

- Cipla Inc. (U.S.)

- L'Oreal (France)

- Procter & Gamble (U.S.)

- Unilever (U.K.)

- Alliance Pharma PLC (U.K.)

- Arcadia Consumer Healthcare (U.S.)

- Vyome Therapeutics Inc. (India)

- ACTION LIFE SCIENCES (India)

- JOHN PAUL MITCHELL SYSTEMS (U.S.)

- JASÖN Natural Products, Inc. (U.S.)

- Nikole Kozemetics (India)

- DABUR (India)

- Kao Corporation (Japan)

- Philip Kingsley Products Ltd. (U.K.)

- Henkel AG & Co. KGaA (Germany)

- Arion Healthcare (India)

- Other Key Players

Recent Development

- In April 2023, Cipla Inc. successfully raised $50 million in funding in April 2023 to develop a series of dermatological products, including a novel treatment for dandruff. This funding will support the research and development of products that are more effective and have fewer side effects than existing treatments.

- In February 2023, AstraZeneca launched a new scalp treatment cream that reduces dandruff and soothes scalp irritation. This product introduction is part of a larger strategy to diversify their dermatological offerings, aiming to capture a 20% increase in their skincare market share.

- In June 2022, Procter & Gamble, introduced a new line of anti-dandruff shampoos under its existing brand, featuring advanced formulations that target the root cause of dandruff. This launch is expected to bolster their sales by 15%, focusing on a blend of efficacy and consumer trust in their products.

Report Scope

Report Features Description Market Value (2023) USD 9.3 Billion Forecast Revenue (2033) USD 17.2 Billion CAGR (2024-2032) 6.5% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Treatment(Fluocinolone shampoos, Ketoconazole shampoos, Selenium sulfide shampoos, Shampoos containing salicylic acid, Tar-based shampoos, Pyrithione zinc shampoos), By Type(Fungal Dandruff, Dry Skin-Related Dandruff, Oily Scalp-Related Dandruff, Disease Related Dandruff), By Product(Non-Medicated, Medicated), By Drug Type(Branded, Generics), By Mode of Prescription(Over-the-counter (OTC), Prescription), By Distribution Channel(Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, Other Distribution Channel), By End-Users(Hospitals, Specialty Clinics, Homecare, Other End-Users) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape AstraZeneca (U.K.), Procter & Gamble, Johnson & Johnson Private Limited (U.S.), Glenmark Pharmaceuticals Limited (India), Cipla Inc. (U.S.), L'Oreal (France), Procter & Gamble (U.S.), Unilever (U.K.), Alliance Pharma PLC (U.K.), Arcadia Consumer Healthcare (U.S.), Vyome Therapeutics Inc. (India), ACTION LIFE SCIENCES (India), JOHN PAUL MITCHELL SYSTEMS (U.S.), JASÖN Natural Products, Inc. (U.S.), Nikole Kozemetics (India), DABUR (India), Kao Corporation (Japan), Philip Kingsley Products Ltd. (U.K.), Henkel AG & Co. KGaA (Germany), Arion Healthcare (India), Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- AstraZeneca (U.K.)

- Procter & Gamble

- Johnson & Johnson Private Limited (U.S.)

- Glenmark Pharmaceuticals Limited (India)

- Cipla Inc. (U.S.)

- L'Oreal (France)

- Procter & Gamble (U.S.)

- Unilever (U.K.)

- Alliance Pharma PLC (U.K.)

- Arcadia Consumer Healthcare (U.S.)

- Vyome Therapeutics Inc. (India)

- ACTION LIFE SCIENCES (India)

- JOHN PAUL MITCHELL SYSTEMS (U.S.)

- JASÖN Natural Products, Inc. (U.S.)

- Nikole Kozemetics (India)

- DABUR (India)

- Kao Corporation (Japan)

- Philip Kingsley Products Ltd. (U.K.)

- Henkel AG & Co. KGaA (Germany)

- Arion Healthcare (India)

- Other Key Players

Our Clients

View Our Licence Options