Cell Culture Market Report By Product Type (Consumables (Media, Sera, Reagents, Buffers and Salts, Growth Factors and Cytokines, Others), Instruments (Bioreactors, Culture Systems, Centrifuges, Cell Counters, Others), Accessories), By Application (Biopharmaceutical Production, Cancer Research, Drug Screening and Development, Regenerative Medicine, Stem Cell Research, Vaccine Production, Others), By End User, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

-

48016

-

June 2024

-

321

-

-

This report was compiled by Trishita Deb Trishita Deb is an experienced market research and consulting professional with over 7 years of expertise across healthcare, consumer goods, and materials, contributing to over 400 healthcare-related reports. Correspondence Team Lead- Healthcare Linkedin | Detailed Market research Methodology Our methodology involves a mix of primary research, including interviews with leading mental health experts, and secondary research from reputable medical journals and databases. View Detailed Methodology Page

-

Quick Navigation

Report Overview

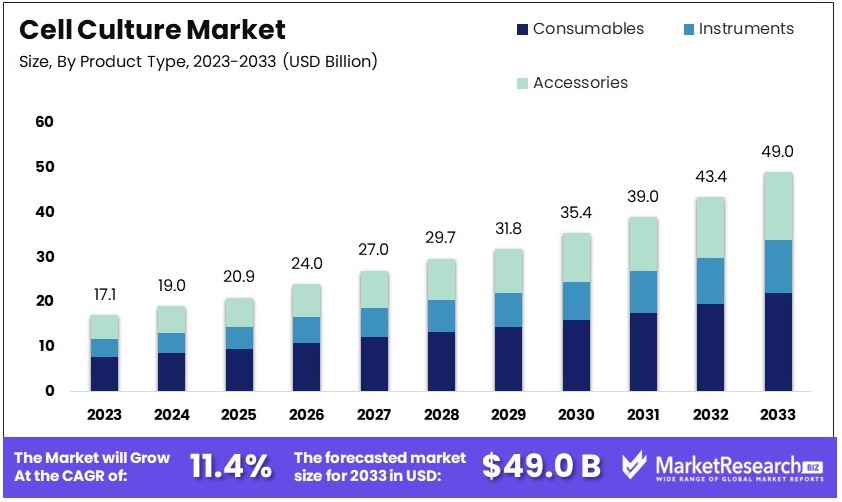

The Global Cell Culture Market size is expected to be worth around USD 49.0 Billion by 2033, from USD 17.1 Billion in 2023, growing at a CAGR of 11.4% during the forecast period from 2024 to 2033.

The cell culture market involves the development and provision of products and environments for the growth of cells in controlled conditions. This market is pivotal for producing biological products, conducting drug discovery, and developing regenerative medicine. It includes culture media, serums, reagents, and equipment necessary for the cultivation of mammalian, bacterial, and other cell types.

Demand is fueled by the need for vaccine production, monoclonal antibodies, and pharmaceutical applications. Key growth drivers include advancements in biopharmaceuticals and the increasing use of cell culture techniques in genetic engineering and cancer research. Companies in this sector focus on innovation and scalability to meet the global demand, particularly in personalized medicine and therapeutic development.

The cell culture market is experiencing significant growth driven by advancements in biotechnology and increasing demand for biopharmaceuticals. This market growth can be attributed to several factors, including technological innovations and strategic product launches. In June 2024, Sphere Fluidics introduced Cyto-CellectPLUS, an innovative assay that enables researchers to measure IgG productivity at the single-cell level. This advancement allows for the identification and selection of cells with the highest productivity, enhancing cell line development and optimizing production processes.

Moreover, the market has witnessed the launch of NewBiologix's proprietary HEK293 cell line in May 2024. This cell line is designed for the expression of viral vectors used in gene therapy. It provides a reliable and scalable solution for producing viral vectors, addressing the growing need for effective gene therapy solutions. These developments highlight the industry's focus on improving efficiency and scalability in cell culture processes.

The market's expansion is also supported by the increasing prevalence of chronic diseases and the rising demand for personalized medicine. The use of cell culture techniques in drug development and regenerative medicine is becoming more widespread, driving further market growth. Additionally, government initiatives and investments in research and development are fostering innovation and supporting market dynamics.

Key Takeaways

- Report Overview: The Global Cell Culture Market was valued at USD 17.1 Billion in 2023 and is expected to reach USD 49.0 Billion by 2033, growing at a CAGR of 11.4%.

- Technology Analysis: Advancements in cell culture and bioprocessing technologies drive market growth by enhancing efficiency and scalability.

- Product Type Analysis: Media dominates with 30% due to its essential role in sustaining cell growth and proliferation.

- Application Analysis: Biopharmaceutical production leads with 40% driven by high demand for cell-based production technologies.

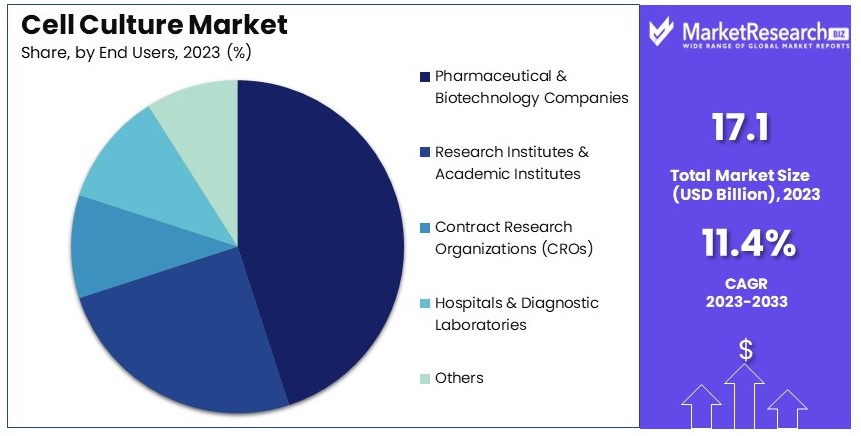

- End User Analysis: Pharmaceutical and biotechnology companies hold a 50% share, heavily utilizing cell culture technologies in development and production.

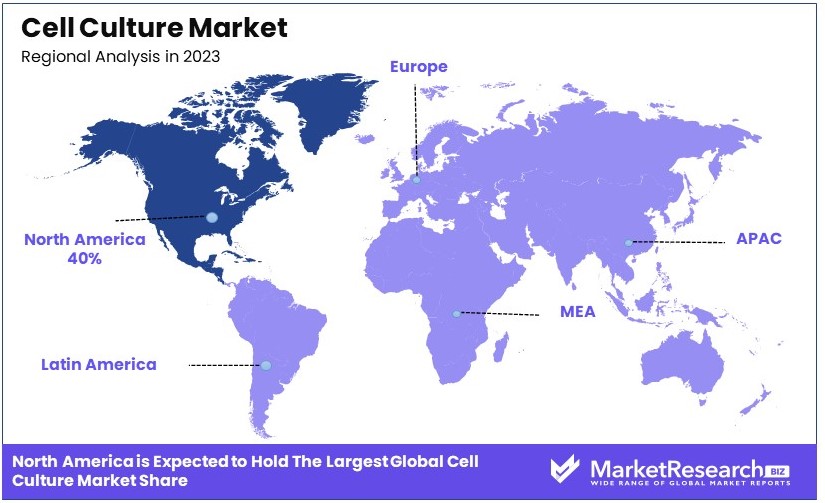

- Dominant Region: North America dominates the market with a 40% share, supported by advanced infrastructure and significant R&D investment.

- High Growth Region: Asia Pacific is the fastest-growing region with a projected CAGR of 12%, driven by expanding healthcare infrastructure and investments.

- Analyst Viewpoint: The cell culture market is set to expand significantly, driven by increasing demand for regenerative medicine and advanced therapeutic applications. However, regulatory challenges and high costs could hinder growth.

Driving Factors

Increasing Demand for Regenerative Medicine and Cell-Based Therapies Drives Market Growth

The cell culture market is experiencing robust growth driven by the escalating demand for regenerative medicine and cell-based therapies. These innovative therapeutic approaches utilize cells to repair or replace damaged tissues and organs, marking a significant advancement in medical treatments for a range of diseases and injuries. For instance, stem cell therapies are under research for potentially revolutionary treatments for Alzheimer's disease, Parkinson's, and spinal cord injuries.

This surge in clinical applications has led to an increased demand for specialized cell lines and sophisticated cell culture technologies, which are essential for developing and testing these therapies. The integration of cell culture into the development of regenerative medicine not only supports current healthcare advancements but also sets the stage for future medical breakthroughs, significantly impacting the growth of the cell culture market.

Advancements in Cell Culture and Bioprocessing Technologies Drives Market Growth

Continuous advancements in cell culture and bioprocessing technologies have been pivotal in driving the growth of the cell culture market. Developments in cell culture media, bioreactors, and automated systems have significantly enhanced the efficiency and scalability of cell production. These improvements support a wide range of applications, from academic research to industrial-scale biopharmaceutical manufacturing.

For example, the introduction of serum-free and chemically defined media has revolutionized cell culture by improving the consistency and reliability of cell growth conditions. Such technological enhancements not only meet the growing demands for high-quality cells required in therapeutic applications and research but also drive the adoption of these advanced products and systems across different sectors of the biotechnology and pharmaceutical industries, thus fueling market expansion.

Growing Investment in Cell-Based Research and Development Drives Market Growth

The cell culture market benefits greatly from increasing investments by governments, pharmaceutical companies, and research institutions in cell-based research and development. These investments are geared towards exploring new cell-based therapies, developing novel cell lines, and advancing cell engineering techniques.

For instance, significant financial contributions like those from the California Institute for Regenerative Medicine (CIRM), which has invested billions in stem cell assay, underscore the vital role of funding in fostering market growth. This influx of capital not only supports the advancement of scientific research and therapeutic innovations but also stimulates the development of new technologies and applications in cell culture. Consequently, this sustained financial support ensures the dynamic growth of the cell culture market by enhancing research capabilities and accelerating the commercialization of cell-based technologies.

Restraining Factors

Regulatory Challenges and Stringent Guidelines Restrain Market Growth

The cell culture market is significantly impacted by rigorous regulatory challenges and stringent guidelines set by authorities like the Food and Drug Administration (FDA) and the European Medicines Agency (EMA). These regulations are designed to ensure the safety and efficacy of cell-based products but can also inadvertently slow market progress.

The extensive requirements for preclinical and clinical testing, alongside demanding manufacturing and quality control measures, can prolong the product approval process. This not only increases the time to market but also escalates development costs. As a result, these regulatory hurdles can deter new entrants and limit innovation within the market, especially for cell therapy products, which require rigorous oversight.

High Costs Associated with Cell-Based Research and Therapies Restrain Market Growth

The development and commercialization of cell-based research and therapies entail substantial financial investment, which poses a significant barrier to market growth. The costs involved in research and development activities, coupled with the need for specialized equipment, skilled personnel, and advanced manufacturing facilities, can be prohibitively high.

This financial burden is particularly challenging for smaller companies and research institutions, which may lack the necessary capital. In regions with limited funding opportunities, these high costs further restrict the expansion of the cell culture market, stifling innovation and the adoption of advanced cell-based therapies.

Product Type Analysis

Media dominates with 30% due to its essential role in sustaining cell growth and proliferation.

In the product type segment of the cell culture market, media stands out as the most crucial component, commanding a significant share due to its foundational role in providing necessary nutrients for cell growth and maintenance. This dominance is fueled by the increasing demand for biopharmaceuticals, where media is critical in the production processes, including the cultivation of cells used in vaccine production and monoclonal antibody production.

Other consumables such as sera, which provides growth factors and hormones, and reagents, necessary for regulating cell environments, also play pivotal roles. Growth factors and cytokines are specifically important for directing cell differentiation and proliferation, catering especially to regenerative medicine and stem cell research. Buffers and salts maintain the pH and osmolarity of the culture environment, which is vital for cell viability and function.

Instruments like bioreactors and culture systems are integral for scaling up cell culture operations, particularly in industrial applications that require large-scale cell production. These systems are designed to maintain optimal growth conditions and are increasingly incorporating advanced technologies for better control and efficiency. Accessories and other equipment such as centrifuges and cell counters facilitate the processing and analysis of cells, further underscoring their utility in both research and clinical settings.

While media captures the largest market share due to its direct impact on cell culture outcomes, other consumables and instruments support the complex infrastructure of cell culture applications, enhancing the overall growth and technological advancement within the market.

Application Analysis

Biopharmaceutical production dominates with 40% due to the critical demand for cell-based production technologies in drug and vaccine manufacturing.

The application segment of the cell culture market is profoundly led by biopharmaceutical production, where cell culture technology is indispensable for the production of vaccines, therapeutic proteins, and monoclonal antibodies. This segment's dominance is driven by the rising global demand for biopharmaceuticals, propelled by an aging population and increasing prevalence of chronic diseases.

Cancer research also relies heavily on cell culture techniques for studying cancer cells and developing new treatments. The use of cell culture in drug screening and development is vital for toxicity testing and other preclinical studies, which are critical steps in the drug development process. Regenerative medicine and stem cell research are rapidly growing fields that utilize cell culture for tissue engineering and to study stem cell properties for potential therapeutic applications.

Vaccine production, another critical area, has seen a surge in demand, particularly highlighted by the global response to pandemics. Cell culture technologies are central to the production of recombinant vaccines and viral vectors, playing a key role in the rapid development and scalability of vaccine production.

Overall, while biopharmaceutical production leads the applications in the cell culture market due to its direct impact on healthcare and medicine, other applications like cancer research and regenerative medicine significantly contribute to the scientific advancements and clinical applications of cell culture technologies.

End User Analysis

Pharmaceutical and biotechnology companies dominate with 50% due to their extensive use of cell culture technologies in drug development and production processes.

The end-user segment of the cell culture market is predominantly occupied by pharmaceutical and biotechnology companies. These entities leverage cell culture technology extensively to develop and manufacture drugs, vaccines, and biologics, making them the largest market shareholders. This dominance is bolstered by significant R&D investments and the increasing incorporation of biologics in therapeutic regimes.

Research institutes and academic institutions also form a significant part of this market, driven by their role in conducting fundamental and applied research in life sciences. Their work often lays the groundwork for innovations in drug development and other clinical applications. Contract research organizations (CROs) provide essential services for pharmaceutical companies, including drug development and clinical trials, where cell culture plays a crucial role in preclinical evaluations.

Hospitals and diagnostic laboratories utilize cell culture methods for various applications, including cancer research, genetic testing, and other clinical diagnostics, though they do not dominate the market share.

While pharmaceutical and biotech companies are the primary drivers due to their extensive use and dependency on cell culture technologies, other end-users like research institutes and CROs are crucial for supporting the research and development landscape that underpins advancements in cell culture applications.

Key Market Segments

By Product Type

- Consumables

- Media

- Sera

- Reagents

- Buffers and Salts

- Growth Factors and Cytokines

- Others

- Instruments

- Bioreactors

- Culture Systems

- Centrifuges

- Cell Counters

- Others

- Accessories

By Application

- Biopharmaceutical Production

- Cancer Research

- Drug Screening and Development

- Regenerative Medicine

- Stem Cell Research

- Vaccine Production

- Others

By End User

- Pharmaceutical and Biotechnology Companies

- Research Institutes and Academic Institutes

- Contract Research Organizations (CROs)

- Hospitals and Diagnostic Laboratories

- Others

Growth Opportunities

Personalized Medicine and Targeted Therapies Offer Growth Opportunity

The cell culture market is set to expand significantly due to advancements in personalized medicine and targeted therapies. The development of patient-specific cell lines and cell-based therapies that align with individual genetic profiles promises to revolutionize treatment approaches, making them more effective and tailored to individual needs.

Technologies like induced pluripotent stem cells (iPSCs) allow for the creation of cell lines from a patient's own cells, minimizing the risk of immune rejection and enhancing the efficacy of treatments. This shift towards personalized medical solutions is fostering substantial growth in the cell culture market, as these technologies require sophisticated cell culture techniques to develop and implement.

Organ and Tissue Engineering Offers Growth Opportunity

The demand for organ and tissue engineering presents a substantial growth opportunity for the cell culture market. Innovations in cell culture methods, alongside advancements in biomaterials and 3D bioprinting, are making it possible to create functional organs and tissues for transplantation or drug testing.

For instance, the ability to engineer tissues like heart muscle or liver constructs from stem cells or specialized cell lines has vast implications for medical research and application. These developments not only help in understanding human biology but also in creating viable therapeutic options, thereby driving the expansion of the cell culture market.

Trending Factors

3D Cell Culture and Organoid Models Are Trending Factors

The adoption of 3D cell culture and organoid models is a key trend within the cell culture market. These advanced culture systems more accurately replicate the intricate cellular arrangements and microenvironments of actual tissues, offering more physiologically relevant models for scientific research, drug testing, and disease modeling.

Organoids, often derived from stem cells or patient-specific cells, enable detailed studies of organ development, disease pathways, and the testing of potential treatments. This move towards more realistic and functional cell models highlights a growing shift in the market, emphasizing the increasing demand for complex and versatile cell culture systems.

Cell-Based Biosensors and Diagnostics Are Trending Factors

The development of cell-based biosensors and diagnostic tools represents a growing trend in the cell culture market. These technologies utilize living cells to detect and analyze various biomolecules, pollutants, or pathogens, providing a unique approach to diagnostics.

Engineered cell lines, for instance, are being utilized to create sensitive and specific tests for early disease detection and to monitor therapeutic responses. This trend is indicative of an expanding role for cell culture technologies in biomedical applications, where they can offer precise and dynamic insights into health and environmental conditions, pushing the boundaries of traditional diagnostic methods.

Regional Analysis

North America Dominates with 40% Market Share

North America's dominance in the Cell Culture Market is driven by advanced research infrastructure, significant investments in biotechnology, and a strong presence of major pharmaceutical companies. The region benefits from substantial funding for cell-based research from both government and private sectors. Additionally, a robust regulatory framework supports the development and commercialization of cell culture technologies, enhancing market growth.

The high market share in North America is also due to the region's focus on innovative therapies, including regenerative medicine and personalized treatments. The presence of leading academic institutions and research organizations facilitates cutting-edge research and development activities. Moreover, favorable healthcare policies and increasing awareness about advanced therapies contribute to the market's expansion.

North America's market presence is expected to remain strong, with continued investments in biotechnology and healthcare. The region's focus on developing new cell-based therapies and advancing bioprocessing technologies will drive further growth. The Cell Culture Market in North America is projected to grow at a CAGR of 10% over the next few years, reinforcing its leading position.

Regional Market Shares and Growth Rates

Europe: Europe holds approximately 30% of the Cell Culture Market. The region's growth is driven by strong governmental support for biotechnology and healthcare innovation. Countries like Germany and the UK are key contributors. The market in Europe is expected to grow at a CAGR of 9.5%, supported by advancements in cell therapy and biomanufacturing.

Asia Pacific: Asia Pacific accounts for about 20% of the Cell Culture Market. Rapid growth in biotechnology and healthcare infrastructure, particularly in countries like China, Japan, and India, is propelling the market. The region's market is projected to grow at a CAGR of 12%, driven by increasing investments and expanding research capabilities.

Middle East & Africa: The Middle East & Africa region holds a smaller share, around 5%, of the Cell Culture Market. Growth is driven by increasing healthcare investments and the adoption of advanced medical technologies. The market is expected to grow at a CAGR of 8%, with countries like the UAE and South Africa leading the way.

Latin America: Latin America comprises about 5% of the Cell Culture Market. The region's growth is supported by expanding biotechnology sectors in countries like Brazil and Mexico. The market in Latin America is anticipated to grow at a CAGR of 7%, fueled by increasing research activities and healthcare investments.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The cell culture market is led by several key players. Thermo Fisher Scientific Inc. and Merck KGaA are market leaders with extensive product portfolios and strong global presence. Their advanced technologies and robust R&D capabilities ensure top positions.

Becton, Dickinson and Company and Corning Incorporated hold significant market shares due to their high-quality cell culture products and innovative solutions. Their strong customer bases and effective distribution networks enhance their market influence.

Lonza Group Ltd. and Eppendorf AG are known for their comprehensive cell culture systems and bioprocessing solutions. Their focus on innovation and customer support strengthens their competitive positions.

Sartorius AG and GE Healthcare contribute significantly through their advanced biopharmaceutical production technologies. Their strategic collaborations and extensive industry expertise boost their market impact.

PromoCell GmbH and HiMedia Laboratories specialize in providing high-quality media and reagents, catering to research and clinical applications. Their targeted product offerings and niche market focus make them key players.

Irvine Scientific and Sigma-Aldrich Corporation (part of Merck) are recognized for their reliable and high-performance cell culture media. Their strong market presence and focus on quality ensure their competitive edge.

STEMCELL Technologies Inc. is notable for its specialized products supporting stem cell research and regenerative medicine. Their innovative solutions and strong research focus position them as key innovators in the market.

Overall, these key players shape the cell culture market with their advanced technologies, strong R&D, and strategic positioning. Their combined efforts drive market growth and innovation.

Market Key Players

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Becton, Dickinson and Company

- Corning Incorporated

- Lonza Group Ltd.

- Eppendorf AG

- Sartorius AG

- GE Healthcare

- PromoCell GmbH

- HiMedia Laboratories

- Irvine Scientific

- Sigma-Aldrich Corporation

- STEMCELL Technologies Inc.

Recent Developments

- June 2024: Sphere Fluidics launches Cyto-CellectPLUS, a new assay that enables researchers to measure IgG productivity at the single-cell level, allowing them to identify and select cells with the highest productivity for enhanced cell line development.

- May 2024: NewBiologix launches a proprietary HEK293 cell line for the expression of viral vectors used in gene therapy, providing a reliable and scalable solution for the production of viral vectors.

- June 2024: MilliporeSigma launches the industry's first off-the-shelf cell culture media for perfusion processes, enabling biopharmaceutical companies to streamline their cell culture workflows and improve productivity.

Report Scope

Report Features Description Market Value (2023) USD 17.1 Billion Forecast Revenue (2033) USD 49.0 Billion CAGR (2024-2033) 11.4% Base Year for Estimation 2023 Historic Period 2018-2023 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Consumables (Media, Sera, Reagents, Buffers and Salts, Growth Factors and Cytokines, Others), Instruments (Bioreactors, Culture Systems, Centrifuges, Cell Counters, Others), Accessories), By Application (Biopharmaceutical Production, Cancer Research, Drug Screening and Development, Regenerative Medicine, Stem Cell Research, Vaccine Production, Others), By End User (Pharmaceutical and Biotechnology Companies, Research Institutes and Academic Institutes, Contract Research Organizations (CROs), Hospitals and Diagnostic Laboratories, Others) Regional Analysis North America - The US, Canada, & Mexico; Western Europe - Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe - Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC - China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America - Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa - Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Thermo Fisher Scientific Inc., Merck KGaA, Becton, Dickinson and Company, Corning Incorporated, Lonza Group Ltd., Eppendorf AG, Sartorius AG, GE Healthcare, PromoCell GmbH, HiMedia Laboratories, Irvine Scientific, Sigma-Aldrich Corporation, STEMCELL Technologies Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) -

-

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Becton, Dickinson and Company

- Corning Incorporated

- Lonza Group Ltd.

- Eppendorf AG

- Sartorius AG

- GE Healthcare

- PromoCell GmbH

- HiMedia Laboratories

- Irvine Scientific

- Sigma-Aldrich Corporation

- STEMCELL Technologies Inc.

Our Clients

View Our Licence Options