Core Plate Varnishes Market By End Users,(Motor, Generator, Transformer, Electromagnetic Poles, Others), By Classification (Pigmented, Un-Pigmented, Other), By Chemical (Alkyd Phenolic, Polyurethane, Polyester, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

-

21136

-

May 2024

-

300

-

-

This report was compiled by Shreyas Rokade Shreyas Rokade is a seasoned Research Analyst with CMFE, bringing extensive expertise in market research and consulting, with a strong background in Chemical Engineering. Correspondence Team Lead-CMFE Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

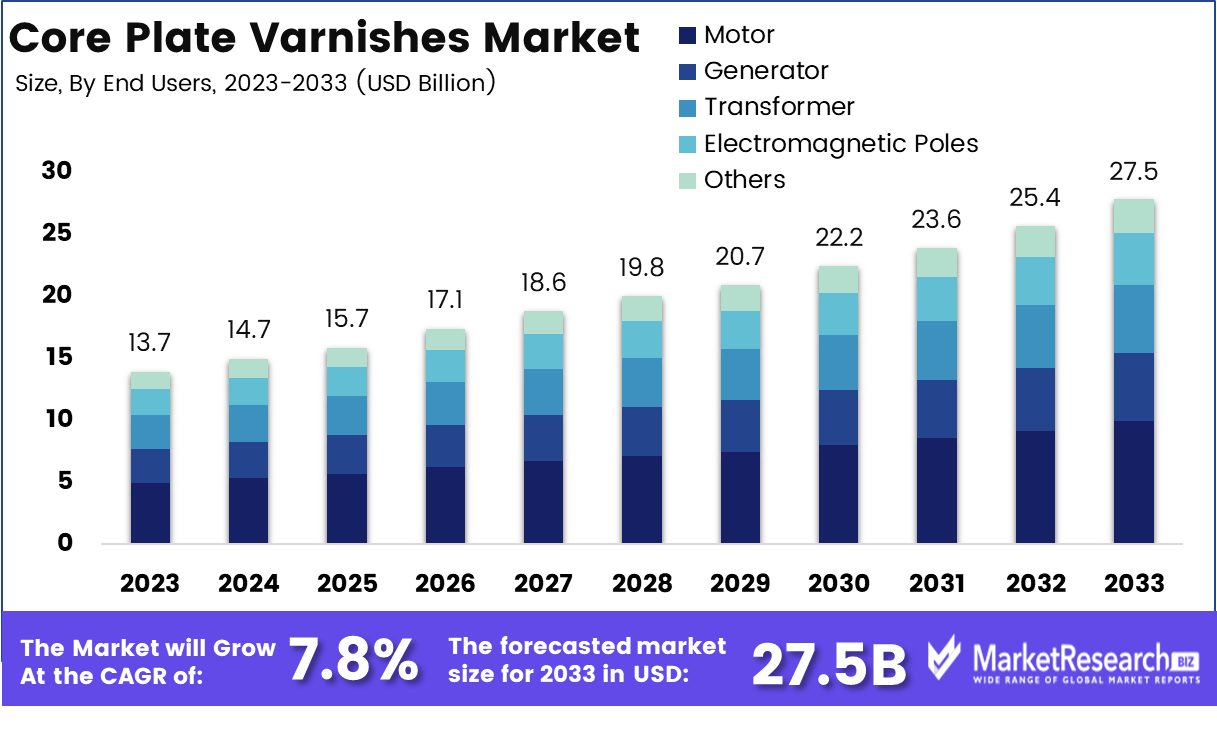

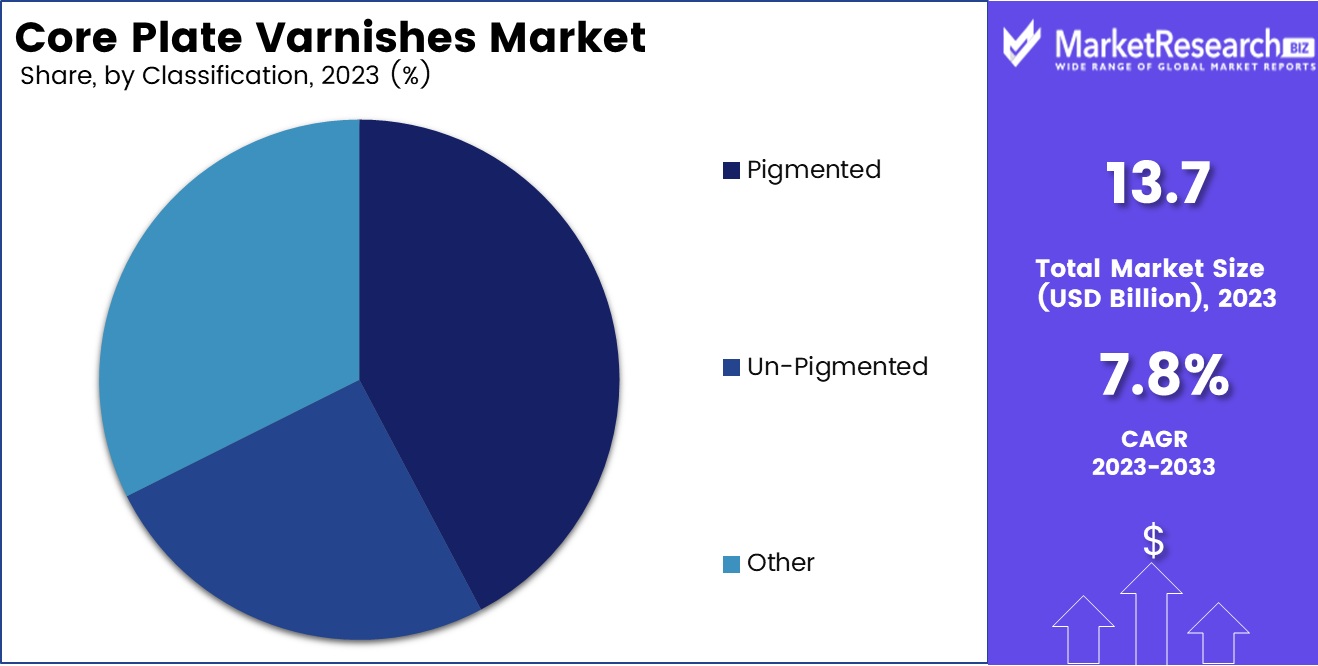

The Core Plate Varnishes Market was valued at USD 13.7 billion in 2023. It is expected to reach USD 27.5 billion by 2033, with a CAGR of 7.8% during the forecast period from 2024 to 2033.

The surge in demand for the utilization of electrical solutions and the high rate of accidents caused by a lack of electrical safety are some of the key driving factors for the core plate varnishes market. Core plate varnishes are high-quality performance, water-based coatings that can be utilized on metal components. Such type of coatings provides a shield to the area against chemical and tangible environmental degradation such as abrasion, corrosion, and impact. These varnishings are classified into three steps viscosity regulating solvent, resins, and additives which are mixed at the time of production of elements for developing a sturdy thickening impact in order to enhance the thickness of the paint base. Moreover, there are certain elements like low-temperature flexibility by using different types of chemicals depending upon their application purpose.

Heavy consumption of electricity has substantially increased across the globe, holding different types of factors like a surge in the rate of inhabitation in urban and rural industries, commercial sectors, increasing industrial formations, and per capita consumption. A maximum amount of energy has been lost during transmission from the production site to distribution centers. To recuperate such type of energy and reduce loss, insulation plays a vital role in enhancing the power transmission methods. Core plate varnishes are generally used to insulate electrical elements like motors, generators, and other electromagnetic poles. The usage of core plate varnishes in saving energy is an ideal technology in which coated laminations of the electrical core are not together by welding connection.

Heavy consumption of electricity has substantially increased across the globe, holding different types of factors like a surge in the rate of inhabitation in urban and rural industries, commercial sectors, increasing industrial formations, and per capita consumption. A maximum amount of energy has been lost during transmission from the production site to distribution centers. To recuperate such type of energy and reduce loss, insulation plays a vital role in enhancing the power transmission methods. Core plate varnishes are generally used to insulate electrical elements like motors, generators, and other electromagnetic poles. The usage of core plate varnishes in saving energy is an ideal technology in which coated laminations of the electrical core are not together by welding connection.Moreover, the surge in focus on renewable energy sources is also paying to the growth of the core plate varnishes market. These renewable energy sources often need transformers for efficacy power transmission, developing a need for core plate varnishes. Additionally, new progression in core plate varnish technologies is anticipated to increase the market expansion. Many manufacturers and producers are constantly funding research and development to enhance the elements and quality performance of core plate varnishes. This has resulted in making new innovative varnishes with good insulation properties, improved heat conductivity, and better resistance to moistness and chemicals. The demand for the core plate varnishes will gradually increase due to their high-quality performance and the viscosity of the paint base will help in market expansion during the forecasted period.

Key Takeaways

- Market Value: The Core Plate Varnishes Market was valued at USD 13.7 billion in 2023. It is expected to reach USD 27.5 billion by 2033, with a CAGR of 7.8% during the forecast period from 2024 to 2033.

- Based on End Users: Motor segment dominates core plate varnishes market by end users.

- Based on Classification: Pigmented varnishes lead classification in core plate varnishes market.

- Based on Chemical: Polyester varnishes are the leading chemical type in market.

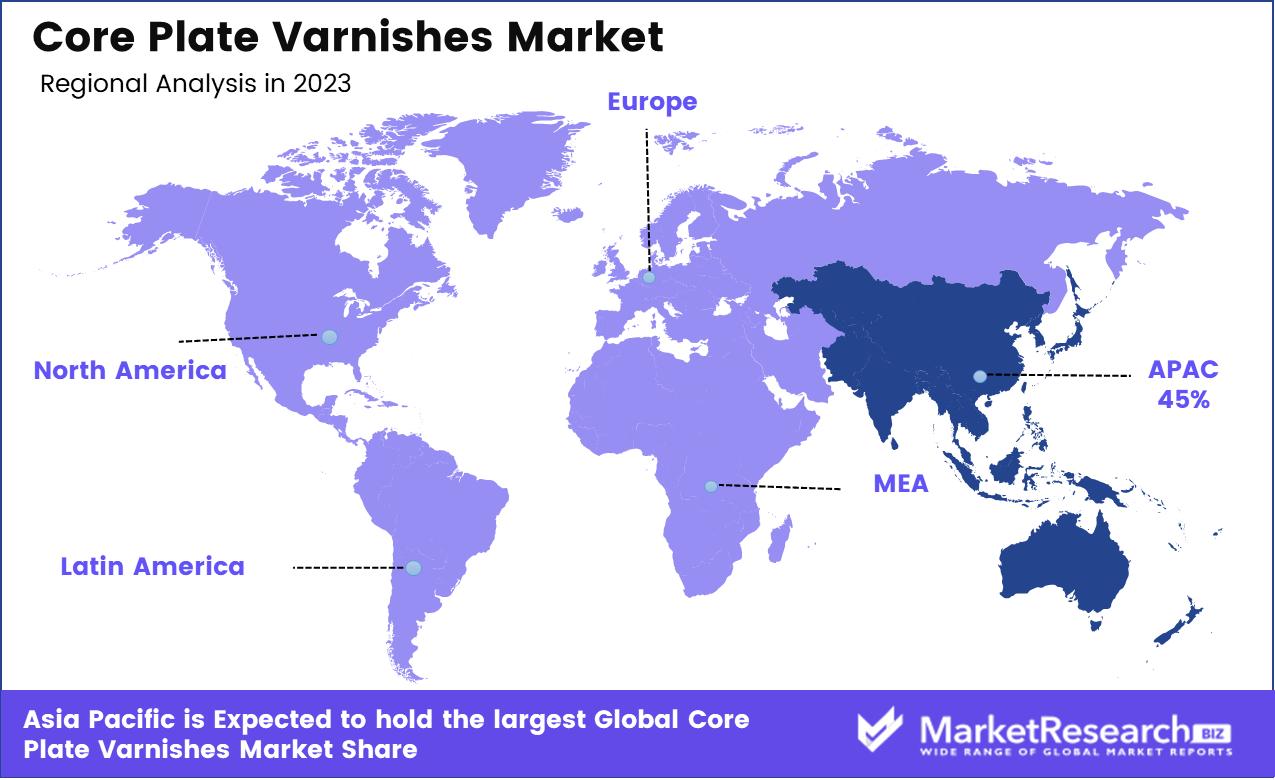

- Regional Analysis: Asia-Pacific dominates with 45% of the global core plate varnishes market.

- Growth Opportunity: In 2023, the core plate varnishes market is set to grow significantly, driven by a strategic focus on ESG priorities and innovative nanocomposite technologies that enhance product performance and sustainability.

Driving factors

Electrification of Transport and Enhanced Material Demands

The burgeoning adoption of electric vehicles marks a significant driver for the core plate varnishes market. This trend is underpinned by global shifts towards sustainable transportation solutions to mitigate climate change impacts. Electric vehicles (EVs) require high-quality magnetic cores for efficient motor performance, directly influencing demand for advanced core plate varnishes. These varnishes enhance the magnetic properties of core plates, crucial for the optimal functioning of EV motors by reducing eddy current losses and improving thermal stability.

As the generative AI in the automotive industry continues to innovate and expand the production of EVs, the demand for specialized varnishes that can withstand high operational temperatures and provide exceptional electrical insulation is expected to rise. This demand is reflective of broader industrial needs to improve energy efficiency and performance in critical components like motor cores.

Policy-Driven Market Expansion in Agriculture and Energy

Government investments and policies play a pivotal role in shaping the core plate varnishes market, particularly through initiatives aimed at enhancing the efficiency of transformers and motors used in agriculture. Supportive policies include subsidies or grants for upgrading agricultural electrical equipment and driving demand for core plate varnishes that contribute to the longevity and efficiency of these devices.

For instance, enhanced varnishes are essential for preventing corrosion and thermal degradation in transformers and motors, thereby ensuring reliable operation under variable field conditions. This factor is part of a larger governmental push towards modernizing infrastructure to boost productivity and sustainability in critical economic sectors, including agriculture.

Innovation Leading Market Transformation

Technological advancements in core plate varnishes significantly influence market dynamics by enhancing product offerings and operational efficiencies. Developments such as modified polyester-based varnishes and coatings that absorb heat and moisture are particularly transformative. These innovations address key industry challenges like energy loss and efficiency degradation under harsh conditions, leading to wider adoption in various applications, including industrial motors and residential transformers.

Such technological enhancements not only improve the performance of electrical components but also extend their operational life, thereby reducing maintenance costs and downtime. The continuous improvement in varnish technologies is a critical factor driving market growth, as stakeholders seek more durable and efficient solutions to meet increasing regulatory and environmental standards.

Restraining Factors

Regulatory Compliance Costs Impacting Market Dynamics

The core plate varnishes market faces significant challenges due to the stringent compliance requirements with quality standards and environmental regulations. These regulations are designed to ensure that the varnishes used in electrical components such as motors and transformers do not adversely affect the environment or human health. Compliance involves not only adhering to standards that limit the use of harmful chemicals in varnish formulations but also implementing processes that mitigate environmental impact during production and disposal.

This compliance can lead to increased production costs, as manufacturers may need to invest in cleaner technologies or reformulate their products to eliminate or reduce the use of restricted substances like volatile organic compounds (VOCs) and other hazardous materials. Furthermore, the necessity to undergo rigorous testing and certification processes to prove compliance adds to the operational expenses. These factors can restrict market growth by increasing the cost of varnishes, potentially making them less competitive compared to alternatives that are not as strictly regulated.

Stringent Disposal and Usage Regulations Limiting Flexibility

Stringent regulatory requirements regarding the use and disposal of chemical substances in core plate varnishes further constrain market expansion. Regulations such as the European Union's REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) and the U.S. EPA's TSCA (Toxic Substances Control Act) impose strict controls over the entire lifecycle of chemical substances, from production to disposal. These laws ensure that any environmental risks are managed effectively but also limit the flexibility of varnish manufacturers in their choice of raw materials and disposal methods.

Such restrictions can hinder innovation by limiting the types of chemicals that can be incorporated into varnish formulations, potentially delaying the development of new and improved products. Additionally, the need for compliant disposal methods can incur further costs, as safe handling, recycling, or garbage disposal of waste materials must meet regulatory standards, often requiring specialized services. Collectively, these regulatory pressures serve to temper the growth of the core plate varnishes market by adding layers of complexity and financial burden to manufacturing and supply chain operations.

End Users Analysis

The motor segment leads the core plate varnishes market, essential for enhancing motor efficiency and longevity.

In 2023, Motors held a dominant market position in the End Users segment of the core plate varnishes market, primarily due to their extensive application across various industries including automotive, manufacturing, and consumer electronics. Electric Motors require high-quality core plate varnishes to ensure efficient performance, durability, and resistance to environmental factors, which significantly drive the demand within this segment.

Generators followed closely, leveraging core plate varnishes to enhance electrical insulation and improve operational reliability, especially in sectors like energy production and industrial applications where uninterrupted power supply is critical. The need for reliable and efficient generators in emerging economies, where energy demand continues to surge, further bolsters this segment's growth.

Transformers also represent a substantial portion of the market, with core plate varnishes playing a vital role in optimizing energy transmission and reducing losses due to eddy currents and other inefficiencies. The push towards renewable energy and the upgrading of aging electrical grids globally enhance the demand for advanced varnishes in this segment.

Electromagnetic poles, although a smaller segment, utilize specialized varnishes to maintain the integrity and performance of electromagnetic components used in a variety of electronic and industrial applications.

The "Others" category encompasses a wide range of niche applications, including household appliances and specialized industrial equipment, where varnishes contribute to the functionality and longevity of these devices.

Classification Analysis

Pigmented varnishes lead the market, preferred for their superior protective and insulative properties.

In 2023, Pigmented held a dominant market position in the Classification segment of the core plate varnishes market, owing to its superior performance characteristics and broad application range. Pigmented varnishes, which contain additives for improved color and specific physical properties, provide enhanced durability and protection to electrical components like motors, transformers, and generators. Their ability to offer better heat dissipation and improved electrical insulation makes them particularly suitable for high-performance applications, where efficiency and longevity are paramount.

Un-pigmented varnishes also play a significant role in the market, particularly in applications where color differentiation is not a priority. These varnishes offer excellent electrical insulation and are commonly used in specialized industrial and commercial applications that focus on transparent coatings to visually inspect the substrate.

The "Other" category includes a variety of specialized varnishes formulated for specific applications, such as those requiring extra heat resistance or flexibility. These niche products address the unique needs of advanced electrical components and systems, albeit on a smaller scale than pigmented varnishes.

Chemical Analysis

Polyester is the dominant chemical type in the core plate varnishes market, offering durability.

In 2023, Polyester held a dominant market position in the Chemical segment of the core plate varnishes market, driven by its exceptional properties that cater to demanding electrical and mechanical requirements. Polyester varnishes are favored for their excellent thermal stability, mechanical strength, and resistance to environmental stresses, making them ideal for a wide range of applications including motors, transformers, and other high-end electrical components.

Alkyd Phenolic varnishes, known for their good adhesion and protective properties, continue to be used in various industrial applications but have seen some displacement by polyester due to the latter's superior performance in harsh conditions. Polyurethane varnishes are also significant in the market, prized for their robustness and flexibility which make them suitable for applications where mechanical stress is an issue.

The "Others" category within this segment includes a variety of specialized chemicals tailored for unique industry needs, such as higher temperature resistance or specific dielectric properties. These niche varnishes are critical in applications where standard solutions do not suffice, but they do not match the volume driven by the widespread adoption of polyester-based solutions.

Key Market Segments

End Users

- Motor

- Generator

- Transformer

- Electromagnetic Poles

- Others

Classification

- Pigmented

- Un-Pigmented

- Other

Chemical

- Alkyd Phenolic

- Polyurethane

- Polyester

- Others

Growth Opportunity

Strategic Emphasis on ESG Priorities

In 2023, the global core plate varnishes market is poised for transformative growth driven by an increased focus on Environmental, Social, and Governance (ESG) priorities by leading companies such as Asian Paints. This focus is not just a compliance measure but a strategic lever for sustainable growth. Companies that align their operations with ESG principles are likely to attract more investment and partnership opportunities, particularly from stakeholders prioritizing sustainability.

For the varnishes market, this translates into a demand for products that are environmentally friendly, such as low-VOC or VOC-free varnishes, which minimize environmental impact and meet stricter regulatory standards. The integration of ESG priorities into business models can enhance brand reputation and foster customer loyalty, which are critical competitive advantages in a market increasingly influenced by consumer and regulatory demands for sustainability.

Innovation Through Nanocomposite Technologies

Another significant opportunity for the core plate varnishes market in 2023 lies in technological innovation, particularly through the development of nanocomposite films. The creation of modified guar gum nanocomposite films reinforced with silver nanoparticles exemplifies the type of innovation that can expand market applications. These nanocomposites offer enhanced properties such as increased thermal stability, improved electrical insulation, and resistance to environmental factors, making them ideal for use in high-performance applications across various industries including electronics, automotive, and aerospace.

By leveraging nanotechnology, manufacturers can develop differentiated products that meet the evolving needs of these industries, potentially opening new markets and applications for varnishes. This advancement not only supports market growth but also aligns with the growing trend towards materials that contribute to greater efficiency and durability, key factors in today's technology-driven market landscape.

Latest Trends

Increased Demand for Sustainable Solutions

One of the most notable trends shaping the core plate varnishes market in 2023 is the heightened demand for sustainable solutions. With growing environmental concerns and regulatory pressures, industries across the globe are increasingly adopting eco-friendly practices. In the realm of core plate varnishes, this translates to a shift towards products that promote energy efficiency, reduce environmental impact, and enhance sustainability throughout the value chain.

Manufacturers are under pressure to develop varnishes that minimize carbon footprint and offer improved lifecycle performance. This trend is driven not only by regulatory compliance but also by consumer preferences for environmentally responsible products. As a result, market players are investing in research and development to formulate innovative varnishes that meet these stringent criteria.

Product Innovation

Another key trend shaping the core plate varnishes market in 2023 is a heightened focus on product innovation. As competition intensifies and market dynamics evolve, manufacturers are increasingly turning to innovation as a means of gaining a competitive edge and capturing new opportunities. In particular, there is a growing emphasis on developing varnishes with enhanced performance characteristics, such as improved adhesion, durability, and resistance to environmental factors.

Additionally, market players are exploring novel formulations and technologies to address emerging application requirements and cater to evolving customer needs. By investing in research and development, companies can stay ahead of the curve and position themselves for success in the dynamic core plate varnishes market landscape.

Regional Analysis

Asia-Pacific dominates the core plate varnishes market with a substantial 45% share of global demand.

In the global core plate varnishes market, regional dynamics vary significantly, influenced by industrial activity, regulatory environments, and technological advancements. Dominating the market, Asia-Pacific accounts for approximately 45% of the global share, driven by robust manufacturing sectors in countries like China, Japan, and South Korea. This region benefits from high-volume production capacities and increasing investments in automotive and electronics industries, which demand high-quality core plate varnish for components requiring excellent electrical insulation and thermal properties.

North America, another key player, showcases strong growth due to the region's stringent environmental regulations and a focus on renewable energy sources that necessitate advanced electrical infrastructure. The U.S. leads in the adoption of innovative varnish technologies, particularly for use in electric vehicles and renewable energy applications, reflecting a market highly responsive to ecological concerns and technological integrations.

Europe follows closely, where the market is propelled by a combination of stringent EU regulations regarding chemical usage and a robust automotive industry. European manufacturers are leading the way in developing and applying environmentally friendly varnish formulations, aligning with the region's aggressive environmental policies.

The Middle East & Africa and Latin America regions, though smaller in market share, are experiencing gradual growth. In the Middle East & Africa, the growth is spurred by increasing urbanization and industrialization, which drive the demand for more efficient electrical components. Latin America benefits from growing investments in infrastructure development that are likely to increase the demand for motors and transformers, thereby pushing the need for core plate varnishes.

Key Regions and Countries

North America

- US

- Canada

- Mexico

Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In 2023, the global core plate varnishes market will be significantly influenced by a diverse array of key players, each contributing unique strengths and strategic focuses. Among these, Helios Group and Rembrandtin Lack GmbH are notable for their robust presence in Europe, known for pioneering eco-friendly varnish technologies that align with the stringent environmental regulations of the region. ALTANA is another significant contributor, leveraging its global reach and extensive R&D capabilities to innovate in the formulation of high-performance varnishes that meet both functional and ecological standards.

In Asia, companies like TOYO INK and Sichuan Dongfang Insulating Material Co., Ltd. play critical roles, driven by regional manufacturing strengths and the escalating demand from the automotive and electronics sectors. TOYO INK, in particular, is adept at integrating advanced material science to enhance the thermal and electrical properties of varnishes, catering to the high-tech industries prevalent in the region.

North American players such as AXALTA and JOHN C. DOLPH COMPANY are pivotal, primarily due to their focus on technological advancements and high-quality standards, which are imperative in industries such as renewable energy and automotive. AXALTA, for example, stands out with its commitment to sustainability and innovation, factors that are increasingly decisive in competitive markets.

Companies like SSAB AB and voestalpine Stahl GmbH underscore the integration of steel and metal industries with core plate varnishes, emphasizing the importance of material enhancements to achieve higher efficiency and performance in electrical applications.

Market Key Players

- Helios Group

- Rembrandtin Lack GmbH

- ALTANA

- SSAB AB

- TOYO INK

- BAKELITE HYLAM LTD

- AXALTA

- M?der

- JOHN C. DOLPH COMPANY

- Super Urecoat Industries

- Sichuan Dongfang Insulating Material Co. Ltd.

- Vishal Enterprises

- AEV Ltd

- voestalpine Stahl GmbH

- Hitachi Chemical Co. Ltd

- Chetak Manufacturing Co

Recent Development

- In April 2024, Quaker Houghton will introduce its new electrical steel self-bonding varnish, QH EVERTREAT™ 7000, at IESSS 2024, offering enhanced processing flexibility and productivity for high-performance lamination stacks in e-Mobility and renewable energy sectors.

- In October 2023, Beckers launched Beckry®Core, a new core plate varnish that enhances motor efficiency and supports compact design in the e-mobility industry, bolstering its leadership in sustainable coatings.

- In February 2023, Siegwerk introduced UniNATURE Water-Oil Barrier Coating, a sustainable, 100% natural coating for single-use paper plates, aligning with EU directives and promoting recyclability and a Circular Economy, according to FINISHING AND COATING.

Report Scope

Report Features Description Market Value (2023) USD 13.7 Billion Forecast Revenue (2033) USD 27.5 Billion CAGR (2024-2032) 7.8% Base Year for Estimation 2023 Historic Period 2016-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered End Users,(Motor, Generator, Transformer, Electromagnetic Poles, Others), Classification (Pigmented, Un-Pigmented, Other), Chemical (Alkyd Phenolic, Polyurethane, Polyester, Others) Regional Analysis North America - The US, Canada, Rest of North America, Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America - Brazil, Mexico, Rest of Latin America, Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa Competitive Landscape Helios Group, Rembrandtin Lack GmbH, ALTANA, SSAB AB, TOYO INK, BAKELITE HYLAM LTD, AXALTA, M?der,J OHN C. DOLPH COMPANY, Super Urecoat Industries, Sichuan Dongfang Insulating Material Co. Ltd., Vishal Enterprises, AEV Ltd,voestalpine Stahl GmbH, Hitachi Chemical Co. Ltd, Chetak Manufacturing Co Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Helios Group

- Rembrandtin Lack GmbH

- ALTANA

- SSAB AB

- TOYO INK

- BAKELITE HYLAM LTD

- AXALTA

- M?der

- JOHN C. DOLPH COMPANY

- Super Urecoat Industries

- Sichuan Dongfang Insulating Material Co. Ltd.

- Vishal Enterprises

- AEV Ltd

- voestalpine Stahl GmbH

- Hitachi Chemical Co. Ltd

- Chetak Manufacturing Co

Our Clients

View Our Licence Options